Paying for unused funds is a common problem for eCommerce sellers. Traditional loans often require you to take a large lump sum upfront, leading to fees on money you don’t immediately need.

Draw-based funding solves this by letting you borrow only when necessary. Instead of paying for idle capital, you access a pre-approved limit in smaller amounts, called draws, as your business requires. Fees apply only to the money you use, aligning costs with your actual needs. This approach can cut borrowing costs by 40% or more.

Key Benefits:

- Pay for what you use: Fees apply only to withdrawn amounts, not the total limit.

- Flexible repayment: Payments adjust based on sales performance, easing financial strain during slower months.

- Quick access: Funds can be available within 24 hours, with no collateral or lengthy paperwork.

- Real-time approval: Based on sales data from platforms like Amazon or Shopify, not credit scores.

By syncing funding with your business cycles, draw-based funding maximizes efficiency and helps eCommerce sellers avoid the high costs of idle capital.

How To Fund Your Ecommerce Business For Cheap (Or Even Free)

sbb-itb-d7b5115

What Is Draw-Based Funding?

Draw-based funding gives businesses access to a pre-approved capital limit but allows them to withdraw smaller amounts - called draws - only when the funds are needed [4][5]. Think of it like a credit card: you’re only charged fees on what you use, not the total amount available.

This setup is quite different from traditional loans. With a conventional loan, you receive the full amount upfront and start paying interest on the entire sum immediately, even if much of it remains unused. In contrast, draw-based funding only applies fees or interest to the funds you’ve actually withdrawn [4][3].

For eCommerce businesses, this model fits naturally with the way they operate. Imagine needing $30,000 today to restock inventory, $20,000 next month for a holiday marketing campaign, and nothing the month after. Draw-based funding allows you to align these cash injections with specific business needs - like inventory cycles, product launches, or seasonal ad spending - without holding onto unused funds [4].

Many draw-based systems function like a revolving line of credit. As you repay what you’ve used, your available balance is restored automatically. This ongoing access to funds is especially helpful for businesses dealing with seasonal cash flow fluctuations [3].

Key Features of Draw-Based Funding

The standout feature of draw-based funding is its flexibility. Instead of committing to a large lump sum, you access funds as specific expenses arise - whether it’s for restocking inventory, running ad campaigns, or launching new products. This way, your money is always working for you, not sitting idle.

Another defining characteristic is usage-based fees. You’re only charged fees or interest on the amount you’ve withdrawn, not the total approved limit. For example, if you’re approved for $100,000 but only use $40,000, you’ll only pay fees on the $40,000. Some providers charge a transparent monthly fee as low as 1.5% on the amount used, while others apply a flat fee (usually 6% to 12% of the borrowed sum) with no compounding interest or late fees [2].

Sales-linked repayment is another key advantage. Payments adjust based on your sales cycles - if revenue slows down, your repayment amounts decrease accordingly. Many systems automate payments as a percentage of daily or weekly sales, with rates typically ranging from 5% to 20% [2]. This flexibility helps reduce financial strain during slower months.

Approval for draw-based funding is data-driven, relying on real-time business metrics like sales volume, order trends, and inventory levels. Lenders use read-only APIs to access this data from platforms like Amazon, Shopify, and Walmart [3][6]. This approach allows for faster decisions - often within 24 hours - and better alignment with your business performance rather than outdated credit scores.

Most providers also offer the option to repay early without penalties. If you have a strong sales month and want to clear your balance to save on fees, you can do so without any extra charges. This gives you added control over your financing costs.

By syncing capital access and repayment with your sales performance, draw-based funding ensures your money works efficiently and aligns with your business needs.

How Draw-Based Funding Works

Here’s how draw-based funding plays out in practice:

You start by connecting your sales channels (like Amazon or Shopify) and bank accounts via read-only APIs. This allows the lender to verify your business performance in real time with minimal paperwork [2][3]. Based on your revenue and sales history - not your personal credit score - the lender sets a maximum funding limit. Businesses with at least $10,000 in monthly revenue can often qualify, and approvals can happen in under 24 hours thanks to AI-powered underwriting [7].

