Running an eCommerce business means managing unpredictable cash flow. Fixed repayment loans can create financial strain during slow sales months, especially for businesses with seasonal revenue swings. Variable repayment, however, adjusts payments based on your sales, offering flexibility to manage cash flow more efficiently. Here’s why this approach works:

- Fixed Payments: Require the same amount monthly, regardless of revenue. This can strain cash flow during low-sales periods, limiting funds for inventory and marketing.

- Variable Repayments: Payments are a percentage of monthly sales (e.g., 10%), automatically decreasing during slow months and increasing during high-sales periods. This aligns repayment with revenue, easing financial pressure.

For eCommerce businesses, variable repayment can help manage seasonal cycles, handle revenue drops, and fund growth opportunities without locking up essential cash. Onramp Funds offers a solution tailored to eCommerce platforms, using real-time sales data for funding and repayment adjustments. Payments are tied to daily sales, ensuring businesses maintain cash flow flexibility while focusing on growth.

Fixed vs Variable Repayment: Cash Flow Impact Comparison for eCommerce

How To Fund Your Ecommerce Business For Cheap (Or Even Free)

sbb-itb-d7b5115

Why Fixed Payment Models Strain eCommerce Cash Flow

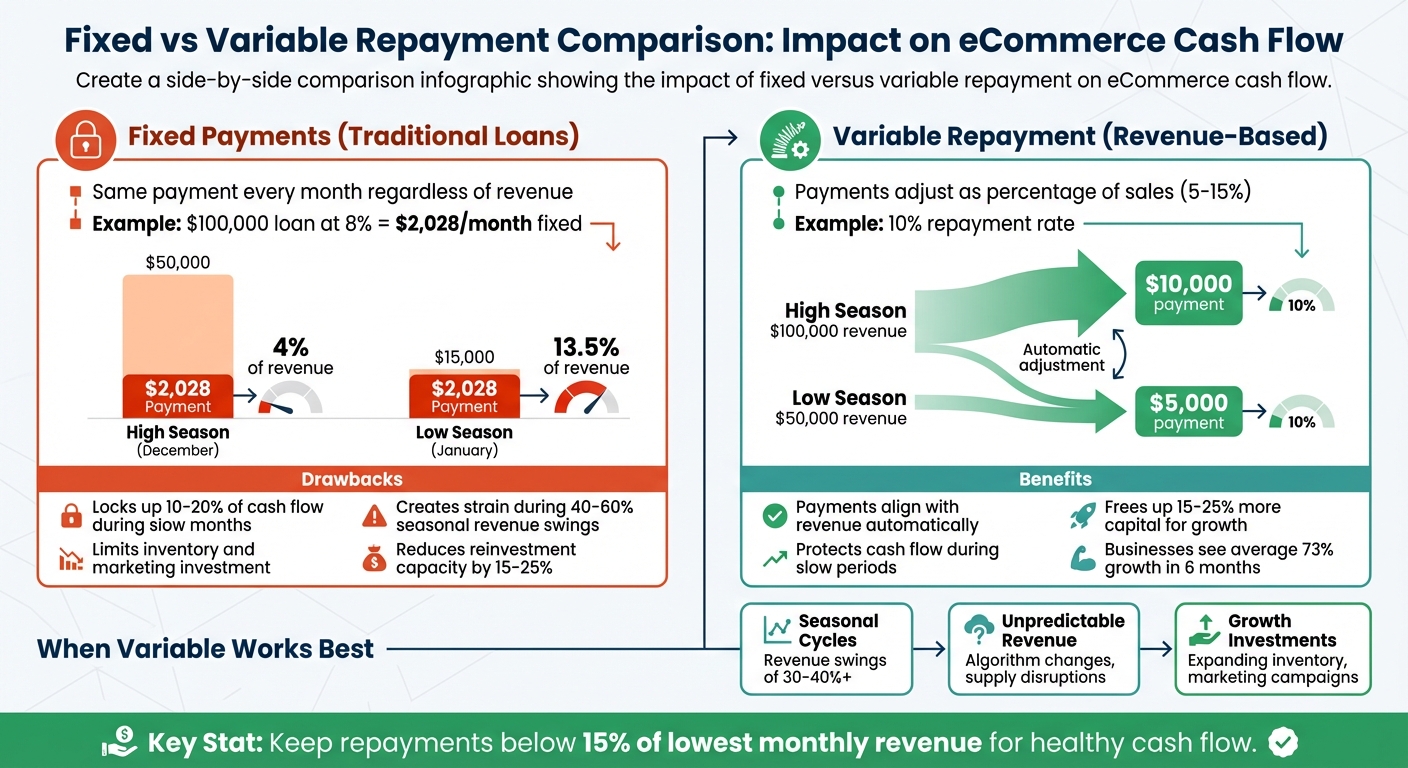

Fixed payment models can feel like a reliable choice at first glance, but they often clash with the unpredictable nature of eCommerce sales. These loans function much like a traditional mortgage - you owe the same amount every month, regardless of how your revenue performs. For example, if you take out a $100,000 loan at an 8% fixed rate over five years, you're looking at a $2,028 monthly payment [1]. While that predictability might seem reassuring, it becomes a challenge when your sales fluctuate.

Fixed Payments During Seasonal Revenue Drops

Seasonal sales dips are where fixed payments really start to pinch. Picture this: you run a holiday-focused eCommerce store and borrow $100,000 at an 8% rate to stock up on inventory. During the holiday rush, you’re pulling in $50,000 a month, so the $2,028 payment is just 4% of your revenue. But come January and February, when sales drop to $15,000, that same payment suddenly eats up 13.5% of your revenue [1]. The payment stays constant, but its impact on your cash flow multiplies dramatically.

This imbalance puts you in a tough spot. You might have to dip into savings just to meet the payment, or delay paying suppliers to stay afloat. Many eCommerce businesses experience seasonal revenue swings of 40-60%, with post-holiday slumps being especially brutal [4]. The rigid nature of fixed payments leaves little room for flexibility, making it harder to navigate these slower months.

Reduced Ability to Invest in Inventory and Marketing

