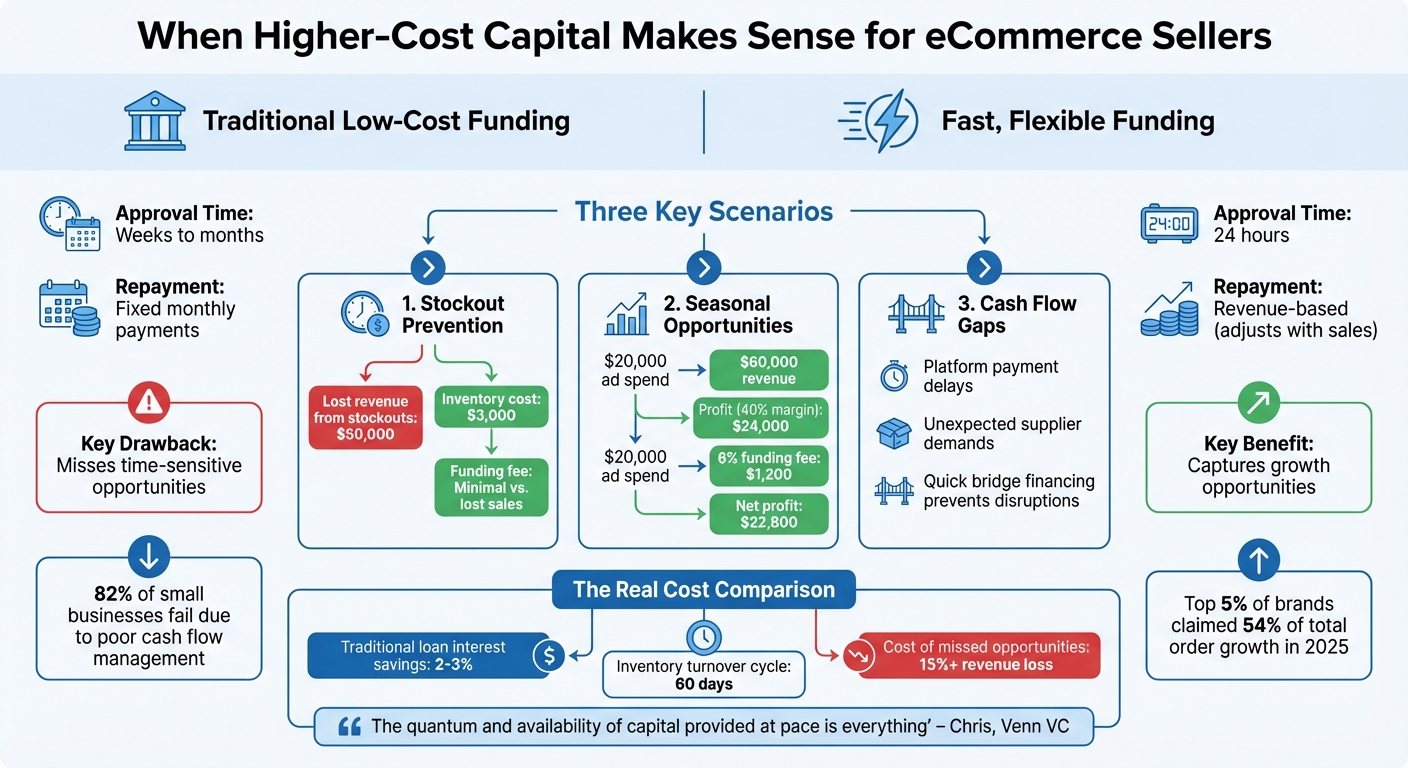

Paying more for funding can sometimes lead to better results. For eCommerce sellers, the cheapest loan isn't always the smartest choice. Quick, flexible funding can help avoid stockouts, seize time-sensitive opportunities, and handle unexpected expenses - all of which can drive higher revenue, even if the financing costs are higher. Here’s why speed and timing often outweigh low interest rates:

- Stockouts hurt sales and rankings. Fast funding helps restock inventory, preventing lost revenue and maintaining marketplace positions.

