Running an eCommerce business means managing cash flow gaps while balancing growth opportunities. To succeed, you need to know when to use growth capital or survival capital.

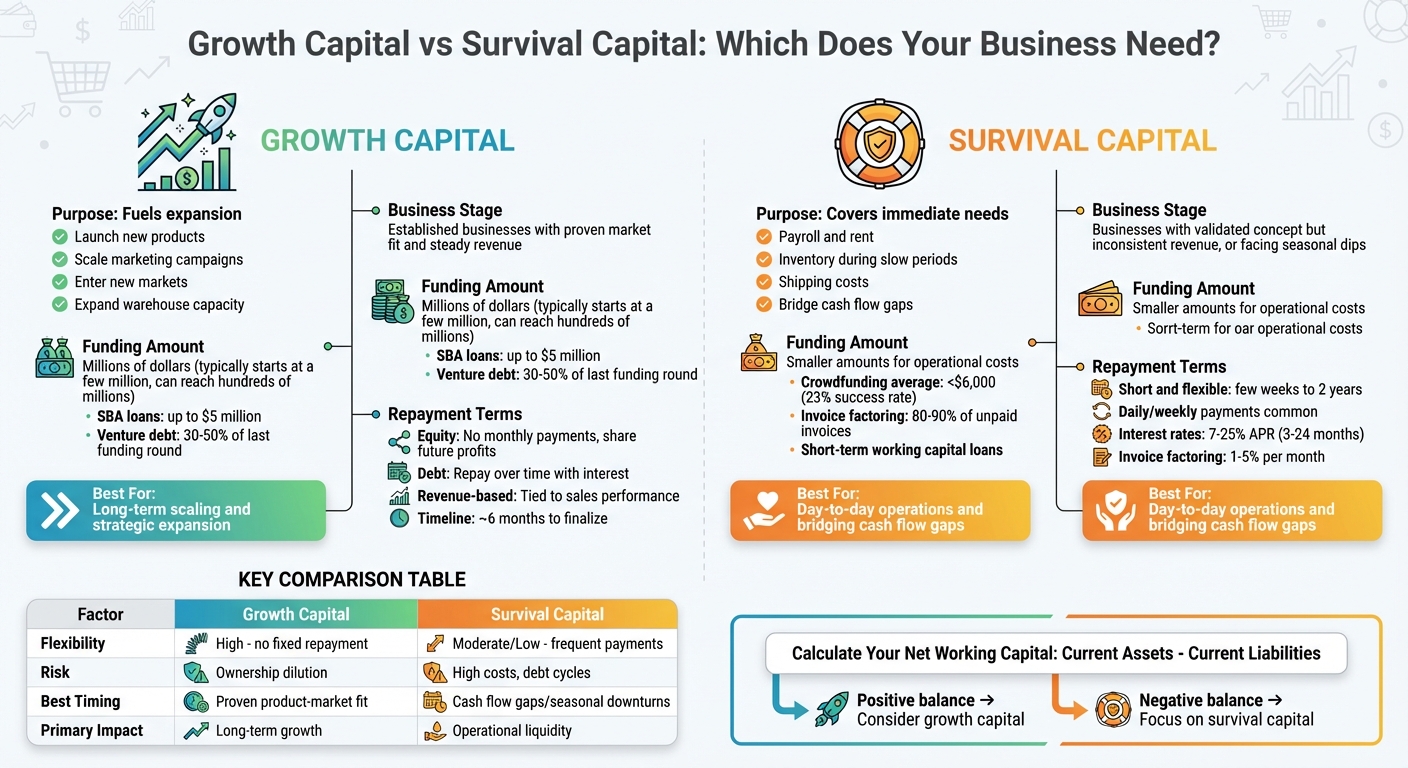

- Growth Capital: Funds expansion - like launching new products, scaling marketing, or entering new markets. Best for businesses with steady revenue and proven market fit. Often involves larger investments (millions of dollars) and can take forms like equity, debt, or revenue-based financing.

- Survival Capital: Covers immediate needs - like payroll, rent, or inventory during slow periods. Ideal for businesses facing cash flow gaps or seasonal dips. Involves smaller amounts and shorter repayment terms, such as invoice factoring or merchant cash advances.

Key takeaway: Growth capital fuels long-term scaling, while survival capital ensures day-to-day operations stay on track. Choosing the right type depends on your business's current stage and priorities.

Growth Capital vs Survival Capital: Key Differences for eCommerce Businesses

1. Growth Capital

Growth capital is a financial boost aimed at helping established eCommerce businesses expand. It’s designed for companies that already have a solid business model, steady revenue, and strong financial fundamentals [6][8].

Let’s break down how growth capital supports strategic expansion.

