When choosing financing, focusing solely on the advertised interest rate can lead to cash flow challenges. The repayment structure - how and when you pay - often has a bigger impact on your business. Fixed monthly payments can strain businesses during slow sales periods, especially for seasonal sellers. Revenue-based repayments, tied to a percentage of your sales, adjust automatically with your income, providing more flexibility to manage cash flow effectively.

Key Takeaways:

- Fixed payments are predictable but rigid, causing cash flow pressure during slow months.

- Revenue-based repayments adjust with sales, offering relief during downturns.

- Seasonal businesses and those with variable sales benefit from repayment terms that align with their revenue patterns.

For eCommerce sellers, choosing financing that matches your sales trends and cash flow needs is critical to maintaining stability and growth.

Why Headline Costs Don't Tell the Full Story

How Low Rates Can Hide the Real Cost

A low advertised rate might look appealing, but it often hides costs that can disrupt your cash flow. The real expense isn’t just about the percentage - it’s about how repayment terms impact your daily operations.

Take, for example, a $100,000 loan with a 9% fixed fee, repaid over six months in equal installments. At first glance, the fee seems reasonable. However, when you factor in the repayment structure, the effective APR balloons to 44.1%[6]. Why? Because you’re paying back the principal in chunks while the fee is charged upfront.

Justin Sherlock, Head of Flexport Capital, explains it plainly:

"The faster this fixed fee loan is paid back, the higher the effective rate is because the interest is being 'pre-paid' upfront, regardless of how long the principal is kept."[6]

This repayment structure essentially treats each installment like a mini-loan, where early payments carry the full weight of the fixed fee. Unlike traditional loans, where paying off early can save on interest, fixed-fee loans do the opposite - speeding up repayment increases the effective APR.

On top of that, fixed-fee loans come with rigid repayment schedules that don’t flex with your cash flow. If your sales take a hit during a slow period, you’re still stuck with the same fixed payment. This can squeeze your working capital, leaving less money for critical needs like inventory or advertising[4]. It’s a clear example of how focusing solely on the rate can overlook the broader impact on your finances.

The Challenge for Seasonal and Variable Sales

For businesses with seasonal or fluctuating sales, the hidden costs of fixed-fee loans become even more problematic. Many eCommerce companies experience revenue spikes during peak seasons but face steep declines in off-peak months. Fixed repayment terms don’t adjust to these natural cycles, creating cash flow headaches.

When sales slow down, rigid monthly payments can leave you scrambling to cover costs. This might mean cutting back on marketing or delaying inventory purchases, which could hurt your ability to bounce back. Worse, it could prevent you from jumping on opportunities like bulk discounts or viral trends[4].

Paul Voge, Co-founder and CEO of Aura Bora, knows this struggle well. In 2020, his beverage company used financing with extended payment terms and higher credit limits to manage the gap between production costs and customer payments. Reflecting on the experience, he said:

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital."[4]

This kind of flexibility is critical for businesses that face delayed customer payments - often stretching 60 to 180 days - while suppliers demand payment upfront. Fixed repayment schedules during these periods only make cash flow issues worse. It’s a reminder of why financing should align with your sales patterns, not work against them.

