Revenue-based financing (RBF) is a flexible funding option for Amazon sellers. Instead of fixed monthly payments, you repay a percentage of your revenue, which adjusts based on sales. This makes it ideal for businesses with fluctuating income or seasonal trends. Here’s how to know if RBF is right for you:

- You earn at least $3,000 in monthly revenue: Consistent sales are key to qualifying for RBF. Lenders evaluate your Amazon sales history (3–6 months) for approval.

- You need fast inventory funding: RBF provides funds within 24–72 hours, helping you restock quickly and avoid stockouts that harm rankings and sales.

- Your store has a proven sales track record: A solid sales history (6–12 months) and positive account metrics (90%+ feedback, healthy ODR) improve approval chances.

- Your sales are seasonal: RBF repayments adjust to your revenue, easing cash flow during slow months and scaling during peak seasons like Black Friday or Prime Day.

- You want to grow without giving up equity: Unlike venture capital, RBF lets you retain full ownership while funding growth initiatives like inventory, marketing, or product expansion.

RBF offers a fast, equity-free alternative to loans, with approvals based on your Amazon performance, not credit scores. If your business meets these criteria, it could be a smart way to scale while keeping control of your operations.

How does Revenue Based Financing Work on Amazon | Abhiroop Medhekar

sbb-itb-d7b5115

Sign 1: You Generate Consistent Monthly Revenue

If your monthly revenue hits at least $3,000, you're already meeting the baseline many revenue-based financing (RBF) providers look for. Why? Because steady revenue signals reliable cash flow, which is crucial for qualifying for this type of funding [2][4].

Most RBF lenders will review your sales history over the past 3–6 months to gauge stability and decide how much funding to offer. Take Sisterly Drinkware, for example - they secured RBF funding by sharing their Amazon sales data. The repayment terms were tied to a percentage of their sales, which gave them flexibility to manage cash flow even during slow periods [2].

To speed up the approval process, consider integrating your Amazon Seller Central account with the lender's platform. This connection provides real-time insights like gross sales, order volumes, payout history, and monthly revenue trends. Lenders such as Onramp Funds use this data to verify your sales history quickly. In fact, approvals can happen in minutes, and funding might be in your account within 24 hours [5].

Before applying, double-check your Seller Central reports to confirm you've maintained at least $3,000 in monthly revenue over the last 3–6 months. A clean, steady sales record without significant dips not only boosts your chances of approval but could also qualify you for larger funding amounts [2]. Even if your personal credit history is limited, your sales performance can do the heavy lifting during the application process.

Sign 2: You Need Fast Inventory Funding

Running out of stock on Amazon can be a nightmare. It doesn’t just mean lost sales - it can also hurt your rankings and erode customer trust. If you’ve ever watched a hot product disappear from your inventory while waiting weeks for a traditional bank loan, you know how frustrating that wait can be. That’s where revenue-based financing comes in. It can provide capital in as little as 24 hours[2], giving you the chance to restock quickly and keep your listings performing well.

This kind of fast funding bridges the cash flow gap between paying for inventory upfront and waiting for sales revenue to roll in. Plus, repayments are designed to grow alongside your business, making it a more flexible option.

Here’s how it works: streamlined underwriting taps directly into your Seller Central data through APIs, allowing for approvals in minutes and funding within hours. Companies like Onramp Funds use this approach to help sellers secure funding almost instantly. Nick James, CEO of Rockless Table, shared his experience in 2024:

"Applied, got our offer, and had cash in our bank account within 24 hours" [6]

Another big advantage of revenue-based financing is its flexible repayment structure. Instead of dealing with fixed monthly payments - which can strain your cash flow during slower periods - you repay a percentage of your daily or weekly sales. If your sales dip, your payments shrink automatically. During busy seasons, payments scale up with your increased revenue. This adaptability helps you avoid the rigid cash flow challenges that come with traditional loans.

For Amazon sellers, getting funding in 24 to 72 hours can be the difference between capturing sales and losing market share. Whether it’s preparing for Prime Day or restocking a top-selling product, revenue-based financing ensures your inventory stays on track without the long delays.

Sign 3: Your Amazon Store Has a Proven Sales Track Record

If your Amazon store has a solid history of sales, it’s another indicator that you may be ready for revenue-based financing (RBF).

