Buy Now, Pay Later (BNPL) platforms are changing the game for eCommerce businesses. They help sellers increase sales, boost average order values, and reduce cart abandonment by offering customers flexible payment options. Sellers get paid upfront, while BNPL providers handle the risks of credit and fraud. Popular platforms like Klarna, Affirm, Afterpay, and PayPal Pay in 4 cater to different needs, from small purchases to high-ticket items. Here's what you need to know:

- Klarna: Ideal for global businesses, offering multiple payment plans and integration with major platforms like Shopify.

- Affirm: Best for big-ticket items with transparent fees and no late charges.

- Afterpay: Great for younger shoppers with simple "Pay in 4" plans.

- PayPal Pay in 4: Seamless for existing PayPal users, offering interest-free installments.

- Shop Pay Installments: Built for Shopify sellers, increasing order values and reducing cart abandonment.

- Sezzle: Helps customers build credit while offering flexible payment options.

- Zip: Focused on mobile-first experiences with a straightforward "Pay in 4" model.

For sellers, choosing the right BNPL platform depends on factors like fees, customer demographics, and integration with your eCommerce platform. Additionally, tools like Onramp Funds can provide financing to support inventory and marketing, ensuring steady growth alongside BNPL adoption.

Best Buy Now Pay Later (BNPL) Solutions for your Business | Affirm, Afterpay and Klarna

sbb-itb-d7b5115

Benefits of BNPL Platforms for eCommerce Sellers

BNPL platforms are transforming eCommerce by boosting cash flow, increasing order values, and improving customer satisfaction. Let’s break down how these benefits can elevate your eCommerce game.

Better Cash Flow Management

One of the biggest perks of BNPL platforms is that you get paid upfront - typically within 1–3 business days - while the BNPL provider handles the rest. They take on the risks of defaults and disputes, so you don't have to worry about chasing payments or losing revenue [3][9]. This setup not only protects your margins but also makes it easier for shoppers to afford higher-priced items, especially those watching their budgets [9].

Higher Average Order Value

BNPL doesn’t just make purchases more accessible; it encourages customers to spend more. For example, Affirm merchants have seen cart sizes grow by over 70%, while Shop Pay Installments boosts order values by as much as 50%. Similarly, retailers using Afterpay and Klarna report increases of around 40% [3][9].

Here’s how it works: splitting a $400 item into four $100 payments feels much less intimidating for customers. This often leads to add-ons or upgrades, whether it’s a $128 fashion piece or a $386 luxury item [10]. On average, customers spend 6% to 6.4% more when using BNPL, and a notable 40% of BNPL sales come from first-time buyers [6]. That means not only are you increasing individual order values, but you’re also bringing in new customers.

Better Customer Experience

Today’s shoppers expect flexibility at checkout. In fact, 56% of them want multiple payment options [9]. BNPL is particularly appealing to younger demographics: 73% of Afterpay’s 20 million users are Gen Z or Millennials, groups that increasingly steer clear of traditional credit cards [9].

"You'll sell more products if customers can make flexible, interest-free payments instead of paying all at once." - Vanessa Petersen, WooCommerce [9]

The numbers back this up. Afterpay retailers see cart conversions rise by 22%, Klarna partners enjoy 20% higher checkout conversion rates, and repeat purchases grow by an impressive 46% [9]. When customers find payment options that suit them, they’re more likely to complete their purchase - and come back for more.

Top BNPL Platforms for eCommerce Sellers

These platforms not only improve cash flow and boost order values but also offer distinct features tailored to various business needs. Here's a closer look at some of the leading options that can help eCommerce businesses grow.

Klarna

Klarna is a leader in the BNPL space, serving 790,000 merchants and over 150 million users across 45+ countries [7]. Its flexibility makes it a great fit for global eCommerce, offering options like "Pay in 4" for smaller purchases, "Pay in 30 days" for quicker payments, and financing plans extending up to 24 months [8].

One standout feature is the absence of a fixed spending limit [11]. Merchants using Klarna report a 23% increase in average order value [14]. It also ranked highest among pure BNPL providers in J.D. Power's 2025 BNPL Customer Satisfaction Study, scoring 638 out of 1,000 [11]. Klarna charges merchants around 3.29% plus $0.30 per transaction [12], while customers enjoy 0% interest on short-term plans or 7.99% to 33.99% APR for longer terms [11].

In March 2025, Klarna replaced Affirm as Walmart's official BNPL partner in the U.S., solidifying its position with major retailers [8]. It integrates seamlessly with platforms like Shopify, WooCommerce, BigCommerce, and Magento [12], and its shopping app offers features like price-drop alerts and rewards, further helping merchants increase cash flow and order values.

