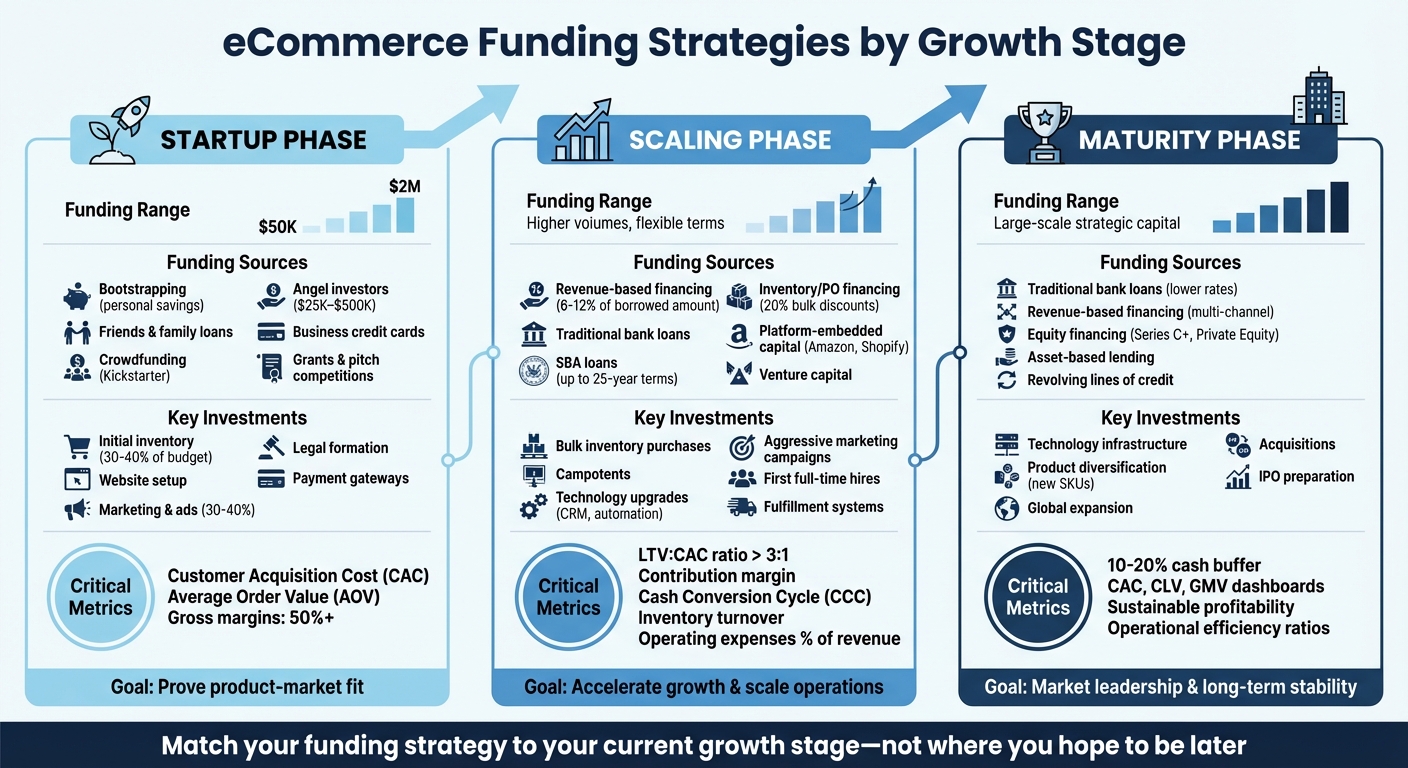

When running an eCommerce business, your funding needs evolve as you grow. Early-stage brands rely on small, quick funding options like personal savings or crowdfunding. As you scale, larger investments are needed for inventory, marketing, and technology upgrades. Mature brands require funding for global expansion and long-term stability, often through equity financing or loans. Here’s a breakdown of funding strategies at each stage:

- Startup Phase: Focus on proving product-market fit. Use personal savings, crowdfunding, or angel investments ($50K–$2M).

- Scaling Phase: Invest in inventory, marketing, and operations. Options include revenue-based financing, credit lines, or venture capital.

- Maturity Phase: Prioritize technology, product diversification, and market leadership. Funding sources include equity financing or long-term loans.