RBF providers usually look for sellers with consistent momentum. This means having 6 to 12 months of active selling under your belt, along with a clean and compliant account history. These factors help lenders evaluate your sales trends and the overall health of your account[3].

Your feedback rating plays a critical role, too. Many lenders require at least 90% positive feedback before approving an application[8]. Why? High ratings show that your business delivers quality products and great customer service, which reduces the risk for lenders. As Dillon Carter, Co-Founder of Aura, puts it:

"Lenders may assess your account health, sales volume, and feedback ratings to determine risk and rates." [8]

Beyond feedback, lenders also check operational metrics like your Order Defect Rate and Late Shipment Rate. These metrics show whether your account is in good standing and compliant with Amazon’s policies.

Monthly sales volume is another key factor. Most providers want to see at least $10,000 in revenue each month to ensure your business can handle percentage-based repayments. Unlike traditional loans that rely on credit scores and collateral, RBF focuses on your real-time sales performance and account health[7]. A proven sales track record, combined with these other factors, signals that your business might be a strong candidate for RBF.

Sign 4: Your Sales Change Seasonally

If your Amazon business experiences seasonal ups and downs, managing cash flow can get tricky. Revenue-based financing (RBF) offers a repayment structure that adjusts to your sales cycles, making it a flexible option for businesses with fluctuating income.

With RBF, repayments are tied to a fixed percentage of your gross sales [4]. This means that during your busy seasons, repayments increase, while in slower months, they decrease. As Matthew Tran, Chief Marketing Officer at AMZ Pathfinder, puts it:

"When sales are up, the company will pay back a larger amount on a dollar-for-dollar basis. When sales are down, repayment amounts will be lower." [10]

This setup helps you maintain cash flow during off-peak times, ensuring you have funds available for key expenses like storage fees, payroll, and utilities without the strain of fixed monthly payments [9]. It’s a practical way to keep your operations running smoothly, no matter the season.

During high-demand periods, RBF can be a game-changer. It allows you to place bulk inventory orders, which not only helps you prepare for events like Black Friday or Prime Day but can also lead to better unit costs and improved Buy Box eligibility [11]. With the quick approval process, you can secure inventory ahead of time and repay the funding naturally as sales pick up [9][11].

Platforms like Onramp Funds provide RBF solutions tailored to your business’s seasonal rhythm, helping you maintain healthy cash flow and capitalize on growth opportunities throughout the year.

Sign 5: You Want to Grow Without Giving Up Equity

One of the standout benefits of revenue-based financing (RBF) is that it allows you to scale your business while holding onto 100% of your equity. For many Amazon sellers, maintaining full ownership and control is non-negotiable, and RBF makes that possible by providing the capital you need without requiring you to hand over a piece of your business.

Unlike venture capital or equity financing, where investors often demand ownership stakes and decision-making power, RBF is entirely tied to your sales performance. There’s no need to worry about giving up board seats, sharing profits, or diluting the ownership you’ve worked so hard to build.

The approval process for RBF is refreshingly straightforward. Instead of relying on credit scores or personal assets, lenders evaluate your sales data directly from your Amazon account through API integration. This eliminates the need for collateral, so your personal assets - like your home or car - stay protected. For example, Ana Guzman, co-founder of Binibi, successfully used RBF to scale her inventory operations while keeping full ownership of her business.

RBF also offers a transparent fee structure. Typically, there’s a flat fee of 2–8%, with repayments set at 5–20% of your revenue. This ensures your costs are predictable and directly tied to your sales. Platforms like Onramp Funds make this process seamless, offering Amazon sellers quick, equity-free funding. With over 3,000 eCommerce loans already provided, these platforms can deliver funding - ranging from 1–2 times your monthly revenue - in less than 24 hours.

This model gives you the flexibility to reinvest in your business, whether that’s expanding your product offerings, boosting advertising efforts, or purchasing larger quantities of inventory. With RBF, you can fuel your growth while retaining full control of your business’s future. It’s a financing option built for sellers who value independence.