- Seasonal and viral trends don’t wait. Acting quickly with available capital ensures sellers can maximize these opportunities.

- Unexpected costs arise. Immediate funding can keep operations running smoothly, avoiding disruptions.

For example, tools like Onramp Funds provide funding within 24 hours, with flexible repayment tied to sales performance. This allows businesses to grow without the rigid terms of traditional loans. The bottom line? Higher-cost capital makes sense when the potential revenue gains outweigh the fees.

Traditional Loans vs Fast Funding for eCommerce: Cost-Benefit Analysis

eCommerce Funding Secrets Every Seller Should Know

sbb-itb-d7b5115

Why Low-Cost Funding Often Falls Short for eCommerce Sellers

Low-cost funding options may seem appealing at first glance, but they often fail to support the fast-paced growth demands of eCommerce businesses. Let’s take a closer look at why higher-cost capital often proves to be a better fit.

Traditional bank loans are known for their low interest rates and standardized terms. However, these benefits are overshadowed by their inability to keep up with the speed and flexibility required in today’s digital marketplace.

The main problem lies in mismatched funding timelines. Banks take weeks - or even months - to process loan applications [2]. Meanwhile, eCommerce opportunities can vanish in a matter of days. Whether it’s a viral product trend, a time-sensitive bulk discount from a supplier, or an unexpected surge in demand, these moments don’t wait for slow-moving loan approvals. As PEAC Solutions aptly puts it, "Waiting weeks for a traditional loan approval isn't an option" [2].

Traditional lenders also struggle to evaluate eCommerce businesses effectively. Their systems are designed to assess physical assets and conventional business models, not the digital metrics or brand equity that drive online sales [2]. This gap in understanding often leaves eCommerce sellers without the financial backing they need, especially when timing is critical.

Slow Approval Times Lead to Missed Opportunities

The sluggish approval process of traditional loans creates a major roadblock for eCommerce sellers. Just as a slow checkout process can drive customers away [3], delayed funding can cause sellers to miss crucial market opportunities.

Nick Robinson, Co-founder of Pick and Pull Sell Car, highlights the impact: "Sellers want a quick, seamless transition so they can move on to their next opportunity. Delayed funding undermines that, leaving them in a state of limbo and unable to plan effectively" [4].

This issue becomes even more pronounced during peak shopping seasons like Black Friday or Prime Day. Sellers need capital months in advance to stock up on inventory [6]. By the time a traditional loan is approved, competitors with faster funding have already captured the market.

The numbers tell a stark story: 82% of small businesses fail due to poor cash flow management [4]. In 2025, eCommerce orders in the US surged by 147% year-over-year. However, the growth wasn’t evenly distributed - the top 5% of brands claimed 54% of the total order growth [5]. What set these top performers apart? Many had immediate access to capital, allowing them to capitalize on opportunities as they arose, while slower-funded competitors were left behind.

On top of approval delays, traditional loans often come with rigid repayment terms that can strain cash flow during slower months.

Fixed Payment Schedules Don't Align with Sales Cycles

The seasonal nature of eCommerce creates unique cash flow challenges. Sellers often need substantial capital during peak months, but their revenue doesn’t materialize until later. Traditional loans, with their fixed repayment schedules, don’t account for these fluctuations, creating unnecessary financial strain.

For example, sellers must invest heavily in September and October to prepare for the holiday rush, but they won’t see the returns until November or December [6]. During slower months, fixed loan payments can drain working capital, leaving businesses struggling to cover essential costs.

As one expert on the Venn VC Podcast explained, "Ecommerce founders aren't looking to service long-term debt, they're looking to fund inventory, advertising, or logistics expenditures that get more products on the shelves" [6].

Traditional loans are typically designed for long-term investments, such as machinery or equipment. But eCommerce operates on short, high-turnover inventory cycles, where funding might be needed for a single order that sells out in 60 days [6].

