Securing funding can either help your business grow or cause financial strain. To make the right decision, you need to carefully evaluate your cash flow, operational readiness, and potential return on investment (ROI). Here’s what you should focus on:

- Cash Flow Health: Ensure your business can handle repayments without stress. Track metrics like debt-to-revenue ratio, monthly revenue consistency, and working capital needs.

- Operational Readiness: Confirm that your systems, team, and supply chain can scale efficiently. Problems like stockouts, high return rates, or outdated infrastructure can hinder growth.

- ROI Projections: Calculate the financial benefits of funding. Use historical sales data, scenario planning, and sensitivity analysis to estimate revenue growth and ROI.

- Funding Options: Choose the right type of funding - options include revenue-based financing, bank loans, SBA loans, merchant cash advances, and equity financing. Each has unique costs, repayment terms, and risks.

- Stress Risks: Avoid using funding to cover daily expenses or mask deeper financial issues. Build a cash reserve and tighten credit policies to ensure stability.

How To Fund Your Ecommerce Business For Cheap (Or Even Free)

sbb-itb-d7b5115

Check Your Cash Flow Health

Before diving into any funding decisions, it’s crucial to evaluate whether your business can handle the repayments. Many eCommerce sellers overlook the actual movement of cash, which can lead to financial stress when funding is added to the mix.

To start, remember that revenue is not the same as cash. Payment processors often hold funds for 2–7 business days, and unexpected outflows like refunds or chargebacks can hit weeks after a sale [4]. For instance, if your monthly sales hit $50,000 but your cash balance is consistently near zero, it’s a red flag. Monitoring the right cash flow metrics can help you determine whether your business is in a position to take on additional debt.

Key Cash Flow Metrics to Track

Strong cash flow is essential for supporting growth funding. Start by looking at your debt-to-revenue ratio, which indicates how much of your revenue is going toward debt repayment. Test this ratio under potential scenarios, such as a 20% drop in sales or rising shipping costs [4].

Next, assess your monthly revenue consistency over at least six months. If 30–50% of your annual revenue comes during the holiday season [4], you’ll need to factor in these fluctuations when planning for debt repayments.

Another critical area is your working capital requirements. Inventory and customer acquisition costs often tie up cash before you see revenue [4]. For example, if shipping eats up 10–20% of your revenue and marketing expenses are high, calculate how much liquid cash remains after covering these essentials. This leftover cash represents your true repayment capacity. A predictable customer base is also key to maintaining steady cash flow.

What Healthy Cash Flow Looks Like

Understanding these metrics is essential before seeking new funding. Healthy cash flow ensures you can cover daily operations, pay suppliers on time, fund inventory cycles without stress, and still have reserves for unexpected challenges.

A strong cash position is evident when positive net income translates to actual cash in your bank account - not just on paper. Your cash flow statement’s ending balance should align with your balance sheet [2]. If there’s a mismatch, it’s a sign to tighten up your financial tracking before taking on more debt.

Businesses with a loyal customer base - where 5–20% of customers generate 80–95% of revenue - tend to have more stable cash flow, making them better equipped for loan repayments [3]. This kind of stability is something lenders look for.

Finally, healthy cash flow often reflects good supplier relationships. Negotiating favorable terms or flexibility can help during tight periods. Paying suppliers upfront while waiting on payment processor releases can create cash gaps that additional funding might exacerbate [4].

Evaluate Your Operations and Ability to Scale

Once your cash flow is solid, it’s time to take a closer look at whether your operations can support growth. Revenue alone isn’t enough to prove you’re ready. You’ll need to dig into your systems, team, and infrastructure to ensure they can handle the demands of scaling up.

Is Your Business Ready to Grow?

Start with your unit economics, like Customer Acquisition Cost (CAC) and Lifetime Value (LTV). If you’re spending heavily on marketing but operating with slim margins, it’s a warning sign that scaling might be tough.

Next, think about inventory management. Can you forecast demand accurately and maintain stock without tying up too much cash? Businesses that frequently deal with stockouts or excess inventory will struggle even more as order volumes rise. High return rates or chargebacks are another red flag - they often point to issues with fulfillment or customer experience. These problems can make lenders reluctant to provide funding [3].