Another major drawback of fixed payments is how they limit your ability to reinvest in your business. Let’s say your monthly revenue drops to $20,000 during a slow period, and over 10% of that is immediately tied up in loan payments [1][3]. That leaves less cash for restocking inventory ahead of peak seasons or launching marketing campaigns to boost sales.

Marketing, in particular, takes a hit. With 10-20% of your cash flow locked into fixed payments, it’s harder to react quickly to market trends or outmaneuver competitors. Yet, marketing is crucial - studies show it can drive 20-30% sales growth for eCommerce businesses [3]. This creates a frustrating cycle: low revenue limits your marketing budget, which in turn stifles growth, making those fixed payments feel even heavier. It’s a clear example of why repayment models that adapt to your revenue are better suited for eCommerce businesses.

How Variable Repayment Works with eCommerce Revenue Patterns

Variable repayment ties your payments directly to your monthly sales, requiring a percentage - usually between 5% and 15% - of your revenue instead of a fixed amount. This setup means higher payments during strong sales months and lower payments when sales slow, easing cash flow pressures.

Payments That Adjust with Revenue

Here’s an example: with a 10% repayment rate, if your eCommerce business earns $100,000 in a month, your payment would be $10,000. But if sales drop to $50,000 the next month, your payment automatically decreases to $5,000. Unlike fixed repayment plans that demand the same amount regardless of how well your business performs, variable repayment adjusts to your sales. This flexibility helps protect your cash flow during slower periods. It’s also particularly useful for businesses with fluctuating revenue, like those affected by seasonal trends.

Tailoring Payments to Seasonal Sales Patterns

Variable repayment is especially effective for businesses with seasonal revenue swings. For instance, during high-revenue periods like Q4, when holiday shopping can boost sales by 50–200%, your payments increase proportionally. At a 12% repayment rate, $300,000 in December sales would mean a $36,000 payment [4]. On the flip side, during slower months like January or February, when sales might dip to $80,000, that same percentage would result in a much smaller $9,600 payment.

This system automatically aligns your financial obligations with your revenue flow, which is crucial for eCommerce businesses where income can vary dramatically. For example, Black Friday might bring a surge in sales, but quieter months often follow. With variable repayment, you can pay more during high-revenue periods and conserve cash during slower times, leaving more funds available for essentials like inventory and marketing [4].

When Variable Repayment Works Better Than Fixed Payments

Variable repayment isn’t a one-size-fits-all solution, but it can be a game-changer for businesses with fluctuating revenue. Knowing when to opt for variable repayment can help you maintain smoother operations and avoid cash flow headaches.