This disconnect becomes even more problematic during unexpected downturns. Guillaume Drew, Founder and CEO of Or & Zon, shared his experience: "During the business's initial stages, delayed funding can stifle momentum and limit strategic possibilities" [4]. When sellers are locked into fixed payments while facing unpredictable revenue, they’re forced into tough decisions - like choosing between making a loan payment or restocking inventory. This can lead to stockouts, lost sales, and damaged supplier relationships, creating a cycle that’s hard to break.

Scenario 1: Restocking Inventory Quickly to Capture Sales

Running out of stock doesn't just stop sales - it can cause a steep drop in search rankings and advertising performance [9]. For sellers on platforms like Amazon or Walmart, this creates a ripple effect. Sales momentum halts, and the longer the stockout, the harder it becomes to recover. In fact, the financial impact of being out of stock often outweighs the cost of securing higher-priced funding to avoid it. This highlights the importance of having quick and adaptable funding options to prevent these cascading losses.

Lost Sales from Stockouts vs. Gains from Fast Restocking

Every day you're out of stock during peak demand is a day of lost revenue. But the damage doesn't stop there. Customers who can’t find your product are likely to switch to competitors, and regaining their loyalty later can be far more expensive than retaining them in the first place [7]. When you weigh the cost of higher-interest financing against the combined losses from stockouts - like missed revenue, reduced rankings, expedited shipping fees, and lower customer retention - the financing costs often pale in comparison.

"The brands that scale fastest are not always the ones with the best products. They're the ones with the most liquidity at the right moment." - Matthew Shearer, SVP, Channel Sales, eCapital [9]

Modern inventory financing solutions can provide 50% to 80% of your inventory’s value, often with same-day approvals [8]. This speed allows sellers to restock quickly, minimizing the damage and gaining a competitive edge.

Example: Using Onramp Funds to Restock Within 24 Hours

Here’s a real-world example of how fast funding can save the day. Nick James, CEO of Rockless Table, encountered a surge in demand and needed immediate capital to restock inventory. "We applied, received our offer, and had cash within 24 hours. Their Austin, TX based team helped me deploy the cash to effectively grow our business", he shared [10].

This rapid turnaround was possible thanks to Onramp's streamlined process. Sellers can get a qualification estimate in just one minute and connect their store in five minutes [10]. For businesses generating at least $10,000 in average monthly sales, funds are typically available within 24 hours of final approval [10]. With this kind of speed, sellers can place supplier orders right away, protect their marketplace rankings, and capture sales that might otherwise go to competitors. Plus, Onramp’s revenue-based repayment model ensures that payments adjust with sales, offering flexibility during slower periods [10].

Scenario 2: Acting Fast on Time-Limited Growth Opportunities

Seasonal promotions, viral trends, and new platform launches often require quick access to funding. Take rhode, the beauty brand founded by Hailey Bieber, as an example. In 2025, rhode expanded from direct-to-consumer sales to retail shelves in Sephora stores across North America and the UK - a bold move designed for rapid growth. By May 2025, e.l.f. Beauty acquired rhode for $1 billion after the brand achieved $212 million in net sales over the prior year [1]. This kind of strategic expansion needed immediate capital to scale inventory, ramp up marketing, and streamline logistics. Any delays in securing funding could have meant missing out on pivotal growth moments, translating directly into lost revenue.

Revenue Lost from Delayed Seasonal Campaigns or Platform Launches

Missing a key shopping season or failing to capitalize on a trending platform like TikTok Shop can be more costly than the financing fees required to act quickly. For example, e-commerce sales climbed 5.3% year-over-year in Q2 2025, outpacing the 3.9% growth in overall retail sales [1]. Sellers unable to fund inventory or marketing during these peak periods risk losing market share to competitors who are better prepared. In these cases, delays in financing can mean lost opportunities that may not come around again.

"Even in a tough market, deals are still happening. Buyers are just choosier, focusing in on brands with proven retention, healthy unit economics, defensible supply chains, and strong margins."

