Building your eCommerce business on platforms like Amazon or TikTok Shop can expose you to serious financial risks. While these platforms offer access to large audiences, relying on them too heavily can lead to unpredictable revenue shifts, account suspensions, and stricter lending terms.

Key takeaways:

- Revenue risks: Algorithm updates, policy changes, or outages can disrupt cash flow.

- Account suspensions: Violations, even minor ones, can halt income and damage trust.

- Funding challenges: Lenders view single-platform businesses as riskier, limiting loan options.

Solution: Diversify sales channels and consider revenue-based financing to manage cash flow during platform disruptions. Selling on multiple platforms and maintaining your own store can reduce dependence, while flexible funding models like Onramp Funds align repayments with your sales performance.

This article explores these risks and provides actionable strategies to protect your business.

The Dangerous Mistake E-commerce Brands Keep Making in 2025 (Key Platform Risk)

sbb-itb-d7b5115

How Platform Dependence Creates Problems

Relying too heavily on a single platform can create serious challenges for businesses. These challenges often fall into three categories: unpredictable revenue shifts, operational disruptions, and limited access to funding. Each of these can destabilize cash flow and leave your business exposed to risks beyond your control.

Revenue Swings from Platform Changes

When a platform controls your customer access and revenue streams, even minor changes in their policies or algorithms can have major consequences. As Stripe points out:

When a platform controls your access to customers, revenue, or operations, your business becomes subject to decisions you can't influence, such as policy changes, algorithm updates, technical issues, and even shutdowns[1].

Take Amazon's upcoming 2026 policy change as an example. Starting May 31, 2026, reviews for product variations - such as those differing in functionality or formulation - will no longer be grouped together. This change could erase years of hard-earned social proof for sellers, leading to lower conversions and revenue drops[3]. Similarly, TikTok Shop plans to phase out independent seller shipping in early 2026, forcing merchants to rely solely on platform-controlled logistics[3].

Platforms can also unexpectedly raise fees. For instance, Walmart Connect's advertising revenue grew by 33% in Q3 2025, far outpacing the overall US retail sales growth of 5% during the same period[3]. Chuck Kessler, SEO and GEO Strategist at Canopy Management, noted:

Every platform is raising standards simultaneously, and each one demands specialized knowledge to navigate well[3].

Technical issues add another layer of unpredictability. As Mailchimp explains:

If your website suddenly crashes or you're having a problem with your payment processor, that downtime could potentially cost you money and customers[2].

Outages or glitches can bring your sales to a halt, leaving you powerless to resolve the situation quickly. These sudden revenue disruptions often create a domino effect, leading to operational and financial difficulties.

Account Suspensions and Business Interruptions

Account suspensions are one of the most immediate dangers of platform reliance. Automated moderation systems can flag accounts for unclear policy violations, chargebacks, or unresolved customer complaints. When this happens, income stops, and access to crucial business data is cut off[1].

From a customer's perspective, a suspended account can make your business seem to disappear. Links stop working, profiles vanish, and trust erodes - even if the issue is eventually resolved[1]. Recovery often requires significant resources, such as legal fees, emergency support, and lengthy appeals[1].

Tighter performance standards are increasing the risk of suspensions. For example, Amazon has ramped up enforcement of its "On-Time Delivery" metric, Walmart now tracks a "Negative Feedback Rate", and TikTok Shop will introduce a 0-to-1,000 Account Health Rating system in March 2026[3]. Under these stricter rules, even small missteps - like a late shipment or a single bad review - could lead to account deactivation.

Payment holds add another layer of complexity. Platforms can freeze payouts during fraud investigations or compliance reviews, cutting off access to funds without notice[1]. Even if your account remains active, these withheld payments can prevent you from restocking inventory or covering basic operating costs. These disruptions not only harm your reputation but also make your business appear riskier to potential lenders.

Limited Funding Options from Single-Platform Revenue

When your revenue depends on one platform, lenders often see your business as a higher risk. Concentrated sales mean that any disruption - like an account suspension or payment hold - could wipe out your income overnight. This perceived instability makes it harder to secure funding, limits borrowing capacity, and often results in stricter repayment terms.

The risks tied to platform dependence only make this problem worse. Lenders are wary of businesses that could lose their primary income source due to platform-related issues. Even if your sales numbers are strong, the potential for sudden revenue loss can make your business seem less creditworthy.

On the other hand, businesses with diversified revenue streams tend to appear more stable. If one platform experiences issues, the others can keep the business running. This stability often makes lenders more willing to offer loans with flexible terms, as the risk of total revenue loss is much lower.

How Platform Dependence Increases Funding Risk

Platform-Dependent vs Diversified eCommerce Businesses: Funding Risk Comparison

Relying heavily on a single platform can heighten funding risks due to the concentration of revenue streams. This type of reliance amplifies the financial vulnerabilities that come with platform dependence.