Consistent sales data is a strong indicator of operational discipline. Once you’ve confirmed that your business is steady, assess whether your current systems can scale efficiently if you secure additional funding.

Can You Scale with Funding?

Scalability isn’t just about growth - it’s about growing in a way that doesn’t cause your operational costs to skyrocket [1]. To do this, you’ll likely need to invest upfront in areas like staffing, technology, and supply chain infrastructure to prevent bottlenecks [4]. Can your team and systems handle double the workload without breaking down?

Your tech stack and supply chain should also be ready to support higher volumes without driving up costs. For eCommerce businesses, shipping alone can eat up 10–20% of total revenue [4]. If your fulfillment workflows aren’t optimized, these costs can spiral. For example, Atomix Logistics uses a pod model to streamline operations and offers a $1,000 Fulfillment Credit after completing 500 orders, helping businesses manage the financial burden of scaling [1]. If your current fulfillment partner can’t handle higher volumes or you’re paying too much for small shipments, scaling could strain your margins.

Sometimes, operational constraints force businesses to become more efficient. Robert Hamm, CEO of HatLaunch, shared:

"I think it makes us a stronger business. We have to be scrappy. We have to execute. We have to use our capital in a do or die fashion and not waste it."

This kind of discipline can drive innovation and clarity, while too much capital can lead to wasteful spending [6]. Before seeking large funding, make sure your operations are lean and capable of using that capital effectively, rather than covering up inefficiencies.

Calculate Expected Growth and ROI

Before diving into funding decisions, it's crucial to estimate your revenue and calculate your ROI. This ensures that the capital you secure will fuel growth rather than create unnecessary financial strain.

Project Your Sales and Revenue Growth

Start by analyzing your historical sales data. Look for trends such as month-over-month growth, seasonal highs, and the products that consistently generate the most revenue. For many eCommerce businesses, June and July alone can account for 30–40% of their annual revenue [10]. If you're planning to secure inventory funding, keep in mind that overseas production often takes between 75 and 140 days [10]. Missing key ordering windows - like placing orders ahead of Chinese New Year - could mean losing out on an entire year's worth of growth opportunities [10].

To prepare for different outcomes, create three scenarios: Base, Downside, and Severe Downside [8]. For instance, if your Base Case forecasts $1 million in revenue with standard marketing efforts, your Downside might predict $600,000 (60% of the target) with a 20% cut in marketing. Your Severe Downside could drop to $300,000 (30% of the target) with a complete hiring freeze [8]. This kind of planning helps you prepare for slower-than-expected growth.

Focus on the key metrics that drive your business: traffic, conversion rates, Average Order Value (AOV), and Cost of Goods Sold (COGS) [8]. If you're using funding to boost marketing, make sure your website is optimized for conversions first. Increased traffic won’t help if your checkout process is clunky or your site is slow to load [9]. Also, align your marketing budget with your inventory levels - running ads when you're out of stock not only wastes money but can also alienate customers. Studies show that 43% of shoppers will permanently switch to a competitor if the product they want is unavailable [10].

Once you’ve mapped out growth projections, the next step is to connect those numbers to actual financial returns.

Calculate Your Return on Investment

After outlining your operational goals, take the time to quantify the potential financial benefits by calculating ROI for your funding plans. For inventory purchases, calculate how much additional revenue the stock will generate compared to its cost. For marketing investments, monitor your Customer Acquisition Cost (CAC) relative to Lifetime Value (LTV) to ensure you're not overspending to gain customers who won’t bring in enough profit.

Use sensitivity analysis to understand how changes in key variables impact your ROI [8]. For example, how would a 10% drop in conversion rates affect your returns? What if your supplier raised their prices by 15%? Testing these variables one by one helps you identify the factors that have the biggest influence on your ROI. You can also apply reverse stress testing to determine the exact point where your business becomes unsustainable. This helps you pinpoint the minimum return you need to stay operational [8].

Investors often use metrics like cash-on-cash multiples and Internal Rate of Return (IRR) to evaluate ROI [5]. Timing is another critical factor - payment processors typically hold funds for 2–7 business days [4], which can delay your ability to reinvest or repay debts.