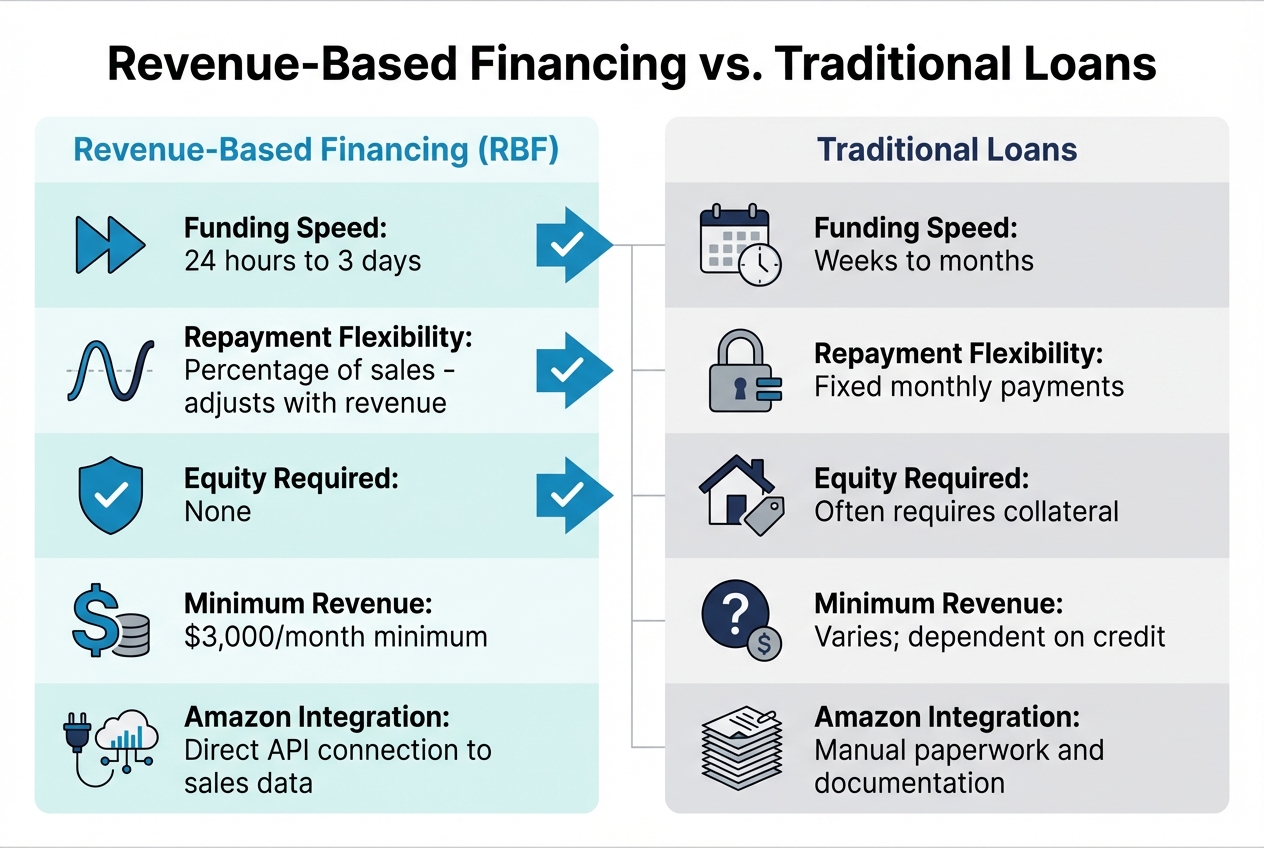

Revenue-Based Financing vs. Traditional Loans

Revenue-Based Financing vs Traditional Loans for Amazon Sellers

Choosing the right funding option for your Amazon business is crucial, especially when your sales cycles fluctuate. Revenue-based financing (RBF) and traditional bank loans are two distinct paths, each with its own approach to funding speed, repayment terms, and risk management. Understanding these differences can help you make an informed decision that aligns with your business needs.

Funding Speed

RBF providers are known for their quick turnaround. By connecting to your Amazon Seller Central account via API, they can access real-time sales data and approve funding in as little as 24 hours to 3 days. On the other hand, traditional bank loans often require weeks - or even months - due to lengthy documentation and credit review processes.

Repayment Flexibility

One of the standout features of RBF is its repayment structure. Instead of fixed monthly payments, you repay a percentage of your daily or weekly sales. This means payments adjust naturally - lower during slow periods and higher when sales increase. Traditional loans, however, stick to fixed monthly payments, which can create cash flow challenges during off-peak seasons.

