Fixed repayment financing offers predictable monthly payments, but it’s not for everyone. To decide if it’s a good fit for your business, consider these key factors:

- Revenue Stability: Your monthly revenue should be consistent, with fluctuations under 20%. Seasonal businesses or those with unpredictable sales may find fixed payments risky.

- Cash Flow Health: Ensure your net cash flow (inflows minus outflows) can cover fixed payments, even during slower months. Negative cash flow or long cash gaps can create challenges.

- Debt Service Coverage Ratio (DSCR): A DSCR above 1.25 is ideal, ensuring your income comfortably covers debt obligations.

- Operating Expenses: Account for inventory restocks, marketing costs, and other irregular expenses that could impact your ability to meet payments.

- Risk of Revenue Drops: Test repayment scenarios, including low-revenue months, to see if your business can handle fixed payments without draining reserves.

If your business has steady revenue, a strong DSCR, and manageable cash flow, fixed repayments can simplify budgeting. But if your sales are seasonal or unpredictable, flexible repayment options might be safer. Use tools like funding calculators and cash flow projections to make an informed decision.

Business Line of Credit vs. Term Loan: Which Is Better?

sbb-itb-d7b5115

Reviewing Your Monthly Revenue Stability

Before committing to fixed monthly payments, it’s crucial to confirm that your revenue can reliably support these obligations. This means digging into your sales history to spot patterns, including any dips or spikes. Understanding these trends will help you evaluate whether fixed repayments are a practical option, which will be explored further in the next sections.

Reviewing Sales Data Over 6–12 Months

Start by pulling detailed sales reports from your eCommerce platform - whether you’re using Shopify, Amazon, or accounting tools like QuickBooks. Focus on net revenue - the actual cash deposited after accounting for refunds, discounts, and taxes [4].

Ideally, your monthly net revenue should stay above $3,000 with fluctuations of less than 20%. For example, if your January revenue averages $10,000, you shouldn’t see drops below $8,000 or spikes above $12,000 in other months. Large variations like these could signal instability. Also, keep an eye on your refund rate - the percentage of purchases that are returned. High refund rates can unexpectedly eat into your revenue [2][4].

Metrics like Average Order Value (AOV) and customer retention rate are also worth monitoring. If AOV fluctuates wildly or retention rates are low, it could mean your revenue is too unpredictable for fixed repayments. A retention rate of around 35% or higher is a good sign since repeat customers help stabilize cash flow [5]. Remember, retaining an existing customer can cost up to 25 times less than acquiring a new one [3].

Mapping Seasonal Sales Variations

Seasonal trends are another key factor to consider. Many eCommerce businesses experience predictable highs and lows throughout the year. For instance, Black Friday and the holiday season often bring revenue surges, but these are often followed by slower months - like August, when vacations reduce shopping activity, or February, when post-holiday spending slows down [1].

To get a clear picture, review sales data spanning several years to identify both normal and peak revenue months. For example, January is often a challenging month for businesses after the December holiday rush. Onramp Funds describes this period as "still waters", where cash flow can become particularly strained [1]. If your slowest month generates only 50% of your average revenue, a fixed repayment plan that works in November might become unmanageable by February.

Mapping these seasonal patterns month by month can help you determine whether your cash flow remains steady enough to handle fixed payments year-round. If your revenue swings too much, fixed repayments might be too risky. These insights will guide you as you move into the next section, which focuses on calculating cash flow and operating expenses.

Calculating Cash Flow and Operating Expenses

Once you've assessed your revenue stability, the next step is to evaluate whether your operating cash flow reliably covers your fixed payment obligations. This means looking beyond profitability on paper and focusing on your net cash flow - the actual cash left after subtracting outflows from inflows over a given period [6]. This figure represents the money you have available to handle bills and other financial commitments.

A critical metric here is your operating cash flow, which reflects the funds generated from regular business activities like sales, payroll, and rent. It’s a strong indicator of whether your business can sustain itself without external funding [6]. Tools like QuickBooks and Xero can simplify this process by syncing with your bank accounts and providing real-time transaction data [9]. Keep in mind that cash flow issues are a major challenge for small businesses, with about 82% of them in the U.S. failing due to cash flow problems [8]. This analysis will also help you prepare for how irregular expenses might impact your cash reserves.

Calculating Net Cash Flow

Start by pulling detailed reports of all cash inflows (like sales and refunds) and outflows (such as supplier payments, payroll, shipping, and marketing costs). Subtract the total outflows from the inflows to determine your net cash flow [6]. For a more detailed picture, you can break this down into operating, investing, and financing categories [6].

It’s important to remember that profit doesn’t equal cash. Delayed payments from customers or inventory tied up in stock can significantly reduce your liquid funds [6].

