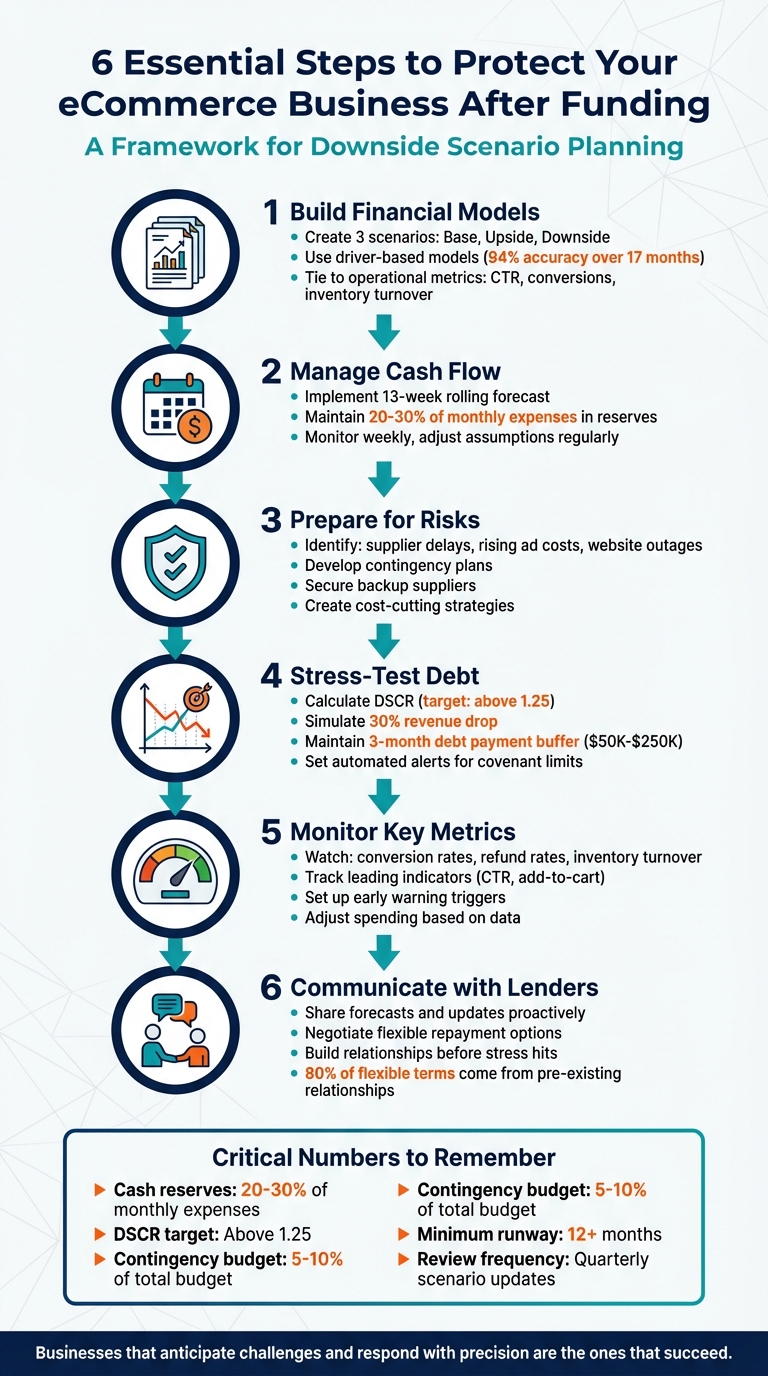

Securing funding for your eCommerce business is a big step, but it comes with risks. Growth can lead to challenges like supply chain delays, unexpected costs, or cash flow gaps. The key? Plan for worst-case scenarios before they happen. Here's how:

- Build financial models: Create base, upside, and downside scenarios to predict how changes in revenue, expenses, or cash flow might impact your business.

- Manage cash flow: Use tools like a 13-week rolling forecast to spot shortfalls early. Keep reserves of 20%-30% of monthly expenses to handle emergencies.

