Managing inventory during unpredictable sales cycles is tough. Stock too little, and you risk losing sales; stock too much, and you tie up cash. Traditional loans often fail to meet the needs of eCommerce businesses with fluctuating revenue due to their rigid requirements and slow approval processes. Instead, flexible financing options like revenue-based financing, inventory credit lines, and revenue-based term loans offer faster, more tailored solutions. These methods align repayment with sales performance, helping businesses maintain inventory and cash flow balance. Here's a quick breakdown:

- Revenue-Based Financing: Repayments adjust based on sales, offering flexibility during slow months.

- Inventory Credit Lines: Borrow only what you need, paying interest on the amount used.

- Revenue-Based Term Loans: Ideal for large purchases, with repayment tied to revenue.

How Sales Fluctuations Affect Inventory Management

When sales vary significantly from one month to the next, managing inventory becomes a daunting challenge. You’re often forced to choose between two risky options: overstocking, which ties up cash and raises storage costs, or understocking, which can lead to lost sales and unhappy customers. This balancing act can spiral into what experts call the "Inventory Death Spiral." Here’s how it works: running out of stock can hurt your marketplace rankings and reduce the effectiveness of your advertising. By the time you restock, regaining lost sales momentum becomes even harder [5]. This unpredictability doesn’t just disrupt your ordering process - it also puts a strain on your cash flow.

The financial pressure is especially intense during the Cash Conversion Cycle. This is the period where you’ve already paid your suppliers but haven’t yet received revenue from sales. For businesses dealing with seasonal products or large retail contracts, this gap can quickly drain working capital. Over-ordering to avoid stock-outs might seem like a solution, but it can backfire by locking up cash and shrinking profit margins [5].

The stakes are even higher when you consider customer behavior. Returning customers are 50% more likely to make a purchase compared to first-time visitors [7]. If you run out of stock, you risk losing these loyal customers for good.

Why Standard Loans Don't Work Well

Traditional loans often fall short for eCommerce businesses, especially those with fluctuating sales. These loans require fixed monthly payments, which don’t align with the ups and downs of your sales cycles [5][6]. Matthew Shearer, SVP of Channel Sales at eCapital, explains the issue clearly:

"Traditional financing wasn't designed for this model. Term loans are rigid. Lines of credit may not reflect inventory cycles" [5].

Banks typically base their lending decisions on historical financial data, ignoring real-time metrics like SKU performance, sales velocity, or inventory turnover. This approach doesn’t account for the actual health of your operations [5]. To make matters worse, lenders often advance only 50–90% of your inventory’s estimated liquidation value, leaving you short on cash [6]. And during volatile market conditions, they become even more conservative. For example, when the COVID-19 pandemic hit in early 2020, zinc prices plummeted by 27.26% in just two months [4]. This kind of sudden drop in collateral value makes traditional lenders hesitant to offer inventory-backed loans, highlighting the need for more flexible financing options.

What Happens When You Can't Fund Inventory

A lack of funding can disrupt your business almost immediately. First, stockouts lead to lost sales opportunities. On platforms like Amazon, running out of stock can also hurt your marketplace rankings, as these platforms prioritize sellers who consistently meet demand. Advertising becomes less effective too, as you’re spending money to drive traffic to listings that can’t convert [5].

Researcher Bangdong Zhi emphasizes the challenges of inventory financing in unpredictable markets:

"Inventory financing is particularly risky in a volatile market environment since fluctuating collateral prices increase default risk" [4].

This heightened risk makes traditional lenders even more cautious, creating a frustrating cycle. The businesses that need flexible funding the most are often the ones least likely to secure it.

sbb-itb-d7b5115

Financing Options That Adjust to Your Sales

When your revenue ebbs and flows, it’s smart to choose financing that moves with it. The right funding solution can ease the strain during slower times and expand alongside your business during busy periods. These options offer terms that match your sales cycle, ensuring your funding grows and shrinks as your needs change. Here are three financing methods designed to handle the unpredictability of fluctuating cash flow.

Revenue-Based Financing

This option is perfectly suited for businesses with inconsistent demand. With revenue-based financing, repayments are tied directly to your sales. Instead of a fixed monthly payment, you repay a percentage of your revenue. When sales are high, you pay more; when sales dip, your payments automatically decrease. This structure helps protect your cash flow during leaner months.

Since 2016, billions have been delivered to merchants through this model, which focuses on performance rather than traditional collateral or assets [2]. The biggest advantage? You’re not stuck with rigid payment schedules that don’t reflect your actual sales patterns. For businesses dealing with seasonal fluctuations or unpredictable demand, this flexibility can be a game-changer - helping you stay stocked and ready when it matters most.

