When it comes to managing business loans, your repayment structure can make or break your daily cash flow. Fixed repayments provide predictability but can strain your finances during slow sales periods. On the other hand, revenue-based repayments adjust with your sales, offering more flexibility to handle seasonal dips or fluctuating income.

Here’s the key takeaway: Misaligned repayment schedules can lead to cash shortages, even if your business is profitable on paper. To avoid liquidity issues, it’s crucial to:

- Align repayments with your revenue cycles.

- Monitor cash flow metrics like the cash flow coverage ratio.

- Use forecasting tools to predict repayment impacts.

- Consider revenue-based funding for more breathing room during slow periods.

Cash Flow Problems? Understand what REALLY impacts your cash

sbb-itb-d7b5115

How Repayment Schedules Affect Daily Cash Flow

Fixed vs Revenue-Based Repayments: Cash Flow Impact Comparison

Your repayment schedule plays a key role in determining how and when money leaves your business. For eCommerce sellers, this can be the difference between running smoothly and scrambling to cover essential costs like inventory restocks or ad campaigns.

Here’s the challenge: fixed repayments create a constant cash outflow that doesn’t adapt to fluctuations in sales [1][2]. Using repayment structures that adjust with your revenue can help avoid the liquidity crunch mentioned earlier. For instance, during slower months or seasonal dips, fixed payments remain due, even if your revenue drops. This mismatch can create a cash flow gap where your expenses outpace your income, potentially forcing you to take on additional, high-interest debt just to keep things running [4][5]. On the flip side, during periods of rapid growth, these fixed payments can drain the cash you need to scale inventory and meet demand [5].

Debt repayments, categorized under financing activities, directly reduce your available cash [2][6]. If these outflows don’t align with your daily sales inflows, you could find yourself strapped for cash - even if your business appears profitable on paper.