- Prepare for risks: Identify potential issues like supplier delays, rising ad costs, or website outages. Have contingency plans, backup suppliers, and cost-cutting strategies in place.

- Stress-test debt: Calculate your Debt Service Coverage Ratio (DSCR) and simulate revenue drops to ensure you can meet loan payments.

- Monitor key metrics: Watch for red flags like lower conversions, rising refunds, or inventory turnover issues. Adjust spending and operations as needed.

- Communicate with lenders: Share forecasts and updates to negotiate flexible repayment options if needed.

Planning ahead protects your business from unexpected disruptions and helps you make smarter decisions when challenges arise.

6-Step Framework for Downside Scenario Planning After eCommerce Funding

Financial Projections for E-Commerce Businesses: What to Include

sbb-itb-d7b5115

Creating Base, Upside, and Downside Financial Models

After securing funding, it’s crucial to have a clear understanding of where your business might head - not just where you want it to go. Financial scenario modeling provides three key perspectives: a realistic projection (base case), an optimistic forecast (upside), and a worst-case scenario (downside). These models guide decisions around spending, inventory, and cash flow management.

What Financial Model Scenarios Mean

Each scenario represents a possible future outcome. The base case is your most likely scenario, built on actual sales data and current trends. As Matt Putra, Managing Partner at Eightx, explains: "The biggest thing we do - the most important thing we do - is build you a forecast. Our forecasts are month by month: income statement, cash flow statement, balance sheet, extending out three years minimum." [2]

The upside scenario outlines what happens if things go better than expected. For example, a product might go viral on TikTok, a competitor might leave your market, or seasonal sales could see a 50% to 75% spike [4][5]. This isn’t just optimism - it’s preparation for growth opportunities so you can scale effectively when the moment strikes.

The downside scenario, on the other hand, explores how your business might be impacted by challenges. These could include a 15% to 30% drop in revenue, suppliers shortening payment terms, or rising ad costs combined with lower conversion rates [2][1]. This model helps you pinpoint your breaking point and plan responses to avoid running out of cash.

For eCommerce businesses, these models should be driver-based, meaning they tie directly to operational metrics like click-through rates, add-to-cart conversions, and inventory turnover [2]. Driver-based models can predict revenue with up to 94% accuracy over 17 months [2], making them a reliable tool compared to guesswork.

With these scenarios in mind, the next step is to build a detailed downside model tailored to your business’s operational realities.

How to Build a Downside Financial Model

Start by gathering six months of bank statements, sales data from all channels (Shopify, Amazon, wholesale), and your current accounts payable and receivable reports [2]. This data provides a realistic starting point.

Next, identify risks that could harm your cash flow over the next 90 days. For eCommerce, common risks include delayed supplier shipments, website outages during peak shopping events, new tariffs on imports, or sudden increases in ad costs [1].

Adjust revenue projections to reflect a typical drop from your base case. For instance, if you sell on Amazon, account for their 14-day payout cycle. If you’re running a direct-to-consumer (DTC) brand, factor in Shopify’s 2–3 business day payout schedule. Focus on when cash actually lands in your account, not just when sales occur.

On the expense side, pay attention to irregular costs like inventory purchases. As Matt Putra explains: "The way we approach it is we look at when you typically buy inventory... the model looks at total COGS for the year and allocates purchases on that schedule." [2] Instead of spreading a large inventory expense evenly over the year, reflect the actual timing of those purchases.

Watch for timing mismatches. For example, cash spent on inventory and ads often leaves your business long before customer payments come in. Holding eight months’ worth of inventory could tie up $200,000 in cash without you realizing it [2]. Calculate your Cash Conversion Cycle (CCC) - the time between paying suppliers and receiving customer payments. For inventory-heavy DTC brands, aim to keep this cycle under 90 days [2]. This analysis will directly influence your cash management strategies.

Set a minimum cash reserve in your model. Most eCommerce businesses should keep 20% to 30% of their monthly burn in cash reserves [2]. If your downside scenario shows your cash balance dropping below this threshold, flag it and plan adjustments at least two to three weeks in advance.