Inventory Credit Lines

An inventory credit line acts like a revolving source of capital. You can draw funds as needed, pay interest only on what you use, and repay to restore your available credit. This gives you the flexibility to manage inventory without committing to a lump sum.

For established supplier relationships, funding can often be secured within a week [1]. During peak seasons, you can borrow more to maintain adequate stock levels, while in slower periods, you can scale back your borrowing and reduce costs. This interest-only model is particularly helpful for businesses with seasonal cycles, allowing you to avoid stockouts when demand surges while keeping expenses manageable during quieter times [1].

Revenue-Based Term Loans

For larger funding needs - like preparing for the holiday rush or launching a new product - revenue-based term loans provide a balanced solution. Unlike traditional term loans with fixed repayments, these loans adjust payments based on your sales performance.

Some lenders release funds in tranches, typically ranging from $100,000 to $500,000, with disbursements spaced out every 45–60 days to align with supplier payment schedules [3]. Repayment is usually spread over 3–9 months and is based on a percentage of your revenue [3]. This setup is ideal for businesses needing significant upfront capital without the burden of fixed monthly payments, giving you the breathing room to invest in growth while staying financially flexible.

Getting Approved with Inconsistent Sales Data

Inconsistent monthly sales can make traditional lenders hesitant. But modern eCommerce financing takes a different approach. Instead of relying on past financial records, these lenders focus on real-time data to gauge your business's current health.

What Lenders Look At

Today's lenders connect directly with platforms like Amazon, Shopify, Walmart, and TikTok Shop to access live performance metrics. They evaluate several factors, including:

- Revenue growth trends

- Sales across different channels

- Current inventory levels

- Product turnover speed

They also look at forecasted revenue and product performance. Metrics like inventory turnover ratios and profit margins help them decide if your products qualify as liquid assets[8].

"Most lenders still prioritize tax returns and personal credit over metrics that actually reflect modern business performance." – Onramp Funds[8]

For revenue-based financing, top-line sales usually determine both the loan amount and repayment terms[8]. This real-time, data-driven process simplifies the qualification process.

Minimum Requirements to Qualify

This financing method is tailored to the needs of eCommerce businesses. To qualify, you'll typically need to link your selling platforms and bank account so lenders can review your live metrics. Many lenders require just $3,000 or more in monthly sales to get started[8]. Some can even approve and deposit funds within one day - a huge advantage over traditional banks that often reject eCommerce businesses based on personal credit.

For revenue-based financing, repayments align with your sales. If your revenue dips during a slow period, your minimum payment decreases as well. Similarly, inventory credit lines depend on the value of your current inventory to set your credit limit[8].

Managing Cash Flow and Inventory Funding

Once you’ve secured flexible financing, the next critical step is aligning your inventory management with actual demand. By combining smart funding strategies with effective inventory practices, you can help your business stay steady, even when sales fluctuate. The goal? Match your purchasing decisions to demand patterns while keeping enough buffer stock to avoid running out.

Forecasting Demand and Planning Reorders

Start by analyzing 12–24 months of sales data to uncover seasonal trends and variability. Tools like the coefficient of variation can help you measure how much sales fluctuate. For example, if your daily sales average 100 units but vary by 20%, you might set your reorder point at 120 units during lead time to account for that fluctuation.

Here’s a simple formula for calculating your reorder point:

(Average Daily Usage × Lead Time) + Safety Stock.

Let’s break this down with an example. If your lead time is 14 days, and you sell an average of 50 units per day with around 30% variation, your basic need would be 50 × 14 (700 units). Adding a safety buffer of about 150 units brings your reorder point to 850 units. It’s a good idea to review these numbers weekly, especially during periods of volatility, to adjust your orders as needed.

Safety Stock and Profit Margin Analysis

Once you’ve forecasted demand, the next step is building safety stock to protect against unexpected spikes in demand or supplier delays. One way to calculate safety stock is:

(Max Daily Usage × Max Lead Time) – (Average Daily Usage × Average Lead Time).

For example, if you sell 100 units daily with a standard deviation of 25 units and your lead time is 10 days, you’d need around 130 units of safety stock to maintain a 95% service level.

Beyond safety stock, keep an eye on your gross profit margins to ensure your financed inventory is delivering solid returns. Use ABC analysis to focus on your most profitable products - those “A” items that typically generate 80% of revenue from just 20% of your SKUs. If your gross margin slips, say from 45% to 30% due to overstock, check your inventory turnover ratio (calculated as the cost of goods sold divided by average inventory). Aiming for 4–6 inventory turns per year is a good benchmark for balance.