Amazon FBA loans VS revenue based financing

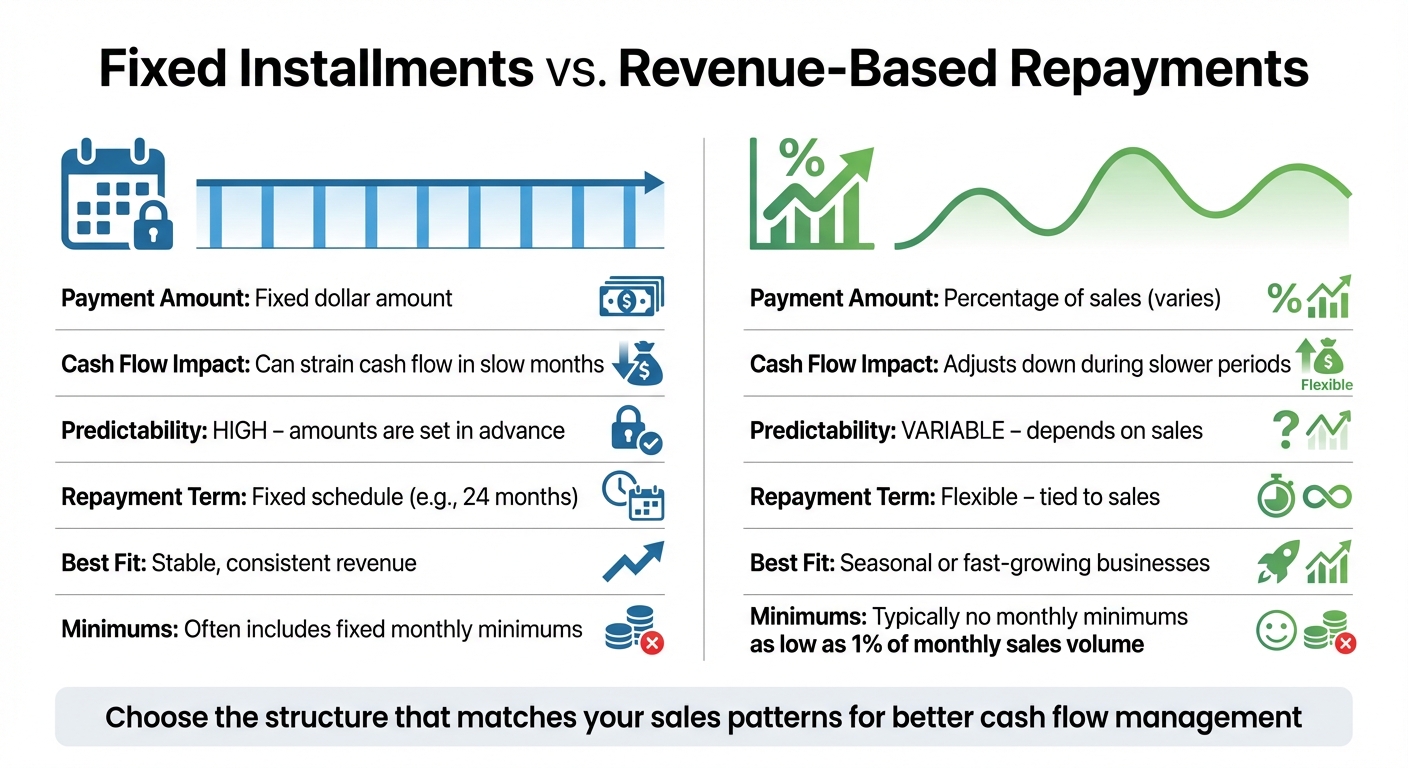

Fixed Installments vs. Revenue-Based Repayments

Fixed vs Revenue-Based Repayment Structures for eCommerce Financing

Fixed Installments: Predictable but Rigid

Fixed installment repayments require you to pay the same dollar amount at regular intervals, no matter how your sales are performing [2]. This setup is great for planning since you always know the exact amount due, the interest rate stays the same, and there's a clear end date for paying off the debt.

But this predictability can come with challenges. If your sales dip - maybe due to seasonality, underperforming ads, or inventory issues - you’re still on the hook for the full payment. That can put a strain on your cash flow during slower periods, potentially forcing you to cut back on other critical expenses. For eCommerce sellers dealing with fluctuating revenue, fixed payments can feel like a financial squeeze. On the other hand, revenue-based repayments offer more breathing room by adjusting based on your earnings.

Revenue-Based Repayments: Flexible and Sales-Driven

Unlike fixed installments, revenue-based repayments change with your sales. Instead of a set dollar amount, you pay a fixed percentage of your daily or monthly revenue [1]. If your sales spike, your payment goes up; if they slow down, your payment automatically decreases. This repayment model continues until the full amount is paid off, without a fixed timeline or minimum monthly payment.

This flexibility is a lifesaver for managing cash flow during slower times. Payments shrink when revenue dips, making it easier to keep your business running smoothly. In fact, repayment percentages can be as low as 1% of your monthly sales volume [2], ensuring payments remain manageable. For businesses with seasonal sales or those selling across multiple platforms, this adaptability can make a big difference.