Key Metrics to Track:

- Startup: Customer Acquisition Cost (CAC), Average Order Value (AOV)

- Scaling: Lifetime Value (LTV) to CAC ratio > 3:1

- Maturity: Maintain a 10–20% cash buffer for stability

The right funding strategy depends on your growth stage. Align your financing with your business goals to maintain strong cash flow and avoid unnecessary debt.

eCommerce Funding Strategies by Growth Stage: Startup to Maturity

The 4 Stages In Your eCommerce Journey and the Key Challenges Along the Way

sbb-itb-d7b5115

Stage 1: Startup Phase – Getting Initial Funding

In the startup phase, the focus is on testing your idea and achieving product–market fit. Most eCommerce founders operate on tight budgets, launching their first product and generating just enough sales to fund the next inventory cycle. At this stage, funding sources are typically smaller and more accessible.

Where Startups Get Their First Funding

Bootstrapping is often the go-to strategy. Founders rely on personal savings, credit cards, or reinvested profits to keep ownership intact and expenses low. Once personal funds are depleted, many turn to friends and family. According to Entrepreneur Magazine, "the most common source of debt financing for start-ups often isn't a commercial lending institution, but family and friends" [4]. These loans or investments can range from a few thousand dollars to $50,000 or more. However, it’s crucial to formalize these arrangements in writing to avoid misunderstandings.

Crowdfunding platforms like Kickstarter allow startups to fund inventory while gauging market interest. A successful pre-order campaign can provide the capital needed for an initial inventory run.

Angel investors often step in after early traction is proven, offering funding between $25,000 and $500,000 in exchange for equity [7]. They invest based on potential rather than established results and typically expect a clear path to profitability with gross margins of at least 50% [6].

Business credit cards provide quick access to funds for smaller expenses like ad spend or initial inventory. However, their high interest rates make them less ideal for larger investments.

Some founders also explore grants and pitch competitions, which provide non-repayable funds. These are often geared toward innovative products or underrepresented entrepreneurs.

This initial funding serves as the foundation for operational and marketing efforts, which are critical at this stage.

What Startups Spend Money On

The first wave of funding typically goes toward legal formation, product design, setting up a tech stack (using platforms like Shopify or WooCommerce), and purchasing initial inventory. Marketing often consumes 30–40% of early budgets [7], covering paid ads, influencer collaborations, and social media campaigns to drive traffic and test customer acquisition strategies.

Inventory is the single largest expense and a significant cash flow challenge. Kemal Didic from Mercury highlights this, saying, "Inventory requires significant cash allocation. Build simple cash flow models for your sales cycle base case, as well as a sensitivity analysis to include upside and downside scenarios" [6]. Running out of stock can severely damage a new brand's reputation [10,15].

Investments in technology and logistics are also key. This includes payment gateways, CRM systems, analytics tools, and fulfillment systems to ensure smooth operations. Since payment processors may hold funds for 1–5 business days [6], careful planning of ad spend and restocking schedules is essential. The goal is to allocate just enough resources to validate product–market fit without overcommitting to infrastructure that’s not yet ready for scaling.

As your spending aligns more closely with revenue and cash flow stabilizes, you're signaling readiness for the next phase of growth.

Signs You're Ready to Move to the Next Stage

Once your initial funding and operations are in place, certain milestones will indicate you're ready to scale. Key signs include a consistent sales history, where revenue becomes predictable rather than reliant on one-off spikes [10,19]. Metrics like a lifetime value (LTV) to customer acquisition cost (CAC) ratio of 3:1 or better, and consistent inventory shortages due to high demand, are strong indicators [8,10,15].

Additionally, your operations - such as supply chain management, 3PL services, and customer support - should be stable enough to handle higher volumes. When these fundamentals are solid, you’re positioned to pursue larger funding options and accelerate growth.

Stage 2: Scaling Phase - Funding to Grow Faster

Once you've nailed down product-market fit and operational stability, it's time to focus on scaling. This phase requires funding to accelerate growth, manage larger capital needs, and adapt to your sales cycle. The goal is to build on your early milestones and push for aggressive expansion.

Funding Options for Growing Businesses

As your operations grow, so do your funding needs. Here are some options that align with the demands of scaling:

- Revenue-based financing (RBF): This option ties repayments to your sales performance. Instead of fixed monthly payments, RBF takes a percentage of your revenue - typically 6% to 12% of the borrowed amount [3]. This flexibility allows you to keep cash flow steady during slow months, giving you room to reinvest in growth.

- Traditional bank loans: While these loans often come with lower interest rates, they can be challenging during the scaling phase. Approval processes are slow, and fixed repayment schedules don't always align with fluctuating revenue. SBA loans, which offer repayment terms of up to 25 years [9], may be a better fit for brands with predictable cash flow.