Equity and Collateral Requirements

RBF doesn’t require you to give up equity or provide personal guarantees, allowing you to retain full ownership of your business while safeguarding personal assets. In contrast, traditional loans often demand collateral or personal guarantees, putting your assets at risk if repayment becomes an issue.

Comparison Table

| Factor | Revenue-Based Financing (RBF) | Traditional Loans |

|---|---|---|

| Funding Speed | 24 hours to 3 days | Weeks to months |

| Repayment Flexibility | Percentage of sales (adjusts with revenue) | Fixed monthly payments |

| Equity Required | None | Often requires collateral |

| Minimum Revenue | $3,000/month minimum | Varies; dependent on credit |

| Amazon Integration | Direct API connection to sales data | Manual paperwork and documentation |

For Amazon sellers looking to act quickly - whether it's restocking inventory for peak seasons or capitalizing on new trends - RBF offers a fast and flexible solution. Services like Onramp Funds simplify the process further by basing funding decisions on your sales performance, eliminating the red tape associated with traditional loans. These differences make RBF an attractive choice for sellers who need agility and speed in their funding options.

Is Revenue-Based Financing Right for Your Amazon Business?

If your Amazon business shows these five characteristics - consistent monthly revenue, urgent inventory needs, proven sales history, seasonal fluctuations, and a desire to retain equity - then revenue-based financing (RBF) could be the perfect fit for your needs. These traits suggest you might benefit from a funding model that prioritizes speed, flexibility, and growth potential, all without the limitations of traditional loans. Let’s dive into how these factors align with what RBF offers.

RBF adapts to your business's performance. For instance, if you're generating at least $3,000 per month in sales and need to quickly restock top-selling items ahead of Prime Day or the Q4 rush, RBF can provide fast funding based on your Amazon store data - not your personal credit score [5]. Repayments are tied to your daily sales, making the process dynamic and manageable.

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales." - Jeremy, Founder and Owner of Kindfolk Yoga [1]

This testimonial highlights how RBF can address the unique challenges of eCommerce sellers.

To determine if RBF is right for your business, review key performance metrics like a declining ACoS, an IPI score above 500, and profit margins between 15–30% [12][13]. These indicators not only reflect efficient management but also demonstrate your ability to use RBF funds strategically - for example, scaling ad campaigns or launching new products.

For sellers who prioritize flexibility and want to grow without giving up equity, RBF offers a financing model tailored to the fast-paced eCommerce world. Services like Onramp Funds integrate directly with your store, offering transparent flat-fee pricing (usually 2–8%) and delivering capital precisely when you need it - without the rigid terms of traditional lending options.

FAQs

How much funding can I get with revenue-based financing?

The amount of funding you can secure largely hinges on your business's monthly revenue and sales performance. Providers usually calculate funding as a percentage of your revenue, with many requiring steady monthly sales of $10,000 to $20,000 or more to qualify. The cash advances offered can vary widely - from a few thousand dollars to several hundred thousand - providing adaptable capital that can be used for inventory, marketing efforts, or operational expenses, all aligned with your revenue trajectory.

What Amazon metrics do lenders check besides revenue?

Lenders look at more than just revenue when evaluating the financial health of an Amazon seller. Key factors include account health metrics such as the order defect rate (ODR), late shipment rate, customer feedback, and whether the seller uses Fulfillment by Amazon (FBA) or Fulfillment by Merchant (FBM).

They also pay close attention to sales trends, ensuring monthly sales are consistent - usually around $10,000 or more. A solid operating history of 6 to 12 months is often preferred, along with gross margins of approximately 30% or higher. These metrics provide a clearer picture of the seller's reliability and overall stability.

Will repayments change if my sales drop or spike?

Revenue-based financing offers a repayment model that flexes with your sales performance. When sales dip, your repayments decrease, helping to ease cash flow pressures during slower times. On the flip side, when sales surge, repayments grow in step with your increased revenue. This approach ties your repayment obligations directly to your earnings, lightening the load during lean months and scaling naturally during periods of growth. Typically, payments are calculated as a percentage of your monthly revenue and continue until a set repayment cap is reached. This setup provides a level of flexibility that aligns seamlessly with the ups and downs of your business’s sales cycles.