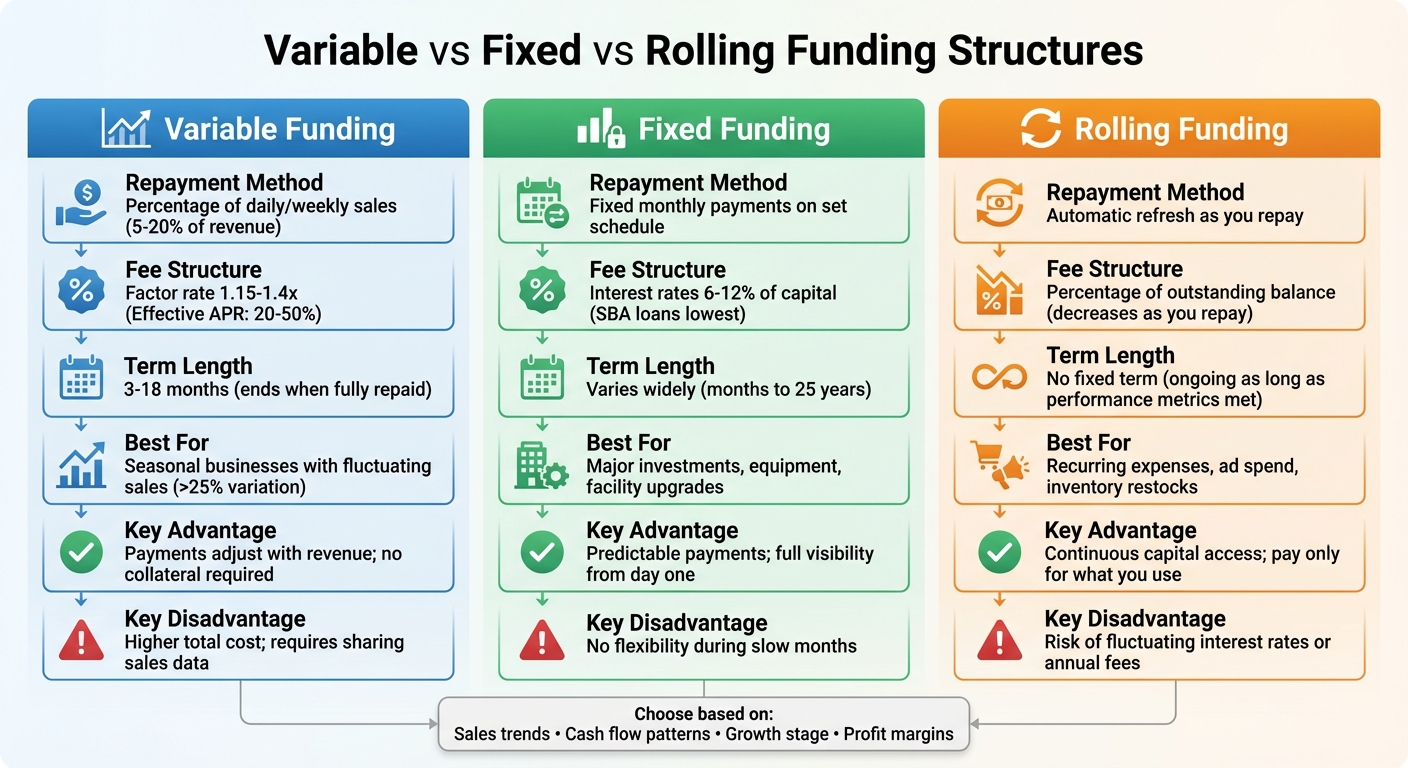

When it comes to funding your eCommerce business, the structure you choose can impact cash flow, repayment flexibility, and growth opportunities. Here's a quick breakdown of the three main funding types:

- Variable Funding: Payments are tied to a percentage of your sales, offering flexibility during slow or peak months. However, it often comes with higher overall costs.

- Fixed Funding: Provides a lump sum with predictable monthly payments, making it ideal for long-term investments. But it lacks flexibility during low-revenue periods.