- Inventory and purchase order financing: Ideal for bulk purchases, this type of funding can help you secure supplier discounts - sometimes up to 20% on large orders [9]. However, it works best when paired with more flexible capital solutions to support other areas like marketing and operations.

- Platform-embedded capital programs: Platforms like Amazon and Shopify offer quick access to funding, but their lack of flexibility and transparency can limit their usefulness for long-term growth. Increasingly, fintech lenders are stepping in with real-time data analysis from platforms like Shopify, Amazon, and Stripe to assess sales performance and provide tailored funding [1][8].

For example, Onramp Funds offers revenue-based financing specifically designed for scaling eCommerce brands. With funding available in as little as 24 hours, repayment terms adjust to your sales, and fees range from 2% to 8%. Their platform integrates with major eCommerce platforms like Amazon, Shopify, BigCommerce, and TikTok Shop, making it a convenient option for growing businesses.

Where to Invest During Growth

In this phase, your capital should be directed toward three critical areas: inventory, marketing, and technology. Each plays a key role in driving growth.

- Inventory: Use funding to secure bulk discounts and prepare for seasonal spikes. Maintaining consistent stock levels ensures you can meet demand, boost search rankings, and maintain sales momentum [8].

- Marketing: Before ramping up ad spend, ensure your unit economics are solid. A strong Lifetime Value (LTV) to Customer Acquisition Cost (CAC) ratio - ideally 3:1 or higher - is essential [12][13]. For instance, in 2019, the fashion brand Hedoine used $50,000 in revenue-based funding to scale Instagram and Facebook marketing campaigns. By the first quarter of 2020, their sales had grown by 1,106% [3].

- Technology: Invest in tools that enhance efficiency and customer experience. This might include automation software to speed up fulfillment, improved checkout processes to boost conversion rates, or advanced inventory management systems [9].

Paul Voge, Co-founder and CEO of Aura Bora, notes: "Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital" [9].

While inventory financing is great for stock replenishment, revenue-based financing is often better suited for marketing campaigns, as repayments scale with your sales [1][9].

Metrics to Track While Scaling

Tracking the right metrics ensures your growth is profitable, not just revenue-driven. Here are the key metrics to monitor:

- Contribution margin: This metric accounts for variable costs like advertising, shipping, and payment fees, providing a clearer picture of profitability as sales volume grows [11][12].

- Cash Conversion Cycle (CCC): Measures how quickly cash invested in inventory turns into revenue. A negative CCC is ideal - it means you're getting paid by customers before paying suppliers [10].

Simon Davis, Founder of SBO Financial, emphasizes: "Cash is the oxygen. You can have great sales, but if you're out of cash, the business will suffocate" [10].

- Inventory turnover: This indicates how efficiently your capital is moving through inventory. It's calculated by dividing Cost of Goods Sold by Average Inventory and should ideally increase as you scale [11].

- LTV:CAC ratio: Acquiring new customers is 5 to 7 times more expensive than retaining existing ones [14]. A strong LTV:CAC ratio (around 3:1) signals sustainable profitability and is often a key metric for Series A investors [12].

- Operating expenses as a percentage of revenue: According to Salesforce, scaling efficiently means increasing revenue without a proportional increase in expenses [14]. If your overhead grows at the same rate as your revenue, you're not scaling efficiently.

Stage 3: Maturity Phase - Funding for Market Leadership

By the time your brand reaches maturity, you've likely established predictable revenue streams, a loyal customer base, and efficient operations. The focus at this stage shifts toward achieving market leadership and ensuring long-term stability. The funding you secure should enable large-scale, strategic moves like international expansion, acquiring competitors, or preparing for a potential exit.

Funding Options for Established Brands

At this stage, mature brands have access to financing options that may not have been available earlier. Here are some of the key funding routes:

- Traditional Bank Loans and Lines of Credit: With a solid credit history and steady cash flow, these loans become more viable. They often come with lower interest rates and longer repayment terms. For instance, SBA loans can stretch up to 25 years [9]. However, the approval process can be slow, and repayments are fixed regardless of revenue variations.

- Revenue-Based Financing: This remains a flexible option, especially for managing seasonal sales fluctuations or multi-channel revenue streams. Platforms like Amazon, Shopify, BigCommerce, and TikTok Shop allow repayment terms to scale based on your actual sales, preserving cash flow for reinvestment.

- Equity Financing (Series C+ or Private Equity): If you're eyeing aggressive expansion or preparing for a major exit, equity financing can provide large capital injections. Beyond funding, this route often brings mentorship and valuable networks. However, it does result in permanent ownership dilution [15].