"If your net cash flow is consistently negative, you'll eventually run out of money - regardless of how profitable you are on paper" [6].

This is why tracking the timing gap - the delay between paying suppliers and receiving payments from customers - is crucial [7].

Using a 13-week cash flow model can provide a clearer view of short-term liquidity risks [8]. Don’t forget to account for often-overlooked costs like merchant fees, fulfillment charges, or future inventory restocks when calculating outflows [8]. Most accounting tools, like QuickBooks or Xero, allow you to run "what-if" scenarios to see how a revenue drop of, say, 10% might affect your ability to meet fixed payments [7].

Accounting for Inventory and Marketing Expenses

Large, irregular expenses like inventory restocks or marketing campaigns can quickly drain your cash reserves, making it harder to meet fixed payment deadlines. To avoid surprises, include these significant costs in your cash flow forecast.

A great example comes from Bedford Park Rangers, a grassroots football club in the UK. In February 2026, they expanded from 12 to 23 teams and used Xero, combined with payment tools, to manage their cash flow. Chairman Jay Allison shared how automating payments and leveraging real-time reporting allowed them to monitor their funds closely, ensuring they stayed within spending limits [10]. This same approach applies to eCommerce businesses: knowing your available cash after accounting for major expenses can help you avoid overcommitting to fixed payments.

Leverage your accounting software to schedule large expenses and assess their impact on your projected cash balance. Tools like Xero and QuickBooks typically offer 30-day and 90-day cash flow projections based on historical data and upcoming bills [9]. You can also manually add hypothetical scenarios, such as a planned inventory purchase, to test how it might affect your ability to meet payments without altering your actual accounts [9]. These projections are essential for ensuring you can handle fixed repayments, even during periods of high spending.

Testing Repayment Scenarios

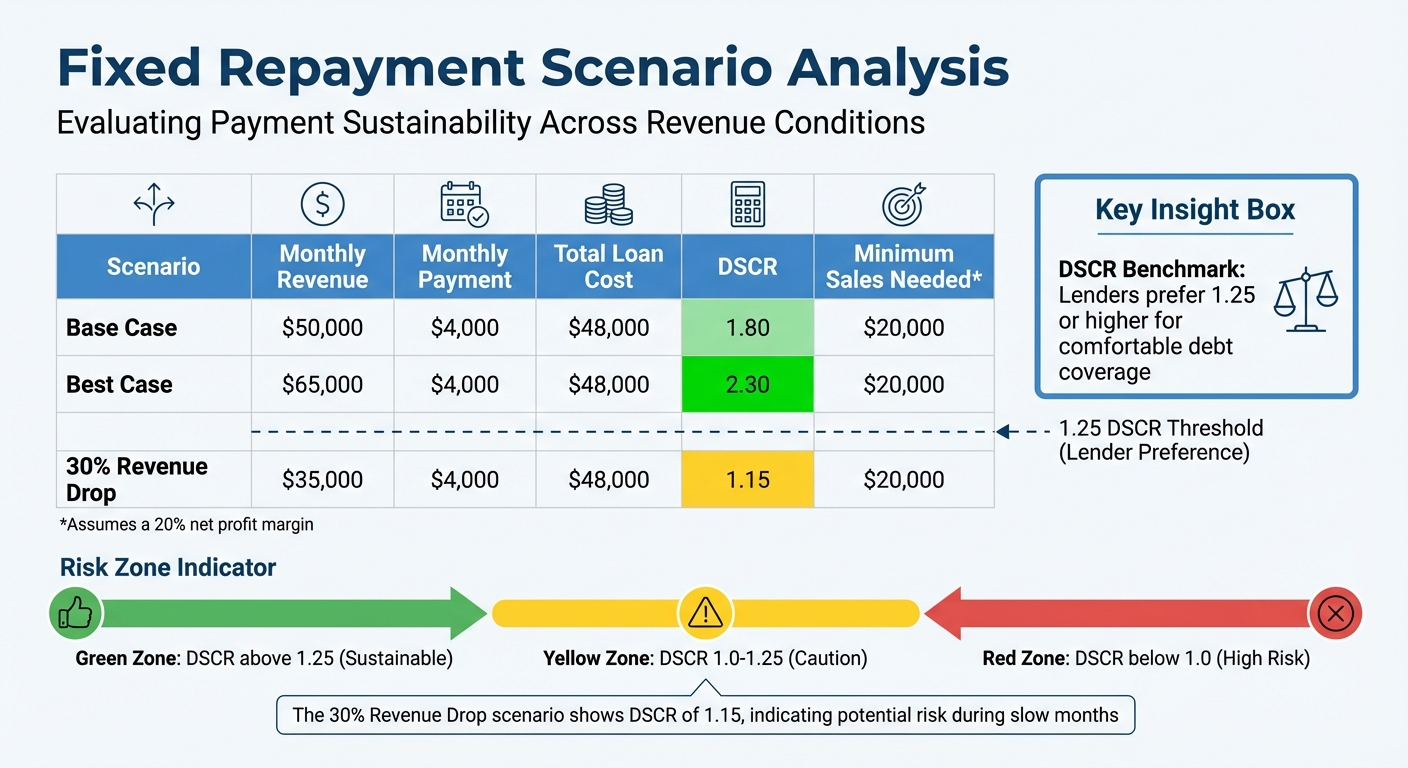

Fixed Repayment Readiness Assessment Table with Revenue Scenarios and DSCR Calculations