Once approved, you withdraw funds as needed. For example, if you need $15,000 to restock inventory or $25,000 for a holiday ad campaign, you can request those amounts when the time is right. You’re in full control of how much you draw and when.

Repayment is typically automated and tied to your sales cycles. Payments are deducted as a percentage of your daily or weekly sales, which aligns with marketplace payout schedules. For instance, if you sell on Amazon, repayments might sync with their bi-weekly settlement periods. When sales are strong, you pay more quickly; when they slow down, repayment adjusts accordingly [2].

As you repay, your available credit is automatically replenished, allowing you to access more funds without reapplying [3]. This revolving feature is especially useful for managing the cash flow gaps that often occur between paying suppliers and receiving marketplace payouts, which can take 15 to 90 days [7].

"Instead of one lump-sum payment, you'll get incremental cash injections aligned to your supply chain needs. This keeps the cost of capital to minimum while maximizing your cash flow." - Rebecca Montag, eCommerce Writer, 8fig [5]

The Problem of Idle Capital in eCommerce

Idle capital refers to money you're paying for but not actively using. In eCommerce, this is a common hurdle that eats into profitability. The problem often stems from traditional funding methods that give you a large lump sum upfront - more than you might need at any given moment. For example, you might need $30,000 today to stock inventory, $20,000 next month for ads, and then nothing for a while. But with fixed repayment terms, you’re stuck paying for funds that aren't helping your business grow.

What Causes Idle Capital

Several factors in eCommerce make idle capital even harder to avoid. One major culprit is Minimum Order Quantities (MOQs). Suppliers often require you to buy large amounts of inventory upfront, which ties up cash for weeks - or even months - before the products sell. Essentially, your money is sitting in a warehouse, not working for you.

Another issue is marketplace payout delays. Platforms like Amazon, Shopify, and Walmart often hold onto your sales revenue for 14 to 30 days before releasing it to you [7]. On top of that, Amazon keeps 10% to 20% of your funds in reserve accounts [1]. Even though you’ve made the sale, you can’t touch that money right away.

Then there’s the cash conversion cycle, which can stretch anywhere from 15 to 90 days [7]. This is the time it takes to pay suppliers, ship products, fulfill orders, and finally get paid by customers. To make things worse, you often have to pay for advertising upfront, weeks before you see any revenue from those campaigns. Traditional funding models with fixed monthly payments don’t account for these delays, leaving you to cover costs on capital that’s not yet earning you returns.

How Idle Capital Affects eCommerce Businesses

The financial strain from idle capital is real and measurable. Fixed repayment plans and high-interest funding models - sometimes with APRs over 80% [7] - can make the situation worse. With term loans or Merchant Cash Advances, you’re locked into paying the same amount every month, regardless of whether your sales are booming or barely trickling in. This rigidity doesn’t account for the seasonal nature of eCommerce, where revenue can swing dramatically - sometimes three to five times higher in Q4 compared to Q1 [1].

"Taking $100K when $60K covers the need means paying fees on $40K idle capital, increasing effective cost by 40%+." - Luca AI [1]

Idle capital also limits your ability to adapt. Multi-channel sellers often have up to 23% more working capital than they need due to fragmented financial visibility [1]. To play it safe, many over-borrow, creating a "safety net" that comes at a steep cost. This inefficiency becomes even more costly as expenses rise - like CPMs, which jumped 22% year-over-year, and COGS, which increased by 15% to 30% due to tariffs in 2026 [1]. Every dollar tied up in idle capital is a dollar that could’ve been used to grow your business.

This all underscores the need for financing solutions that align costs directly with how and when you use the funds.

How Onramp Funds' Draw-Based Funding Reduces Idle Capital Costs

Lump Sum vs Draw-Based Funding Cost Comparison for eCommerce

Idle capital can be a drain on resources, especially when you’re paying for funds you’re not actively using. Onramp Funds tackles this problem head-on with its draw-based funding model. This approach allows you to access funds only when you need them, helping you avoid the fees that come with unused capital. Whether it’s restocking inventory for a product launch or boosting a marketing campaign, you’re only paying for the money that’s actively driving your business forward.