Fixed Repayments vs. Revenue-Based Repayments

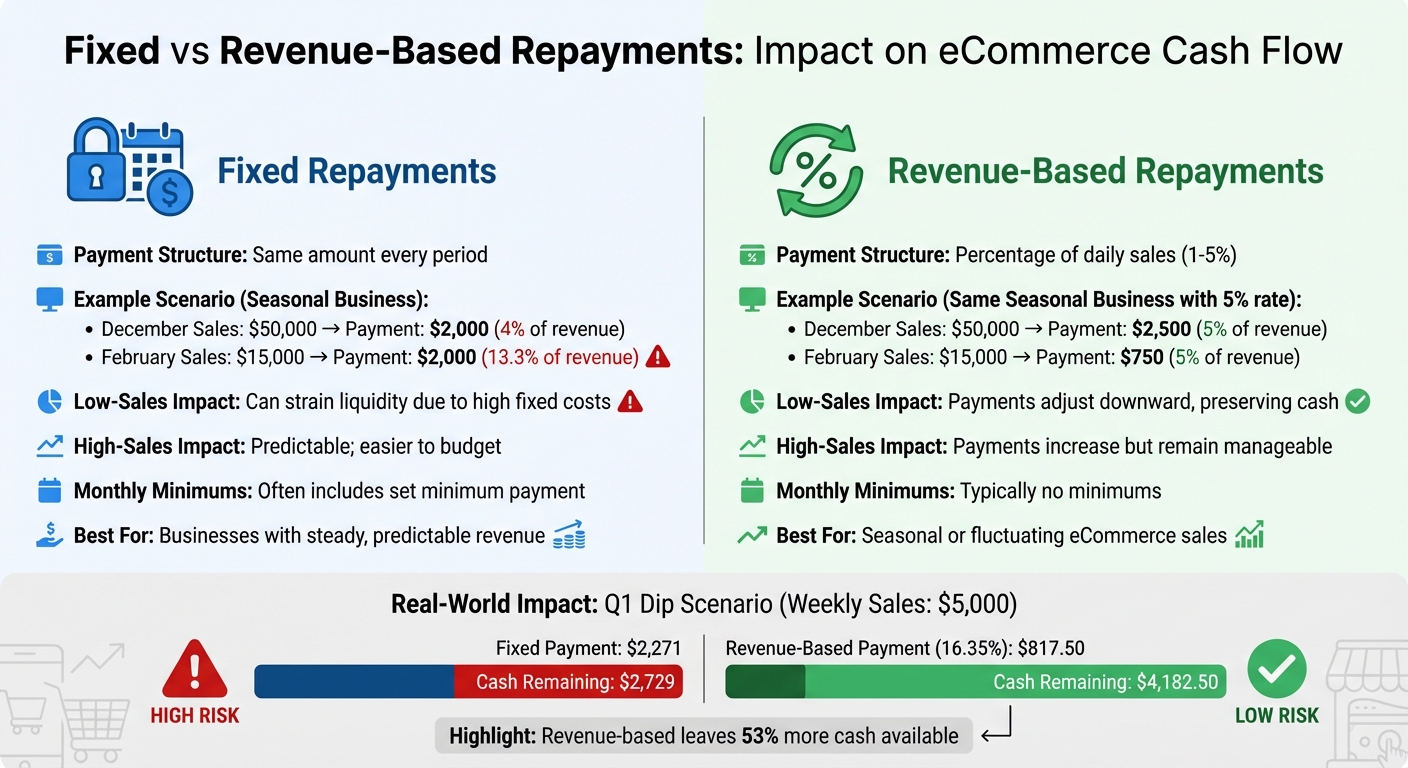

Fixed repayment models require you to pay the same amount every period, no matter if you had a stellar $10,000 sales day or a sluggish $1,000 sales day. While this predictability can simplify long-term budgeting, it offers no flexibility when sales slow down. You’re locked into that payment, rain or shine.

Revenue-based repayments, on the other hand, adjust based on a percentage of your daily sales. For example, Onramp Funds uses this model with remittance rates as low as 1% of daily sales [3]. In a strong sales week, you pay more; in a slow week, you pay less. There are typically no monthly minimums, so during slow periods, you’re not forced to drain your reserves to meet a rigid payment amount [3].

Take a seasonal business as an example. If it generates $50,000 in December and $15,000 in February, a fixed $2,000 payment in February would eat up 13.3% of revenue. But under a 5% revenue-based model, the payment adjusts to $2,500 in December and just $750 in February, leaving more cash available during slower months.

| Feature | Fixed Repayments | Revenue-Based Repayments |

|---|---|---|

| Payment Amount | Fixed dollar amount | Percentage of daily sales (e.g., 1-5%) |

| Low-Sales Periods | Can strain liquidity due to high fixed costs | Payments adjust downward, preserving cash |

| High-Sales Periods | Predictable; easier to budget if margins are stable | Payments increase, but remain manageable |

| Monthly Minimums | Often includes a set minimum payment | Typically no minimums [3] |

| Best For | Businesses with steady, predictable revenue | Seasonal or fluctuating eCommerce sales |

This repayment structure also has a ripple effect on your cash conversion cycle, as we’ll explore next.

Impact on Cash Conversion Cycle

Your repayment schedule doesn’t just influence your immediate cash flow - it also affects the timing of cash collection from inventory sales. The cash conversion cycle (CCC) measures how long it takes to turn inventory into cash, from purchase to sale to customer payment [5]. Repayments can disrupt this cycle by pulling cash out of your business before you’ve completed it.

Here’s how it works: imagine you buy $10,000 of inventory on January 1st. It takes 30 days to sell, and your customers take another 15 days to pay, resulting in a 45-day CCC. Now, suppose you have a $3,000 fixed loan payment due on January 15th - before you’ve sold the inventory or collected payment. You’d need to cover that payment from your reserves, leaving less cash available for reordering inventory or grabbing growth opportunities [7][8].

Revenue-based repayments, however, help keep your CCC stable. Since payments scale with your actual sales, you’re not draining cash reserves before your inventory has converted into revenue. This alignment is critical for eCommerce businesses, where inventory often ties up cash that could be used elsewhere [8].

As Kelley Birrell, Content Manager at LedgerGurus, wisely says:

Revenue is vanity, profit is sanity, cash is king [7].

Your repayment structure determines whether you hold onto that "cash is king" status or find yourself constantly short on the liquidity needed to operate and grow.

Repayment Effects on Liquidity: Examples

Looking at the cash conversion cycle, these examples highlight how repayment terms can directly influence liquidity. Understanding these effects is crucial for managing operational costs effectively.

