Revenue-based financing (RBF) is a funding model where businesses receive upfront capital and repay it as a percentage of their revenue until a fixed amount is repaid. It’s a flexible option for businesses with consistent revenue, especially eCommerce sellers. Unlike loans, RBF doesn’t require collateral or personal guarantees, and repayment adjusts with your sales performance.

Key Takeaways:

- How It Works: Borrow funds and repay a percentage of revenue until a pre-agreed total is met (e.g., borrow $100,000, repay $150,000 at a 1.5× factor rate).

- Best For: eCommerce businesses with $3,000+ monthly revenue and 6–12 months of sales history.

- Advantages: Quick approval, no equity loss, payments tied to revenue, no personal guarantees.

- Challenges: Higher cost compared to traditional loans, limited to revenue-generating businesses, and capped funding amounts.

RBF is ideal for businesses needing short-term capital for revenue-driving activities like inventory purchases or marketing. However, it’s not suitable for pre-revenue startups or long-term investments. Always review repayment terms to ensure they align with your business margins and goals.

How Revenue-Based Financing Works

Application and Approval Process

Getting started with revenue-based financing is straightforward and skips the hassle of extensive paperwork. Simply connect your eCommerce platform - like Shopify, Amazon FBA, or WooCommerce - to the lender's system. You can also link tools like Xero for accounting or payment processors such as Stripe. These integrations allow lenders to access real-time sales data, which helps determine your eligibility and funding options [2].

The approval process is fast and automated, with many lenders providing cash offers in as little as two hours. Once approved, funds can land in your account within 24 hours [1] [2]. To apply, you'll need to share basic business information, such as your company name, address, phone number, Tax ID or EIN, and at least 6 to 12 months of revenue history. After approval, lenders often present multiple funding offers with varying repayment terms and revenue-share percentages [3].

Next, let’s explore how repayments adjust based on your sales.

Repayment Structure

Repayment with revenue-based financing works differently from traditional loans. Instead of fixed monthly installments, you repay a set percentage of your gross revenue - usually between 1% and 10% - on a monthly or even daily basis [1]. This means your payments fluctuate with your business performance. When sales are strong, you pay more and reduce your balance faster. On slower months, payments decrease, helping you maintain cash flow.

The total repayment amount is determined upfront by a factor rate, not by compounding interest. For instance, borrowing $100,000 at a factor rate of 1.5× means you’ll repay $150,000 total, no matter how long it takes [1]. There’s no collateral required, no personal guarantees, and no financial benefit to paying early since the repayment amount is fixed from the start.

Onramp Funds: RBF for eCommerce Sellers

Onramp Funds is a revenue-based financing platform tailored for small and medium-sized eCommerce businesses. It integrates seamlessly with popular eCommerce platforms like Amazon, Shopify, BigCommerce, WooCommerce, Squarespace, Walmart Marketplace, and TikTok Shop. You can receive a cash offer in as little as two hours, with funding available within 24 hours after approval [2].

Onramp Funds operates with a transparent fee structure - typically between 2% and 8% - and avoids hidden charges. Repayments are flexible, automatically adjusting based on your sales performance rather than sticking to fixed monthly amounts. Businesses with at least $3,000 in monthly sales are eligible, and the platform provides personalized support. Additionally, a funding calculator is available to help you estimate your financing options before you apply.

How to get Revenue-based Financing for your Shopify Store?

Benefits and Drawbacks of Revenue-Based Financing

Taking a closer look at the pros and cons of revenue-based financing (RBF) can help determine whether it's a good fit for your business, depending on where you are in your growth journey.

Benefits of RBF

One of the standout advantages of RBF is its payment flexibility. When sales slow down during off-peak months, your payments automatically adjust downward, helping to protect your cash flow during those tougher times.

Another big plus? You keep full ownership of your business. There’s no need to give up equity, hand over board seats, or deal with investor demands for an exit strategy. And when time is of the essence, RBF can be a lifesaver - funds are often available within 24 hours. This quick access can be crucial for seizing opportunities, like stocking up on inventory before a busy season or launching a timely marketing campaign.

RBF also doesn’t require personal guarantees. Instead, lenders focus on your revenue history rather than your credit score. The repayment cost is fixed upfront through a factor rate (usually between 1.1× and 1.9× the borrowed amount), so you won’t have to deal with the unpredictability of compounding interest.

But, as with anything, there’s a flip side. Let’s explore the challenges that come with RBF.