"Klarna is more versatile and better suited for businesses selling higher-priced items or operating in multiple countries." - Bogdan Rancea, Co-founder, Ecommerce-Platforms.com [12]

Affirm

Affirm is known for its upfront, transparent pricing - no late fees or hidden charges. As the primary BNPL partner for Amazon and Target, it supports purchases up to $17,500 [13]. With options like biweekly "Pay in 4" plans and monthly installments up to 60 months, it's a solid choice for big-ticket items like electronics, furniture, and home improvement products [8][11].

In 2024, Affirm saw 46% year-over-year revenue growth, reaching $2.32 billion, and now works with 377,000 businesses [7]. Customers pay 0% to 36% APR depending on their plan, with no late fees ever [8][11]. Investopedia rated Affirm 4.8 out of 5, calling it "Best Overall" for its fee-free structure and broad merchant network [11]. Despite its strengths, Affirm scored 607 out of 1,000 in J.D. Power's 2025 BNPL Customer Satisfaction Study - the lowest among major providers [11].

Afterpay

Afterpay, now integrated with Block's ecosystem as Cash App Afterpay, keeps things simple with its "Pay in 4" model spread over six weeks. It's particularly popular with younger shoppers. Purchases are capped at $600 to $5,000 depending on customer approval [8][11], and merchants pay 4% to 6% plus $0.30 per transaction [12][13]. Customers pay 0% interest on "Pay in 4" plans, while monthly installments may carry APRs up to 35.99% [8][11]. Late fees are capped at 25% of the purchase price or $68, whichever is less [8][11].

Integration is straightforward with Shopify, WooCommerce, BigCommerce, and Magento, and the platform assumes all fraud and credit risks, ensuring merchants are paid upfront [12]. Investopedia rated Afterpay 4.1 out of 5, highlighting its strong reputation and trust scores [11].

"Afterpay's one-size-fits-all approach is easy to understand... Ideal for fashion, beauty, and low-ticket DTC products." - Bogdan Rancea, Co-founder, Ecommerce-Platforms.com [12]

PayPal Pay in 4

For merchants already using PayPal, adding Pay in 4 is a seamless process. It integrates directly with PayPal accounts and connects to a global network of 30 million merchants [11]. The platform offers interest-free "Pay in 4" installments for purchases up to $1,500, as well as monthly financing options for larger amounts with APRs ranging from 9.99% to 35.99% [11].

In 2024, PayPal processed $33 billion in BNPL transactions, a 21% increase from the previous year [7]. Features like "Purchase Protection" reduce checkout friction and build trust [8][2]. Investopedia rated PayPal Pay in 4 at 4.3 out of 5, naming it "Best for Merchant Network" [11]. However, PayPal doesn't allow payment rescheduling, which may limit flexibility for some customers.

Shop Pay Installments

For Shopify merchants, Shop Pay Installments is a built-in solution powered by Affirm. It requires no third-party integrations and activates directly within Shopify admin settings [13][4]. Merchants using Shop Pay report a 50% increase in order value and 28% fewer abandoned carts [8][2][13][14].

"Shop Pay Installments gives online small businesses the same BNPL benefits enjoyed by major retailers, including a larger average order value and less cart abandonment." - Michael Keenan, Shopify [13]

The platform offers "Pay in 4" for smaller purchases with 0% interest and monthly installments up to 12 months with APRs ranging from 10% to 36% [13]. Refunds come without additional fees, and the smooth checkout process keeps customers within the Shopify ecosystem.

Sezzle

Sezzle stands out as a Public Benefit Corporation, offering a "Sezzle Up" program that helps customers build credit by reporting payment histories to credit bureaus [11]. It provides a standard "Pay in 4" model with 0% interest and monthly plans through its Bread partnership [11]. Customers can reschedule payments for a small fee (up to $7.50), adding flexibility. Merchants typically pay 6% plus $0.30 per transaction [13], while late fees are capped at $15 and failed payment fees at $5 [11].

Investopedia rated Sezzle 3.5 out of 5, naming it "Best for Flexibility" [11]. It scored 615 out of 1,000 in J.D. Power's 2025 study [11], making it a good choice for budget-conscious shoppers who also want to build credit.

Zip

Zip offers a straightforward "Pay in 4" model over six weeks, focusing on a mobile-first experience. Customers receive a virtual card that works across a wide range of merchants, making it highly accessible. Merchants typically pay 2% to 4% per transaction, and the platform's quick approval process helps maintain high conversion rates at checkout.