Side-by-Side Comparison

| Feature | Fixed Installments | Revenue-Based Repayments |

|---|---|---|

| Payment Amount | Fixed dollar amount | Percentage of sales (varies) |

| Cash Flow Impact | Can strain cash flow in slow months | Adjusts down during slower periods |

| Predictability | High – amounts are set in advance | Variable – depends on sales |

| Repayment Term | Fixed schedule (e.g., 24 months) | Flexible – tied to sales |

| Best Fit | Stable, consistent revenue | Seasonal or fast-growing businesses |

| Minimums | Often includes fixed monthly minimums | Typically no monthly minimums |

sbb-itb-d7b5115

How Onramp Funds Supports eCommerce Sellers

Onramp Funds offers a financing solution that aligns perfectly with the ups and downs of your sales cycle, making it easier for eCommerce sellers to manage their cash flow.

Repayments That Adjust to Your Sales

Onramp Funds takes a revenue-based approach to repayments, setting them as a percentage of daily sales - starting as low as 1% [2]. This means your payments naturally rise when your sales are booming and decrease during slower periods, giving you the flexibility to maintain stability even during off-seasons.

By connecting with all your sales channels - whether it’s Amazon, Shopify, TikTok Shop, Walmart, or others - Onramp gets a complete view of your overall business performance [1]. This comprehensive data ensures that your funding limits and repayment terms reflect your total revenue, not just the performance of one platform. Thanks to this approach, businesses working with Onramp report an average revenue growth of 60%, and 75% of customers return for additional funding [2].

This flexibility is paired with a straightforward, transparent fee structure.

No Surprises: Transparent Fee Structure

Onramp charges a fixed fee ranging from 2% to 8% of the funding amount [2]. For example, if you receive a $100,000 advance with a 5% fee, you’ll repay a total of $105,000 - no matter how long it takes. Compare that to a traditional bank loan with a 12% APR, which would cost about $6,618 in interest [7]. With Onramp, there’s no interest piling up and no hidden fees - just clear costs you know upfront.

Customers seem to appreciate this transparency, as evidenced by Onramp’s "Great" rating on Trustpilot, where it holds an impressive 4.9 out of 5 stars from 220 reviews [2].

Seamless Integration with eCommerce Platforms

Onramp’s system integrates directly with major eCommerce platforms like Amazon, Shopify, TikTok Shop, Walmart, eBay, BigCommerce, WooCommerce, and Squarespace. Using real-time data from these channels, Onramp ensures its dynamic repayment model keeps your cash flow steady. This multi-channel approach also means you can qualify for higher funding limits because Onramp evaluates the full performance of your business, not just one storefront.

How to Choose the Right Repayment Structure

Match Repayment Terms to Your Sales Trends

Take a close look at your sales patterns from last year - especially the highs and lows. If your business has noticeable ups and downs throughout the year, fixed monthly payments might squeeze your cash flow during slower months [7]. A revenue-based repayment model, where you pay back a percentage of your daily sales, can ease this pressure. When sales dip, your repayments automatically decrease, helping you maintain cash flow.

For sellers operating across multiple platforms like Amazon, Shopify, or Walmart, it’s better to choose financing that accounts for your total sales across all channels [1]. Platform-specific financing options, such as Shopify Capital, only adjust based on sales from that particular platform. This can leave you in a tough spot if your other storefronts aren't performing well. Since eCommerce businesses often operate on 60–180 day cycles, it’s crucial to pick financing that aligns with these needs rather than locking yourself into a rigid, multi-year bank loan [3].

Once you’ve considered your sales patterns, the next step is understanding the long-term costs.

Understand the Full Cost Over Time

Don’t just focus on the upfront numbers - make sure to calculate the total repayment amount, including all fees. For example, a $100,000 advance with a 1.1 factor rate means you’ll pay $10,000 in fees. On the other hand, a bank loan with a 12% APR might initially seem cheaper but could force you to rely on higher-cost credit during slower sales periods [7][3].