Real-world examples highlight the impact of ROI-focused decisions. In 2024, DAVAN Strategic used funding to place major inventory reorders and expand their distribution through Amazon fulfillment centers. By leveraging AI-powered financial planning tools and flexible capital, they hit $1 million in sales in just one week [7]. Similarly, Jake Chambers, owner of Pupsentials, invested in high-end Japanese embroidery machines costing $40,000–$50,000 each. This allowed him to fulfill orders faster, boosting monthly sales from $20,000–$50,000 to $100,000–$200,000 [7]. These cases demonstrate how targeted investments can deliver measurable growth when guided by solid ROI calculations.

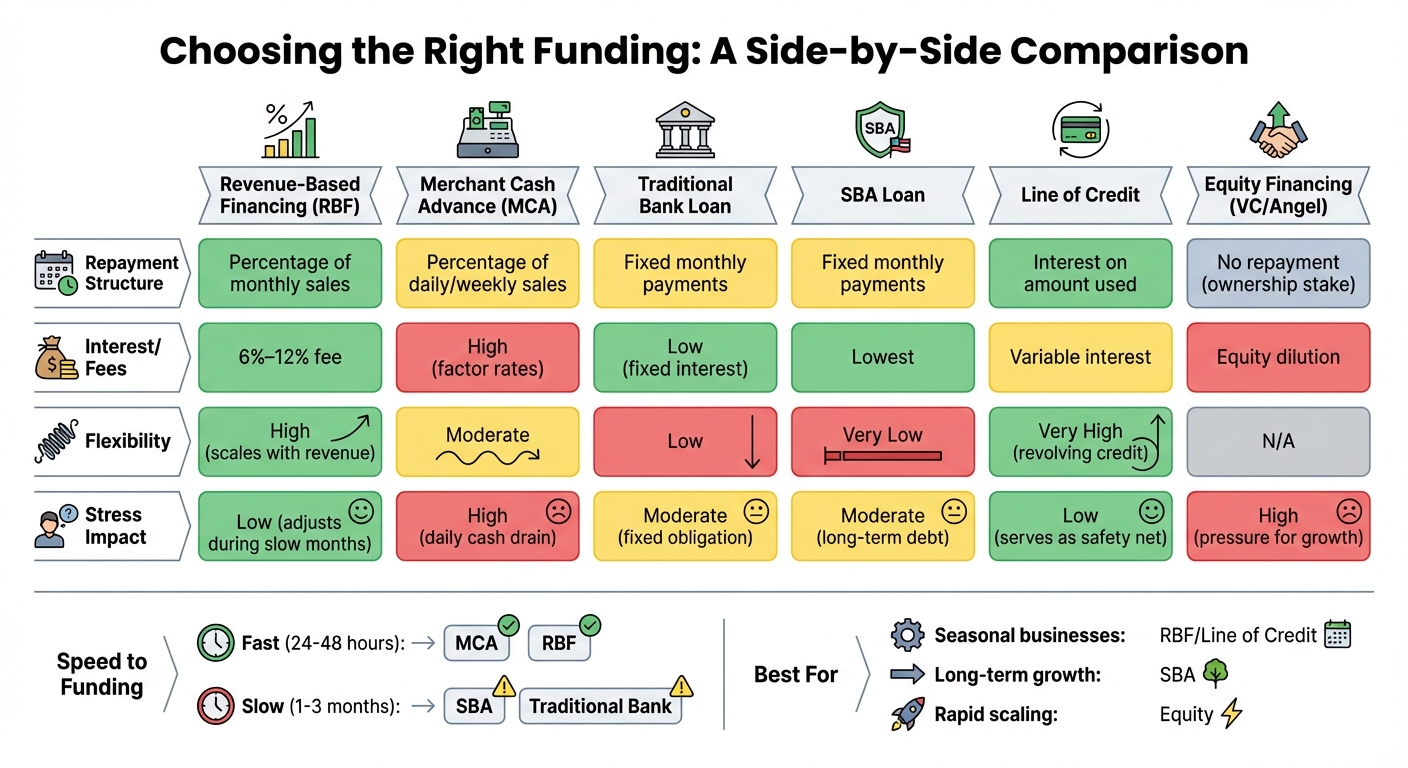

Compare Different Funding Options

Business Funding Options Comparison: Repayment Terms, Costs, and Stress Impact

Once you’ve outlined your ROI and growth projections, the next step is finding a funding option that matches your business needs and goals.