Stricter Lender Requirements

Businesses tied to one platform often face stricter scrutiny from lenders compared to those with diversified revenue streams. Why? Because a single-channel dependency exposes a business to external factors beyond its control - factors that can wipe out revenue in an instant.

Immediate risks include payment holds, delays, or fraud investigations that can freeze cash flow without warning [1]. Stripe explains this challenge clearly:

A suspended seller account or frozen payment processor can halt your income overnight. If your business relies heavily on that channel, cash flow will dry up instantly. - Stripe [1]

Additionally, algorithm changes or sudden platform policy updates can slash revenue, making it harder to meet repayment obligations [1]. If an account gets suspended, businesses lose not only revenue but also access to customer data and performance analytics - key tools lenders use to assess stability.

Lenders are naturally cautious about approving loans for platform-dependent businesses. Approval rates are lower, and lenders often require more proof of financial resilience [4]. Security concerns also play a role; in a 2024 survey, 61% of companies reported experiencing a third-party data breach or security incident [1]. These risks make lenders wary, further differentiating the risk profiles of platform-reliant businesses from diversified ones.

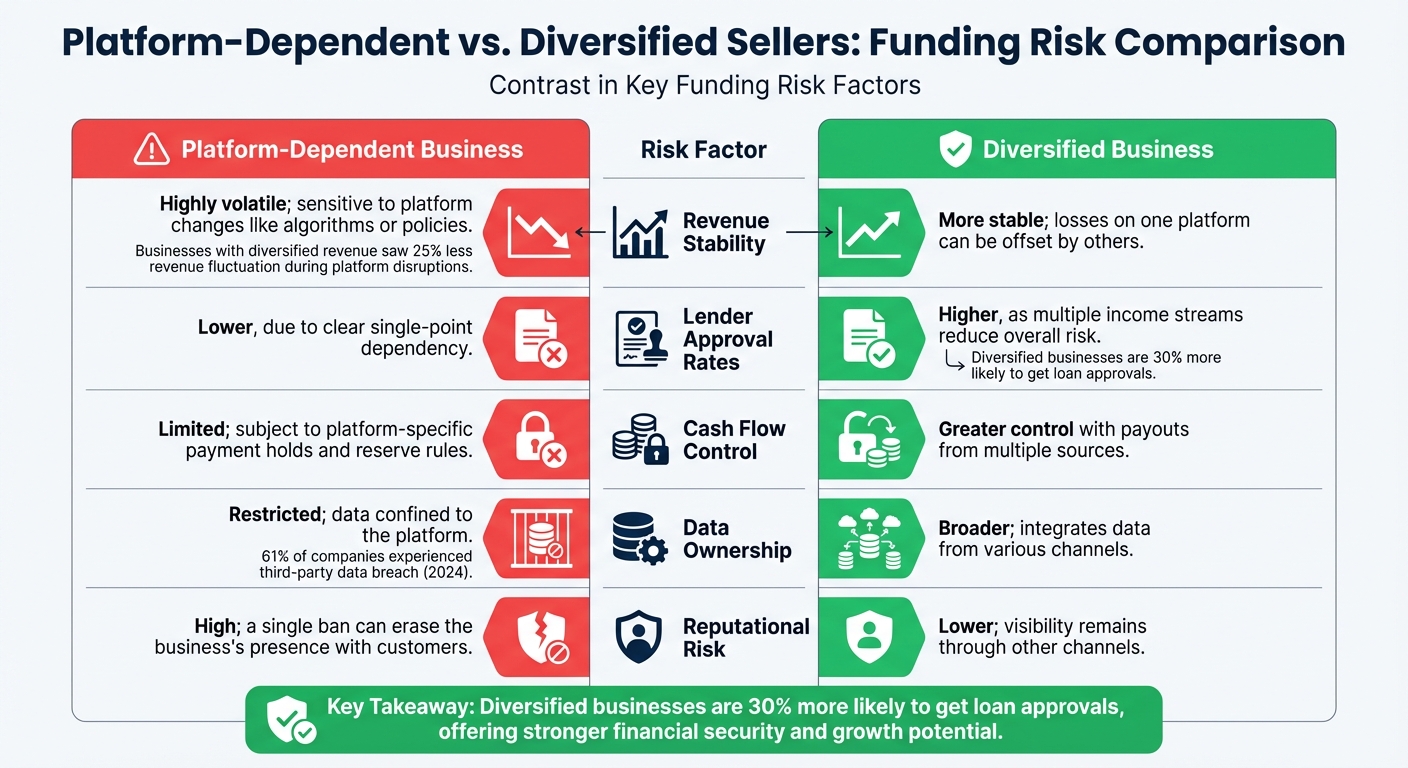

Platform-Dependent vs. Diversified Sellers: Funding Metrics

A direct comparison shows how reliance on a single platform impacts funding evaluations. Diversified businesses consistently demonstrate lower risk across critical metrics:

