Fixed monthly loan payments can harm eCommerce businesses with unpredictable sales cycles. A low-interest loan might seem appealing, but rigid repayment schedules can drain cash reserves during slow periods. Instead, financing options tied to revenue offer flexible solutions that adjust payments based on sales performance. This approach helps businesses maintain cash flow, seize growth opportunities, and avoid financial strain.

Key insights:

- Revenue-based financing adjusts payments to sales, reducing repayment amounts during slow months and increasing them during strong months.

- Fixed-payment loans, even with low rates, can create cash flow challenges for seasonal businesses or those with fluctuating revenue.

- Flexible repayment models allow sellers to invest in inventory and marketing without risking operational stability.

For eCommerce sellers, aligning financing with sales performance ensures resources are available when needed most, even if the overall cost is slightly higher.

Finding the Right Capital: Revenue-Based Financing Explained

sbb-itb-d7b5115

Problems with Low-Cost, Fixed-Payment Loans

In the world of eCommerce, financial inflexibility can often magnify existing cash flow struggles, creating additional hurdles for businesses.

Fixed Payments Create Cash Flow Problems

Even loans with low interest rates can become problematic if fixed payments eat into reserves during slow sales periods. The issue arises when these rigid payments clash with the unpredictable nature of revenue. As Oliver Whelan, Chief Revenue Officer at Storfund, explains:

"If you take speculative financing on the basis that you are going to spend that money on marketing and quadruple your sales... and that does not come through, ultimately you've eaten away margin without seeing the return or the benefit of that financing" [1].

In situations where expected sales growth doesn’t materialize, businesses are left with shrinking margins and less working capital to manage daily operations. This rigidity can strain operations and limit the flexibility needed to adapt during periods of reduced revenue.

Inflexible Loans Don't Match Revenue Fluctuations

Fixed-payment loans are especially challenging for eCommerce businesses that deal with seasonal sales cycles or fluctuating revenue streams. During peak seasons, operational costs often rise, but revenue may not align immediately. Fixed repayments remain constant regardless of these shifts, forcing businesses to stretch their resources thin.

This lack of alignment can leave businesses facing tough choices: meeting loan obligations or capitalizing on growth opportunities, like buying inventory in bulk or increasing marketing efforts when costs are lower. In many cases, the inability to redirect funds due to rigid repayment terms can cost more in missed opportunities than opting for a financing option with slightly higher fees but greater flexibility [2][3].

Flexible Repayment Options for eCommerce Businesses

How Revenue-Based Financing Works

Revenue-based financing offers a repayment model that adjusts with your sales. Instead of committing to fixed monthly payments, you repay a set percentage of your revenue until the total amount (principal plus a flat fee) is paid off. For example, a $100,000 advance with a 6% fee means you'll repay $106,000 in total. Payments are typically deducted daily or weekly, slowing down when sales are lower and speeding up when sales increase. This approach eliminates the need for compounding interest, personal guarantees, or collateral, making it straightforward and tied to your business's performance.

Onramp Funds' Financing Features

Onramp Funds takes this flexible model and customizes it for eCommerce businesses. They provide revenue-based financing with funding available within 24 hours of approval. Their platform connects directly to major sales channels like Shopify, Amazon, WooCommerce, BigCommerce, Walmart Marketplace, and TikTok Shop. Repayments are automatically deducted as a percentage of your daily or weekly revenue, adjusting naturally to reflect your sales trends.

The fee structure is simple and predictable, ranging from 2% to 8%. For instance, borrowing $50,000 with a 6% fee means you’ll repay $53,000, regardless of how long it takes. Onramp Funds evaluates eligibility based on your business's performance rather than personal credit scores. By reviewing as little as 90 days of sales data from your connected platforms, they can determine your qualification. Businesses generating at least $3,000 in monthly sales typically qualify. Additionally, if you sell across multiple platforms, your combined revenue can help you access higher funding limits, offering more opportunities for growth.