As Vaibhav Totuka of Qubit Capital notes: "Investors are no longer solely captivated by rapid growth; they now prioritize sustainable profitability" [15].

- Asset-Based Lending: For brands that manufacture their products, this option allows you to use machinery or equipment as collateral to secure funding at lower interest rates without giving up equity [3].

Once funding is secured, the next step is to channel it into strategic investments that drive growth and stability.

Long-Term Investments for Mature Brands

To maintain growth and competitiveness, mature brands should focus on three key areas: technology, product diversification, and global expansion.

- Technology Upgrades: Automating processes can reduce fulfillment times, minimize shipping errors, and enhance website performance. Investments in tools like checkout optimization and advanced cybersecurity can improve customer experience while cutting operational costs [9].

- Product Diversification: Expanding your product range requires capital to scale up SKU counts and fund larger production runs. Bulk purchasing can improve margins. For example, in 2026, Aura Bora used Brex's corporate credit solutions - offering credit limits 30 to 40 times higher than traditional banks - to finance large product runs without straining their working capital.

Paul Voge, Co-founder and CEO of Aura Bora, highlighted: "Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital" [9].

- Global Expansion: Entering international markets requires significant investment in logistics infrastructure and navigating local regulations. With US Direct-to-Consumer eCommerce sales projected to hit $212.9 billion in 2025 - a 16.6% increase from 2024 [15] - brands can leverage domestic success to expand globally while carefully managing risks like currency fluctuations and compliance challenges.

Preparing for Acquisition or Going Public

If you're positioning your brand for acquisition or an IPO, your funding strategy becomes a critical factor in showcasing operational stability and growth potential. Here's how to approach it:

- Equity Financing: Venture capital or private equity firms can inject the large sums needed for scaling while offering strategic guidance and networks. These funds can be directed toward logistics, technology upgrades, or international expansion [1][9].

- Revolving Lines of Credit: These can help manage cash flow during exit preparations, especially when dealing with seasonal fluctuations or unexpected expenses [9]. This is crucial, given the sharp 97% drop in D2C funding since its 2021 peak [15].

- Operational Improvements: Strengthen unit economics and address any operational inefficiencies. Tools like spend management software and automated bill pay can help maintain a strong credit history and ensure cash flow transparency - both critical during due diligence for acquisitions or IPOs [9].

- Tranche-Based Financing: Aligning capital draws with specific milestones, such as inventory production or marketing campaigns, can prevent over-leveraging while ensuring financial stability [16].

Finally, presenting key metrics like CAC (Customer Acquisition Cost), CLV (Customer Lifetime Value), and GMV (Gross Merchandise Value) in real-time dashboards can appeal to potential buyers or underwriters. Syncing storefront data with platforms like QuickBooks or Xero ensures a comprehensive and professional financial overview [1][2].

Matching Funding to Your Business Needs

Once you've laid the groundwork, the next step is ensuring that your funding aligns with your business investments. The trick is to match the type of capital you secure with the specific needs of your business at each stage. For instance, a startup purchasing its first inventory has very different funding requirements compared to a well-established company launching a new product line. Aligning these factors carefully not only protects your cash flow but also helps you avoid taking on debt that doesn't serve your goals.

How Funding Aligns with Business Investments

Your funding strategy should evolve alongside your business operations.

- Startup Phase: At this stage, about 30–40% of your expenses typically go toward purchasing initial inventory. The rest often covers website creation, basic marketing efforts, and fulfillment needs. Funding sources like bootstrapping, small business loans, or angel investments ranging from $50,000 to $2,000,000 are common. Metrics such as Customer Acquisition Cost (CAC) and Average Order Value (AOV) are critical for guiding your spending decisions here.

- Scaling Phase: When scaling, your focus shifts to larger inventory purchases, more aggressive marketing campaigns, technology upgrades (like CRM systems), and hiring your first full-time employees. Funding options such as revenue-based financing, lines of credit, or venture capital become more accessible. Maintaining a healthy Lifetime Value (LTV) to CAC ratio - ideally above 3:1 - is essential for sustained growth.

- Maturity Phase: At this point, priorities include investing in long-term technology infrastructure, launching new product lines, and pursuing market leadership initiatives. Larger funding sources like SBA loans or equity financing are often the best fit.

| Growth Stage | Key Investments | Aligned Funding Types | Key Metrics |

|---|---|---|---|

| Startup | Inventory, website, ads | Loans, crowdfunding ($50K–$2M) | CAC, AOV |

| Scaling | Marketing, team, fulfillment | Revenue-based financing, credit | LTV > 3× CAC |

| Maturity | Tech upgrades, new product lines | Equity, SBA loans | 10–20% cash buffer |

By aligning your funding to your stage and priorities, you can better manage your cash flow and make smarter financial decisions.