| Risk Factor | Platform-Dependent Business | Diversified Business |

|---|---|---|

| Revenue Stability | Highly volatile; sensitive to platform changes like algorithms or policies | More stable; losses on one platform can be offset by others |

| Lender Approval Rates | Lower, due to clear single-point dependency | Higher, as multiple income streams reduce overall risk |

| Cash Flow Control | Limited; subject to platform-specific payment holds and reserve rules | Greater control with payouts from multiple sources |

| Data Ownership | Restricted; data confined to the platform | Broader; integrates data from various channels |

| Reputational Risk | High; a single ban can erase the business’s presence with customers | Lower; visibility remains through other channels |

When platforms control all transactions, they often impose reserve rules, freezing capital and increasing the risk of technical loan defaults [1]. Diversified businesses, however, are less vulnerable to such disruptions. With multiple payment processors and payout schedules, they maintain better control over their cash flow and financial stability.

How to Reduce Platform Dependence Risks

Reducing your reliance on a single platform requires intentional steps in both your sales and funding strategies. The aim is to spread out risks, ensuring your business can grow steadily without being overly affected by one platform’s rules or algorithm changes. This approach helps shield you from revenue fluctuations, account suspensions, and funding challenges.

Sell on Multiple Platforms

Selling across various platforms is one of the simplest ways to minimize risk. By diversifying your presence on marketplaces like Amazon, Shopify, TikTok Shop, eBay, and Etsy, you’re less likely to face a total income freeze if one platform changes its policies or algorithms.

Beyond using multiple marketplaces, having your own online store gives you more control. When you manage your own storefront, you control checkout processes, customer data, and pricing. Unlike third-party platforms, your direct-to-consumer channel isn’t subject to sudden policy shifts, and you maintain direct relationships with your buyers. Keeping an independent email list or CRM ensures you can still reach your customers even if a platform limits your communication tools or suspends your account.

Owning your customer data also strengthens your funding options. When you have access to detailed customer information from multiple channels, lenders can get a clearer picture of your business’s stability. Regularly document your revenue sources and test worst-case scenarios to identify which backup platforms can keep your sales running if your primary channel becomes unavailable.

While selling on multiple platforms reduces revenue risks, pairing this strategy with funding solutions that adapt to your sales performance can further boost your financial security.

Use Revenue-Based Financing

Traditional loans can be tough on businesses that depend heavily on one platform, often requiring stricter qualifications and offering less favorable terms. Revenue-based financing, on the other hand, adjusts repayment according to your actual sales, helping ease cash flow issues. This type of funding aligns with your business performance, so during slower periods or platform disruptions, your repayment obligations decrease naturally.

For example, Onramp Funds offers equity-free financing tailored for eCommerce sellers on platforms like Amazon, Shopify, BigCommerce, WooCommerce, Squarespace, Walmart Marketplace, and TikTok Shop. Their repayment model takes a percentage of your sales, meaning payments automatically scale down when revenue dips due to platform issues. There’s no fixed monthly payment to worry about during times of uncertainty, such as account holds or algorithm changes.

The fee structure is straightforward, ranging from 2-8%, with no hidden charges. To qualify, businesses need to generate at least $3,000 in monthly sales, and the application process integrates with your connected stores to evaluate eligibility based on your actual sales history - not rigid credit checks. This flexibility is especially helpful during periods of revenue volatility, ensuring your funding doesn’t add to financial strain when cash flow tightens.

Tools for Managing Funding Risk

To support efforts in spreading out risk, consider the tools below to help manage funding challenges. Start by identifying your revenue streams and pinpointing vulnerabilities, especially those tied to platform disruptions.

Funding Calculators for Risk Assessment

The Onramp Funds calculator is a handy tool that estimates your available funding based on your current sales data. By directly connecting to your eCommerce platforms, it analyzes your revenue history to provide funding estimates and simulate repayment scenarios. This allows you to plan for both growth and potential slowdowns, offering a safety net if a platform faces disruptions. It also helps you keep track of sales performance across multiple channels, giving you a clearer picture of your business health.

Track Revenue Sources and Sales Performance

Keeping tabs on where your revenue comes from is crucial for assessing risk. A good starting point is calculating the percentage of sales each platform contributes. For example, if one platform accounts for more than 70% of your sales, you could be exposed to significant risk [1]. A simple spreadsheet tracking monthly sales by channel can highlight trends or sudden shifts, making it easier to identify over-reliance on a single source.