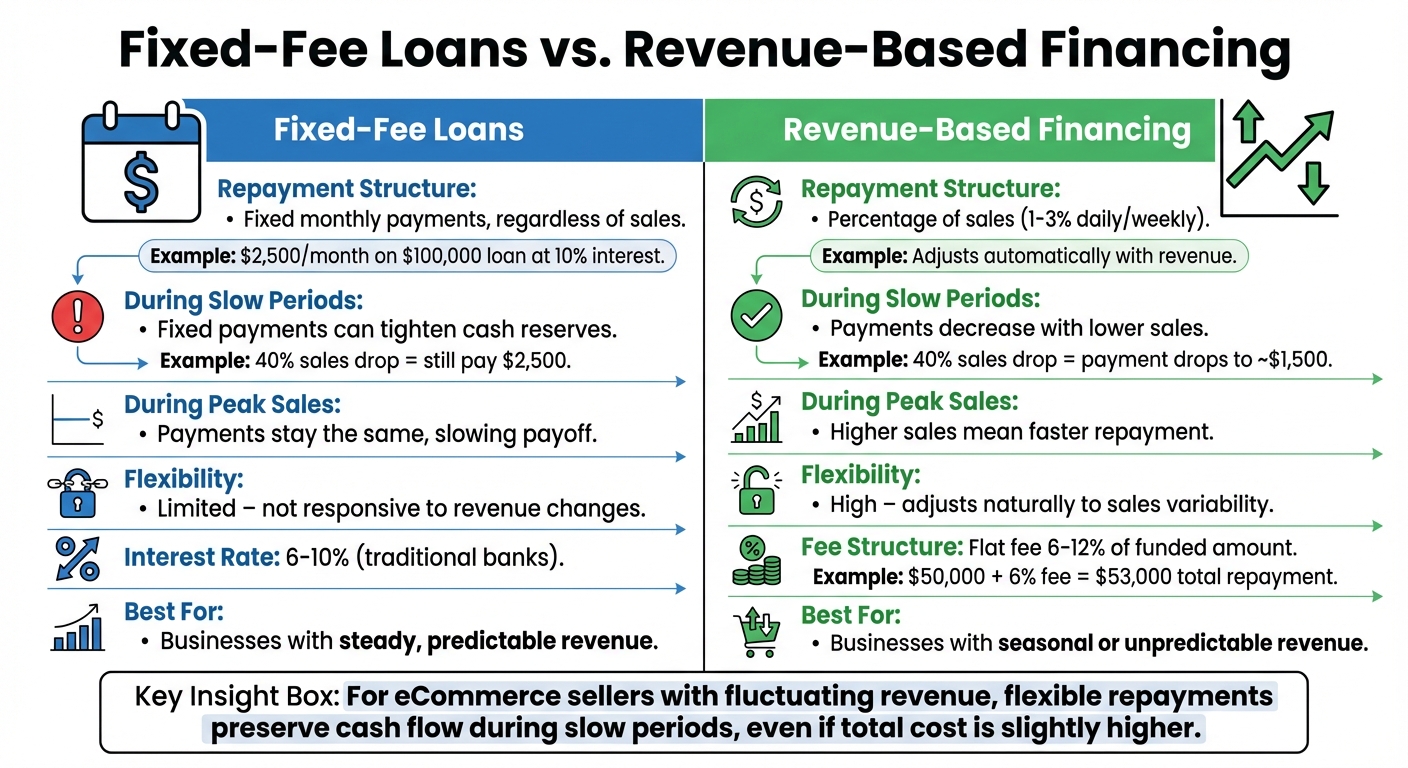

Fixed-Fee Loans vs. Revenue-Based Financing

Fixed-Fee Loans vs Revenue-Based Financing Comparison for eCommerce

Repayment Models and Cash Flow Effects

When comparing these two financing options, the repayment structure and its impact on cash flow stand out. Fixed-fee loans require the same monthly payment, no matter how your sales perform. For instance, borrowing $100,000 with a traditional loan at 10% interest might mean paying about $2,500 every month for the entire term. This consistency can be challenging for eCommerce businesses that experience fluctuating revenues. Whether your monthly sales are $50,000 or $200,000, that $2,500 payment remains the same.

On the other hand, revenue-based financing ties repayments to your actual sales - usually taking 1%–3% of daily or weekly revenue. For example, if your sales drop by 40% after the holidays, a fixed-fee loan would still demand the full $2,500 monthly payment, potentially straining your finances. With revenue-based financing, your payment would decrease proportionally (perhaps to around $1,500), leaving more cash available for essential needs like advertising or inventory restocking. This flexibility can make a significant difference in managing cash flow during slow sales periods.

| Aspect | Fixed-Fee Loans | Revenue-Based Financing |

|---|---|---|

| Repayment Structure | Fixed monthly payments, regardless of sales | Percentage of sales (1–3% daily/weekly) |

| During Slow Periods | Fixed payments can tighten cash reserves | Payments decrease with lower sales |

| During Peak Sales | Payments stay the same, slowing payoff | Higher sales mean faster repayment |

| Flexibility | Limited – not responsive to revenue changes | High – adjusts naturally to sales variability |

Cost Predictability vs. Payment Flexibility

The choice between these options often comes down to predictability versus flexibility. Fixed-fee loans provide predictable monthly payments, making it easier to plan budgets. These loans, often offered by traditional banks, typically carry interest rates between 6% and 10%. This structure works well for businesses with steady, reliable revenue streams.

