As your business grows, so do its funding needs. Early on, personal savings or small-scale investments might suffice. But as you scale, you'll need larger, more flexible funding sources to handle inventory, marketing, and infrastructure. Here's a quick breakdown of how funding evolves across different business stages:

- Startup Phase: Founders often bootstrap or rely on personal savings, with typical startup costs around $10,000.

- Initial Growth: Revenue-based financing or small loans help manage cash flow and fund inventory expansion.

- Scaling: Venture capital becomes critical for aggressive growth, with Series A funding often exceeding $11 million.

- Maturity: Late-stage funding like private equity or venture debt supports acquisitions, international expansion, or exit strategies.

The key is aligning your funding strategy with your business stage. Early on, non-dilutive funding like micro-grants or revenue-based financing protects ownership. Later, equity investments bring the capital needed for larger growth initiatives but require giving up some control. Understanding your stage and funding options ensures you can grow without compromising your financial stability or long-term goals.

Understanding Funding Stages

sbb-itb-d7b5115

Stage 1: Pre-Launch and Early Validation

At this stage, the focus is on confirming that your product fits the market, all while keeping your financial risk as low as possible. Early-stage funding is about proving there's demand for your idea before seeking outside investments or taking on debt. To start, rely on personal funds and income from initial sales.

Bootstrapping and Personal Savings

Bootstrapping is all about using your own savings and reinvesting early sales revenue into the business. This gives you full control over decisions and timelines, but it also puts your personal finances on the line.

Many founders keep their day jobs or sell personal assets to cover initial costs like inventory and website creation. Some even consider using retirement accounts. If that's on your radar, options like ROBS (Rollover for Business Startups) let you tap into retirement funds penalty-free - but it’s a high-risk move with potential long-term consequences for your financial future [10].

If you turn to friends and family for funding, be sure to use formal agreements to define terms clearly and avoid misunderstandings [5][11]. While this method is quick and straightforward, it can strain personal relationships if the business doesn’t succeed [12][13].

Once you’ve maxed out personal funds, it’s time to look at other non-dilutive funding options.

Micro-Grants and Small-Scale Funding

Non-dilutive funding allows you to raise money without giving up ownership in your company. Micro-grants from government agencies, nonprofits, or corporations fit this category. They’re highly competitive but come with almost no financial risk since you don’t have to repay them [10][12]. Business competitions also fall into this category, offering awards ranging from a few thousand dollars to as much as $250,000 in pre-seed funding [5][11].

Crowdfunding platforms like Kickstarter or Indiegogo are another great option. Not only do they help you raise small amounts from a large number of backers, but they also act as a litmus test for your product. If people are willing to prepay for your idea, that’s solid proof of market demand [10][12].

Microloans, typically under $50,000, are another route. These loans often come from nonprofit or community lenders and have more flexible credit requirements than traditional banks [10][2]. Platforms like Kiva and Accion base their decisions on your business plan and revenue potential rather than just your credit history [15][14].

Key Metrics for Early-Stage Funding

Tracking the right metrics not only boosts your credibility with potential funders but also lays the groundwork for securing larger investments down the line. Metrics like partnerships, user growth, monthly active users, and customer acquisition costs (CAC) show that you’re capable of executing your vision [14]. Increasingly, alternative lenders and fintech platforms prioritize digital metrics - like customer reviews and sales history - over traditional credit scores [16].

Before you seek external funding, validate your idea with a Minimum Viable Product (MVP) to confirm there’s real demand [2]. Keep tabs on your CAC and early sales data, even if they’re modest. Build a financial safety net to cover three to six months of operating costs, and set aside 5%–10% of your budget for unexpected expenses [14]. These steps show funders that you’re financially prepared to launch and grow an eCommerce business.