Stay informed about platform policies and industry updates. Changes like fee increases, algorithm updates, or new policies can often be spotted in advance, giving you time to adjust your strategy [1]. Additionally, test your backup plans periodically. If you don’t have a clear way to pivot when your primary platform falters, it’s time to build alternative sales channels. These insights can also guide you in choosing the financing model that aligns best with your cash flow.

Fixed vs. Revenue-Based Repayment: A Comparison

Once you have a clear understanding of your revenue data, it’s easier to weigh financing options to reduce risk. Different repayment structures handle platform disruptions in unique ways, so choosing the right one is key.

Traditional fixed repayment models require the same monthly payment, regardless of how well your sales are performing. This can strain your cash flow during slow periods. On the other hand, revenue-based financing adjusts repayments according to your actual revenue, offering more flexibility during downturns.

| Feature | Traditional Fixed Repayment | Onramp Funds Revenue-Based Financing |

|---|---|---|

| Monthly Payment | Fixed amount every month | Percentage of sales (automatically adjusts) |

| During Platform Disruption | Payment remains fixed | Payment decreases with lower sales |

| Fee Structure | Varies | Fixed fee of 2-8% |

| Qualification | Credit checks and financial statements | Minimum $3,000 monthly sales |

| Cash Flow Impact | High strain during slow periods | Adjusts naturally with revenue |

| Hidden Costs | Late fees and penalties possible | No hidden fees |

When faced with challenges like frozen funds or a drop in traffic due to algorithm changes, revenue-based financing can help you avoid the double blow of lost sales and rigid debt payments [1]. Since repayments scale with your revenue, you’ll have the breathing room needed to address the issue or shift focus to other sales channels without risking default.

Conclusion

Relying on just one eCommerce platform can leave your business vulnerable to serious funding challenges. Platform disruptions often lead to sudden drops in revenue, which can alarm traditional lenders. For example, when Amazon raised its fees in 2023, many sellers saw their profit margins shrink by 5-15%. Similarly, Shopify's 2024 compliance crackdowns impacted about 10% of merchants [5][7]. These disruptions can hurt your sales and make it harder to secure financing when you need it most.

Diversifying your sales channels can improve revenue stability and boost your funding options. When TikTok Shop faced disruptions in 2025, sellers who operated on multiple platforms saw 25% less revenue fluctuation compared to those relying on just one [6][8]. Data also shows that businesses with diversified revenue streams are 30% more likely to get loan approvals, proving that spreading out your sales can directly enhance your financial outlook.

Consider this real-world example: A U.S. beauty brand that depended on Amazon for 90% of its revenue lost $150,000 per month during a Q1 2025 suspension. By branching out to Shopify and TikTok Shop - and securing a $300,000 advance through Onramp Funds' revenue-based financing - they regained cash flow in just 45 days. This shift led to 35% year-over-year growth, thanks to a more balanced sales strategy [5][7].

Onramp Funds offers financing solutions tailored for businesses navigating market volatility. Their revenue-based financing adjusts repayment amounts based on your sales, helping you maintain cash flow during tough times. If your sales dip, your payments do too. Clients report funding approvals twice as fast and effective costs 20% lower than those from traditional lenders. Even during the volatile conditions of 2025, businesses using Onramp Funds managed to maintain 95% cash flow stability [8][9].

Take a close look at your revenue streams - if more than 50% of your sales come from one platform, your business could be at risk. Use Onramp Funds' online calculator to get pre-approved in just 24 hours. Build the financial safety net you need to adapt to platform changes and confidently expand to new sales channels. By combining diversified revenue streams with flexible financing, you can safeguard your business for the future.

FAQs

How do I know if I’m too dependent on one platform?

If most of your income comes from a single platform, you could be putting yourself at risk. Changes in policies, payout delays, or unexpected disruptions can leave you in a tough spot. For instance, if your cash flow depends on payout timelines - especially with delays stretching 20-30 days or more - that’s a clear warning sign. To protect yourself, take time to regularly assess where your revenue is coming from and work on spreading your sales across multiple channels. Diversification can help you avoid being overly reliant on one source.

What should I do first if my seller account gets suspended or payouts are frozen?

If your seller account is suspended or your payouts are frozen, the first step is to reach out to the platform’s support team to identify the root cause. This might require reviewing platform policies, providing necessary documentation, or addressing specific compliance issues. While you work on resolving the problem, it’s wise to explore funding options to keep your cash flow steady and cover critical expenses. Acting quickly on these steps can help reduce interruptions to your business operations.

How can revenue-based financing protect cash flow during a platform disruption?

Revenue-based financing offers a smart way to safeguard your cash flow during unexpected platform disruptions. With funding that adjusts to your business's revenue, it provides the flexibility needed to navigate challenges like revenue fluctuations or sudden policy shifts. This approach helps ensure your operations remain stable, reducing reliance on platform-dependent income and giving you the tools to manage financial hurdles effectively.