Once you've mapped out your cash flow and operating expenses, the next step is to test repayment scenarios. This means plugging in actual numbers to see if fixed payments fit within your budget without straining your cash reserves. It's a crucial step in determining whether a fixed repayment plan aligns with your financial situation.

Using a Funding Calculator

A funding calculator helps break down fee structures into an Annual Percentage Rate (APR), making it easier to understand the true cost of borrowing. To use it, input details like the loan amount, fixed fee, term, and any one-time fees. For instance, if you're looking at a $50,000 loan with a 1.2 factor rate, your total repayment would be $60,000. Spread over a 12-month term, this works out to a fixed monthly payment of $5,000.

Some calculators go further by factoring in monthly sales and growth rates to show how the loan impacts your cash flow. They often provide insights like the total repayment amount, effective APR, and risk zones. For example:

- Green Zone (Sustainable): APR under 20%

- Yellow Zone (Caution): APR between 21–49%

- Red Zone (High Risk): APR of 50% or higher [11].

This kind of breakdown helps you visualize and compare different borrowing scenarios more effectively.

Creating a Repayment Comparison Table

A repayment comparison table is another tool to assess how different loan amounts and fee structures affect your monthly obligations and sales requirements. Start by gathering the loan amount, fixed fee percentage, and repayment term. Use these to calculate the total repayment (principal × factor rate or principal + fixed fee) and divide it by the number of months to find your monthly payment [11][12].

From there, outline three revenue scenarios: Base Case, Best Case, and a 30% Drop. For each, calculate the Debt Service Coverage Ratio (DSCR), which measures whether your income comfortably covers debt payments. A DSCR above 1.0 means you can meet your obligations, but lenders often prefer a buffer, aiming for a DSCR of at least 1.25 [12][13]. To estimate the minimum sales needed, divide your fixed monthly payment by your net profit margin. For example, a $4,000 payment requires $20,000 in sales at a 20% profit margin.

| Scenario | Monthly Revenue | Monthly Payment | Total Loan Cost | DSCR | Minimum Sales Needed* |

|---|---|---|---|---|---|

| Base Case | $50,000 | $4,000 | $48,000 | 1.80 | $20,000 |

| Best Case | $65,000 | $4,000 | $48,000 | 2.30 | $20,000 |

| 30% Revenue Drop | $35,000 | $4,000 | $48,000 | 1.15 | $20,000 |

*Assumes a 20% net profit margin.

This table provides a clear view of whether fixed payments are manageable and highlights potential risks during lower revenue periods.

Testing Low-Revenue Months

It's essential to prepare for months when revenue dips, such as January or February after the holiday season. Adjust your revenue assumptions to reflect these periods and see if your cash reserves and DSCR can still handle the fixed payments [12][13].

A study conducted in March 2023 by Giorgia Barboni and P. Agarwal with 799 borrowers in Uttar Pradesh, India, revealed that businesses with unpredictable sales often preferred flexible repayment options, even at slightly higher rates (26% APR vs. 24% APR). Among those choosing flexibility, 56% used a "repayment holiday" during lean months like January and February. These businesses saw 16% higher sales after 8 months and 22% higher sales after 36 months, while maintaining a 90% on-time repayment rate [15].

"Waiting until the last minute to address your loan renewal can limit your options. Don't leave it entirely in your lender's hands - start the conversation at least three months in advance to stay ahead."

If your analysis shows that a significant revenue drop would push your DSCR below 1.25 or drain your cash reserves, it's a red flag. In such cases, postponing the loan until your cash flow improves or exploring flexible repayment options could be the smarter move.

Deciding If Fixed Repayment Works for Your Business

Take a close look at your cash flow and financial metrics to determine if fixed repayment is a good fit for your business. These insights will help you decide if this repayment model aligns with your financial situation.

Checklist for Fixed Repayment Readiness

Before committing to fixed repayment terms, make sure your business checks these boxes. These benchmarks build on earlier revenue insights and help gauge readiness. To start, your monthly sales should exceed $3,000 - a basic eligibility requirement for financing[16][19]. Additionally, you’ll need a Debt Service Coverage Ratio (DSCR) above 1.25, a gross profit margin of at least 45%, and a Customer Lifetime Value (CLV)-to-Customer Acquisition Cost (CAC) ratio of 3:1 or higher[16][17][18][19].

