Modern lenders no longer rely on old-school credit scores and collateral to fund eCommerce brands. Instead, they analyze real-time data from platforms like Shopify, Amazon, and TikTok Shop to assess your business. Here's what matters most:

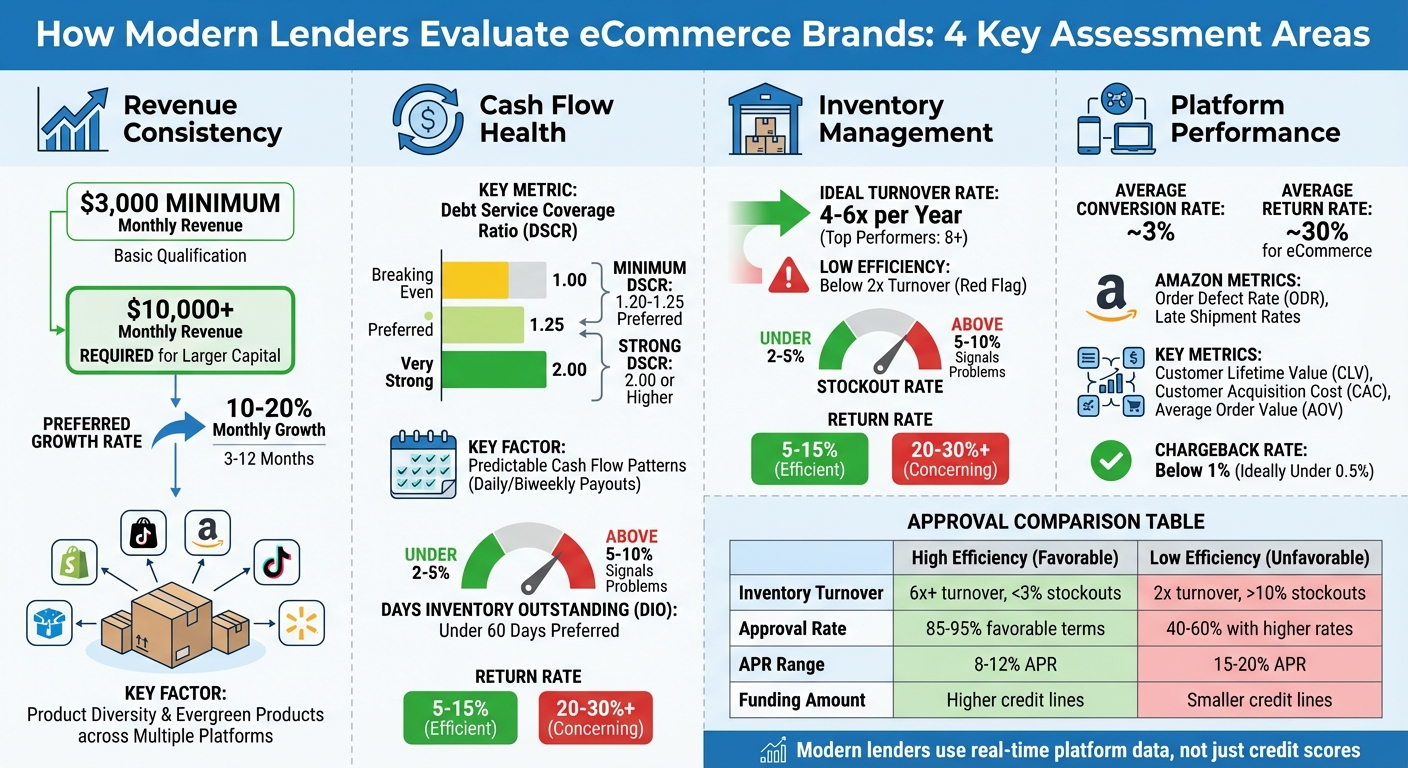

- Revenue Consistency: Lenders prefer stores with stable monthly sales ($3,000 minimum) and growth trends over 3–12 months.

- Cash Flow Health: Predictable cash flow, profitability, and a strong Debt Service Coverage Ratio (1.25+ preferred) are key.

- Inventory Management: Efficient inventory turnover (4–6x/year) and low stockout rates (<5%) show operational efficiency.

- Platform Performance: Metrics like conversion rates, Customer Lifetime Value (CLV), and account health (e.g., Amazon ODR) influence decisions.

To improve your chances, organize your financial data, integrate platforms for transparency, and focus on metrics that reflect your store's stability and growth potential.

How Modern Lenders Evaluate eCommerce Brands: Key Metrics and Benchmarks

Revenue Consistency and Growth Patterns

When it comes to assessing funding eligibility, modern lenders rely on 3–12 months of your store’s sales data to evaluate how stable and reliable your revenue is over time [1]. This transaction history plays a key role in determining whether your business qualifies for funding.