Access Funds When You Need Them Most

Think of it as having a reserve you can tap into as your business demands. Onramp Funds connects directly to major eCommerce platforms like Amazon, Shopify, Walmart, and TikTok Shop. By analyzing your real-time sales data, they determine your funding offer - typically 1 to 2 times your monthly revenue[8]. This ensures you can withdraw funds for immediate needs without worrying about unnecessary fees on idle money[3].

Repayment Adjusts to Your Sales

Instead of fixed monthly payments, Onramp Funds uses a flexible repayment system tied to your sales performance. For instance, if your repayment rate is 25% and you generate $25,000 in sales, you’ll repay $6,250. But if your sales dip to $20,000, your repayment adjusts to $5,000[8][9]. There are no fixed minimums or personal guarantees, so even during slower months or seasonal downturns, your payments naturally align with your cash flow. This flexibility ensures you’re not overburdened when sales fluctuate, making it easier to manage your finances.

Quick and Straightforward Funding

Onramp Funds streamlines the entire process, deploying capital in as little as 24 hours. Their data-driven underwriting pulls insights from your sales, advertising, and web analytics to make quick decisions[8]. The funding is equity-free, so you maintain full ownership of your business, and the fee structure is straightforward - no hidden charges[3]. Fees decrease as you repay your balance, and there are no penalties for early repayment. This means you can pay off your balance sooner and save on costs, unlike traditional loans that often come with rigid terms.

How to Implement Draw-Based Funding with Onramp Funds

Getting started with draw-based funding through Onramp Funds is straightforward and doesn’t involve lengthy approval processes. By leveraging the flexibility of draw-based funding, you can maximize your capital efficiency. Here’s a step-by-step guide to implementing it.

Step 1: Check Your Eligibility

To qualify, you’ll need at least $3,000 in monthly sales - this helps minimize idle capital fees. Onramp connects directly to your eCommerce platform, whether you’re using Amazon, Shopify, Walmart, or TikTok Shop. This connection allows the platform to evaluate your real-time business performance, such as revenue growth, sales channels, and forecasts, instead of relying on personal credit scores or tax returns [3]. The setup process is quick, taking just a few minutes. You’ll also need to link a bank account to complete the process [3].

Step 2: Use the Funding Calculator

Before making a draw request, use Onramp’s funding calculator to estimate your funding needs and costs. This tool helps you align borrowing with your actual operational requirements, avoiding unnecessary debt. Simply input your projected sales, desired draw amount, and repayment timeline. The calculator will determine your funding limit - typically 1 to 2 times your monthly revenue - and provide repayment terms, which are tied to a percentage of your sales, usually between 5% and 20% [2][8].

For example, if you plan to draw $20,000 for inventory and your sales are projected at $60,000 for November with a 10% repayment rate, you’d repay $6,000 that month [2]. The calculator also shows how repayments adjust based on sales performance, helping you plan more effectively.

Step 3: Request Targeted Draws

Once approved, you can log into your Onramp dashboard and request the exact amount you need for specific purposes - like restocking inventory ahead of a product launch or funding a PPC campaign. Funds are typically deposited within 24 hours [3][10]. This targeted approach ensures you’re only borrowing what’s necessary. For instance, if you need $10,000 for an ad campaign, you can draw that amount without overextending your finances.

Step 4: Monitor and Adjust Repayments

Your Onramp dashboard provides real-time tracking of repayments, which are automatically deducted as a percentage of your daily sales - starting as low as 1% [10]. If your sales slow during an off-season, repayments automatically scale down, giving you more flexibility. There are no fixed payment dates or minimum amounts [2]. Once you’ve repaid approximately 60% of your balance, you can request additional draws based on updated performance data [2]. This adaptive repayment structure allows you to stay agile and avoid overextending your resources.