Onramp Funds: Financing for eCommerce Sellers

BNPL platforms are great for driving sales, but they don’t help with funding inventory or marketing efforts. That’s where Onramp Funds comes in. They offer fast, equity-free capital to help eCommerce businesses grow - whether it’s stocking up on inventory, scaling advertising, or handling increased demand.

Features of Onramp Funds

Onramp provides three funding options tailored to different business needs:

- Variable Advances: Payments adjust with sales, making it a good choice for businesses testing new products or managing unpredictable cash flow.

- Fixed Advances: Offers fixed, equal payments, ideal for businesses looking for stability in budgeting.

- Rolling Cash Lines: A revolving credit line that grows with your sales, letting established businesses pay fees only on the funds they use.

With approvals in as little as 24 hours, Onramp uses real-time sales data to make funding decisions - no personal credit checks or collateral required. Fees range from 2% to 8%, and repayment schedules (daily, weekly, or bi-weekly) align with sales cycles, reducing financial pressure during slower periods [15].

"Having the flexibility to draw funds as we need them has been a game changer for our growth. Andrew and his team's communication and customer service are always excellent - I know I have a true partner with Onramp."

- John Doe, CEO at Curriculum [15]

Onramp’s customers have reported impressive results, including 60% revenue growth. Additionally, 75% of borrowers return for additional funding, with offers reaching up to $2 million based on store performance [16][18].

eCommerce Platform Integration

Onramp integrates with major platforms like Amazon, Shopify, Walmart Marketplace, TikTok Shop, WooCommerce, BigCommerce, Squarespace, Shopline, and Stripe [15]. By connecting directly via a secure, read-only API, Onramp pulls sales data automatically - no manual uploads required.

To qualify, businesses must meet the following requirements:

- Be a legal U.S. entity (LLC, C-Corp, or S-Corp)

- Generate at least $10,000 in monthly sales on a supported platform [15]

Unlike financing tied to a single marketplace, Onramp supports multi-channel growth, providing a broader and more flexible funding solution. This approach considers your entire business, often resulting in larger funding offers [17].

Why Choose Onramp Funds

Onramp complements BNPL platforms by addressing the operational side of eCommerce growth. While BNPL helps customers afford purchases, Onramp ensures you have the capital to stock inventory, ramp up advertising on platforms like Google and TikTok, and avoid running out of stock during peak seasons [17]. Their revenue-based repayment model adjusts to your sales volume, protecting your cash flow during slower times and speeding up repayment when business is booming [15].

The platform is rated "Great" on Trustpilot, with 227 reviews highlighting its straightforward process, excellent communication, and the benefit of working with real people instead of automated systems [15].

"Onramp has been the bridge when it came to quick capital for additional inventory."

- Ashunta, Verified Customer [15]