Purpose

Growth capital isn’t meant for everyday operational costs. Instead, it’s used to fund major initiatives like:

- Running outbound advertising campaigns

- Hiring sales or technical teams

- Researching and developing new products

- Stocking up inventory for entering new markets

- Expanding into related product categories [7][8][9]

For example, if your eCommerce store has proven demand for its products and you’re ready to scale up with a big marketing push or need to grow warehouse capacity, growth capital can provide the financial support to make it happen.

Business Stage

This type of funding works best for businesses that have moved past the startup phase and proven their concept in the market. Companies with predictable revenue, healthy profit margins, and clear growth potential are ideal candidates [6][8].

If your business is still figuring out product-market fit or struggling to manage basic operations, growth capital may not be the right fit yet. It’s tailored for businesses in the expansion stage, where rapid growth often creates temporary cash flow gaps due to upfront investments in areas like staffing, software, or infrastructure.

Funding Amount

Growth capital typically involves larger investments compared to seed funding. While seed rounds generally range from $50,000 to $2 million, growth capital often starts at a few million dollars and can go up to hundreds of millions [8].

The exact amount depends on your revenue history. For instance, term loans are often calculated as a multiple of your current revenue [6]. Small Business Administration (SBA) loans for growth can go up to $5 million with favorable terms [1][11], and venture debt may provide 30% to 50% of your last funding round [11].

Repayment Terms

Growth capital can take different forms:

- Equity: Investors take a share of future profits, so there are no monthly payments.

- Debt: Loans are repaid over time with interest, allowing you to keep full ownership.

- Revenue-based financing: Repayments are tied to your sales performance.

Deals typically take about six months to finalize [6][7][8][9][10].

2. Survival Capital

Survival capital is all about keeping your eCommerce business afloat during tough times. It’s the short-term funding that gets you through cash flow gaps, helping you cover essentials like payroll, rent, inventory, shipping, and even website maintenance. The goal? To keep the business running until your revenue becomes more predictable.

"The Survival Business focuses on meeting monthly expenses and generating enough profit for the owner."

- Dhanraj Kumavat, Author, The Productivity Way [12]

This type of funding becomes crucial once your business has proven it can attract customers but hasn’t yet achieved steady revenue. It’s also a lifeline during unexpected challenges, like supplier delays, seasonal slowdowns, or when cash is tied up in inventory ahead of a busy sales period.

Purpose

Survival capital isn’t about growth or scaling; it’s about addressing immediate financial needs. In eCommerce, this often means replenishing inventory, covering shipping costs, or bridging the gap between paying suppliers and receiving customer payments.

The focus here is reactive. It’s about handling urgent issues like stock shortages, seasonal revenue dips, or cash flow gaps that could otherwise bring your operations to a halt. Unlike growth capital, which looks to the future, survival capital is firmly rooted in keeping the day-to-day running smoothly.

Business Stage

Survival capital is most relevant in the Survival Stage, the second phase of business growth. At this point, you’ve validated your business idea, built a customer base, and started generating revenue. However, that revenue isn’t yet consistent enough to fully fund your operations or expansion.

This stage can be tricky. Many businesses fail here - around 80% of small businesses don’t make it past their first year due to cash flow problems, high expenses, or poor management [13]. The challenge is to move from just surviving to finding a sustainable balance between income and expenses. This is where survival capital plays a critical role, offering flexible funding tailored to your immediate needs.

Funding Amount

Survival capital usually involves smaller amounts compared to growth capital. Instead of millions for expansion, survival funding focuses on covering immediate operational costs.

For example, early-stage businesses often turn to crowdfunding, where the average campaign raises less than $6,000, and only about 23% of campaigns hit their goals [2]. For more mature businesses, funding might come through performance-based options like invoice factoring, which advances 80% to 90% of unpaid invoice values, or revenue-based financing, where repayments adjust according to your sales [14]. These smaller, short-term funding options distinguish survival capital from the larger-scale investments associated with growth funding.

Repayment Terms

The repayment terms for survival capital are typically short and flexible, often ranging from a few weeks to two years. Merchant cash advances and short-term loans often require daily or weekly payments, which can be challenging during slower periods.

For instance, working capital loans might come with interest rates of 7% to 25% APR and terms lasting 3 to 24 months. Invoice factoring, on the other hand, can charge 1% to 5% per month on the advanced amount. Revenue-based financing offers more flexibility, as repayments are tied directly to your sales - if sales slow down, your payments decrease too [14]. However, frequent payments can still strain your finances during downturns, so it’s important to weigh the pros and cons of each option carefully.

sbb-itb-d7b5115

Pros and Cons

Building on our earlier discussion, the advantages and challenges of different funding types highlight how crucial it is to align your financial strategy with your business's needs. Here's a closer look at how growth capital and survival capital serve distinct purposes, depending on where your business stands.

Growth capital, typically equity-based, offers a major upside: no fixed repayment obligations. This means you can direct your cash flow toward scaling your business without worrying about immediate financial outflows. However, this freedom comes at a cost. You might face ownership dilution, meaning a reduced share of your company and possibly less control over key decisions. Timing also plays a big role - securing growth capital too early could result in less favorable terms, while waiting too long might mean missing critical market opportunities.