- Lisa Tolliver, Managing Director, Capstone Partners [1]

How Revenue-Based Repayment Supports Growth Investments

To navigate these challenges, revenue-based repayment structures provide flexibility, especially during unpredictable sales periods. Unlike fixed payment loans, revenue-based financing adjusts to your sales performance. For instance, when launching on a new platform or running a seasonal campaign, sales can be volatile. Onramp’s repayment model ties payments directly to sales deposits, meaning if demand dips or campaigns underperform, payment amounts decrease automatically [10]. This setup allows businesses to pursue aggressive growth strategies without the fear of rigid monthly payments draining cash flow during slower periods.

For companies venturing into omnichannel strategies - blending online marketplaces with retail partnerships - this dynamic repayment approach ensures costs are tied directly to the revenue generated by these investments [1]. Whether it’s restocking inventory quickly or jumping on a fleeting growth opportunity, having access to flexible funding can make higher-cost capital a worthwhile investment.

Scenario 3: Covering Unexpected Expenses and Payment Delays

Running an eCommerce business comes with its share of surprises - some of them expensive. Whether it’s a sudden payment hold, an unexpected supplier demand, a spike in shipping costs, or equipment breaking down, these challenges can grind operations to a halt if cash isn’t available immediately. Waiting for traditional bank loans, which often involve lengthy approval processes, isn’t an option when suppliers are threatening to stop shipments or platforms are delaying payouts. Quick access to funds becomes critical to avoid disruptions and maintain customer trust.

Avoiding Business Disruptions During Cash Shortages

Onramp offers a lifeline by providing capital within 24 hours[10], enabling sellers to address urgent expenses without delay. What makes it stand out is its revenue-synced repayment system. Payments automatically adjust based on sales deposits, so if a platform delay or an unexpected cost reduces cash flow, repayment amounts decrease as well. This flexibility takes the pressure off during tough times.

Torrie V., the Founder and Owner of Torrie's Natural, shares her experience:

"Onramp has simplified cash flow by automating everything: easy to request, set it and forget it payments - quick and fast!"

For businesses with ongoing or recurring needs, Onramp’s Rolling Cash Line provides a revolving borrowing option. Sellers can access funds as often as every two weeks without having to reapply, making it a seamless way to manage both planned and surprise expenses.

Example: Using Onramp Funds to Bridge a Cash Flow Gap

Fast capital can make all the difference when payment delays or upfront inventory costs create a temporary cash shortage. Ashunta, an Onramp user, highlights how it helped her:

"Onramp has been the bridge when it came to quick capital for additional inventory..."

Adam B. from The Full Spectrum Company emphasizes the speed of the process:

"Onramp's process is very straightforward and easy to navigate. I had funds in my account within a day of final approval."

This rapid access to funds helps sellers maintain strong supplier relationships, avoid penalties for late payments, and keep inventory levels steady during payout delays. With over 3,000 eCommerce loans issued and approvals based on real-time sales data - not personal credit checks - Onramp ensures sellers can secure what they need without the typical delays of traditional banking[10]. It’s a practical solution for staying operational and maintaining stability, even in the face of unexpected challenges.

Calculating the Return on Higher-Cost Capital

Higher-cost capital only makes sense when the benefits - like increased revenue or avoided costs - outweigh the fees. While the fees might seem steep at first, they can be completely justified if they prevent stockouts, ensure timely product launches, or maintain strong supplier relationships. The key is to crunch the numbers ahead of time. This kind of analysis ties back to the earlier point about the importance of timing when it comes to using capital.

Comparing Funding Fees to Revenue Gains

Let’s build on some earlier examples to illustrate this. Say you’re facing a potential stockout that could cost $50,000 in Q4 sales, but the inventory needed to avoid it costs just $3,000. The fee to secure that inventory becomes an easy decision. Or consider a marketing campaign: a $20,000 ad spend during a peak sales period generates $60,000 in revenue. With a 40% profit margin, that’s $24,000 in profit. Even if you pay a 6% fee on the capital (about $1,200), you’re still left with $22,800 in profit. These scenarios highlight why comparing funding fees to potential revenue gains is so important before making a decision.