Use a 13-week rolling cash flow forecast for short-term planning [2]. This weekly tool helps you identify potential cash shortfalls before they become crises. Update it weekly by comparing actual results to your forecast. If you consistently overestimate collections or underestimate costs, adjust your assumptions [2].

How to Use Models for Decision Making

Once your models are complete, use them to guide key decisions in real time. These scenarios aren’t just spreadsheets to file away - they’re tools for action. Your base case helps you plan for normal conditions, your upside case highlights when to invest in growth, and your downside case shows when to tighten spending.

Monitor leading indicators like click-through rates and add-to-cart conversions. A drop in these metrics today could signal a cash flow hit in two to three weeks [2]. This early warning allows you to cut ad spending, delay purchase orders, or negotiate extended payment terms with suppliers - offering a small premium, like 1%, to extend terms from 30 to 60 days if necessary [2].

Stress-test major decisions against your downside model. For example, before placing a large inventory order, see if it would push your cash balance below your minimum threshold during a revenue dip. If it would, consider reducing the order size or securing extra working capital.

As Eightx advises: "If the downside kills you, don't do it." [2] That’s the bottom line - if your downside scenario shows you running out of cash with no way to recover, it’s a decision to avoid. But if your model shows you can weather the storm with some adjustments, you’ll have a clear plan for which expenses to cut and when.

Identifying Key Risks in eCommerce Operations

Common Risks After Securing Funding

Securing funding can feel like a significant milestone, but it often brings new challenges that can test your operations. For example, payment processors usually hold funds for 2 to 7 business days [7], which can create immediate cash flow gaps. Add to that refunds and chargebacks, and liquidity can quickly become a concern.

Managing inventory becomes trickier as well. Larger order volumes post-funding can lead to over-investing in stock, tying up capital unnecessarily. Conversely, under-investing can result in stockouts, especially during peak seasons. For seasonal businesses, the stakes are even higher - some generate 30% to 50% of their yearly revenue during the holiday season [7]. This makes precise planning essential.

Operational costs can also spiral faster than expected. Shipping alone can consume 10% to 20% of total revenue [7], and unexpected surges in costs can strain budgets further. On top of that, customer acquisition costs (CAC) often rise as marketing budgets expand. Kimberly Burghardt from Clearco highlights a critical pitfall:

Prioritizing short-term growth metrics to satisfy investors may divert focus from the company's long-term vision, customer satisfaction, and financial sustainability, possibly jeopardizing the company's future. [9]

Debt can also become a significant issue. High-interest loans or merchant cash advances taken to fuel rapid growth risk over-leveraging your business. Chris Allen, SVP of Marketing at Heartland, explains:

You need money for stock and marketing before you make sales, which can lead to a cash shortage. This problem can slow you down, making it hard to meet customer demand and keep growing. [8]

Balancing debt-to-revenue ratios is critical as you scale. Recognizing these risks early gives you the chance to make adjustments and protect your cash flow, which is explored further in later sections.

Spotting Early Warning Signs

Keeping an eye on specific operational metrics can help you identify risks before they escalate. For instance, a drop in inventory turnover (calculated as COGS divided by average inventory) suggests that capital may be tied up in slow-moving products.

Delays in paying suppliers are another red flag. If payment terms are consistently extended, it could point to cash flow struggles. Similarly, a noticeable gap between forecasted and actual sales - especially during peak demand periods - can leave you with excess inventory and financial strain.

Refunds and chargebacks also deserve close monitoring. In 2022, eCommerce businesses lost over $40 billion to payment fraud, with fraud accounting for about 3% of total annual revenue [10]. A sudden increase in these metrics could signal product quality issues or fraudulent activity, both of which can quickly drain resources.

These warning signs underscore the importance of thorough downside planning and stress testing to navigate potential challenges effectively.

Managing Cash Flow and Planning for Contingencies

Once you've pinpointed key operational risks, the next step is managing cash flow effectively to keep things running smoothly during challenging periods.