Revenue-based financing can also be a game-changer. Since repayments adjust based on your actual sales, this approach helps protect your profit margins during slower periods. Plus, it ensures you have the cash flow to restock high-performing items when demand picks up again.

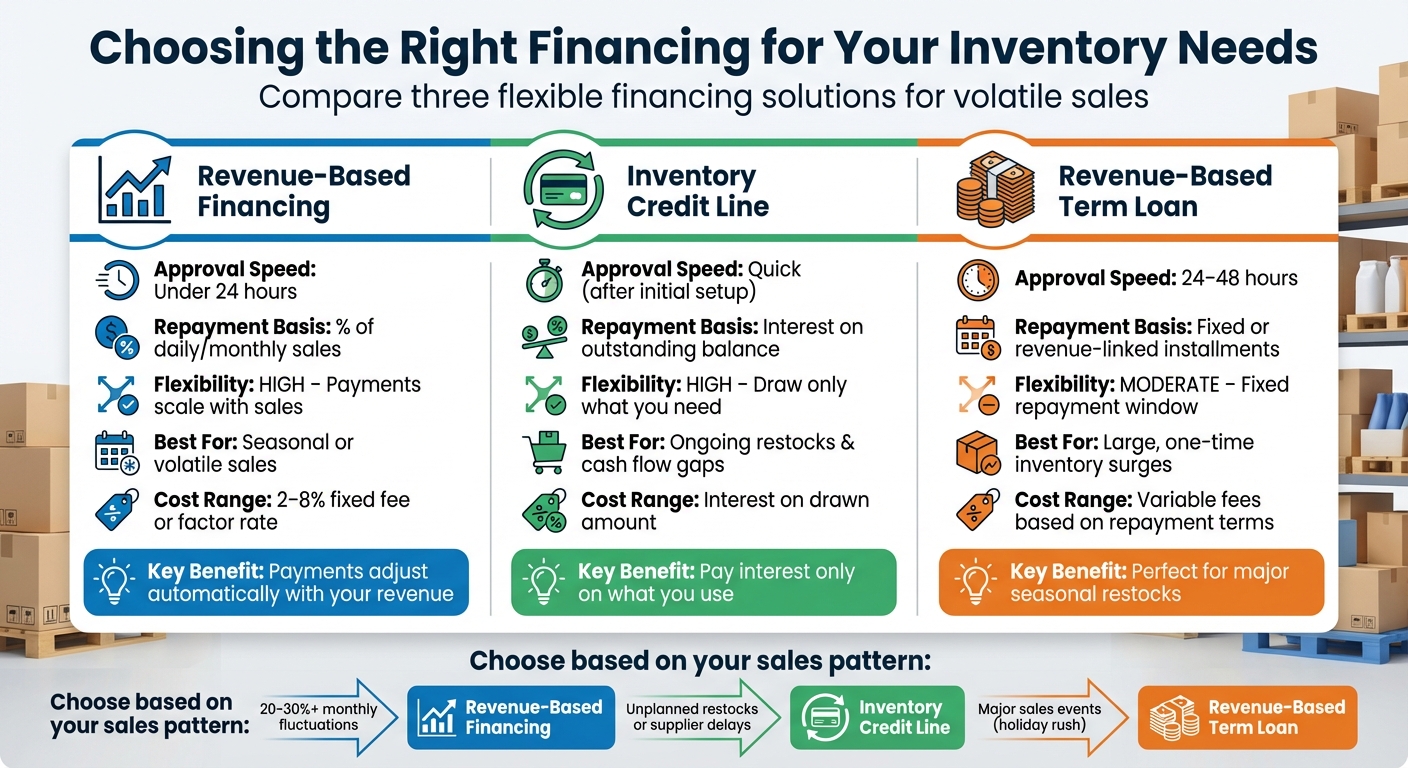

Comparing Financing Options: Which One Is Right for You?

Comparison of Flexible Financing Options for eCommerce Inventory Management

When managing fluctuating sales and inventory needs, choosing the right financing option can make all the difference. By matching your cash flow challenges with the right funding method, you can keep your inventory well-stocked and your operations running smoothly - even during unpredictable demand.

Comparing Speed, Cost, and Flexibility

Revenue-based financing works well for businesses with inconsistent monthly sales. Payments are tied to a percentage of your revenue, so they adjust automatically - lower during slow periods and higher when sales increase. Onramp Funds typically approves advances in less than 24 hours [10]. Costs range from a 2–8% fixed fee or a factor rate, with APRs varying depending on your business performance.