Onramp makes this process simpler with its transparent fee model. Unlike other funding options, it avoids hidden costs and compounding interest, giving you a clear view of the fees upfront. This clarity allows you to directly compare the costs to your expected profit margins. One user shared their experience:

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales." [10]

Using Onramp Funds' Calculator to Estimate Costs

Onramp’s funding calculator is a handy tool that removes the guesswork from financial planning. By entering your average monthly revenue (minimum $10,000), you can see your funding limit and repayment percentage. For example, you can model a $30,000 inventory purchase over terms ranging from 1 to 6 months to understand fee structures and repayment options.

The calculator also offers flexibility. You can choose between revenue-based repayment - where payments adjust based on your sales - or fixed repayment structures for more predictable cash flow management. Since Onramp bases approvals on real-time sales data instead of personal credit checks, and funds can be deposited in under 24 hours, you can act quickly when opportunities arise. With over 3,000 eCommerce loans issued and an A+ rating from the Better Business Bureau, Onramp Funds is built to help sellers make smart, timely decisions with their capital [10].

Conclusion

From restocking inventory quickly to capitalizing on seasonal opportunities or handling unexpected expenses, accessing higher-cost capital can be a game-changer for growth. Opting for this type of funding isn’t just about covering immediate needs - it’s about staying ahead and avoiding stagnation. When critical holiday sales are at risk due to inventory shortages, or a seasonal campaign has the potential to generate substantial revenue, waiting weeks for traditional bank approval could seriously set your business back. As Chris from Venn VC puts it:

"The quantum and availability of capital provided at pace is everything" [6].

If your margins can handle the cost and the funding leads to a 15% revenue boost, the fee essentially pays for itself through the opportunities it enables. The bigger risk isn’t the financing fee - it’s the cost of missed chances. Missing out on seasonal sales, losing supplier discounts, or delaying your market entry while competitors move forward can have far greater consequences than the price of quick funding. This is the key reason why having fast access to capital is so important.

In today’s competitive landscape, the businesses that grow are the ones that can move quickly when opportunities arise. A small difference in capital costs - say, 2–3% - is negligible compared to the advantage of turning over inventory in 60 days or making the most of time-sensitive opportunities [6].

Onramp Funds simplifies this decision with clear fees and a revenue-based repayment structure that aligns with your sales. Whether you’re replenishing stock, launching a seasonal campaign, or addressing a cash flow gap, their funding calculator helps you see exactly what you’ll pay so you can make an informed choice based on your potential returns.

Don’t let slow processes and rigid terms hold you back. With Onramp Funds’ flexible options, you can put capital to work when it matters most.

FAQs

How do I know if higher-cost funding is worth it for my business?

Higher-cost funding can make sense when it opens doors to strategic growth opportunities, such as quickly restocking inventory, adding new products to your lineup, or seizing a time-sensitive chance in the market. The key is to weigh the potential revenue boost against the funding costs. If the expected returns not only cover the expenses but also fuel business growth, it could be a worthwhile decision. On the flip side, if your cash flow is already stretched thin or the growth potential is uncertain, the risks might outweigh any potential benefits.

What numbers should I calculate before using fast capital?

Before tapping into fast capital, take the time to map out your projected sales, cash flow requirements, and the timing of your sales deposits. This step is crucial to ensure that repayment schedules sync up with your sales cycle, helping to maintain your business’s financial health. Thoughtful planning allows you to use higher-cost funding effectively while steering clear of avoidable risks.

How does revenue-based repayment change my risk during slow months?

Revenue-based repayment helps ease financial pressure during slow months by linking your payments to a percentage of your sales. This setup ensures you only make payments when you generate revenue, allowing you to maintain cash flow and better manage finances during times of reduced income.