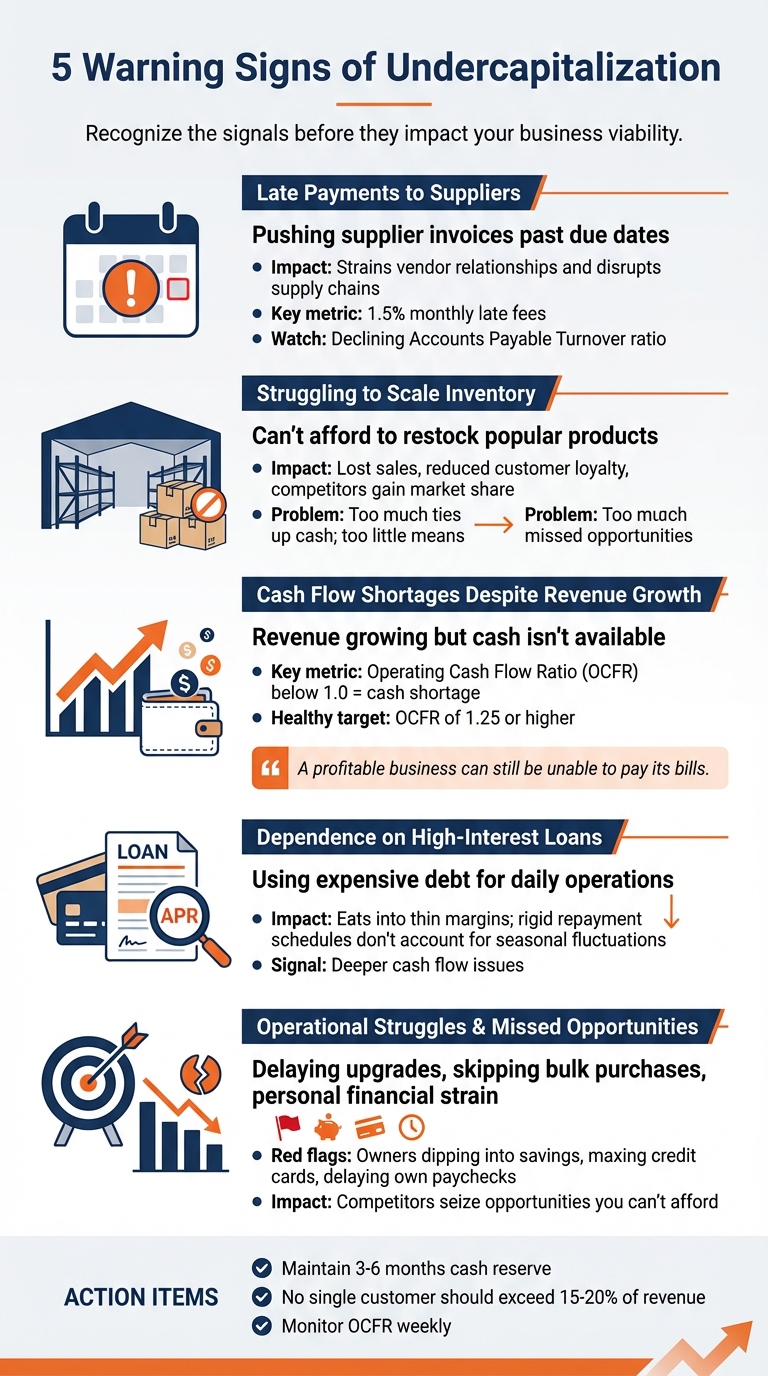

Undercapitalization can silently undermine your business, even when revenue is growing. Many businesses face cash flow gaps - where expenses like inventory and marketing outpace incoming cash - leading to operational struggles. Here’s what to watch for:

- Late Supplier Payments: Delayed invoices strain vendor relationships and risk supply chain disruptions.

- Inventory Challenges: Stockouts or overstocking tie up cash and hurt sales.

- Cash Flow Shortages: Revenue growth without liquidity creates financial strain.

- High-Interest Debt Reliance: Using expensive loans for daily operations signals deeper issues.

- Missed Growth Opportunities: Limited funds prevent scaling and investments.

Key Fixes:

- Use revenue-based financing to align repayments with sales.