Monthly Revenue Stability

Lenders typically set minimum monthly revenue requirements. For basic qualifications, your store needs to generate at least $3,000 per month, while securing larger amounts of capital usually requires exceeding $10,000 in monthly revenue [1][4]. Beyond these benchmarks, lenders also analyze metrics like sales velocity and revenue trends.

With access to real-time sales data through connected platforms, lenders can gain a clear picture of your store's performance. They also keep an eye on operational factors like order defects and late shipments, as these directly affect your ability to maintain consistent sales [1].

"Sellers with steady (or rising) sales stand out. But even if your revenue dips seasonally, platforms like Onramp adjust eligibility based on your store's rhythm - not a rigid calendar."

Once revenue thresholds are met, lenders shift their focus to longer-term growth patterns.

Growth Trends Over Time

Lenders value businesses that show steady growth momentum over 3–12 months. Stores achieving monthly growth rates of 10–20% are often viewed more favorably and may secure better funding terms [1].

Product diversity is another critical factor. Lenders assess whether your revenue comes from a wide range of products or is heavily dependent on just one or two items. Relying too much on a limited product selection can increase risk, especially if demand for those products declines. On the other hand, having a mix of evergreen products - those that sell consistently year-round - combined with a presence on multiple platforms like Amazon, Shopify, and Walmart, demonstrates resilience and reduces perceived risk [1].

sbb-itb-d7b5115

Cash Flow and Financial Health

When lenders evaluate a business's financial stability, they don't stop at revenue consistency. They take a deeper dive into cash flow, profit margins, and debt management to get a full picture of financial health.

Cash Flow Patterns

A steady and predictable cash flow is a big green flag for lenders. For example, businesses with frequent cash inflows - like daily or biweekly payouts - are seen as lower risk because they’re better positioned to handle repayments. To get a clearer view, lenders often connect directly to major eCommerce platforms. This allows them to track how quickly inventory is converted into cash and verify bank transactions, ensuring that cash flow remains consistent. Businesses operating across multiple marketplaces also stand out, as they’re less dependent on any single sales channel for revenue stability [1].

"The more transparent and frequent your cash flow, the lower your perceived risk."

- Onramp Funds [1]

Beyond cash flow regularity, lenders also look at profitability and how well a business manages its debt.

Profit Margins and Debt Service Coverage Ratio

One key metric lenders use is the Debt Service Coverage Ratio (DSCR). This is calculated by dividing net operating income by total debt service. A DSCR of 1.00 means the business is breaking even, while most lenders prefer to see a ratio of at least 1.20 to 1.25. A DSCR of 2.00 or higher is considered very strong. Many loan agreements include DSCR covenants, which means if your ratio dips below the agreed threshold, lenders may step in. This could involve actions like claiming a percentage of your revenue until the ratio improves. Keeping a close eye on your DSCR monthly can help you spot potential issues early and make necessary adjustments to either boost revenue or cut expenses [5].

Inventory Management and Operations

Managing inventory effectively is a clear indicator of how well a business operates and its potential for growth. When lenders assess your business, they don’t just look at your sales numbers. They also consider how quickly you move products, how often you run out of stock, and whether too much capital is tied up in unsold inventory. These factors give them a better picture of your operational efficiency and financial health.

Inventory Turnover and Stockout Rates

Inventory turnover is a key metric that shows how often you sell and replace your inventory within a given period. It’s calculated by dividing your Cost of Goods Sold (COGS) by your average inventory value. For eCommerce businesses, a turnover of 4–6 times per year is common, while top performers hit 8 or more. On the flip side, a turnover below 2 suggests overstocked inventory, which could signal inefficiencies[3].

Stockout rate, another critical metric, is calculated as:

(stockouts ÷ total SKUs) × 100.

For smooth operations, this rate should stay under 2–5%. If it climbs above 5–10%, it can indicate issues with demand forecasting, which may hurt your revenue and customer satisfaction[2][3]. Lenders also pay close attention to sales velocity - how quickly you sell through your inventory - as it reflects market demand and operational agility[1].

"Risk assessment in eCommerce financing isn't about red tape. It's about real data, real performance, and real-world agility." - Onramp Funds[1]

How Inventory Efficiency Affects Funding Decisions

Let’s look at an example. A Shopify apparel brand generating $2M in revenue applied for $500K in funding but was denied. Why? Their inventory turnover was just 1.5x, meaning their stock sat unsold for about 243 days. Lenders saw this as a red flag, with too much capital tied up in inventory. After adopting demand forecasting tools and improving turnover to 5x, the brand reapplied and secured funding on much better terms[3].

| Metric | High Efficiency | Low Efficiency |

|---|---|---|

| Turnover & Stockouts | 6x+ turnover, <3% stockouts | 2x turnover, >10% stockouts |

| Approval Likelihood | 85–95% favorable terms | 40–60% with higher rates or denial |

| Funding Terms | 8–12% APR, higher amounts | 15–20% APR, smaller credit lines |

| Key Lender Concern | Scalability confirmed | Cash flow risk, overstock issues |

To make your business more appealing to lenders, consider strategies like just-in-time ordering or leveraging AI-driven demand forecasting tools through your eCommerce platform. Another useful metric to track is Days Inventory Outstanding (DIO), which is calculated as:

365 ÷ turnover rate.