- Rolling Funding: Acts as a revolving credit line, refreshing as you repay. It's great for covering recurring expenses but may involve fluctuating fees or interest rates.

Quick Comparison

| Funding Type | Best For | Key Advantage | Key Disadvantage |

|---|---|---|---|

| Variable | Seasonal businesses | Payments adjust with revenue | Higher total cost |

| Fixed | Major investments | Predictable payments | No flexibility during slow months |

| Rolling | Recurring expenses | Continuous access to capital | Risk of variable costs |

To choose the right structure, consider your sales trends, cash flow, and growth plans. Variable funding works well for fluctuating sales, fixed funding suits stable businesses with large investments, and rolling funding supports ongoing needs like ads or inventory restocks.

Comparison of Variable, Fixed, and Rolling Funding Structures for eCommerce

1. Variable Funding Structure

Repayment Method

With variable funding, your repayment adjusts based on your daily or weekly sales performance. Instead of a fixed monthly payment, you pay a percentage of your revenue. For example, if your business generates $50,000 in a month and the repayment rate is 10%, you’d pay $5,000. If sales drop to $25,000, your payment would adjust to $2,500. This percentage-based approach - typically between 5% and 20% of credit card receipts or bank deposits - offers flexibility. During slower periods, payments decrease, and during strong sales periods, repayment speeds up. Let’s now look at how fees impact the overall cost of repayment.

Fee Structure

Fees are calculated using a factor rate, generally ranging from 1.15 to 1.4 times the amount funded. For instance, if you receive $50,000 with a 1.3 factor rate, your total repayment would be $65,000, regardless of how quickly or slowly you pay it off. This setup results in effective APRs between 20% and 50%. One advantage here is the absence of prepayment penalties, meaning you can pay off the balance faster during high-revenue months without incurring additional costs.

Term Length

Variable funding doesn’t come with a fixed repayment deadline. The term ends once the total amount (advance plus fees) is repaid. Terms typically range from 3 to 18 months, depending on your revenue. For example, a retailer receiving a $200,000 advance might repay it in just 4 months during a peak season with $500,000 in monthly sales. However, during slower periods, repayment could extend to 12 months - still without additional fees. This flexible structure makes it appealing for businesses with uneven revenue patterns.

Ideal Use Cases

Variable funding works best for businesses with fluctuating sales cycles, as repayment scales alongside seasonal demand. It’s particularly useful if your gross margins exceed 30% and your monthly revenue varies by more than 25%. This structure can help you manage cash flow during slower periods while enabling strategic investments, such as stocking up for high-demand seasons, preparing holiday inventory, or launching marketing campaigns. Studies have shown that this approach can lower default rates by 20%–30% [6].

sbb-itb-d7b5115

2. Fixed Funding Structure

Repayment Method

Fixed funding operates on a straightforward repayment system with fixed monthly payments based on a set amortization schedule [8]. Both bank loans and SBA loans follow this structure, covering principal and interest together. This setup makes budgeting easier since payments are predictable. However, it lacks flexibility during slower sales periods, which can be a challenge for businesses with fluctuating revenues [1]. Now, let’s take a closer look at how fees are structured in fixed funding.

Fee Structure

The cost of fixed funding is primarily determined by interest rates [4]. SBA loans often have the lowest rates for small businesses due to government backing [4]. In revenue-based fixed structures, repayment involves a fixed percentage of turnover - usually between 1% and 3% - until a set total amount is paid back. Fees in these structures typically fall between 6% and 12% of the borrowed capital [7][4]. Business credit cards, on the other hand, can provide up to 51 days of interest-free capital if the balance is paid in full. If not, annual interest rates can climb above 20% [10]. Next, let’s explore the term lengths associated with fixed funding.

Term Length

The length of fixed funding loans varies widely depending on the type. Short-term working capital loans might last only a few months, while SBA loans can extend up to 25 years [4]. Revenue-based fixed structures generally have terms of up to 5 years [7], and traditional bank loans usually range from 1 to 25 years [9][4]. It’s important to align the loan term with your project’s return on investment (ROI). For example, if a project generates returns within nine months, opting for a three-year loan could result in unnecessary costs [8].