Drawbacks of RBF

The biggest downside to RBF? It’s not cheap. The built-in flexibility comes at a price, with factor rates climbing as high as 2.5× the principal amount - making it more expensive than traditional bank loans.

Another limitation is that RBF isn’t an option for everyone. To qualify, lenders typically require four to six months of consistent revenue, which rules out most pre-revenue startups. Additionally, the amount of capital you can secure is tied to your revenue - usually capped at about one-third of your annual revenue or 4–7 times your monthly revenue. This means you might not access as much funding as you could through equity financing.

There’s also the issue of limited state oversight. Without strong regulatory protections, it’s essential to carefully review contracts before signing. And while payments are tied to revenue, they continue until the full debt is repaid - even if external factors like supply chain issues or inflation create additional challenges.

Benefits vs. Drawbacks Comparison

Here’s a quick look at how the benefits and drawbacks stack up side by side:

| Benefits | Drawbacks |

|---|---|

| Retain full ownership: No equity dilution required. | Higher cost: More expensive than traditional loans. |

| Payment flexibility: Payments adjust with sales fluctuations. | Revenue requirements: Not an option for pre-revenue businesses. |

| Quick access to funds: Often available within 24 hours. | Fixed repayment: No benefit for early payoff. |

| No personal guarantees: Your assets are safe. | Limited funding: Capital is tied to current revenue. |

| Revenue-based repayments: Payments align with sales performance. | Contract risks: Requires careful review due to limited regulation. |