Stage 2: Product-Market Fit and Initial Growth

After navigating the lean operations and bootstrap funding of Stage 1, Stage 2 is where you shift gears. With your product validated and sales becoming more consistent, the focus now turns to scaling operations. This stage requires more substantial funding to support growth, especially for managing cash flow, restocking inventory, and expanding marketing efforts. In 2020, the U.S. eCommerce industry generated $789 billion in revenue and was forecasted to exceed $1.1 trillion by 2024 [6]. Yet, nearly 90% of eCommerce businesses fail within their first 120 days, with cash shortages being a leading cause [17]. As you move past early validation, you’ll need flexible financing strategies to meet the demands of this growth phase.

Revenue-Based Financing for Growth

Revenue-based financing (RBF) offers a practical way to access capital without sacrificing ownership. With RBF, you receive a lump sum upfront and repay it as a fixed percentage of your daily or weekly sales. The repayment adjusts to your revenue - if sales slow down, so do your payments - helping you maintain cash flow during slower periods [17]. Plus, RBF providers typically approve funding within 48 to 72 hours, making it a fast solution.

The cost of RBF is a flat fee, usually between 6% and 12% of the borrowed amount [4]. This makes it a good fit for businesses with high-margin products, as the fees are less likely to eat into profits. RBF works best for activities that directly generate revenue, like restocking inventory before a busy season or increasing digital ad spend. However, it’s not ideal for covering fixed expenses like rent or salaries.

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital." - Paul Voge, Co-founder and CEO, Aura Bora [4]

One of the biggest perks of RBF? You keep full ownership of your company. There’s no equity dilution, and you won’t need to give up control or board seats [17].

Angel Investors and Early Venture Capital

While RBF is great for immediate scaling, larger, long-term growth often requires equity investment. Angel investors and seed-stage venture capital firms can provide the significant funding needed for projects like regional expansion or major product development [17][7]. These investors are typically looking for high-growth opportunities and are willing to wait longer for their returns in exchange for equity [17].

The downside? You’ll give up some ownership and possibly a say in decision-making. Plus, securing venture capital can be a lengthy process, involving months of pitching and negotiations. It’s best suited for initiatives that demand substantial upfront investment, like building infrastructure or creating proprietary technology, especially if these projects won’t generate immediate revenue [17].

Traditional banks often view online-only businesses as risky due to a lack of physical assets, making equity financing or alternative lending options more practical [7]. For short-term needs like inventory or marketing, though, non-dilutive options such as RBF remain a better choice.

Metrics for Securing Growth Funding

To attract investors or secure larger funding amounts, you’ll need to prove your business is ready for growth. Show that you have a repeatable sales process, strong customer retention, and consistent revenue growth [3]. Modern lenders focus more on real-time sales performance than traditional credit scores [3].

Key metrics like customer acquisition cost (CAC) and lifetime value (LTV) can demonstrate the efficiency of your marketing efforts. Maintaining high gross margins is also essential, especially if you’re using revenue-based models, as these margins ensure you can cover repayment fees [3].

It’s also smart to keep a liquidity cushion for unexpected expenses, like inventory or manufacturing cost spikes [6]. Synchronizing your storefront with accounting software like QuickBooks or Xero can streamline your funding applications and potentially increase your credit limits as your sales grow [3].

Stage 3: Rapid Scaling and Market Expansion

Once you've established a solid foundation with initial growth and validated funding strategies, the next step is scaling up swiftly to secure market share. At this stage, it’s all about leveraging capital to expand operations, build your team, and amplify marketing efforts. With global eCommerce sales expected to surpass $8.1 trillion by 2026, the potential is enormous - but so is the competition[9].

Venture Capital for High-Growth Brands

This phase often involves Series A and Series B funding rounds, which are specifically designed to support businesses in high-growth stages. Series A investors typically seek out companies with proven business models, steady revenue streams, and a roadmap to profitability[12]. As of Q4 2023, the median Series A funding round stood at $11.3 million, while Series B rounds reached a median of $21 million in Q1 2024[5]. This influx of capital not only accelerates growth but also helps fortify your position in the market.