Types of Funding to Consider

There’s no one-size-fits-all solution when it comes to funding. Each option has its own repayment terms, costs, and benefits. Here’s a breakdown:

- Revenue-Based Financing (RBF): This option ties repayments to a percentage of your monthly sales (typically 5%–25%). Payments automatically adjust based on your revenue, making it a great fit for businesses with seasonal sales or fluctuating cash flow [12].

- Traditional Bank Loans: These provide a lump sum with fixed monthly payments and typically lower interest rates. However, approval can take weeks or months, and banks often require strong credit scores and collateral [11][12].

- SBA Loans: Small Business Administration (SBA) loans offer low interest rates and long repayment terms - up to 25 years. The average loan size is around $370,000, but the application process can be lengthy, often taking 60 to 90 days [12][14].

- Merchant Cash Advances (MCAs): MCAs provide quick funding (sometimes within 24 hours), but repayments are deducted daily or weekly, often at a higher overall cost [12].

- Asset-Based Lending: This type of funding uses assets like inventory or unpaid invoices as collateral, making it useful for businesses needing capital for bulk purchases or short-term supply needs [12][14].

- Business Line of Credit: A line of credit offers flexibility by letting you borrow as needed and pay interest only on the funds you use. It’s ideal for covering unexpected expenses or seizing new opportunities [12].

- Equity Financing: Venture capital or angel investors provide funding without requiring monthly repayments. However, this comes at the cost of giving up partial ownership and often includes pressure to achieve rapid growth [11][13].

For example, the founders of Glitch Energy scaled their business from $0 to seven figures in just one year by opting for flexible funding rather than venture capital. This choice allowed them to retain full ownership and autonomy [11].

Paul Voge, Co-founder and CEO of Aura Bora, highlighted the importance of strategic funding in managing inventory:

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital." [12]

Side-by-Side Funding Comparison

The table below summarizes key funding options based on repayment terms, costs, and their impact on your business:

| Funding Type | Repayment Structure | Interest/Fees | Flexibility | Stress Impact |

|---|---|---|---|---|

| Revenue-Based Financing | Percentage of monthly sales | 6%–12% fee | High (scales with revenue) | Low (adjusts during slow months) |

| Merchant Cash Advance | Percentage of daily/weekly sales | High (factor rates) | Moderate | High (daily cash drain) |

| Traditional Bank Loan | Fixed monthly payments | Low (fixed interest) | Low | Moderate (fixed obligation) |

| SBA Loan | Fixed monthly payments | Lowest | Very Low | Moderate (long-term debt) |

| Line of Credit | Interest on amount used | Variable interest | Very High (revolving credit) | Low (serves as a safety net) |

| Equity (VC/Angel) | No repayment (ownership) | Equity dilution | N/A | High (pressure for growth) |

Key Considerations

Fast funding options, like MCAs and eCommerce-specific financing, can deliver funds in as little as 24–48 hours but often come with higher costs. On the other hand, SBA loans and traditional bank loans are more affordable but take longer to secure, often requiring one to three months.

If retaining full ownership is a priority, debt-based options such as loans, RBF, or lines of credit are better choices. However, if you’re open to giving up equity in exchange for capital, venture capital or angel investors can provide significant resources to fuel rapid growth [11][14].

Identify Stress Risks and Match Funding to Your Goals

Warning Signs of Financial Stress

Once you've evaluated your cash flow, it's crucial to keep an eye out for red flags that could indicate financial trouble. Did you know that poor cash flow management plays a role in more than 82% of business failures? [19] A good place to start is by calculating your cash runway: divide your current cash reserves by your net burn rate [8][15]. This will give you a clear picture of how long your business can operate with its existing resources. For context, many small businesses have just a 27-day cash buffer [19], leaving little room for error.