Example: Fixed Repayment During Low-Sales Periods

Consider an eCommerce business that secures $25,000 in funding with a fixed monthly repayment of $2,271. During a strong sales week in Q4, with revenue hitting $15,500, this repayment accounts for 14.6% of sales. At this level, the payment is manageable and predictable. However, eCommerce businesses often see a 40–60% drop in sales during Q1 following the holiday season[9].

Fast forward to February, when weekly sales plummet to $5,000. That same $2,271 repayment now consumes 45.4% of revenue, leaving just $2,729 for inventory restocks, advertising, supplier payments, and other essential expenses. This imbalance makes it difficult to manage inventory and other critical operations on time.

Example: Flexible Repayment with Revenue-Based Models

Now, imagine a repayment model tied to a remittance rate of 16.35%. Here, repayments adjust based on actual sales. During a slow $5,000 sales week, the repayment would be just $817.50 - leaving $4,182.50 in available cash[3]. When sales rebound to $15,500, the repayment increases to $2,534, which is more manageable when revenue is higher.

This flexibility is especially helpful for eCommerce businesses, as Q4 often accounts for 30–50% of their annual revenue[9]. The inevitable post-holiday slowdown in Q1 can strain liquidity, but revenue-based payments ease the pressure by scaling down during these dips.

Comparison Table: Fixed vs. Revenue-Based Repayments

The table below compares fixed and revenue-based repayment models across different sales scenarios for a Shopify seller:

| Sales Week | Weekly Sales | Fixed Repayment | Revenue-Based (16.35%) | Cash After Fixed | Cash After Revenue-Based | Cash Shortage Risk |

|---|---|---|---|---|---|---|

| Q4 Peak | $15,500 | $2,271 | $2,534 | $13,229 | $12,966 | Low for both |

| Average Week | $14,700 | $2,271 | $2,403 | $12,429 | $12,297 | Low for both |

| Slow Week | $14,500 | $2,271 | $2,371 | $12,229 | $12,129 | Moderate for fixed |

| Q1 Dip | $5,000 | $2,271 | $817.50 | $2,729 | $4,182.50 | High for fixed |

This comparison reveals that fixed payments are suitable for stable or high-sales periods but can create liquidity challenges during slower weeks. Revenue-based payments, on the other hand, leave about 53% more cash on hand during a Q1 dip ($4,182.50 versus $2,729)[3], offering much-needed flexibility to cover operating expenses during tough times.

Tools and Methods for Forecasting Repayment Impacts

Using Forecasting Tools for Cash Flow Planning

Accurate cash flow forecasting depends heavily on real-time sales data. It's a critical step in managing repayment obligations without jeopardizing daily liquidity. Onramp Funds integrates directly with platforms like Shopify and Amazon Seller Central, pulling live sales data to create tailored funding scenarios based on weekly sales performance, eliminating the need for manual spreadsheets[3][10].

With its funding calculator, the platform uses your store's data to simulate repayment outcomes before any commitment is made[3]. For instance, you can explore how a revenue-based repayment model with a 1% daily remittance rate might impact your cash flow during both busy and slow sales periods. This level of visibility allows you to choose between fixed payments (predictable dollar amounts) and revenue-based payments (a percentage of daily sales), depending on your store's sales patterns[3].

"The ability to curate automated dashboards and forecasts is incredibly valuable. The enhanced BILL platform empowers me to equip our teams with the insights needed to propel our business forward with confidence." - Jennifer Dent, Senior Finance Manager, 1021 Creative[11]

Rolling forecasts, such as a 13-week model for short-term needs like inventory or ad spend, and a 52-week model for tracking seasonal trends, are especially useful. These tools also account for delays in cash receipt, such as Amazon's 14-day payout hold[12]. By using these forecasting methods, businesses can monitor key metrics that directly impact their repayment strategies.

Key Metrics for Repayment Analysis

Once you've established a forecasting framework, it's essential to focus on specific metrics that help evaluate the impact of repayments on your cash flow.

- Cash Flow Coverage Ratio: This metric assesses whether your operating cash flow is sufficient to cover debt obligations. A strong ratio indicates that your business can comfortably handle fixed payments, even during slower sales periods. A weaker ratio may signal potential liquidity issues.