- Monitor cash flow with real-time tools to identify gaps early.

- Build a reserve covering 3–6 months of expenses to stay prepared.

Even profitable businesses can fail without proper cash flow management. Spot the signs early, take action, and secure your financial stability.

How To Stop Your Business Failing From Undercapitalisation

Warning Signs of Undercapitalization

5 Warning Signs Your Business Is Under-Capitalized Despite Revenue Growth

Catching undercapitalization early can save your business from falling into a financial crisis. Below are the key warning signs that your working capital might not be sufficient to keep your operations running smoothly.

Late Payments to Suppliers

Pushing supplier invoices past their due dates is a telltale sign of cash flow trouble. Essentially, you're leaning on your vendors for free credit. This practice not only strains your relationships with suppliers but can also disrupt your supply chain [4]. Vendors may tighten payment terms, reduce order quantities, or even stop working with you altogether, leaving you unable to meet customer demands when it matters most.

Keep a close eye on your Accounts Payable Turnover. A declining ratio suggests liquidity problems and could indicate frayed vendor relationships [5]. Late payments also come with penalties - standard late fees are often around 1.5% monthly [5] - which can worsen your financial strain.

Struggling to Scale Inventory

If you can't afford to restock popular products, it's a clear signal that your working capital is stretched too thin. Inventory often requires upfront payment, long before you see any revenue [2]. This creates a cash flow bottleneck, leading to stockouts that not only cost you immediate sales but also hurt customer loyalty and your standing in the marketplace. Competitors can easily swoop in to take advantage of your inability to meet demand [2].

For eCommerce businesses, inventory is a double-edged sword. Buying too much ties up cash in unsold goods, while buying too little means missed opportunities during peak sales periods [4].

Cash Flow Shortages Despite Revenue Growth

Revenue growth can be misleading if your cash flow isn't keeping pace. A key metric to watch is your Operating Cash Flow Ratio (OCFR), which is calculated by dividing cash flow from operations by current liabilities. A ratio below 1.0 signals cash shortages, while a healthy business should aim for an OCFR of 1.25 or higher [3].

Problems worsen when you offer extended payment terms to customers (e.g., net-30 or net-90) but need to pay suppliers immediately [3]. This mismatch creates a funding gap that grows as your sales increase. You might be making sales on paper, but the cash isn't available when critical expenses like rent, payroll, or inventory invoices are due. As Shopify explains:

"A profitable business can still be unable to pay its bills. Similarly, just because a business is meeting all of its financial obligations doesn't mean it's profitable" [1].

This highlights the gap between revenue and actual liquidity - a distinction every business owner should understand.

Dependence on High-Interest Loans

Relying on expensive short-term debt to cover daily expenses, rather than using it for strategic growth, points to a deeper cash flow issue [4]. Margins in eCommerce are often razor-thin, and high interest rates quickly eat into your profits [2].

Another complication with short-term loans is their rigid repayment schedules, which don't account for the seasonal ups and downs common in eCommerce [4][6]. During slower months, these fixed payments can drain your reserves, making it even harder to balance your cash flow. If you're regularly using high-interest debt for daily operations, it’s a clear sign of financial instability.

Operational Struggles and Missed Opportunities

Limited working capital forces tough decisions, like delaying technology upgrades or skipping bulk inventory purchases that could lower costs. Over time, these constraints allow competitors with stronger financial positions to seize opportunities you can't afford to pursue.

Another red flag is personal financial strain - when business owners dip into their own savings, max out credit cards, or delay their own paychecks to keep operations afloat [1]. If you're personally subsidizing your business, it’s a strong indicator that the company itself lacks sufficient capital.

Here’s a quick summary of how these red flags impact your business:

| Red Flag | Impact on Your Business |

|---|---|

| Late Supplier Payments | Strains vendor relationships and disrupts supply chains [4]. |

| Frequent Stockouts | Results in lost sales, lower search rankings, and reduced market share [1][2]. |

| Payroll Delays | Signals severe cash shortages and risks losing valuable employees [1]. |

| Cutbacks on Growth Investments | Reducing marketing or technology spending slows growth and weakens competitiveness [1]. |

| Dependence on High-Interest Debt | Can lead to a debt spiral that drains profits and cash reserves [4]. |

To safeguard your business, aim to maintain a cash reserve that covers 3–6 months of expenses. Additionally, diversify your revenue streams - no single customer should account for more than 15–20% of your total revenue. This reduces the risk of cash flow disruptions if a major client delays payment [5].