Ideal Use Cases

Fixed funding is best suited for long-term investments, such as purchasing equipment, upgrading facilities, expanding internationally, or acquiring other businesses [8][10]. It’s most effective for businesses with steady monthly revenue that can comfortably handle fixed payments, even during slower periods. However, it’s less ideal for startups burning through cash quickly or businesses with significant seasonal revenue swings [1]. Eligibility typically depends on traditional factors like personal credit scores and multi-year tax returns, rather than real-time performance metrics like those used in eCommerce [1].

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital" [4] - Paul Voge, Co-founder and CEO of Aura Bora

3. Rolling Funding Structure

Repayment Method

Rolling funding provides a continuous flow of capital, automatically refreshing your available credit as you make repayments. This eliminates the hassle of reapplying for funds. Unlike traditional loans, which provide a one-time payout based on past performance, rolling funding adjusts dynamically to your repayment activity. Many models also offer flexibility, such as reduced payments during slower periods or the option to pay off early without penalties.

Fee Structure

Fees are calculated as a percentage of the outstanding balance and decrease as you repay. Since there are usually no penalties for early repayment, you can clear your balance when cash flow allows, giving you greater control over your finances.

Term Length

One standout feature of rolling funding is the absence of a fixed term. As long as you meet your performance metrics and keep up with regular payments, the funding remains available. This ensures consistent liquidity without the need for repeated applications, making it an excellent option for businesses with evolving needs.

Ideal Use Cases

Rolling funding shines when you need quick access to capital to seize growth opportunities. It’s particularly useful for managing fluctuations in eCommerce demand, like viral product surges, seasonal trends, or fluctuating advertising costs. For instance, it can help scale successful ad campaigns, replenish inventory during unexpected sales spikes, or act on market opportunities without delay. Clearco, for example, reported a 46% year-over-year increase in deployed capital through this model [11].

"Founders tell us they're tired of marketing campaigns lagging while waiting for new funding approvals. They need uninterrupted capital flow that matches their growth rhythm, not one that forces them to pause high-performing ads or get stuck in reapplication gaps." - Jill Renwick, Clearco

Need Cash for your Shopify Store? Try This!

Comparing the Advantages and Disadvantages

For eCommerce sellers, funding options come with their own sets of trade-offs. These differences can impact your cash flow, predictability, and overall costs. Knowing how each structure works can help you pick the right one for your business.

Here’s a quick rundown of the benefits and challenges associated with each funding option:

Variable funding, such as revenue-based financing, adjusts payments based on your sales. If your revenue dips, your payments drop too, making it a great option for seasonal businesses. On the flip side, this flexibility often comes at a higher overall cost. Plus, you’ll need to share real-time sales data with lenders, which might not appeal to everyone.

Fixed funding offers stability and predictability. With set monthly payments, budgeting becomes easier, and you’re protected from interest rate changes. However, this structure can create pressure during slower months, as payments remain the same regardless of your revenue.

Rolling funding provides a flexible, revolving pool of capital. As you repay, funds become available again, and you only pay for what you use. Many rolling options even allow early repayment without penalties. The downside? There’s a risk of fluctuating interest rates or added annual fees, which can increase your costs over time.

Here’s a table to summarize the key points:

| Funding Structure | Best For | Key Advantage | Key Disadvantage |

|---|---|---|---|

| Variable (RBF/MCA) | High-growth, fluctuating sales | Payments scale with revenue; no collateral [4] | Higher total cost; requires sharing sales data [4] |

| Fixed (Term Loans) | Major launches, seasonal pushes | Predictable terms; full visibility from day one [2] | Fixed payments don't adjust for slow periods [4] |

| Rolling (Line of Credit) | Continuous ad spend, recurring restocks | Automatically replenishes available capital; pay only for what is used [2][4] | Risk of fluctuating interest rates or accumulating annual fees [4] |

Selecting the Best Funding Structure for Your Business

Finding the right funding structure starts with understanding how your cash flow behaves. If your revenue tends to fluctuate - like experiencing a big boost during Q4 holiday sales followed by slower months - variable funding might be your best bet. With this option, repayments adjust based on sales, helping you avoid cash flow issues. On the other hand, if you're gearing up for a product launch or need to stock up on inventory for a major event, fixed funding gives you the predictability you need to budget effectively [2]. This understanding of cash flow not only helps with variable funding decisions but also in choosing between fixed and rolling options.