Creating a Weekly Cash Flow Budget

A weekly cash flow budget acts like an early warning system, helping you spot potential issues before they spiral out of control. Start by forecasting revenue based on historical conversion rates and traffic data. Keep a close eye on both organic (SEO) and paid (PPC) search performance, as these are major drivers of sales [11].

Don't forget to account for reverse logistics by setting aside a reserve for returns. With nearly 30% of online purchases being returned, this is a critical step [12].

Shift your focus toward customer retention instead of putting all your energy into acquiring new customers. Why? Returning customers tend to spend up to 30% more than new ones and are up to 70% cheaper to retain [11]. For example, email marketing can be a powerful tool - open rates typically range from 20% to 30%, and click-through rates hit around 25%. Even cart abandonment emails, when sent within 3–6 days, can recover roughly 30% of lost sales [11].

Tracking key metrics weekly is essential. As Fadi Shuman puts it:

Measure and track everything [11].

Keep an eye on conversion rates, customer acquisition costs, and checkout friction. Reducing cart abandonment can improve cash inflows without requiring additional marketing spend [11][12].

These insights can also help you choose financing options that offer flexibility when needed.

Using Flexible Repayment Options

Revenue-based financing can provide breathing room during tough times. This option ties repayments to a percentage of sales, meaning your debt obligations automatically decrease when revenue dips [3]. It’s a practical way to keep operations flexible without being locked into fixed monthly payments [3].

To make informed decisions, model three different lender scenarios and evaluate their impact on cash flow over a 12- to 36-month period [3]. Pay close attention to Net Income Margin and Contribution Margin to ensure repayment plans don't hurt profitability [3]. A Financial Planning and Analysis Manager at Denny's highlighted the value of this approach:

In just hours, we can model scenarios to understand what the organization will look like 12 months from now. It's valuable [6].

Set clear triggers - like a specific percentage drop in market demand - that signal when to activate contingency budgets or seek emergency financing [5][13].

Aligning repayments with revenue keeps your business nimble and better prepared for unexpected challenges.

Reducing Costs

Cutting costs strategically helps maintain stability without stifling growth. Start by diversifying your supplier base. Having at least two backup sources for critical components ensures production continuity and avoids costly rush fees during disruptions [3].

Negotiate flexible contracts with vendors so you can make adjustments without hefty penalties. Staged investments and scalable production options can also help you avoid excess inventory if demand suddenly slows down [13]. Organize your budget into essential and discretionary categories, making it easier to shift spending during downturns [13].

Adopt phased recruitment strategies that can be ramped up or paused depending on market conditions, reducing the risk of overcommitting to fixed labor costs [6]. Cross-training employees is another smart move - it allows you to reallocate staff between projects as needed [13]. Companies that modernized their financial processes, like Public Trust cutting its budget cycle by 20 days or Denny's reducing its annual budgeting by 25% while generating 60% more "what-if" scenarios, show how proactive planning can lead to greater financial agility [6].

Stress Testing Debt and Financial Obligations

Once you've secured your cash flow, the next step is to test how well you can handle debt obligations during tough times. This process goes beyond just protecting your cash flow - it dives into how much financial strain your business can take before debt becomes unmanageable.

Evaluating Debt Service Capacity

A key metric to assess here is your Debt Service Coverage Ratio (DSCR), which measures whether your cash flow is enough to cover loan payments. To calculate it, divide your Net Operating Income by your total debt service (principal plus interest). A DSCR above 1.25 is considered solid, while anything below 1.0 indicates you're falling short on meeting your obligations.

To prepare for downturns, simulate a 30% drop in sales and recalculate your DSCR monthly. If it dips below 1.2, it's time to activate contingency plans. Additionally, set aside a dedicated cash buffer - somewhere between $50,000 and $250,000 - to cover at least three months of debt payments. Here's why this matters: during the 2022–2023 economic slowdown, eCommerce companies with DSCRs below 1.2 saw default rates jump to 15%, compared to just 5% for those above that threshold.