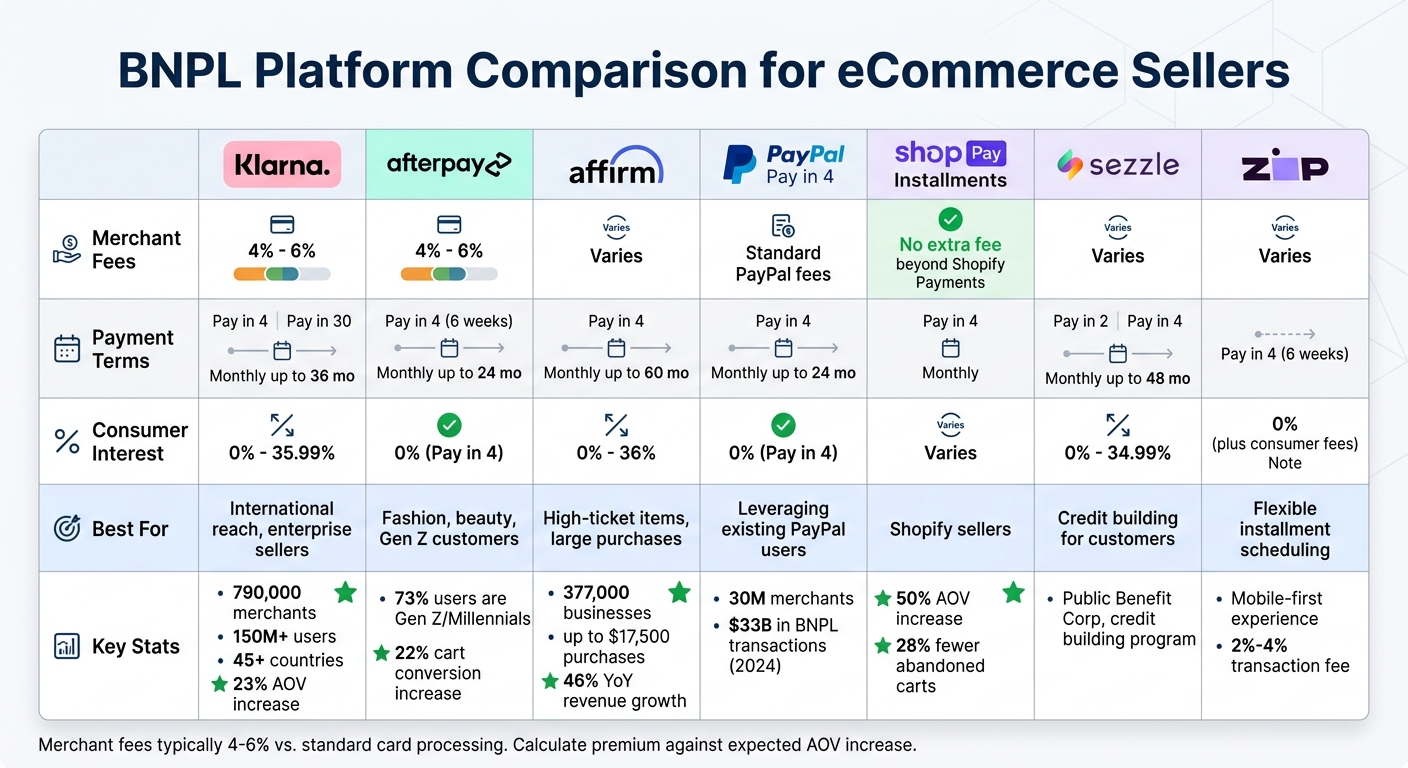

BNPL Platform Comparison

BNPL Platform Comparison: Fees, Terms, and Best Use Cases for eCommerce

When deciding on a Buy Now, Pay Later (BNPL) platform, it's critical to weigh the operational differences. While each platform brings unique perks to the table, understanding how merchant fees, payment terms, and integration options compare can help you make an informed decision.

Merchant fees for BNPL are higher than standard credit card processing, typically falling between 4% and 6% per transaction [19]. However, most BNPL platforms take on the risks of fraud and chargebacks, which can protect your business from potential losses [8].

Here’s a breakdown of key differences among the leading BNPL providers:

| Platform | Merchant Fees | Payment Terms | Consumer Interest | Best For |

|---|---|---|---|---|

| Klarna | 4% - 6% [19] | Pay in 4, Pay in 30, Monthly (up to 36 mo) | 0% - 35.99% [8] | International reach, enterprise sellers [21] |

| Afterpay | 4% - 6% [19] | Pay in 4 (6 weeks), Monthly (up to 24 mo) | 0% (Pay in 4) [8] | Fashion, beauty, Gen Z customers [12] |

| Affirm | Varies | Pay in 4, Monthly (up to 60 mo) | 0% - 36% [8] | High-ticket items, large purchases [9] |

| PayPal Pay in 4 | Standard PayPal fees | Pay in 4, Monthly (up to 24 mo) | 0% (Pay in 4) [8] | Leveraging existing PayPal users |

| Shop Pay Installments | No extra fee beyond Shopify Payments | Pay in 4, Monthly | Varies | Shopify sellers [21] |

| Sezzle | Varies | Pay in 2, Pay in 4, Monthly (up to 48 mo) | 0% - 34.99% [8] | Credit building for customers [22] |

| Zip | Varies | Pay in 4 (6 weeks) | 0% (plus consumer fees) [8] | Flexible installment scheduling [22] |

Integration options also vary widely. Klarna offers a robust SDK designed for headless commerce, making it ideal for more complex eCommerce setups. On the other hand, Afterpay’s SDK is less flexible [19]. Shopify users benefit from the seamless integration of Shop Pay Installments, while WooCommerce supports a range of BNPL plugins [20][9].

"The merchant fee for BNPL is materially higher than a standard card transaction. Klarna and Afterpay both charge in the 4 to 6 percent range per transaction." - Contra Collective [19]

Given the higher fees, it’s essential to calculate the premium against the expected boost in average order value (AOV). If the increased AOV from BNPL adoption outweighs the additional transaction fees, the platform can positively impact your net revenue [19]. For high-volume merchants, offering multiple BNPL options can help attract a broader customer base with minimal operational effort once the systems are in place [19].

This comparison provides a clear starting point for aligning a BNPL platform with your business objectives.

How to Choose the Right BNPL Platform

What to Consider

Start by ensuring the BNPL provider integrates smoothly with your eCommerce platform, whether it’s Shopify, WooCommerce, Magento, or BigCommerce [5].