How to Fix Undercapitalization

If you're seeing signs of undercapitalization, it's time to take action. Addressing cash flow issues quickly can help stabilize your finances and set the stage for growth. Here's how you can tackle common challenges like late supplier payments, inventory struggles, and reliance on expensive loans.

Revenue-Based Financing with Onramp Funds

One way to smooth out cash flow fluctuations is through revenue-based financing (RBF). This type of funding adjusts repayments based on your sales - when business is booming, you pay more; during slow periods, you pay less [6][7].

"Revenue-based financing (RBF) is one of the most flexible funding solutions for Amazon sellers, especially when sales are seasonal or unpredictable." - Onramp Funds [6]

Onramp Funds makes this process seamless by integrating with major platforms and delivering funding within 24 hours, all while letting you retain 100% ownership. Repayment fees range from 6% to 12% of revenue, and you can borrow up to one-third of your annual recurring revenue or four to seven times your monthly recurring revenue [6][7].

But funding alone isn't enough. Real-time cash flow management tools can help you stay ahead of potential issues.

Use Cash Flow Management Tools

To avoid cash flow surprises, real-time tracking tools are a game changer. These tools connect directly to platforms like Amazon Seller Central and Shopify, pulling sales and inventory data to give you a clear view of your finances [1]. Many also allow you to forecast cash flow gaps up to 12 months in advance, helping you prepare for seasonal trends, supplier delays, or big marketing pushes [2].

"Cash flow management tools and automation can help business owners streamline decision-making and avoid risky cash shortfalls." - Onramp Funds [1]

Pay close attention to metrics like receivables turnover and inventory cycles. For example, tracking how long it takes to convert inventory and marketing investments into actual sales revenue can help you prevent shortages [2]. Tools like QuickBooks can also highlight spending patterns and cash flow gaps, giving you the insights you need to make informed decisions [8].

Once you’ve stabilized your cash flow, the next step is building a financial cushion.

Build a Capital Reserve

A strong capital reserve can cover 3–6 months of operating expenses, giving you a safety net for unexpected challenges [2][8]. Onramp Funds' flexible repayment model makes it easier to build this reserve. Since payments adjust with your sales, you can save more during high-revenue periods and conserve cash when sales slow down [6].

Use your reserve strategically. For instance, you can secure bulk order discounts from suppliers, maintain inventory during peak seasons, or ramp up advertising when demand is high [8]. The key is to borrow with purpose, ensuring every dollar you spend delivers measurable results and a solid return on investment [8].

sbb-itb-d7b5115

Examples of Businesses That Fixed Undercapitalization

Many eCommerce businesses have successfully tackled undercapitalization by combining flexible financing options with strategic planning. These stories highlight how revenue-based funding can address cash flow challenges and fuel growth.

Scaling Inventory During Peak Seasons

KMR Bakery, a niche eCommerce bakery, faced a sudden surge in demand when a competitor shut down. Without sufficient credit, they ran into stockouts, losing potential sales. To turn things around, the owner opted for revenue-based financing. This allowed them to stock up on inventory, invest in equipment, and seize the opportunity to capture market share - all while maintaining steady revenue growth [14].

Similarly, a tech retailer underestimated the capital required for the holiday season. Revenue-based financing became their lifeline, enabling them to expand inventory, keep up with supplier payments, and ultimately increase sales by 50% [13]. The repayment structure, tied to their sales, provided flexibility - higher payments during peak sales weeks and lower payments during slower periods. This adaptability helped them avoid the financial strain that comes with rigid loan terms.

Better Cash Flow with Flexible Repayment Plans

Another eCommerce store, heavily reliant on paid ads, struggled with recurring cash shortages despite increasing revenue. By switching to Onramp Funds' sales-based repayment model - where 5-10% of daily revenue was used for repayments instead of fixed monthly payments - they stabilized their cash flow and reduced interest costs by up to 50% [11][12]. The automated system, synced with their sales deposits, eliminated the hassle of manual payments and the risk of missing deadlines [9].