sbb-itb-d7b5115

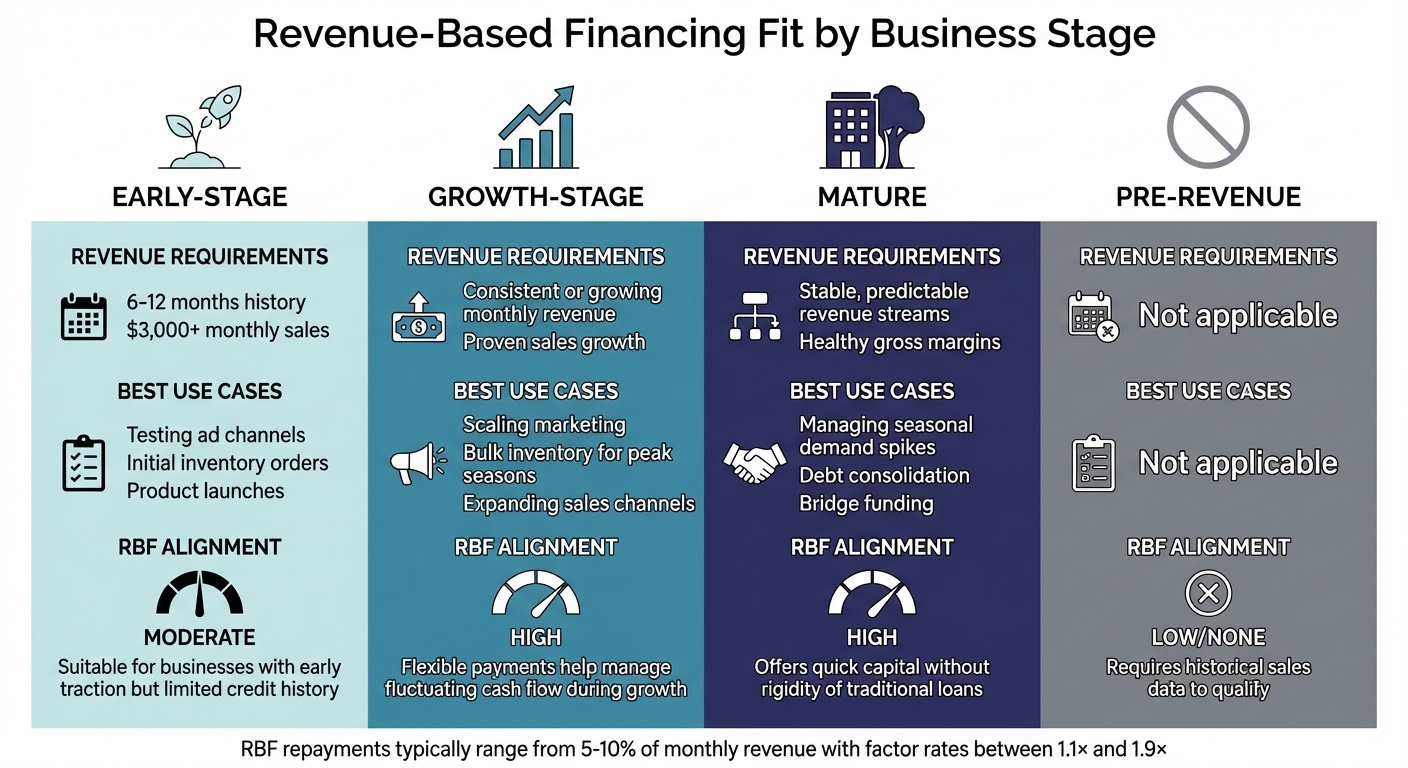

RBF for Different Business Stages

Revenue-Based Financing by Business Stage: Requirements and Use Cases

RBF for Early-Stage Businesses

If you're running a startup with at least six months of operations and generating $3,000 or more in monthly revenue, Revenue-Based Financing (RBF) can be a game-changer. This type of funding allows you to invest in inventory and marketing without giving up equity - meaning you retain full ownership and control during those critical early growth phases.

One major perk? Approvals are quick, often delivering funds as soon as the next business day. This speed can be crucial when you need to act fast on inventory opportunities or surging demand. Plus, repayments are tied to your gross revenue (usually 5% to 10%), so if sales slow down - whether due to seasonal dips or supply chain hiccups - your repayment adjusts accordingly.

Before applying, make sure you have a steady revenue history, typically six to 12 months. It’s also important to review the factor rate carefully. The repayment ceiling (commonly 1.3×–3× the original funding) should fit comfortably within your profit margins.

Next up: how RBF can fuel your business as it moves into the growth stage.

RBF for Growth-Stage Businesses

As your business scales, RBF can fund essential activities like marketing campaigns, inventory purchases, and supply chain improvements - all without the equity dilution that comes with venture capital. What makes RBF particularly appealing is its flexibility: payments are based on a percentage of your monthly revenue. This means your repayment amount increases when sales are strong and decreases during slower months.

For growth-stage companies, RBF works best when directed toward high-return activities like restocking inventory or launching marketing campaigns. These efforts directly generate the revenue needed to repay the funding. Additionally, RBF can help bridge cash flow gaps caused by staggered payments, making it easier to maintain momentum.

However, keep in mind that RBF typically comes with fixed factor rates, so there’s no financial benefit to paying off the balance early, even if your revenue grows faster than expected.

As your business matures, your funding needs may shift toward managing seasonal cycles and maintaining stability.

RBF for Mature Businesses

For established businesses, RBF offers a flexible way to handle seasonal demand spikes or quickly fill funding gaps. Unlike traditional loans, RBF doesn’t come with rigid repayment schedules or personal guarantees. Payments naturally adjust to your revenue - rising during busy months and shrinking during slower periods - helping you maintain steady cash flow.

Another advantage is that RBF usually doesn’t require collateral or personal guarantees, which means your personal assets stay protected. This makes it a great option for funding inventory or trying out new marketing strategies without taking on unnecessary risk.

That said, it’s crucial to assess the repayment duration. RBF is most effective for short-term projects where you can confidently predict the return on investment, such as revenue-generating campaigns or seasonal inventory needs.

How to Determine If RBF Fits Your Business

Questions to Ask Before Choosing RBF

Before diving into Revenue-Based Financing (RBF), make sure your business checks a few key boxes:

- Sales History: You’ll need 6–12 months of sales data, with monthly revenues between $3,000 and $7,500. Platforms like Shopify or Amazon can help you pull this data. If your business is pre-revenue or sees irregular sales, RBF likely isn’t an option - lenders rely heavily on consistent revenue to assess repayment ability.

- Gross Margins: Ensure your business can handle a 5%–10% repayment rate without disrupting operations. For instance, if your monthly revenue is $50,000 and the repayment rate is 10%, you’ll owe $5,000. This payment should leave enough cash to cover essentials like inventory, marketing, and overhead.

- Purpose of Funds: RBF works best for short-term, revenue-driving needs - think inventory restocks or targeted marketing campaigns. It’s not ideal for long-term investments or projects with delayed returns.

- Factor Rate: Understand the total cost of the loan. For example, borrowing $100,000 at a 1.5× factor rate means you’ll repay $150,000. Compare this cost to traditional loan APRs to determine if it aligns with your expected ROI.

Answering these questions will help you decide if RBF is the right funding approach for your current business needs.