Take Northwood Space, for instance. The company raised $100 million in Series B funding less than a year after securing $30 million in Series A. This allowed them to scale production significantly[22].

"The resources were very intentionally brought on at this point to support the missions that are coming forward for us" - Bridgit Mendler, Founder and CEO, Northwood Space[22]

While venture capital provides essential funding and strategic guidance, it does come with trade-offs, such as equity dilution and heightened performance expectations. However, if used wisely, this funding can open doors to new markets and opportunities[12].

How to Allocate Capital for Scaling

Scaling effectively requires a focused approach to capital allocation, which typically revolves around three main areas: customer acquisition, inventory expansion, and team growth.

- Customer Acquisition: Invest in high-performing marketing channels, such as social media ads, SEO, and email automation. These channels can drive significant revenue growth, especially when paired with an optimized conversion strategy[21].

- Inventory Expansion: Use funds to bulk-purchase stock and secure volume discounts, reducing per-unit costs. Additionally, investing in warehousing and inventory management systems can prevent stockouts during high-demand periods[6][19]. A 2026 case study by Qubit Capital showed how a fashion marketplace achieved 300% monthly revenue growth by combining bank loans for inventory with angel investments for marketing[8].

- Team Growth: As operations scale, hiring specialists like digital marketers, logistics coordinators, and product developers becomes crucial. But recruitment must be handled carefully - one bad hire can cost an eCommerce business an average of $70,200 in lost profits[20]. Investing in technology, such as automated systems and ERPs, can also streamline operations and reduce manual errors[19][20].

Efficient allocation of resources, combined with clear performance metrics, ensures that you meet investor expectations while achieving sustainable growth.

Investor Expectations at the Scaling Stage

At this stage, investors are laser-focused on unit economics. Metrics like Customer Lifetime Value (CLV) to Customer Acquisition Cost (CAC) ratios, Gross Merchandise Value (GMV), and churn rates are critical indicators of market traction and long-term viability[9]. To prepare for investor scrutiny, ensure all financial statements, cap tables, market analyses, and legal documents are well-organized and easily accessible[12].

"A healthy ratio of CLV to CAC speaks volumes about long-term profitability" - Qubit Capital[9]

With D2C funding down 97% from its 2021 peak, showcasing strong performance metrics is no longer optional - it’s a necessity for securing continued investment and achieving growth[9].

Stage 4: Market Dominance and Exit Preparation

At this stage, the focus shifts from potential to proven performance. Investors now prioritize liquidity events, requiring audit-ready financials, strong governance, and evidence of solid unit economics. The emphasis moves from "belief-driven" investments to "evidence-driven" decisions, with a sharp eye on cash flow stability and a clear path to profitability [23]. This shift in priorities significantly influences funding strategies in the later stages.

Private Equity and Late-Stage Investors

Late-stage funding typically involves Series C–E rounds and pre-IPO bridge financing, with amounts ranging from $20 million to over $500 million [23]. Private equity firms often pursue majority buyouts, leveraging their control to install new management teams and refine operations. On the other hand, growth equity investors focus on minority stakes in companies that are profitable or nearing profitability, giving founders access to capital for international growth or strategic acquisitions while retaining operational control [23].

Venture debt becomes a practical option at this point, offering $5 million to $100 million in non-dilutive capital. This funding can extend the company’s runway between equity rounds or support mergers and acquisitions. These loans usually come with interest payments and small stock warrants, often less than 0.5% [23].

"Debt is now considered to be a proper, prudent, and wise component of the capitalization of pre-profit companies (especially later-stage companies)." – David Spreng, Founder and CEO, Runway Growth Capital [25]

Metrics like Net Revenue Retention exceeding 110% and customer acquisition cost payback periods under 12 months are critical benchmarks for late-stage investors [23]. The competition for funding is intense - venture capital supports only about 1% of U.S. eCommerce companies generating between $5 million and $50 million in sales [24]. These funding strategies help lay the groundwork for a structured and well-timed exit.