Your business's growth stage also plays a big role. If you're just starting out and your sales are unpredictable, a more flexible funding structure could be ideal. For businesses further along and planning major expansions, the stability of fixed funding is a better fit. Meanwhile, if your marketing strategy involves continuous ad spending, rolling funding offers a steady flow of capital that replenishes as you make repayments [2].

Another important consideration is your unit economics. Businesses with tight profit margins may find the higher costs of variable funding challenging - especially since some merchant cash advances can exceed 50% APR [5][4]. If your LTV-to-CAC ratio (Lifetime Value to Customer Acquisition Cost) is below 3, the expense might outweigh the benefits [3].

Onramp Funds takes a modern approach by using real-time sales data from platforms like Amazon, Shopify, Walmart, and TikTok Shop instead of relying solely on credit scores [5]. This method can unlock credit limits that are 10 to 20 times higher than traditional business credit cards [4]. Plus, funding is often available within 24 hours, with repayments tied to a percentage of your sales.

To make the most of your funding, it’s smart to plan for a 10% to 20% buffer to cover unexpected costs or market changes [3]. Also, when comparing funding options, don’t just focus on the headline rate. Be sure to account for origination fees, platform charges, and revenue share percentages to get a clear picture of the true APR [5][4]. This thorough approach will help you optimize your cash flow and capital efficiency.

Conclusion

Choosing the right funding structure depends on how your business operates and its financial rhythm. Variable funding adjusts repayment amounts based on your sales, making it a good fit for businesses with fluctuating revenue between slow and busy periods. Fixed funding offers a predictable lump sum with set repayment terms, making it ideal for significant investments like inventory purchases or product launches. Meanwhile, rolling funding functions like a revolving credit line, replenishing as you make repayments - perfect for covering ongoing expenses such as advertising.

The best option aligns with your cash flow, profit margins, and growth stage. For instance, a business with tight margins might find variable funding challenging, especially when the effective APR can exceed 50% [5]. On the other hand, high-margin, rapidly scaling businesses often benefit from the flexibility of revenue-based financing. Fixed funding works well for large, one-time investments, while rolling funding ensures consistent capital for recurring costs. The key is to select the model that complements your business’s operational needs.

As your business grows, your funding needs may change. Many eCommerce sellers start with one structure - such as fixed funding for a seasonal inventory boost - and later transition to rolling funding to support ongoing efforts like customer acquisition as operations stabilize. Flexibility in adapting your funding strategy can make a significant difference in sustaining growth.

FAQs

How do I estimate the true APR for variable funding?

To get a clearer picture of the actual APR for variable funding, remember that the interest rate can shift based on market conditions. It's important to assess how these potential rate changes might impact your loan repayments over time. By doing this, you can estimate the effective APR and understand possible costs more accurately. Some lenders provide tools that take into account factors like the starting rate, rate caps, and general market trends to help you make these calculations.

Which funding type is safest if my sales are seasonal?

For seasonal eCommerce businesses, flexible funding options like revenue-based financing or purchase order financing can be a smart choice. With revenue-based financing, repayments are tied to your sales, which means you’ll pay less when business slows down - helping to ease cash flow pressure. On the other hand, purchase order financing is great for covering inventory costs during those high-demand peak seasons.

Fixed repayment loans, however, can be tough to manage during slower months, as they require consistent payments regardless of your revenue. That’s why flexible options are often a better fit for handling the ups and downs of seasonal business.

Can I switch funding structures as my business grows?

Yes, businesses can adjust their funding structures as they grow and their needs change. It’s actually quite common to transition to a different financing option over time. For instance, a business might begin with short-term funding like Merchant Cash Advances (MCAs) but later shift to options like rolling cash lines or fixed repayment loans. This approach helps ensure that funding keeps pace with evolving cash flow requirements, inventory levels, or seasonal fluctuations.