A DIO under 60 days signals strong liquidity, which lenders view positively. Additionally, keep an eye on your return rates. Efficient brands typically maintain return rates between 5–15%, while rates above 20–30% could point to quality problems or cash flow challenges[3].

Platform Performance and Data Access

When it comes to assessing your business for funding, lenders look beyond just revenue and cash flow. They dive into how your eCommerce platform operates, using real-time performance data to make decisions. Gone are the days when credit scores and collateral were the only factors. Today, lenders connect directly to platforms like Shopify, Amazon, and TikTok Shop to evaluate your business's health and operations in real time[1][9]. This data forms the backbone of the key metrics they analyze.

Platform Metrics That Matter

Lenders focus on metrics that reflect the strength and stability of your business. For instance, they examine conversion rates, which hover around 3% for most eCommerce sites[6]. They also consider repeat purchase rates and Customer Lifetime Value (CLV) to understand your long-term growth potential[6][8].

If you’re an Amazon seller, your account health metrics are a big deal. Lenders will review your Order Defect Rate (ODR), late shipment rates, and customer feedback scores to assess how smoothly your operations are running. They’ll also evaluate your product portfolio by looking at your ASIN concentration to ensure you’re not overly reliant on just a few products[1].

Marketing efficiency is another area under the microscope. Lenders compare your Customer Acquisition Cost (CAC) to metrics like Average Order Value (AOV) and CLV. If you’re spending more to acquire customers than they’re worth, it raises red flags[6][8]. Additionally, high return rates - given that the average eCommerce return rate is about 30% - could signal issues with product quality or customer satisfaction[7].

Data Integration Quality

In addition to these metrics, the way you manage and share your data can significantly influence your funding prospects. Directly integrating your platform with a lender’s system through APIs provides a seamless flow of accurate, real-time data[1]. This automated syncing ensures that lenders have a clear view of your sales, cash flow, and fulfillment operations, reducing the chances of errors and delays[10].

Diversification also plays a role. Businesses that sell across multiple channels - like running both an Amazon storefront and a Shopify store - are seen as less risky because they’re not overly dependent on a single platform[1]. Using accounting software that syncs with your bank accounts and payment processors adds another layer of transparency, keeping your financial records up-to-date and helping lenders speed through the underwriting process[10].

"Approval is based on real-time sales data from platforms like Amazon, Lazada, Shopee, or TikTok Shop, not just credit scores or collateral." - Shabnam Mansukhani, CrediLinq[9]

How to Improve Your Appeal to Lenders

Getting approved for funding requires clear organization, transparent records, and a solid plan to repay. The good news? Most of what lenders evaluate is within your control. By tidying up your financial records, understanding how much you can realistically borrow, and preparing for flexible repayment options, you can increase your chances of approval. Let’s break it down step by step.

Clean Up Financial Records and Data

Your financial records are the backbone of any loan application. Start by centralizing all your sales data - whether it’s from Amazon, Shopify, Walmart, or TikTok Shop - into one comprehensive view. This makes it easier for lenders to see consistent cash flow patterns and ensures transparency in your operations [1].

Pay attention to your account health metrics, too. For example, keeping your chargeback rate below 1% (and ideally under 0.5%) can make a big difference in how lenders perceive your reliability [11]. To further strengthen your profile, tighten your fulfillment timelines, clarify return policies, and avoid spikes in refunds. If you’re using Shopify, consider leveraging Shopify Payments or Shop Pay regularly. These platform-native systems can boost your visibility and improve your eligibility scores [11].

Another key factor is how you plan to use the funds. Detail how the money will grow your revenue - whether it’s restocking fast-moving inventory or scaling up ad campaigns [1]. Diversifying your product mix can also help. Offering evergreen products, instead of relying solely on seasonal or trending items, signals stability and can lead to better funding terms [1].

Use Funding Calculators to Plan Ahead

Before applying for a loan, take advantage of funding calculators to estimate how much you can borrow and what repayment might look like. These tools provide month-by-month repayment schedules, breaking down payments into principal and fees while showing your remaining balance over time [12]. Many calculators allow you to adjust funding amounts - ranging from $2,500 to $500,000 - and test different terms, like 6-month versus 12-month repayment periods, so you can see how monthly payments change [13].