- Operating Cash Flow Margin: This measures how much of your sales revenue converts into operating cash. A noticeable decline in this margin could be an early warning sign that repayments are putting a strain on liquidity.

- Daily Sales Volume: For revenue-based repayment models, daily sales volume is a key factor. Since remittance amounts are tied to sales, monitoring this metric ensures that payments remain proportional to income, making it easier to assess how much cash remains for operational needs[3][10].

Comparison Table: Cash Flow Metrics Before and After Repayments

| Metric | No Repayments | Fixed Repayments | Revenue-Based Repayments |

|---|---|---|---|

| Daily Liquidity | Maximum; all revenue retained | Reduced by a set dollar amount regardless of sales | Reduced by a set percentage; scales with sales |

| Cash Flow Predictability | High (based solely on sales) | High (fixed outflow) | Moderate (outflow tied to sales) |

| Risk of Cash Crunch | Low (if sales continue) | Higher during seasonal dips | Lower; payments decrease during slow periods |

| Growth Potential | Limited by existing capital | High (due to capital injection) | High (due to capital injection) |

This table highlights how repayment methods affect cash flow differently. While avoiding repayments maximizes liquidity, it can limit growth due to a lack of additional capital. Fixed repayments offer predictability but may strain cash flow during low-sales periods. Revenue-based repayments, on the other hand, adapt to fluctuating sales, making them a more flexible option for eCommerce businesses. In fact, merchants using specialized eCommerce funding have reported an average revenue growth of 60%[3]. These tools and metrics lay the groundwork for practical strategies to maintain liquidity while managing repayment obligations effectively.

Practical Steps to Prevent Cash Flow Problems

Align Repayments with Peak Revenue Periods

Revenue-based financing offers a flexible way to manage repayments by tying them directly to your sales volume. This means you pay more during busy seasons and less during slower periods. For example, Onramp Funds uses a variable repayment model, where businesses remit a percentage of daily revenue - typically between 5% and 15% - instead of a fixed amount. This approach helps prevent cash flow issues during off-peak months [26,28].

Take the case of a seasonal electronics retailer: they aligned their repayments with their Q4 holiday sales, which accounted for 60% of their annual revenue. During slower months, they paid just 8% of sales instead of a fixed $15,000 monthly payment. This adjustment preserved $200,000 in liquidity annually, ensuring they could pay suppliers on time and avoid cash shortages [26,27].

By syncing repayments with revenue, businesses can avoid overextending themselves during slow periods while freeing up cash for critical needs like inventory and advertising during peak demand. This strategy also complements efforts to improve liquidity through better supplier terms.

Optimize Inventory and Supplier Terms

Negotiating longer payment terms with suppliers can significantly improve cash flow. Extending terms from net‑30 to net‑60 or net‑90 can free up 10–20% of working capital each month, giving you more flexibility to cover repayments without resorting to additional borrowing [26,28]. Additionally, improving inventory turnover can further enhance liquidity.

Using techniques like ABC analysis - where high-turnover items are prioritized and automated reorder points are set - can reduce carrying costs by 15–25%. For instance, a fashion eCommerce business increased its inventory turnover from 4× to 8× annually by adopting this strategy. This improvement freed up enough cash to comfortably handle $50,000 in monthly repayments without liquidity issues [13].

Tracking your Cash Conversion Cycle (Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding) is another practical way to align cash flow with repayment schedules. Even extending supplier payment terms by 10 to 30 days can help ensure that your outgoing payments remain manageable [26,28].

While optimizing supplier terms can improve day-to-day cash flow, combining this with flexible funding options can provide the capital needed to scale during high-demand periods.

Use Equity-Free, Fast Funding for Growth

For businesses looking to grow without giving up equity or committing to rigid payment schedules, revenue-based financing is a game-changer. Onramp Funds, for example, offers financing that doesn’t require fixed monthly payments or personal guarantees [3]. By integrating with platforms like Amazon Seller Central and Shopify, Onramp Funds pulls real-time sales data to calculate repayments that adjust to your daily revenue [3].