Handling Seasonal Sales Cycles

For eCommerce businesses with clear seasonal sales patterns, variable repayment is a natural fit. Since payments are tied to your revenue - usually between 5% and 10% of monthly sales - this model adjusts automatically. During slower months, your payments decrease, leaving more cash available for essentials like payroll or restocking inventory. Fixed repayment schedules, on the other hand, can strain your finances during these off-peak periods, making variable repayment a more flexible option for managing seasonal ups and downs.

Dealing with Unpredictable Revenue Changes

Revenue can take a sudden hit due to factors like algorithm shifts or supply chain disruptions. Fixed payments remain constant, even when income drops, which can create serious financial stress. Variable repayment adjusts to your current revenue, offering relief when sales decline. For example, if your revenue falls by 30%, your repayment decreases proportionally, helping you manage cash flow without sacrificing critical operations [1]. This approach not only helps you weather volatility but also ensures you have resources to focus on growth opportunities.

Funding Growth Investments

When you’re channeling funds into growth - whether it’s for expanding inventory, launching a big marketing campaign, or developing new products - fixed payments can feel restrictive. They might force you to choose between paying off loans and investing in your business. Variable repayment, however, adapts to your revenue, reducing payments during leaner periods and freeing up cash for these growth initiatives. This flexibility is especially useful for businesses with longer cash conversion cycles, where supplier payments often come before customer payments. By aligning repayment with revenue, this model supports both your day-to-day needs and long-term goals.

How Onramp Funds' Revenue-Based Financing Works

Onramp Funds provides a financing option tailored for eCommerce businesses operating on platforms like Amazon, Shopify, Walmart Marketplace, and TikTok Shop. This model uses real-time sales data to determine funding, bypassing the need for traditional credit scores or lengthy business histories. Instead, funding decisions are based on how your business is performing right now.

Repayment as a Percentage of Sales

Repayments with Onramp Funds are tied to a fixed percentage of your daily sales. This means payments automatically adjust to match your cash flow. When sales are booming, payments increase; when sales slow down, payments decrease. This flexibility ensures you’re never stuck with rigid monthly bills that don’t reflect your revenue. Plus, the model is non-dilutive, so you retain full ownership of your business, and most businesses won’t need to offer personal guarantees.

Instead of traditional interest rates, Onramp charges a fixed fee. This keeps your total repayment cost predictable, no matter how quickly you pay back the advance[8][9]. This transparency makes financial planning easier and eliminates the worry of mounting interest. Businesses that secure funding through Onramp typically see an average growth of 73% within six months[9]. Why? Because they can invest in critical areas like inventory, fulfillment, and advertising without cash flow concerns. It’s a system designed to grow with your business, offering flexibility and clarity.

Fast Funding with Clear Terms

The application process is quick and straightforward. Simply connect your eCommerce storefront to Onramp’s portal, and the platform analyzes your sales data in real time[7]. You can receive funding in as little as 24 hours. Pricing is clear and upfront - no hidden fees. As Eric Youngstrom, CEO of Onramp Funds, puts it:

"Onramp's AI lending tools instantly match cash needs with eCommerce and retail supply chain and inventory cycles, ensuring business owners have the capital they need to grow their businesses"[9].

To qualify, your business must generate at least $3,000 in monthly sales. Onramp integrates seamlessly with major eCommerce platforms, automatically pulling sales data to adjust repayments without requiring manual input. This hands-off system lets you focus on running your business while repayments adjust naturally based on your actual performance.

How to Evaluate and Implement Variable Repayment

Analyzing Your Cash Flow Patterns

Start by pulling 12–24 months of sales data to get a clear picture of your revenue trends. Look for patterns, such as peak seasons and slower periods. For example, if you sell winter apparel, you might notice a 200% revenue spike in November and December, followed by a 35% dip in February. Use accounting tools to compare your monthly cash inflows against your expenses to identify these trends[11].

Next, break down your expenses into two categories: fixed costs (like rent and salaries) and variable costs (such as ad spend and fulfillment fees)[11]. To measure how much your cash flow fluctuates, calculate the standard deviation of your net monthly cash flow. If the volatility exceeds 20–30% of your average revenue, variable repayment may be a better fit than fixed payments[1][2]. Why? Fixed payments can eat up 15–20% of your cash during slower months, leaving you with limited funds for essentials like inventory or marketing.