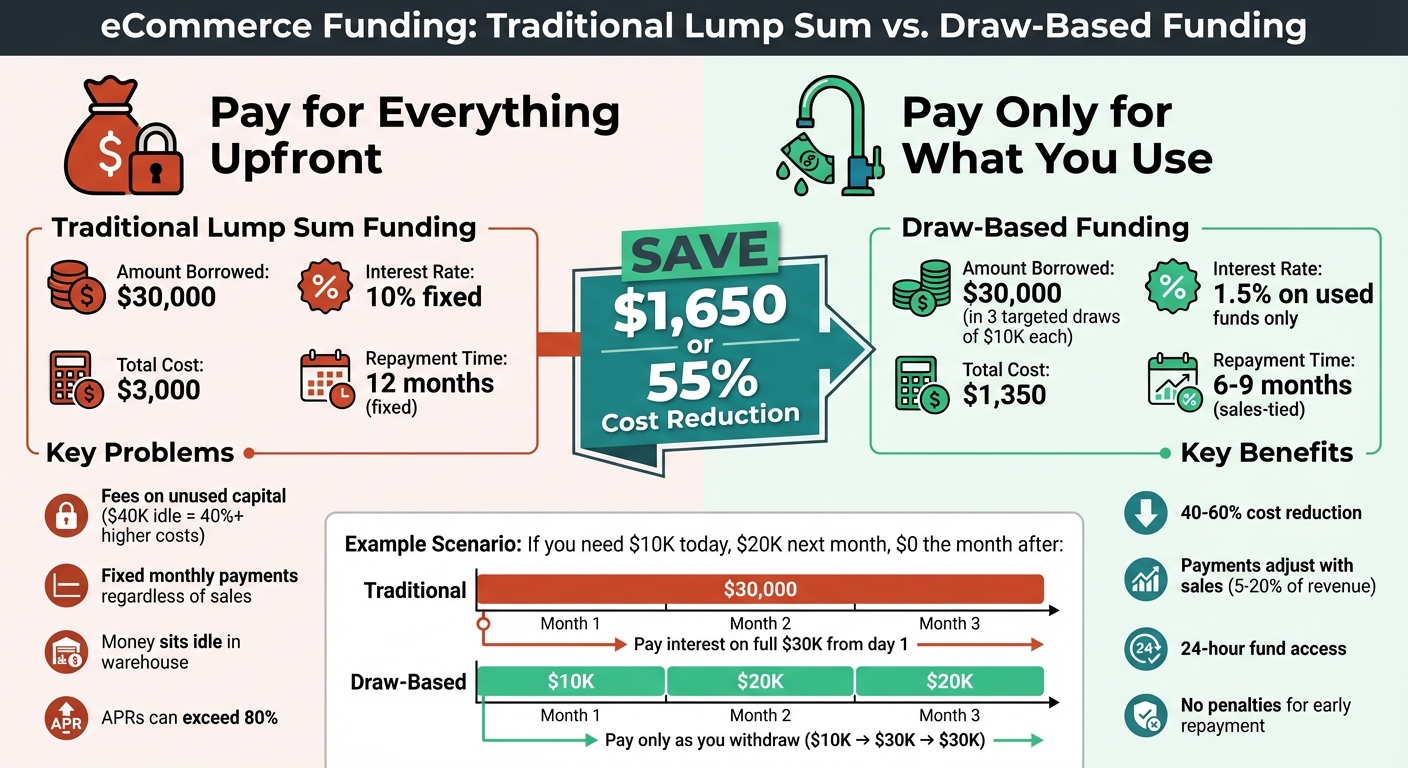

Comparing Costs: Lump Sum vs. Draw-Based Funding

Here’s a quick comparison to highlight the cost savings of draw-based funding:

| Scenario | Funding Type | Amount Borrowed | Interest Rate | Total Cost | Repayment Time |

|---|---|---|---|---|---|

| Upfront | Lump Sum | $30,000 | 10% fixed | $3,000 | 12 months |

| Draw-Based | Targeted Draws | $30,000 ($10K x 3 draws) | 1.5% on used | $1,350 | Sales-tied (6-9 months) |

Measuring Cost Savings and Capital Efficiency

It's one thing to align funding with usage, but understanding how to measure the resulting cost savings and efficiency takes things to the next level.