Preparing for an Exit Strategy

Preparation for an exit should begin 12–24 months in advance. This involves addressing reporting gaps, strengthening the board, and building relationships with potential investors. Companies must ensure multi-year audited financials and strong internal controls to meet the standards of public-market regulators or satisfy M&A due diligence requirements. Cleaning up cap tables and resolving governance issues early can also simplify negotiations during late-stage funding rounds.

Secondary sales are often used alongside late-stage funding to provide liquidity for early employees and stakeholders without requiring a full company exit [23]. Strategic capital allocation, particularly for M&A tuck-ins, can help consolidate market share and enhance valuation ahead of an exit. For instance, Dollar Shave Club successfully achieved a high-profile acquisition by Unilever, while Casper faced challenges with profitability despite reaching the public markets - illustrating the balance required between growth and sustainability [24].

"Late-stage investors shift from belief-driven bets to evidence-driven underwriting: they demand rigorous metrics, defensible unit economics, and institutional-quality governance." – Jarsy Learning Center [23]

Advanced Financial Structures at Maturity

Mature companies often use advanced financial tools like convertible debt, equity swaps, and pre-IPO bridge financing to manage growth while preserving valuation flexibility. Strategic partnerships can also provide funding in exchange for access to technology, customer bases, or intellectual property [23][24][25].

Pre-IPO bridge financing, typically led by investment banks or crossover funds, helps companies transition to public markets while meeting stringent underwriting requirements [23]. Additionally, with venture funds typically operating on nine-year lifespans, there’s inherent pressure to achieve liquidity events within that timeframe [24]. Aligning exit strategies with these investor timelines is crucial for ensuring a successful outcome rather than missing a critical opportunity.