Business Stage and RBF Fit

Here’s a quick overview of how RBF aligns with businesses at different stages:

| Business Stage | Revenue Requirements | Best Use Cases | RBF Alignment |

|---|---|---|---|

| Early-Stage | 6–12 months of revenue history; $3,000+ monthly sales | Testing ad channels, initial inventory orders, product launches | Moderate - suitable for businesses with early traction but limited credit history |

| Growth-Stage | Consistent or growing monthly revenue; proven sales growth | Scaling marketing, bulk inventory for peak seasons, expanding sales channels | High - flexible payments help manage fluctuating cash flow during growth |

| Mature | Stable, predictable revenue streams; healthy gross margins | Managing seasonal demand spikes, debt consolidation, bridge funding | High - offers quick capital without the rigidity of traditional loans |

| Pre-Revenue | Not applicable | Not applicable | Low/None - requires historical sales data to qualify |

This breakdown highlights how RBF can serve businesses differently depending on their stage, revenue, and financial goals.

Conclusion: Deciding on Revenue-Based Financing

Revenue-Based Financing (RBF) offers a flexible, equity-free way to access capital that aligns with your business’s actual performance. For eCommerce sellers, this means managing seasonal ups and downs while keeping full ownership intact. Unlike traditional loans with fixed monthly payments, RBF adjusts based on your revenue - lower payments during slow months and higher contributions when sales are strong.

The suitability of RBF often depends on where your business stands. If you’ve been operating for at least 6–12 months, generate monthly revenues above $3,000, and need funds for short-term, revenue-focused goals like restocking inventory or ramping up marketing, RBF could be a smart choice. Its growing popularity underscores how this model is helping businesses scale without giving up equity.

Onramp Funds specializes in RBF for eCommerce sellers, offering cash offers within hours and funding in just 24 hours. Repayments are tied to a percentage of your revenue, ensuring you never pay more than your business can handle.

Before you commit, take a close look at the total cost and repayment terms. Make sure these won’t interfere with essential expenses and that the returns from your investment outweigh the costs. Once you confirm the numbers work in your favor, the decision becomes much simpler.

If you’re looking for fast, adaptable funding to fuel growth, Onramp Funds delivers the capital you need - quickly and without the strings of traditional loans or equity loss. Apply today and secure funding that grows with your business.

FAQs

How does revenue-based financing compare to traditional loans in terms of cost and flexibility?

Revenue-based financing (RBF) works by charging a flat fee, usually between 2% and 8% of the funding amount, with repayment tied to a set multiple of the advance - often 1.5× the amount borrowed. While this setup offers a clear repayment structure, it can end up costing more annually compared to a traditional loan, which typically comes with lower interest rates for businesses with stable cash flow and fixed repayment terms.

One of the standout benefits of RBF is its flexible repayment model. Payments adjust based on your monthly revenue - higher when sales are strong and lower during slower months. Plus, RBF doesn’t require collateral or personal guarantees, making it a quicker and less restrictive option. On the other hand, traditional loans come with fixed monthly payments, often require collateral, and can take weeks to process. For businesses with unpredictable income, RBF can be a better fit, while those with steady cash flow might find traditional loans more cost-effective.

What kinds of businesses benefit most from revenue-based financing?

Revenue-based financing is a great option for eCommerce and subscription-based businesses with steady or seasonal revenue patterns. This funding approach provides the flexibility businesses need to address growth-focused priorities, such as buying inventory, running marketing campaigns, or expanding operations.

Since repayments are linked to your revenue, this model is particularly appealing to businesses aiming to secure funding without committing to fixed monthly payments. It’s a smart solution for managing cash flow that can ebb and flow over time.

What are the potential risks of revenue-based financing, and how can your business prepare for them?

Revenue-based financing (RBF) can be a helpful tool for businesses, but it’s not without its risks. Since repayments are tied directly to a percentage of your monthly revenue, a sudden drop in sales can create cash flow challenges - even though payments adjust accordingly. For businesses with slim profit margins, the overall cost of this type of financing can end up being higher than traditional loans, which could cut into profitability. Companies with seasonal or unpredictable revenue patterns might also struggle to qualify or keep up with payments if growth slows down.

To minimize these risks, it’s important to have a stable revenue stream in place - typically between $3,000 and $10,000 in monthly sales, along with 6–12 months of consistent history. Running detailed cash flow projections can help you determine if revenue-based payments will still be manageable during slower months. Opting for a reasonable repayment cap, such as 1.5× the funding amount, and maintaining healthy profit margins can also keep costs under control. Lastly, use RBF strategically for growth-focused expenses like inventory or marketing that are likely to boost sales and help cover financing costs.