Tools like Excel can help you model different scenarios, testing how revenue declines could impact your ability to stay afloat. The goal? Ensure your reserves are sufficient to keep operations running even under significant pressure. [14]

Tracking Survival Metrics

Beyond DSCR, there are other survival metrics to keep an eye on. These indicators can help you pinpoint when adjustments are needed to avoid crossing critical financial thresholds. For instance:

- Make sure your lowest bank balance covers at least 60 days of essential expenses - around $75,000.

- Maintain a runway of over 12 months and set up automated alerts for any covenant limits.

- Monitor covenant compliance closely, aiming for a current ratio above 1.5 and a debt-to-EBITDA ratio under 3x.

Take this example: a $5 million-funded apparel company used these metrics to spot a potential covenant breach early. By cutting back on inventory purchases, they extended their runway from four months to eight. During slower sales periods - like when holiday revenue falls 15% short of projections - tools like QuickBooks or custom Google Sheets dashboards with automated alerts can act as your early warning system. [14]

Communicating with Lenders

Open and proactive communication with lenders is crucial, especially before missing any payments. Regular updates can help you avoid defaults and even secure flexible options like payment deferrals or covenant resets. For instance, monthly check-ins with Onramp Funds, which offers revenue-based financing with repayments tied to 10–15% of sales, can strengthen your relationship with your lender. Research shows that 80% of flexible repayment terms come from relationships built before financial stress hits.

If your metrics start slipping, share your DSCR and runway dashboards with lenders. Combine these insights with the results of your stress tests to have informed discussions. For example, a DTC beauty brand with $3 million in funding faced a 25% drop in sales due to supply chain delays. By sharing weekly cash flow forecasts with their lender, they negotiated a three-month principal deferral, stabilizing their DSCR at 1.3. [14]

Setting Up Monitoring and Adjustment Processes

Once you've stress-tested your debt and obligations, it's time to establish a system that keeps your financial health on track. In eCommerce, conditions can shift rapidly, so having a dynamic monitoring process ensures you can adapt quickly. Regular reviews and flexible adjustments are essential to catch potential problems early and address them before they grow. A good starting point is conducting quarterly financial reviews to recalibrate your plans for upcoming events.

Quarterly Financial Scenario Reviews

Every three months, set aside time to revisit and refine your financial models. Instead of relying on a single forecast, scenario analysis allows you to explore multiple outcomes: a base case (normal operations), a worst case (unexpected challenges), and a best case (ideal growth). This approach helps you prepare for a range of possibilities rather than banking on one prediction.

Focus your reviews on specific, near-term events rather than trying to account for every possible detail. For instance, if you're planning a new product launch in Q3 or gearing up for the holiday season, adjust variables like customer demand or shipping costs. Assign probabilities to potential risks, such as supply chain disruptions or seasonal demand spikes, to better prepare.

Take Jazzi McGilbert's experience as an example. By updating her financial scenarios quarterly, she was able to adjust her lease strategy and safeguard her business from significant losses. This highlights the importance of tailoring your reviews to major events like product launches or seasonal peaks.

Analyzing Cost Sensitivity

After updating your scenarios, dig deeper into which costs have the biggest impact on your bottom line. Cost sensitivity analysis helps you pinpoint how specific factors - like fluctuating shipping rates or increased marketing expenses - affect profitability. By modeling these variables, you can make smarter decisions when facing downturns.

Use tools like spreadsheet software to test different assumptions and see how changes in costs or revenue play out. For example, consider how your margins would shift if your main logistics provider went out of business or if advertising rates surged. Preparing for these scenarios ahead of time ensures you're not blindsided when market conditions change. Be sure to update your models whenever there's a significant shift, such as new regulations or changes in consumer behavior.