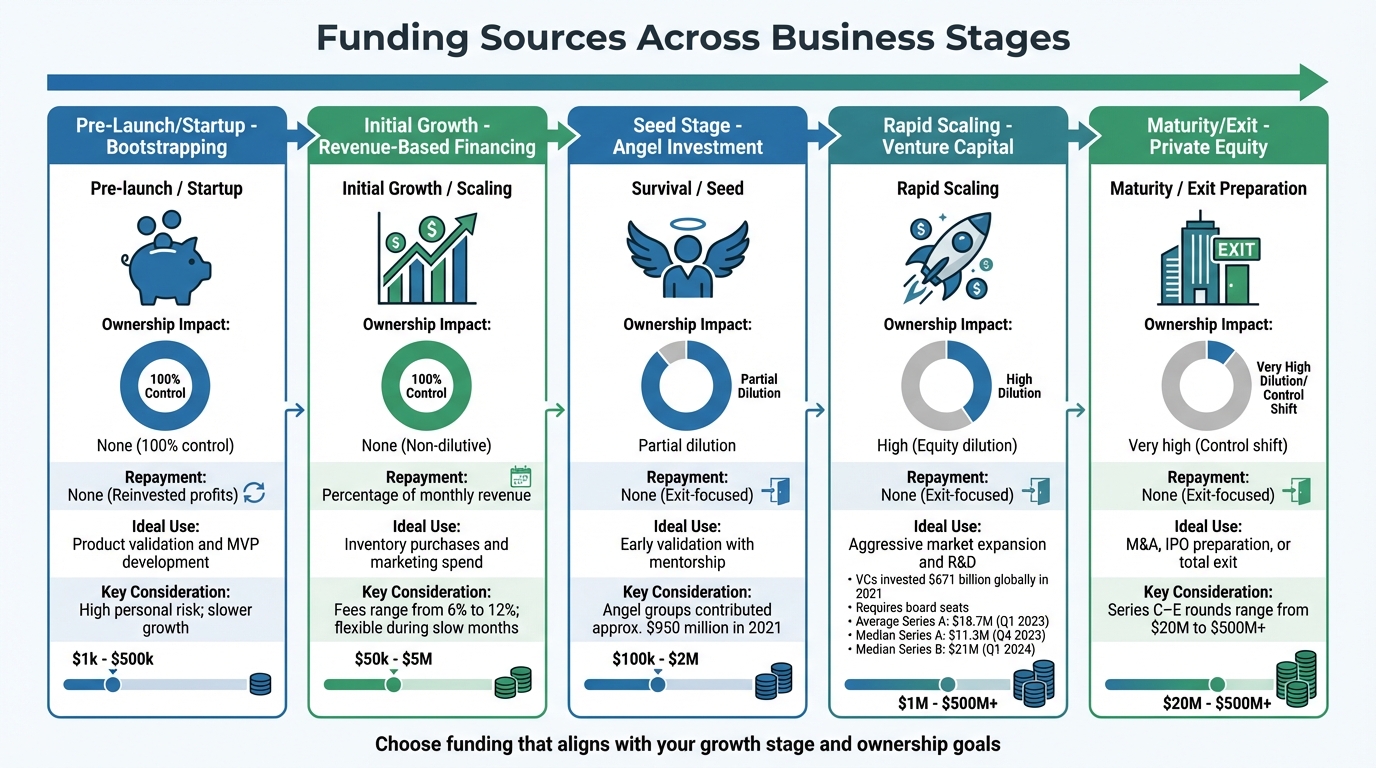

Comparing Funding Sources Across Business Stages

Funding Sources Comparison by Business Stage

Finding the right funding source for your business is all about aligning your current stage with a capital structure that meets your short-term needs without sacrificing future flexibility. For instance, bootstrapping allows you to retain full ownership, but it can restrict early growth. Once you’ve established product-market fit, revenue-based financing becomes a viable option. With fees ranging from 6% to 12% that adjust based on sales, this type of funding works well for things like replenishing inventory or seasonal marketing campaigns.

When it’s time to scale aggressively, venture capital often steps in. In the first quarter of 2023, the average Series A round hit $18.7 million. While this can fuel rapid market expansion, it comes at the cost of significant equity dilution and often involves giving up board seats [12]. For mature brands gearing up for an exit, private equity provides substantial funding - ranging from $20 million to over $500 million - but typically demands majority control or heavy operational oversight [12]. The table below breaks down these funding options by business stage.

Funding Source Comparison Table

| Funding Source | Business Stage | Ownership Impact | Repayment Structure | Ideal Use Case | Key Considerations |

|---|---|---|---|---|---|

| Bootstrapping | Pre-launch / Startup | None (100% control) | None (Reinvested profits) | Product validation and MVP development | High personal risk; slower growth |

| Revenue-Based Financing | Initial Growth / Scaling | None (Non-dilutive) | Percentage of monthly revenue | Inventory purchases and marketing spend | Fees range from 6% to 12%; flexible during slow months [18][4] |

| Angel Investment | Survival / Seed | Partial dilution | None (Exit-focused) | Early validation with mentorship | Angel groups contributed approximately $950 million in 2021 [12] |

| Venture Capital | Rapid Scaling | High (Equity dilution) | None (Exit-focused) | Aggressive market expansion and R&D | VCs invested $671 billion globally in 2021; requires board seats [12] |

| Private Equity | Maturity / Exit Preparation | Very high (Control shift) | None (Exit-focused) | M&A, IPO preparation, or total exit | Series C–E rounds range from $20M to $500M+ [12] |

For businesses at intermediate stages, traditional bank loans and SBA financing can serve as alternatives. These non-dilutive options preserve ownership but often require collateral, personal guarantees, and lengthy approval processes. While they work well for more established businesses, they’re less practical for early-stage eCommerce brands [4][1].

Paul Voge, Co-founder and CEO of Aura Bora, shared how accessing credit limits 30–40 times higher than traditional banks allowed his company to fund large product runs without draining working capital:

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital." - Paul Voge, Co-founder and CEO, Aura Bora [4]

Ultimately, your funding choice should align with your immediate needs while keeping your long-term ownership goals in mind. Non-dilutive options like revenue-based financing can protect your equity while providing working capital, whereas equity-based funding offers larger investments but at the cost of control and ownership.