Inventory credit lines are like business credit cards, giving you the flexibility to draw funds as needed and pay interest only on what you use. This option is ideal for ongoing restocking needs, especially when you can pay off the balance quickly. However, as Onramp Funds points out:

"A line of credit... works best when you can quickly pay off the balance to prevent fees from hurting you too badly." [8]

Carrying a high balance over time can lead to significant interest costs, so it’s best suited for short-term needs.

Revenue-based term loans provide a one-time lump sum, making them a great option for large inventory purchases, such as holiday restocks. These loans often come with approval times of 24–48 hours and repayment terms between 30 and 120 days. As Settle explains:

"Businesses can pay vendors upfront while paying [the lender] back in 30–120 days, creating smoother inventory turnover." [9]

Here’s a quick comparison of these three options:

| Feature | Revenue-Based Financing | Inventory Credit Line | Revenue-Based Term Loan |

|---|---|---|---|

| Approval Speed | Under 24 hours | Quick (after initial setup) | 24–48 hours |

| Repayment Basis | % of daily/monthly sales | Interest on outstanding balance | Fixed or revenue-linked installments |

| Flexibility | High – Payments scale with sales | High – Draw only what you need | Moderate – Fixed repayment window |

| Best For | Seasonal or volatile sales | Ongoing restocks & cash flow gaps | Large, one-time inventory surges |

| Cost Range | 2–8% fixed fee or factor rate | Interest on drawn amount | Variable fees based on repayment terms |

This table highlights how each option aligns with different business needs, helping you decide based on your sales patterns and inventory cycles.

If your sales see monthly fluctuations of 20–30% or more, revenue-based financing can help buffer cash flow challenges. For unplanned restocks or supplier delays, an inventory credit line offers flexible, on-demand funding. And if you’re gearing up for a major sales event, a revenue-based term loan provides the capital you need without locking you into a long-term repayment plan.

Conclusion

Managing fluctuating inventory doesn’t have to drain your cash reserves or lock you into rigid financing terms. The secret lies in aligning your funding approach with your revenue patterns, rather than forcing your business to adapt to inflexible repayment schedules. Tools like revenue-based financing and inventory credit lines provide the adaptability that traditional bank loans often lack. They let you pay more during high-sales periods and less when things slow down.

To navigate unpredictable inventory needs effectively, you need a mix of smart financial strategies and disciplined planning. Accurate forecasting helps you avoid over-ordering products that may sit unsold, which could leave you stuck with unnecessary debt[1]. It’s also wise to time your capital draws with supplier payment schedules - splitting payments into deposits and final balances can reduce financing costs and leave room in your budget for essential expenses like marketing[3].

Flexible financing options that adapt to your business’s seasonal trends and multichannel demands will always be more effective than rigid loans that don’t match your cash flow[3]. As your business grows, inventory financing can grow with you, offering a way to scale without giving up equity or ownership[1].

This type of financing shines as a short-term solution for managing volatility while proving the strength of your unit economics[1]. It gives you the space to handle unpredictable demand, ensuring you can keep shelves stocked, satisfy customer needs, and build a path toward sustainable growth. With the right financing partner and accurate planning, your business stays agile, ready to meet challenges, and positioned for future success.

FAQs

How do I choose between revenue-based financing and an inventory credit line?

When deciding, consider your sales trends and cash flow requirements. Revenue-based financing is ideal if your sales fluctuate, as repayments adjust based on your revenue. It also offers quick funding without needing collateral. On the other hand, inventory credit lines are better for businesses with consistent sales. They provide fixed payment schedules and continuous access to funds but may require collateral and take longer to approve. Your choice should align with your revenue consistency and repayment preferences.

What sales data do I need to get approved if my revenue is inconsistent?

If your income fluctuates, you'll need to share recent sales figures to paint a clear picture of your business's performance. This includes monthly sales data, average monthly revenue, and a detailed sales history over time. Lenders usually expect to see at least $3,000 in monthly sales, $10,000 for revenue-based financing, and a gross margin of 30% or higher. Additionally, showcasing any seasonal trends in your sales can strengthen your case. Providing clear data on sales patterns and channels helps lenders evaluate how well you can manage repayment.

How can I avoid overbuying inventory when using flexible funding?

To keep from overbuying inventory, prioritize accurate forecasting and thoughtful planning. Leverage tools like sales data, inventory trends, and cash flow forecasts to predict your true needs and avoid piling up unnecessary stock. Regularly refresh these forecasts using real-time data and scenario analysis to ensure your purchasing aligns with actual sales patterns.

Keep an eye on key metrics like Days Inventory Outstanding (DIO) and shifting demand trends. These insights help you make smarter buying decisions, ensuring you borrow just enough to keep your stock at optimal levels - without the risk of overstocking.