To make this analysis actionable, create a spreadsheet to compare repayment scenarios. Use your sales data to simulate how fixed and variable repayments would impact your cash flow. This exercise not only highlights your cash flow trends but also ensures that your repayment plan aligns with your business cycles.

Finally, take these insights a step further by running them through a funding calculator to model different repayment scenarios.

Using Onramp Funds' Funding Calculator

Once you’ve mapped out your cash flow, use Onramp Funds’ funding calculator to refine your repayment strategy. This tool connects directly to your eCommerce platform - whether it’s Shopify, Amazon, Walmart Marketplace, or TikTok Shop - to pull in your average monthly revenue. From there, you can input your funding needs (e.g., $50,000) and see how daily-sales-based repayments would look[10].

The calculator provides a clear breakdown of total repayment and adjusts payments based on changes in revenue. For instance, if your average monthly sales are $200,000 and you set a 10% repayment rate, your monthly payment would be around $4,167 at that average. But if sales drop by 30% during a slow season, your payment would decrease to $2,800 - offering much-needed flexibility compared to a fixed $4,500 payment, which could strain your cash reserves[2].

You can also test different scenarios, such as optimistic (+25%) or pessimistic (–30%) sales projections. This approach helps ensure your repayment plan stays manageable even during downturns. As a rule of thumb, keep your projected repayments below 15% of your lowest monthly revenue to maintain healthy cash flow[1][5].

Conclusion

Variable repayment models offer eCommerce businesses a way to align financing with fluctuating revenue. Unlike fixed payment plans that demand a set monthly amount regardless of sales performance, variable repayment adjusts based on your cash flow. This flexibility helps protect your working capital during slower sales periods and scales repayments as revenue grows, creating a more adaptable approach to managing finances [1][2].

When considering variable repayment, think about your revenue patterns, cash reserves, and growth objectives. For businesses experiencing revenue swings of 30–40%, tying repayments to income can help preserve cash reserves [1]. Additionally, maintaining 3–6 months of operating expenses in reserve can provide a buffer against payment fluctuations [6]. If you're focused on growth - like expanding inventory or launching marketing campaigns - variable repayment models can free up 15–25% more capital for reinvestment compared to fixed payment plans.

To make informed decisions, use tools to simulate repayment scenarios. By analyzing historical cash flow and testing different repayment structures, you can see how variable repayment impacts your business during both strong and weak sales periods. Onramp Funds' funding calculator is a practical resource for this type of analysis.

Onramp Funds also simplifies access to revenue-based financing. Their platform connects directly to your eCommerce store - whether you sell on Shopify, Amazon, Walmart Marketplace, or TikTok Shop - and provides funding within 24 hours, with clear fees ranging from 2–8% [10].

FAQs

Is variable repayment more expensive than fixed payments?

Variable repayment models can actually be a smart choice for businesses with fluctuating revenue, as they aren't automatically pricier than fixed payments. Here's why: with variable repayments, your payments adjust according to your sales. This means during slower months, your payments shrink, easing financial pressure. On the flip side, when business is booming, payments increase proportionally.

In contrast, fixed payments stay the same no matter how your revenue shifts. This predictability can be a challenge if your cash flow takes a hit during a downturn. Ultimately, whether a variable model is more cost-effective depends entirely on your business's revenue patterns and how you manage your cash flow.

What happens to my payment if sales drop suddenly?

If your sales take a hit, a revenue-based financing model adjusts your payments automatically because they’re linked to your current sales revenue. This means during slower times, your repayment amount decreases, giving you breathing room to manage cash flow without the stress of fixed payment obligations.

How do I know what repayment percentage is safe for my cash flow?

A good repayment percentage largely depends on how your revenue flows and what your operating costs look like. Generally, setting aside 2% to 8% of your sales for repayments tends to be a manageable range. This approach lets you adjust payments as your revenue rises or dips.

To figure out what works best for you, take a close look at your average monthly sales and any seasonal trends that might affect your income. Make sure the repayment plan won’t strain your finances during slower months. By keeping an eye on your sales data regularly, you can stay flexible and ensure your cash flow covers both your repayments and day-to-day business expenses.