Unlike traditional loans with fixed monthly payments (e.g., $10,000 per month, regardless of sales), this model scales repayments based on actual revenue. This flexibility is especially useful for eCommerce businesses experiencing 20–50% year-over-year growth and needing quick access to capital for inventory or marketing.

The funding comes with a flat fee structure, ranging from 2% to 8% of the funded amount, and remittance rates can be as low as 1% of daily sales [3]. This approach allows businesses to strategically deploy capital, whether it’s for stocking up ahead of a busy season or launching a marketing campaign, while keeping enough cash on hand for day-to-day operations. Many merchants using this type of funding have reported an average revenue growth of 60% [3].

Conclusion

Managing repayments effectively means aligning payment structures with your cash flow patterns. Fixed repayment plans offer predictable budgeting but can strain liquidity during slower months. On the other hand, revenue-based models adjust payments based on daily sales - typically charging 5–10% during high-revenue periods and less when sales slow down. This flexibility helps maintain steady operational liquidity throughout the year.

To complement these repayment structures, using advanced forecasting tools is crucial. Real-time dashboards that track metrics like the cash flow coverage ratio (ideally above 1.0) can signal potential issues early. For example, eCommerce businesses leveraging these tools have seen cash shortages drop by 25–40% by aligning repayments with peak revenue forecasts. This proactive approach helps avoid the 20–30% liquidity gaps that often occur during slower seasons [13][14][15].

Combining flexible repayment models with smart strategies - such as negotiating net-60 supplier terms or improving inventory turnover - strengthens cash flow resilience. Revenue-based financing, like the solutions provided by Onramp Funds, adjusts payments to match daily sales, ensuring you have access to capital even during slower periods. This kind of financing grows with your business instead of working against it [3].

Ultimately, selecting repayment plans that align with your business cycles is key. Whether you're navigating seasonal fluctuations, planning for growth, or weathering slower times, matching your financing structure to your revenue patterns safeguards liquidity and supports long-term growth.

FAQs

How can revenue-based repayments help manage cash flow during slower sales periods?

Revenue-based repayments adapt to your business's income, so when sales slow down, your repayment amounts decrease as well. This approach eases financial pressure, helping you keep critical operations running and maintain cash reserves.

Tying repayments directly to your revenue creates a manageable way to meet loan obligations without straining your cash flow - even during seasonal slumps or unexpected drops in income.

What tools can help eCommerce businesses forecast the impact of repayment schedules on cash flow?

To get a handle on how various repayment schedules might impact your cash flow, start by using tools that let you see inflows and outflows side by side. Many eCommerce sellers rely on accounting platforms equipped with forecasting features. These tools can automatically pull in your sales data and apply repayment terms, giving you a clear picture of how your daily cash balances shift under different scenarios.

For a deeper dive, cash flow management software can be a game-changer. These programs let you model multiple repayment plans, compare best-case and worst-case scenarios, and track cash flow trends over time with easy-to-read visuals. Prefer doing things your way? Spreadsheet templates in Excel or Google Sheets are a flexible option. You can customize them to track revenue, expenses, and repayment schedules, making it simple to test different structures and see their immediate impact on your cash position.

By mixing these approaches - automated accounting tools, scenario-focused cash flow software, and customizable spreadsheets - you’ll get a well-rounded view of how repayment schedules could affect your daily liquidity.

How can eCommerce businesses match loan repayments to their revenue cycles?

To keep your cash flow steady, it’s smart to align your loan repayments with how and when your business earns revenue. Start by forecasting your cash flow - track when money flows in from sales and when it goes out for expenses like operating costs and loan payments. This will help you pinpoint high-revenue periods, such as post-holiday sales, when you can afford to make larger payments. During slower months, you can scale back to smaller payments.

You might also want to match your repayment schedule to your payout cycle, like the day after your payment processor deposits funds. Flexible repayment plans - such as weekly or monthly payments based on a percentage of sales - can ease the strain on your cash reserves. For businesses with seasonal income, negotiating terms for smaller payments during slower months and larger ones during peak seasons can make a big difference.

It’s also a good idea to keep a short-term cash cushion - enough to cover one to two weeks of operating expenses. This safety net can help you handle any unexpected delays in cash flow. Regularly update your forecasts with real sales data and tweak repayment amounts as needed to meet your financial commitments without disrupting your day-to-day operations.