Pay special attention to your cash conversion cycle. If your cash gap stretches beyond 60 days, fixed repayments can become risky, even if your business is profitable[18].

"The longer the [cash] gap, the more cash you need to keep the business running. Many brands become profitable yet cash-poor due to a long cash gap."

- Graham Davies, Addition Finance[18]

Also, review your inventory turnover ratio and Day Sales Outstanding (DSO). A low inventory turnover could mean cash is tied up in unsold stock, while a high DSO may strain your working capital[16][18][19]. If your business experiences high refund and return rates, this could lead to unpredictable cash outflows, making it harder to meet fixed repayment obligations[17]. On top of that, many online retailers lose between 60% and 80% of their shopping carts, further complicating revenue predictability[17].

Once you’ve assessed these factors, weigh the benefits against potential risks to decide if fixed repayment is the right choice.

When to Choose (or Avoid) Fixed Repayment

Fixed repayment is a solid option for businesses with steady revenue and a DSCR that stays above 1.25 - even during slower months. It’s particularly suitable for businesses with strong gross margins, efficient cash cycles, and low churn rates[16][18][19].

However, it can be risky for businesses with seasonal or unpredictable sales. Revenue fluctuations can deplete cash reserves during slow periods, making fixed payments harder to manage. For example, payment fraud - responsible for over $40 billion in losses in 2022 and costing businesses about 3% of annual revenue[20][21] - can compound these challenges. Rigid payment schedules in such scenarios could lead to overdraft fees and mounting debt[22]. If your business faces irregular sales or high chargeback rates, it’s better to wait until your cash flow stabilizes before committing to fixed repayment terms.

If your analysis highlights vulnerabilities - like a DSCR dropping below 1.25 in slower months or cash gaps exceeding 60 days - consider postponing financing. Alternatively, explore flexible repayment options that adjust according to your sales performance[18][22]. This approach aligns with earlier findings about the challenges of seasonal revenue gaps and cash flow management.

Conclusion

Take a close look at your revenue trends from the past 6–12 months and calculate your net cash flow after covering operating expenses. Use repayment simulations with precise inputs - like loan amount, factor rate, payback period, and any one-time fees - to understand how fixed repayments could affect your margins during both busy and slower periods. Be mindful of potential risks, such as liquidity challenges or issues with loan performance, which could make it harder to meet fixed obligations[23]. These steps are essential for making informed financing decisions.

Leverage accounting tools and funding calculators to get a clearer picture of your financial health. These tools can break down complex fee structures into an Annual Percentage Rate (APR), making it easier to compare different funding options[11].

Run realistic growth scenarios to see how fixed repayments might impact your seasonal cash flow. If your analysis highlights financial vulnerabilities, it might be better to delay fixed repayment plans until your cash flow stabilizes. Keep external factors in mind, such as rising funding costs, inflation, and currency fluctuations, which could increase expenses and affect your creditworthiness[23]. Research shows that combining financial planning, smart investments, and proactive risk management explains 68.4% of the variance in business sustainability for small and medium enterprises[24]. This kind of analysis helps you determine whether fixed repayment is a good fit for your business.

Let your revenue data, cash flow evaluations, and repayment simulations guide your decision-making. The goal is to choose a financing model that supports your growth without putting unnecessary strain on your operations. This final review reinforces earlier points about the importance of revenue consistency and careful cash flow management.

FAQs

How much cash buffer should I keep before taking fixed payments?

It's often suggested to keep a cash reserve that covers 3 to 6 months of operating expenses before taking on fixed repayments. Why? This buffer helps you handle things like seasonal slowdowns, surprise expenses, or unpredictable cash flow. To figure out how much you need, take a close look at your essential monthly expenses and multiply that by 3 to 6. Having this financial cushion ensures you can manage fixed payments without putting unnecessary pressure on your business's finances.

What’s the fastest way to estimate my DSCR from my statements?

To estimate your Debt Service Coverage Ratio (DSCR) quickly, simply divide your net operating income (NOI) by your total debt service, which includes both principal and interest payments. This straightforward calculation relies on your current financial statements and skips the need for any complicated tools.

How do I stress-test fixed payments for my slowest month?

To test the resilience of fixed payments, try simulating a worst-case revenue scenario. Reduce your monthly income by 30-50% to mirror what might happen during your slowest month. Then, update your cash flow forecast to account for this lower income, along with your fixed expenses and repayment obligations. The goal is to see if your cash flow can still handle those payments. Cash flow forecasting tools can help you model these scenarios and assess whether your business can manage fixed repayments during tough times.