In contrast, revenue-based financing emphasizes flexibility. It charges a flat fee - usually 6%–12% of the funded amount - so you know the total repayment amount upfront. For example, a $50,000 advance with a 6% fee would result in a total repayment of $53,000. However, the actual monthly payments vary based on your sales. During high-revenue months, you'll pay more and finish repaying faster. In slower months, payments shrink, aligning with your cash flow.

For businesses with seasonal or unpredictable revenue, this adaptable repayment model can preserve cash reserves and support ongoing operations, even if the total cost is slightly higher. This flexibility can be particularly valuable for eCommerce sellers who face significant revenue swings throughout the year[4].

Examples of Flexible Financing in Practice

Funding Seasonal Inventory and Marketing

Seasonal eCommerce businesses often face a tricky timing gap: they need to pay for inventory upfront, but their revenue only peaks later in the season. Revenue-based financing offers a way to bridge this gap without the stress of fixed payment schedules. For instance, imagine a seller gearing up for the holiday rush who secures $100,000 with a flat 6% fee. Their total repayment would be $106,000, but the beauty of this setup is that repayments rise and fall with revenue. When sales spike, repayments increase; when sales dip, payments adjust, helping to maintain steady cash flow.

This flexibility also extends to marketing campaigns. Sellers can use revenue-based financing to test ads without worrying about rigid monthly payments. If an ad campaign underperforms early on, repayments automatically decrease in line with reduced sales. This adaptability prevents the frustrating "stop-start" issue, where cash shortages force sellers to pause campaigns, potentially harming ad performance and momentum[3].

Handling Variable Sales Periods

Flexible financing isn't just for peak seasons - it’s a lifeline during everyday ups and downs in revenue. For example, a seller might see a 40% drop in sales after the holidays. With a traditional loan, they'd still owe the same fixed monthly payment, regardless of their reduced income. Revenue-based financing, on the other hand, ties repayments to weekly sales. During slower periods, payments shrink, easing the pressure on cash flow.

This approach also works well for sellers managing inventory cycles. Instead of taking one large loan, many sellers prefer to draw smaller amounts throughout the quarter as needed. This strategy aligns funding with stock requirements, offering more control and flexibility over their finances[3].

Conclusion

Key Points for eCommerce Sellers

Fixed payment plans can put a strain on your cash reserves, especially during slower sales periods. For businesses with unpredictable sales cycles, choosing a financing option that adapts to your revenue can be more practical than chasing small cost savings. Revenue-based financing ties repayments to your actual sales - often around 1–3% of weekly revenue[3][4] - so when sales dip, your repayment amount decreases as well. This flexibility can provide much-needed relief during off-seasons and help you avoid the cash flow issues that fixed-payment loans often create.

If your business experiences seasonal fluctuations - like an outdoor furniture seller navigating slow winter months - or if you're experimenting with new marketing strategies, it's crucial to align your financing with your sales performance. Opt for options that adjust dynamically instead of locking you into rigid monthly payments[5][6]. Look for features such as quick approval times (usually within 1–2 days), flat fees (typically 6–12%), and no personal guarantees. These elements can give you the flexibility to capitalize on growth opportunities without putting your personal assets at risk[3][4][7].

Flexible financing can be a game-changer for sustainable growth. It allows you to invest in inventory and marketing when needed while automatically reducing repayment pressure during slower times[5][6][4]. This approach helps you avoid the "stop-start" cycle, where cash shortages force you to halt campaigns or delay inventory purchases. Interruptions like these can disrupt your momentum and hurt your ad performance over time[3].

FAQs

When is flexible repayment worth a higher fee?

Flexible repayment options can justify a higher fee if they help manage cash flow during unpredictable sales periods, such as seasonal highs or lows. By syncing repayment terms with your business's revenue cycles, this approach eases financial pressure, allowing for smoother day-to-day operations and more adaptable financial planning.

How do revenue-based payments affect my cash flow in slow months?

Revenue-based payments align with your sales, offering relief during slower months. Instead of committing to fixed amounts, you pay a set percentage of your revenue - usually between 2% and 8%. If your sales dip, your payments shrink accordingly, easing financial pressure. This setup allows you to better manage cash flow, handle seasonal fluctuations, and keep resources available for critical expenses like inventory and marketing, all without the stress of rigid payment commitments.

What sales history is required to qualify for revenue-based financing?

To qualify, your business should have consistent monthly sales ranging from $10,000 to $20,000, at least 6 months of operating history, and gross margins of 30% or higher. These requirements are designed to ensure your business is in a solid position to handle this type of financing.