Some warning signs to watch for include using funding to cover everyday operating expenses rather than fueling growth, struggling to meet payroll without dipping into reserves, or consistently delaying payments to suppliers [16][17][19]. If you're leaning on credit to manage routine costs, it's a sign that your cash flow may be out of balance.

"If you're relying on credit cards and/or loans to cover everyday expenses, it's a sign that your cash flow is out of sync." - Commerce Bank [16]

Another key indicator is a declining LTV-to-CAC ratio, which suggests you're overspending on customer acquisition without seeing enough return. Similarly, an increase in accounts receivable can signal trouble. Late customer payments affect 48% of U.S. businesses [19], and this can create a liquidity gap. Addressing these issues is critical - additional funding might only mask deeper problems if your cash flow isn't aligned with your operations.

Match Funding to Your Business Goals

Once you've identified potential risks, it's time to ensure your funding strategy aligns with your business objectives. The type of funding you choose should directly support your goals. For instance, if you're gearing up for a seasonal sales spike and need to boost inventory, revenue-based financing could be a smart choice. This option ties repayments to your sales, offering flexibility during slower periods.

Before diving into aggressive growth, it's wise to build a financial cushion. Ideally, aim to have three to six months' worth of operating expenses in reserve [18]. This buffer can protect your business from unexpected downturns and give you breathing room to meet obligations. Additionally, tightening your credit policies can help improve cash flow. Options like requiring upfront deposits or offering small discounts for early payments can accelerate your cash cycle and reduce financial pressure [16][19].

Regular financial audits are also essential. If your operating costs are growing faster than your profits, it's time to trim non-essential expenses before taking on new funding [16][17]. The goal is for funding to enhance your business's strengths - not to cover up underlying weaknesses.

"Steady, predictable cash flow is the key to stability and avoiding financial stress." - Commerce Bank [16]

Conclusion

To decide if funding will drive growth or create challenges, take a close look at your cash flow, scalability, ROI, and financial risks.

Run stress tests on your financial models to ensure that your ending cash balances match your balance sheet projections [2]. Don’t forget to calculate the total cost of capital, factoring in origination fees, platform charges, and potential equity dilution. This can help you avoid unpleasant surprises down the road [3]. These steps reinforce the importance of the cash flow and ROI evaluations discussed earlier.

As mentioned previously, it’s vital to align funding with your business objectives. Tailor your funding choices to your company’s stage: seed funding works for validation, Series A/B is ideal for scaling, and revenue-based or inventory financing can address short-term needs [1][3].

Focus on achieving profitability that lasts. Investors are shifting their priorities, placing more emphasis on efficiency rather than unchecked growth [1]. By leveraging the tools and frameworks in this guide - like cash flow analysis and ROI metrics - you can make well-informed decisions that build your business without overextending it.

FAQs

How much debt can my business safely handle?

The level of debt your business can manage hinges on factors like cash flow, operational efficiency, and future growth objectives. It's essential to ensure that debt repayments align with your cash flow in a way that doesn't interfere with day-to-day operations or expansion plans. Take a close look at your cash flow, profit margins, and overall expenses to determine a debt level that feels manageable. A good rule of thumb? Keep debt payments below your available cash flow, allowing enough flexibility for operations and any unforeseen expenses.

What should I fix operationally before taking funding?

Before seeking funding, it's crucial to tackle any operational challenges that could slow down growth or create unnecessary stress. Take a close look at your processes, workflows, and infrastructure to confirm they’re ready to handle the demands of scaling. Prioritize updating outdated systems, creating dependable workflows, and strengthening your business’s overall resilience. An operational readiness assessment can be a helpful tool to spot weaknesses, ensuring your business is set up to make the most of new funding without running into bottlenecks or setbacks.

How do I stress-test ROI so funding won’t backfire?

To make sure your ROI holds strong and funding decisions don't backfire, dive into key metrics like revenue, expenses, and profit margins under different scenarios. For example, simulate what happens if growth rates slow down or costs rise unexpectedly. This helps you see if your ROI remains positive under pressure.

Set a clear benchmark for ROI - like a 5:1 ratio - to determine if the investment is worth pursuing. And don’t stop there. Keep your calculations up to date so your funding choices stay aligned with your growth objectives while keeping financial risks in check.