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales." - Jeremy, Founder and Owner, Kindfolk Yoga [9]

Other businesses that adopted flexible repayment models saw their profit margins swing from negative to 15% [11][15]. During slower sales periods, repayments paused, allowing them to reinvest their cash into growth instead of servicing fixed debt [10][12]. This approach also helped them diversify their supplier base and maintain steady growth over 12-24 months without the stress of creditor demands [10][12].

These examples illustrate how revenue-based financing can transform undercapitalized businesses into thriving operations ready for sustainable growth.

Conclusion

A growing revenue stream doesn’t always mean your business is financially secure. Signs like overdue supplier payments, inventory shortages, cash flow gaps, dependence on high-interest credit, and missed opportunities for growth can point to a deeper issue: undercapitalization. Ignoring this problem has proven fatal for 82% of small businesses [8].

To avoid this fate, start with disciplined financial management. Review your finances regularly - weekly account reconciliations are a must. Calculate your operating cash flow ratio (aim for at least 1.25) [3], and work toward building a cash reserve that can cover six months of expenses [4]. These steps offer a more accurate view of your business's financial health, going beyond just tracking sales figures.

If you identify cash flow gaps, financing options can help. For example, revenue-based financing adjusts repayment amounts based on your sales, reducing strain during slower periods [16]. With repayments automatically linked to daily sales, this approach eliminates the stress of fixed payments while maintaining consistent cash flow.

"Hyper-focusing on expenses, cash flow, and receipts is wise in any economic climate – and doubly so in recessionary times." - Eric Youngstrom, Founder and CEO, Onramp [16]

FAQs

What are the warning signs that your business may be undercapitalized, even with growing revenue?

Undercapitalization occurs when a business lacks the cash needed to handle daily operations or support growth, even when revenue is on the rise. This can result in cash shortages that disrupt critical areas like inventory, payroll, marketing, and supplier relationships.

Here are some key warning signs to watch for:

- Delayed supplier payments or frequent requests to extend payment terms, which can signal cash flow issues.

- Inability to scale inventory to meet growing demand because funds are tied up or unavailable.

- Heavy reliance on high-interest credit, such as credit cards or short-term loans, which can erode profitability over time.

- Late customer payments, creating gaps in cash flow that can affect the entire business.

- Negative operating cash flow, even when profits are reported, suggesting cash is tied up in receivables or expenses.

- Low working capital ratio (current assets ÷ current liabilities) below 1.5:1, which indicates a limited ability to meet short-term financial obligations.

Catching these red flags early gives you the chance to act. Steps like streamlining your invoicing, negotiating better terms with suppliers, or exploring financing options can help address cash flow problems and keep your business moving forward.

How does revenue-based financing help solve cash flow problems?

Revenue-based financing gives eCommerce businesses access to upfront capital, which is repaid as a percentage of their monthly gross revenue. The repayment adjusts based on your sales performance, making it a more manageable option for cash flow.

This model helps tackle common cash flow hurdles like delayed supplier payments, low inventory levels, or surprise expenses - without the stress of fixed monthly payments. It’s a smart way to maintain smooth operations while fueling growth.

What are the best ways to build a capital reserve for my business?

Building a solid capital reserve begins with improving cash flow. Start by speeding up the money coming in - automate your invoices, offer discounts for early payments, and accept flexible payment methods like credit cards or ACH transfers. On the flip side, negotiate longer payment terms with your suppliers. Pair this with smart inventory management techniques, such as demand forecasting or just-in-time practices, to avoid locking up cash in extra stock. Cutting back on unnecessary expenses through automation and regular cost reviews can also free up funds to grow your reserve.

Using reliable cash flow management tools can make a big difference. These tools help you create accurate forecasts, track how you're performing against them, and adjust your spending when needed. A good goal is to build a "rainy day" fund that covers three to six months of operating expenses, giving you a cushion for unexpected challenges. If your cash flow alone can’t get you there, look into flexible financing options like revenue-based funding or invoice financing. These alternatives can help bridge gaps without piling on high-interest debt. By combining these approaches, you can create a reserve that keeps your business steady, even as it grows.