Building Contingency Budgets

Set aside 5–10% of your budget for unexpected expenses or revenue shortfalls. This reserve isn't just a safety cushion - it's an active tool that requires regular monitoring and adjustments. While industries like construction may need a larger contingency (around 15%) due to fluctuating costs, eCommerce businesses can usually manage with a smaller reserve. [15][17]

To calculate your contingency fund, multiply the likelihood of an event by its potential financial impact rather than relying on arbitrary percentages. For example, if there's a 30% chance of your website crashing during Black Friday, which could result in $100,000 in lost sales, allocate $30,000 for that risk. As uncertainties decrease - like securing a stable supplier - you can reallocate any unused funds. [16]

It's also important to set clear rules for accessing these funds. Define approval processes and establish trigger points based on key metrics, such as a significant drop in revenue or operational disruptions. This ensures accountability while allowing you to act quickly when emergencies arise. [15][18]

Conclusion

Once you've tackled cash flow issues and debt management, the next step is ensuring your business's long-term stability. Securing funding is just the beginning - it’s how you manage that capital that truly matters. Smart financial planning and risk management are essential tools, not optional add-ons. By creating base, upside, and downside scenarios, you replace uncertainty with actionable insights, helping you spot potential problems before they escalate.

Tools like weekly cash flow budgets and debt stress testing give you the ability to handle uncertainty with confidence. As Jared Sorensen from Preferred CFO wisely notes:

The goal is not to predict the storm perfectly. The goal is to ensure that when it arrives, the company is ready - not scrambling, not surprised, and not paralyzed. [19]

This proactive mindset separates businesses that endure challenges from those that falter. Throughout this discussion, we’ve seen how scenario planning, disciplined budgeting, and active risk management are at the core of financial resilience.

Take, for example, Jazzi McGilbert’s thoughtful strategy when launching Reparations Club. By preparing for worst-case scenarios while also seizing growth opportunities, she turned her vision into a seven-figure business in just three years. [1]

In unpredictable times, overconfidence without preparation can be a dangerous gamble. [19] Whether it’s supply chain hiccups, sudden sales spikes, or seasonal slumps, having a well-thought-out plan allows you to act quickly and strategically. Regularly reviewing scenarios, maintaining contingency budgets, and setting clear action points ensure you’re always ready to adapt as circumstances shift.

Start incorporating these strategies today. The businesses that succeed aren’t the ones that avoid challenges - they’re the ones that anticipate them and respond with precision.

FAQs

What should I include in a downside scenario model?

A downside scenario model is all about preparing for the unexpected. Here’s what it should cover:

- Risk Assessment: Pinpoint potential threats, such as an economic slump or disruptions in the supply chain. Knowing where vulnerabilities lie is the first step in addressing them.

- Scenario Planning: Map out conservative projections to understand how tough conditions could affect cash flow and daily operations. This helps you see the bigger picture during challenging times.

- Financial Contingency Plans: Have a game plan for emergencies. This might mean securing backup funding, reworking budgets, or ensuring there’s a financial cushion to fall back on.

- Business Continuity Plans: Develop strategies to keep the business running smoothly during a crisis. This includes setting up response protocols and ensuring clear communication channels.

By covering these bases, you can better anticipate and navigate potential hurdles, keeping operations steady even when things get rough.

How do I pick the right cash reserve amount after funding?

To determine the right cash reserve for your business, start by analyzing your cash flow forecast. Look at factors like seasonal trends, potential payment delays, and unplanned expenses. A good rule of thumb is to have enough to cover 3-6 months of operating expenses, but this should be adjusted based on how variable your business is and your comfort level with risk.

Focus on critical areas such as inventory management, marketing efforts, and technology investments when allocating your reserve. Keep an eye on key performance metrics regularly to fine-tune the amount you set aside. The ultimate goal is to strike a balance between maintaining financial security and pursuing growth opportunities.

What numbers warn me fastest that cash will get tight?

Significant drops in cash inflows or sudden spikes in outflows are often the first signs of cash flow trouble. These could show up as delayed payments from customers or unplanned expenses that catch you off guard. To stay ahead of these issues, it’s important to keep a close eye on your cash flow forecasts and monitor key metrics like net cash flow and ending balances. Regular reviews can help you identify potential problems early, giving you time to act and keep your finances on track.