Always ask for a detailed breakdown of all fees and penalties before you commit [5]. A loan calculator can be a helpful tool to compare the total repayment amount - not just the monthly payments - across different options [8].

Finally, consider how flexible the repayment terms are.

Prioritize Flexibility Over Low Rates

The repayment structure often matters more than the advertised interest rate. A low rate on a fixed-installment loan might look appealing, but if it forces you to take on high-interest debt during slow sales, the overall cost can skyrocket [7]. In 2021, only 7% of businesses reported avoiding financial services altogether [7]. Meanwhile, eCommerce retailers secured about $4.6 billion in financing during Q3 2022 alone [3]. These numbers highlight how important working capital is for sellers - and why repayment flexibility is just as critical as the cost.

Financing that adjusts to your revenue can make all the difference. Revenue-based options, which sometimes require as little as 1% of daily sales [2], offer the flexibility to scale repayments up or down depending on how your business is performing. This adaptability can be a game-changer for managing cash flow effectively.

Conclusion

When weighing financing options, it's crucial to look beyond the headline cost and focus on the repayment structure. A fixed-payment loan with a low advertised rate might seem appealing, but it can lead to high payments during slower months. This can strain your cash flow and push you toward costly alternative credit solutions [7]. The difference between fixed-payment and revenue-based models highlights the importance of choosing financing that aligns with your sales patterns.

Flexible repayment terms tackle these cash flow issues head-on. With revenue-based repayments, your payments adjust automatically based on your sales. During slower periods, payments decrease, allowing you to preserve cash for essential needs. As sales rebound, payments increase proportionally. This dynamic approach helps protect your margins and gives you the flexibility to grow without the stress of rigid financial obligations [5,9,11].

Onramp Funds takes this a step further with revenue-based financing tailored to match your sales cycle. They offer a transparent fee structure ranging from 2%–8% and integrate seamlessly with platforms like Amazon, Shopify, and Walmart [2,9]. Plus, there are no hidden costs, no equity dilution, and no personal guarantees required - giving you the support you need without unnecessary complications.

FAQs

How do revenue-based repayments benefit seasonal businesses?

Revenue-based repayments adapt to your business’s actual sales, making them a great fit for businesses with seasonal fluctuations. When sales peak during busy months, payments rise accordingly. On the flip side, during slower periods, payments decrease, helping you preserve steady cash flow throughout the year.

This approach eliminates the stress of fixed payments during off-seasons, giving you the freedom to concentrate on running and growing your business without the pressure of rigid repayment terms. It’s a practical way to match your financing to the rhythm of your sales cycles.

Why can a low interest rate be misleading in financing?

A low interest rate might look tempting at first glance, but it doesn’t always tell the whole story. Things like flat fees, hidden costs, or a repayment plan that clashes with your cash flow can quietly drive up the true cost of financing, making it more expensive than it seems.

Take fixed daily or weekly payments, for example. While they might seem straightforward, they can put a strain on your cash flow if your business experiences seasonal ups and downs in sales. On the flip side, repayment plans that adjust based on your revenue offer more breathing room, letting payments scale back during slower periods. The key is to dig into the full repayment terms - not just the interest rate - so you can choose a financing option that supports your business’s growth without unexpected setbacks.

Why are flexible repayment terms important for eCommerce businesses?

Flexible repayment terms give eCommerce businesses the ability to sync their payments with how well their sales are doing, making cash flow management much smoother. Instead of sticking to fixed monthly payments, many of these plans operate on a revenue-based model. What does that mean? Payments adjust according to sales - higher payments during strong sales periods and lower ones when sales slow down. This setup helps reduce financial pressure and lowers the chances of missed payments.

This approach is particularly useful for businesses with seasonal sales or unpredictable sales cycles. It allows them to better handle expenses during both busy and slower times. On top of that, revenue-based financing usually comes with straightforward, flat-fee pricing. Businesses know exactly what they’ll pay from the start, without having to worry about fluctuating interest rates. These features combine to give businesses the breathing room they need to stay focused on growth, free from the constraints of rigid repayment schedules.