Tips for Managing Cash Flow

Strong cash flow management is the backbone of sustainable growth. Start by forecasting your 12-month cash outflows. This should include costs like COGS (Cost of Goods Sold), marketing expenses tied to your CAC, and platform fees. Add a 10–15% buffer to account for unexpected volatility. This approach helps you identify your actual financing gap and prevents over-borrowing.

- Match repayment structures to your revenue cycles: If your sales fluctuate seasonally, revenue-based financing can be a lifesaver. With this option, you repay a percentage of your sales, which helps protect cash flow during slower months. On the other hand, fixed monthly loan payments work better for businesses with steady, predictable revenue streams. Many revenue-based financing providers require at least $10,000 in monthly sales, with approval often available within 24 hours.

- Prepare your financial documents: Before applying for funding, gather essential paperwork like profit and loss statements, balance sheets, and cash flow projections. For startups, this might also include personal credit reports and three months of bank statements. These documents not only streamline the application process but also demonstrate your ability to repay.

- Avoid unsuitable debt: Compare the true cost of different funding options carefully. Watch out for warning signs like high CAC without corresponding LTV growth, markets that need more than a 20% cash buffer, or restrictive loan terms. If your financing gap still exceeds your revenue projections after adding buffers, explore non-dilutive options like grants or crowdfunding before committing to more debt.

Cash flow issues are a leading cause of small business failures - accounting for over 80% of closures. Staying disciplined with your funding strategy and cash flow management can make all the difference [5].

Conclusion: Choosing the Right Funding for Your Growth Stage

Your approach to funding should evolve alongside your business. Early on, eCommerce brands often lean on personal savings, small business loans, or angel investors to cover initial expenses like inventory and marketing. As growth picks up, options like revenue-based financing or venture capital become more suitable, helping fund larger marketing efforts and technology improvements while maintaining healthy LTV-to-CAC ratios above 3:1. For established brands, larger financing solutions are often necessary to support long-term investments, such as launching new product lines or securing market leadership. The key is aligning your funding strategy with the specific needs of your growth stage.

Choosing the wrong funding can create challenges, whether through excessive equity dilution or rigid repayment terms that disrupt cash flow. Your business metrics can help guide your decisions. For example, if your revenue is under $5,000 per month, you’re likely in the startup phase. On the other hand, if you’re seeing consistent growth and an LTV that’s three times your CAC or more, you’re well-positioned for scale-focused funding options.

Revenue-based financing offers a flexible option for businesses at various stages. Repayments are tied to your actual sales - typically 5–10% of daily revenue - helping you manage cash flow during slower periods while automatically scaling as your business grows.

Take a close look at your cash flow for the next 12 months, adding a 10–20% buffer for unexpected costs, to identify your funding gap. Consider factors like interest rates, repayment terms, and eligibility requirements. For instance, if your monthly sales exceed $3,000 and you need capital that grows with your business without sacrificing equity, Onramp Funds provides revenue-based financing with fast approvals (often within 24 hours) and transparent fees ranging from 2–8%.

The bottom line? Match your funding strategy to your current stage of growth. Evaluate your metrics, outline your cash needs, and choose financing that fits where your business is today - not where you hope it will be later.

FAQs

How do I know which growth stage my eCommerce brand is in?

To figure out where your eCommerce brand stands in its growth journey, take a close look at key factors like revenue, cash flow, and operational priorities.

- Startup or early growth: At this stage, the focus is all about proving your product's value and keeping cash flow steady. Every dollar counts, and resources are often tight.

- Scaling: Brands here are working on growing their inventory and ramping up marketing efforts to reach a broader audience.

- Mature: This phase is about maintaining steady growth, achieving profitability, and investing in infrastructure to support long-term success.

By examining your financial health and aligning it with your business objectives, you can pinpoint your current stage and plan your next steps.

What funding option best fits seasonal or uneven sales?

Revenue-based financing (RBF) works perfectly for businesses with seasonal or fluctuating sales. With this model, repayments adjust based on your revenue - higher payments during peak months and lower ones during slower times. This flexibility ensures your funding aligns with your cash flow, making it simpler to handle expenses during unpredictable sales cycles.

How much cash reserve should I keep before taking on new funding?

Maintaining cash reserves sufficient to cover 12 to 18 months of operating expenses is a smart move. This cushion allows you to manage critical needs - like inventory, marketing efforts, and day-to-day operations - without putting your cash flow at risk, especially when you're in the process of securing additional funding.