How to Calculate Idle Capital Costs

The formula for idle capital cost is straightforward: (Undrawn Amount × Interest Rate × Idle Period).

Let’s break it down with an example. Suppose you have a $50,000 loan at a 12% annual interest rate, but you only need $30,000. The unused $20,000 will cost you: $20,000 × 12% × (3/12) = $600 over three months. However, with draw-based funding, you’d only take out $30,000 initially and request the remaining $20,000 when required. This approach eliminates that $600 in unnecessary expense. These savings highlight why timing your fund withdrawals can make a big difference.

By switching to draw-based funding, businesses can cut idle capital costs by 40% to 60%, which directly improves overall capital efficiency [11].

Improving ROI and Efficiency

Reducing idle capital doesn’t just save money - it maximizes your return on investment (ROI). Draw-based funding ensures that every borrowed dollar is tied to activities that generate revenue. As re:cap puts it:

"If your return is lower than your cost of capital, you're destroying value. If it's higher, you're creating value" [11].

To make smart financial decisions, use your cost of capital as a benchmark. Investments should always deliver returns that exceed this "hurdle rate" [11][12].

Here’s an example: Imagine funding a $15,000 marketing campaign at 15% APR. If that campaign brings in $25,000 in sales with a 30% margin, you’d earn a $7,500 gross profit - far outweighing the interest expense. On top of that, draw-based funding offers flexibility. Since repayments adjust with your sales pace, you won’t be stuck with rigid monthly payments during slower sales periods. This flexibility keeps your capital working efficiently, even when seasonal fluctuations come into play.

Conclusion

Draw-based funding changes how eCommerce businesses handle capital. Instead of paying interest on unused funds, you access money only when you need it - for things like restocking inventory, seasonal promotions, or seizing growth opportunities. This approach eliminates the cost of idle capital and helps improve your profits.

What really stands out is how repayments are tied to your actual sales. During slower periods, you’re not stuck with fixed monthly payments. This flexibility ensures that every borrowed dollar supports activities that directly contribute to your growth.

For eCommerce sellers dealing with cash flow issues - like waiting 14 to 30 days for marketplace payouts or managing seasonal demand - draw-based funding offers the adaptability needed to scale effectively. With approvals possible in just 24 hours, you can act quickly on opportunities without the delays of traditional banking.

Onramp Funds takes this a step further with revenue-based financing tailored for eCommerce. By connecting directly with platforms like Shopify, Amazon, and Walmart, it evaluates your business using real-time performance data instead of outdated credit scores. Transparent fees between 2% and 8%, combined with repayments based on a percentage of sales, mean you keep control of your business while accessing the capital you need.

By aligning funding with your immediate needs, draw-based financing provides a streamlined and efficient solution for today’s fast-paced eCommerce environment.

Curious about how it can work for you? Use Onramp Funds' funding calculator to explore draw-based financing and take the next step toward sustainable growth.

FAQs

How is draw-based funding different from a loan?

Draw-based funding gives businesses the freedom to access funds only when they need them, with interest charged solely on the amount used. This setup is especially helpful because repayments flex with sales, providing relief during slower months. On the other hand, traditional loans come with fixed payments that don’t change, no matter how much revenue is coming in, which can strain cash flow. By tying costs directly to performance, draw-based funding offers a solution that better matches the unpredictable nature of eCommerce businesses.

What eCommerce expenses are best for a draw?

Draw-based funding works well for covering costs like restocking inventory, running seasonal marketing campaigns, or testing and developing products. With this method, businesses can access funds only as needed, making it easier to match financing with day-to-day operations while avoiding extra expenses.

Will repayments drop if my sales slow down?

Revenue-based funding offers flexibility in repayments. If your sales dip, your payments decrease accordingly. This approach aligns with your business performance, providing relief during slower periods and helping you manage cash flow more effectively.