Conclusion

As your business grows, your approach to funding has to adapt. While bootstrapping might work during the early stages, scaling requires a broader mix of capital sources. A well-rounded capital stack ensures you can cover day-to-day operations, invest in growth opportunities, and build for the future [26][27]. Adjusting your funding strategy at each phase of growth is not just important - it’s essential.

Cash flow challenges remain the top reason 82% of small businesses fail [26][27]. To avoid this, plan ahead by establishing funding relationships early and choosing repayment terms that align with your sales patterns.

"The eCommerce funding you use in the rest of 2023 to ramp up your marketing and fulfillment will impact 2024. If you choose financing with burdensome repayment terms, you'll compromise your future cash flow" [26].

Balancing your funding with your growth strategy is critical to long-term success. By leveraging the financing options discussed earlier, you can create a tailored solution that keeps your business on track. For example, Onramp Funds offers revenue-based financing that allows you to scale without giving up equity. With funding available in as little as 24 hours, transparent fees, and repayments tied to your sales, Onramp Funds ensures you maintain full ownership while accessing the capital you need. Whether it’s preparing inventory for the holiday rush or expanding into new markets, choosing the right funding partner can be the difference between stagnation and growth.

Take a close look at your funding strategy to ensure it includes balanced sources and repayment terms that support your sales cycles and growth objectives.

FAQs

How do funding options differ between the early and late stages of business growth?

Funding options differ greatly between the early and late stages of business growth, depending on your company’s progress, risk profile, and financial requirements.

Early-stage funding targets startups that are just getting off the ground. Common sources include seed funding, angel investors, and venture capital. These investors are typically open to taking bigger risks in exchange for equity. Their support often goes toward essential activities like developing your product, conducting market research, or launching operations.

In contrast, late-stage funding is geared toward businesses that have already demonstrated market success. This type of funding is often used to scale operations, enter new markets, or prepare for an IPO or acquisition. Options here include Series C or D funding, debt financing, and revenue-based financing. Late-stage investors usually look for companies with a proven track record and steady revenue, as they tend to favor lower-risk opportunities.

To sum it up, early-stage funding lays the groundwork for your business, while late-stage funding fuels expansion and positions you for long-term success.

How do I choose the right funding strategy for my business's growth stage?

Choosing the right funding strategy depends on your business's stage of growth, financial requirements, and future goals. For startups, options like bootstrapping, angel investors, or crowdfunding are often a good fit. These methods usually offer more control and fewer formalities compared to traditional financing. As your business matures, more structured approaches like bank loans, venture capital, or revenue-based financing may be better for handling larger investments in areas like inventory, marketing, or expansion.

To make the best decision, take a close look at your cash flow, revenue model, and growth timeline. For instance, if you need fast funding to handle a sudden spike in demand, short-term financing might be the way to go. However, if you're scaling and open to giving up some equity in exchange for substantial funding, venture capital could be a stronger option. A well-prepared business plan and clear financial forecasts will help ensure your funding choice supports both your immediate needs and long-term vision.

What key metrics should you focus on to secure funding during the scaling stage?

During the scaling stage, keeping an eye on the right metrics is key to attracting investors and showcasing your business's growth potential. Revenue growth is one of the most important indicators, as it demonstrates consistent increases in sales. Meanwhile, gross margin gives insight into profitability after accounting for direct costs, offering a glimpse into how efficiently your operations are running.

Equally important are your customer acquisition cost (CAC) and lifetime value (LTV). A strong CAC-to-LTV ratio signals that you're bringing in customers in a cost-effective way while ensuring long-term profitability. Lastly, maintaining cash flow stability is critical. Metrics like your burn rate and runway reassure investors that you can handle expenses and scale wisely. Together, these metrics provide a solid foundation for proving your readiness to move to the next growth phase.