"Growth capital investors focus on companies with a proven business model, positive unit economics, and significant market potential. Essentially, these investors want to pour metaphorical gasoline onto the fire." - Arc Team [8]

Survival capital, on the other hand, is designed for speed and immediate needs. It’s an excellent tool for bridging seasonal cash flow gaps or covering unexpected expenses, like inventory shortages. Revenue-based financing, a common form of survival capital, adjusts repayments based on your sales, offering some flexibility. But there’s a catch: many survival capital options, such as merchant cash advances or factoring, come with frequent repayment schedules - often daily or weekly. This can strain your cash flow during slower periods. If not carefully managed, high-cost options could lead to a cycle of debt.

Here’s a quick side-by-side comparison to break it down further:

| Factor | Growth Capital | Survival Capital |

|---|---|---|

| Flexibility | High - no fixed repayment schedule | Moderate to low - frequent repayment needed |

| Risk | Ownership dilution and reduced decision control | Higher financing costs; risk of debt cycles |

| Best Timing | When product-market fit is proven | During cash flow gaps or seasonal downturns |

| Primary Impact | Drives long-term growth | Maintains operational liquidity |

Choosing between growth and survival capital boils down to your business's current stage and priorities. Growth capital is ideal for scaling a validated business model, while survival capital is essential for navigating short-term financial hurdles. Aligning your funding strategy with your immediate and long-term goals ensures your business stays on a sustainable path.

Conclusion

Growth capital and survival capital serve two very different purposes, and understanding which one your business needs starts with a simple question: What’s your priority right now? Survival capital is all about keeping things running - it helps cover inventory shortages, smooth out seasonal cash flow dips, and handle unexpected supply chain hiccups. Growth capital, however, is focused on the bigger picture, like expanding into new markets, acquiring competitors, or scaling operations.

To make the right funding choice, start by crunching the numbers. Calculate your net working capital (Current Assets – Current Liabilities). A positive balance means you’re in a stable position to explore growth opportunities. A negative balance signals it’s time to focus on survival capital to meet immediate financial needs [1][5]. Planning ahead is crucial - waiting until a crisis hits can force you into costly emergency financing [3].

"If the business is failing, funding might not be the right answer." - Luis Gonzalez, Former Senior Content Marketing Manager, Ramp [4]

Match your funding strategy to your business’s current stage and goals. If you’ve already validated your business model and want to scale without losing equity, non-dilutive options like revenue-based financing could be a smart move. On the other hand, if you’re dealing with a temporary cash crunch, survival capital with flexible repayment terms can help you weather the storm. Take Glitch Energy as an example: they grew from $0 to seven figures in just one year by choosing flexible funding over venture capital, allowing them to maintain full ownership while scaling [15].

FAQs

How can I tell if my business needs growth capital or survival capital?

Determining whether your business needs growth capital or survival capital comes down to your financial position and what you aim to achieve.

If you're finding it hard to cover essential costs - like payroll, supplier payments, or restocking inventory - you’re likely in need of survival capital. This type of funding is designed to keep your operations steady during tough times, ensuring the business can continue functioning without interruptions.

However, if your finances are stable and you're aiming to expand - whether that means breaking into new markets, launching products, or scaling your operations - growth capital is the way to go. This funding focuses on fueling initiatives that drive expansion while maintaining your current financial health.

Take a close look at your cash flow, operational stability, and long-term goals. Whether it’s tackling immediate financial hurdles with survival capital or chasing bigger opportunities with growth capital, aligning the funding to your situation can help secure your business’s future.

What risks can arise from choosing the wrong type of funding?

Choosing the wrong type of funding can create major hurdles for your eCommerce business. For example, opting for growth capital when your business isn’t ready or lacks steady profitability can make it tough to meet repayment terms or satisfy investor demands. This could lead to financial stress or, worse, losing control of your business.

On the flip side, depending on survival capital - like short-term loans or emergency funds - when your business really needs long-term growth capital can leave you without the resources to expand. This can stifle your ability to scale and stay competitive. Plus, mismatched funding can throw off your cash flow, especially if repayment schedules don’t align with your revenue cycle. This increases the risk of operational disruptions or even insolvency.

To steer clear of these pitfalls, it’s essential to evaluate your business’s financial needs carefully and select funding that supports both your immediate stability and future growth plans.

How can survival capital support my business during slow seasons?

Survival capital gives your business the financial breathing room it needs to stay steady during slower seasons when revenue dips. It ensures you have enough cash on hand to handle essential expenses like stocking inventory, paying employees, and covering operational costs. This helps you avoid interruptions and keeps things running smoothly.

Think of it as a safety cushion that helps you weather seasonal ups and downs without scrambling to cut costs or take on last-minute loans. With survival capital in place, your business can maintain its operations and be ready to thrive when sales pick up again.