It’s also smart to stress test your financial data. For example, model a 20% revenue drop over the past 60 days to see if you could still meet repayment requirements during slower sales periods [11]. A profit margin calculator can also be helpful. By inputting your costs and selling prices, you can confirm that your unit economics are strong enough to handle repayment while covering operating expenses [14].

"A loan repayment calendar shows the borrower how much they need to pay each month, the portion that goes towards principal and interest, and the remaining balance of the loan." - DecisionRules [12]

With these financial estimates in hand, you’ll be better prepared to present a repayment plan that lenders can trust.

Prepare for Sales-Based Repayment

If you’re considering sales-based financing - where repayment is a fixed percentage of your daily or weekly revenue - you’ll need to be ready with real-time data and a solid plan. Start by enabling direct data integration with your eCommerce platform. This allows lenders to access up-to-date sales metrics, speeding up the approval process and making automatic repayment adjustments easier [16].

Next, verify that your profit margins are high enough to absorb repayment fees, which typically range from 6% to 12% of the loan amount [16]. It’s also a good idea to create a backup plan in case sales take an unexpected dip. This shows lenders that you’ve thought through potential challenges and are financially responsible [15].

Finally, align your funding use with activities that directly generate revenue, like marketing campaigns or bulk inventory purchases. This ensures a healthy repayment cycle. Some lenders, like Onramp Funds, offer repayment plans that scale with your sales - slowing down during slow periods and speeding up when business is booming. But even with this flexibility, it’s crucial to ensure your baseline margins can handle the repayment percentage.

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital." - Paul Voge, Co-founder and CEO, Aura Bora [16]

Key Takeaways

When assessing eCommerce brands, modern lenders focus on four main areas: revenue consistency, which reflects steady and reliable growth; cash flow health, showing strong financial management; inventory efficiency, with turnover rates typically between 4–6 times a year and minimal stockouts; and platform performance, supported by integrated data from sales channels[3]. These metrics move away from traditional credit-score-based evaluations, relying instead on real-time data and operational transparency.

To improve your appeal to lenders, start by organizing your financial records. Consolidate sales data from major platforms like Amazon, Shopify, Walmart, and TikTok Shop. Keeping your order defect rates low demonstrates operational reliability, which is a key signal of trustworthiness. Additionally, use funding calculators to simulate different repayment scenarios. Ensure your profit margins can handle sales-based repayments - often 10–15% of your monthly revenue - and prepare for slower sales periods to maintain repayment capability.

The rise of embedded finance and AI-driven lending is transforming the industry. Lenders now prefer brands that provide omnichannel data and real-time inventory tracking. This allows for instant approvals and tailored loan terms, significantly reducing origination costs and delivering funds in as little as 24 hours.

FAQs

What can eCommerce brands do to improve their chances of getting approved for funding?

To improve your chances of securing funding, start by ensuring your financial records are in excellent shape. This means keeping everything up-to-date, from tax returns and bank statements to incorporation documents. Show potential lenders that you’re on top of your finances by tracking key metrics like monthly sales, cash flow, and outstanding debt. Highlighting your ability to manage new funding is crucial. Additionally, having strong business credit scores and meeting common benchmarks - such as generating at least $3,000 in monthly revenue and operating for 6 to 12 months - can significantly improve your eligibility.

Your operational performance matters just as much. Consistent sales on platforms like Shopify or Amazon, coupled with strong account health metrics (think positive customer reviews and low order defect rates), can make a big difference. On top of that, efficient inventory management, accurate revenue forecasting, and diversifying your sales channels will help demonstrate stability and lower risk. These efforts can make you stand out as a dependable and appealing candidate for funding.

What do lenders look for when evaluating eCommerce businesses?

Lenders evaluate eCommerce businesses by looking at critical financial and operational metrics to gauge their stability and growth potential. These factors typically include revenue consistency (like monthly sales trends and growth rates), cash flow stability (operating cash flow and debt levels), and efficiency metrics such as average order value, inventory turnover, and payment cycles.

They also consider customer-related metrics like lifetime value, order defect rates, and customer reviews. On top of that, platform performance on sales channels - whether it’s Shopify, TikTok Shop, or others - plays a role in the assessment. Keeping detailed, accurate financial records and using data-driven tools to showcase your business metrics can make a strong impression on potential lenders.

Why is good inventory management important for securing better funding terms?

Efficient inventory management plays a crucial role in securing favorable funding terms. It signals to lenders that your business maintains steady cash flow, avoids the pitfalls of overstocking or running out of stock, and treats inventory as dependable collateral. This helps reduce the lender's risk, making them more likely to offer better financing options.

By ensuring your inventory is well-organized and closely aligned with market demand, you showcase both operational efficiency and financial stability - two critical factors lenders prioritize when assessing eCommerce businesses.