Your average order value (AOV) plays a big role in deciding if BNPL is right for your business. It works best for AOVs between $100 and $500. For lower-value sales (under $30), fees ranging from 2% to 8% can eat into your margins. On the other hand, if you sell higher-priced items like furniture or electronics, look for platforms offering monthly financing options, sometimes stretching up to 60 months.

Geographic reach is another key factor. For example, Shop Pay Installments operates in the US, Canada, and the UK, while Klarna is available in 45 countries across Asia, Europe, and North America [8]. Picking a provider that matches your customers’ locations can directly impact sales.

Don’t overlook profit margins. If your margins are slim - around 3% to 5% - fees between 3% and 6% per transaction could be a challenge. Before committing, weigh the potential increase in AOV (which can jump by as much as 85%) against these costs [5, 46]. Some businesses offset these fees by slightly increasing product prices, often by about 5%.

"The best online payment processing service is not simply the one with the lowest transaction fee – it's the one that supports your business model today while leaving room for where you want to go next." - ConnectPay [23]

These technical and financial considerations will help you align your BNPL choice with your overall business strategy.

Matching BNPL to Your Business Goals

Beyond fees and integration, think about how the platform fits your growth plans. If your goal is to boost conversions and attract younger shoppers, look for providers that offer visible on-site financing options and appeal to millennials and Gen Z. In 2022, 26% of millennials and 11% of Gen Z used BNPL services [24]. For instance, Shop Pay Installments can reduce cart abandonment rates by up to 28% [2].

If customer acquisition is a priority, consider providers with large existing user bases. Shop Pay boasts over 200 million users, while PayPal connects with 426 million accounts [1]. These networks not only build trust but also help attract new customers.

Another perk of many BNPL platforms is their ability to reduce credit and fraud risks. They often pay you upfront and in full [5], which is particularly beneficial for businesses with thin margins or those in industries prone to chargebacks. For example, Sunbit offers a 90% approval rate, ensuring more customers can complete their purchases [7].

Once you’ve outlined your priorities, narrow your options by testing 2 to 4 platforms. From there, demo the top 1 or 2 that best fit your technical needs and business goals [24]. This hands-on evaluation will help you identify the platform that aligns with your growth strategy.

Conclusion

Buy Now, Pay Later (BNPL) platforms have become a game-changer for eCommerce businesses, with the market projected to hit $258.4 billion by 2031 [8]. These tools not only boost conversion rates but also enhance customers' purchasing power across a wide range of products.

However, sales growth alone isn’t enough to ensure lasting success. While BNPL can drive faster transactions, maintaining steady growth requires reliable working capital. That’s where Onramp Funds steps in. With its revenue-based financing tailored to your sales cycle, Onramp Funds provides the cash flow you need for essentials like inventory, advertising, and managing seasonal spikes [17]. It also supports multi-channel expansion across major eCommerce platforms, giving you the freedom to grow without being tied to a single marketplace [17]. By combining the power of BNPL platforms with Onramp Funds, eCommerce sellers can not only boost sales but also secure the liquidity needed for long-term growth.

FAQs

How do I know if BNPL will be profitable for my store?

To figure out if offering Buy Now, Pay Later (BNPL) makes sense for your business, start by looking at how your customers shop. BNPL can often lead to higher average order values and better conversion rates. But here’s the key question: Do the extra sales outweigh the fees charged by BNPL providers? And do those fees still leave room for healthy profit margins?

Another factor to consider is how BNPL providers structure their fees. Some use revenue-based repayment models, which adjust costs based on your sales. This can help lower financial risks during slower periods.

Keep a close eye on metrics like cash flow, sales volume, and overall profitability. These numbers will help you measure whether BNPL is actually helping your bottom line or just adding extra costs.

Should I offer Pay in 4 or longer monthly financing?

Choosing between Pay in 4 and longer monthly financing comes down to understanding your goals and what your customers prefer.

Pay in 4 divides a purchase into four interest-free payments over a few weeks. This can encourage more conversions and increase average order values, as it feels like a lighter commitment for buyers.

On the other hand, longer monthly financing spreads payments over several months. This option is ideal for higher-priced items, as it makes them feel more attainable. However, it may come with interest or additional fees.

To decide, consider your audience’s preferences and how either option fits with your cash flow strategy.

Can Onramp Funds help me buy more inventory after BNPL increases sales?

Onramp Funds offers fast, revenue-based financing designed to support your business after BNPL increases your sales. This type of financing allows you to purchase more inventory and manage cash flow effectively. Repayments are tied to a percentage of your sales, giving you the flexibility to grow without dealing with equity dilution or strict loan terms.