Need funding for your eCommerce business? Picking the right option can make or break your growth. Here’s a quick breakdown to help you decide:

- Merchant Cash Advances (MCAs): Fast, flexible, tied to daily sales, but costly (20%-60% APR).

- Revenue-Based Financing (RBF): Monthly repayment tied to revenue, moderate cost, ideal for steady sales.

- Business Loans: Low-cost, fixed payments, long-term, but slower approval and stricter requirements.

Key takeaway: Match the funding type to your needs - quick cash for short-term goals, flexible terms for scaling, or low-cost loans for major investments. Dive into each option to see which aligns with your business cycle and cash flow.

Quick Comparison

| Funding Type | Speed | Cost (APR) | Repayment Terms | Best For |

|---|---|---|---|---|

| Merchant Cash Advance | 1-2 days | 20%-60% | Daily/weekly percentage | Seasonal campaigns, quick cash |

| Revenue-Based Financing | 1-2 days | 15%-40% | Monthly percentage | Scaling marketing, inventory |

| Business Loans | 1-12 weeks | 5%-11% | Fixed monthly payments | Long-term growth, large sums |

Pro tip: Before committing, calculate your exact funding needs, compare costs, and ensure repayment terms fit your revenue patterns.

eCommerce Funding Options Comparison: MCAs vs RBF vs Business Loans

eCommerce Financing Options to Scale Your Business - eCom Week LA 2021

sbb-itb-d7b5115

Determining Your Business's Funding Needs

Before diving into funding options, it’s crucial to pinpoint exactly what you need funding for and why. This clarity ensures you borrow the right amount - avoiding the pitfalls of borrowing too much or too little - and helps you select a repayment plan that won’t squeeze your cash flow.

Short-Term vs. Long-Term Funding Needs

Short-term needs typically involve working capital that cycles through your business every 60–120 days. This could include restocking inventory, keeping ads running during busy seasons, or covering operational expenses when marketplace payouts are delayed. For events like Q4 or Prime Day, you’ll want quick-access funding with flexible repayment terms.

On the other hand, long-term needs focus on growth. Think about buying warehouse space, hiring senior team members, or expanding your product offerings. These investments take time to pay off and require funding with longer repayment periods and lower interest rates, such as multi-year bank loans [10].

The key is aligning your funding type with your business cycle. Over 80% of small businesses fail due to cash flow struggles [10]. For example, if your business operates on quarterly cycles but you’re stuck with rigid monthly payments, slower periods could lead to unnecessary financial strain. Matching your funding duration to your business rhythm can help you avoid these issues.

Once you’ve clarified your funding timeline, the next step is calculating exactly how much capital you need.

Calculating Your Capital Requirements

With your timeline in place, it’s time to quantify your funding needs. Start by identifying the purpose of the funding. For instance, dropshipping businesses typically require less capital compared to inventory-heavy or manufacturing models [11]. For a premium eCommerce launch - including custom website development, inventory across multiple SKUs, IT systems, and warehouse setup - you might need around $112,000 in initial capital [12].

Break down your expenses into clear categories:

- One-time costs: Website development, branding, legal fees.

- Monthly fixed costs: Salaries, rent, platform fees.

- Variable costs: Inventory purchases, advertising spend.

If your business hasn’t reached profitability yet, calculate how many months of runway you’ll need to break even. Many eCommerce businesses require about 26 months of runway, which could mean needing a cash reserve of around $215,000 [12].

Key metrics like daily sales velocity, inventory levels, and Return on Ad Spend (ROAS) can help you gauge how urgently you need funding. For example, if your marketplace payout cycle is much longer than the payment terms you have with suppliers, you might face an immediate funding gap [4].

"If you don't secure this runway, growth stalls definitely fast." - Financial Models Lab [12]

Experts suggest keeping at least two months’ worth of operating expenses as a safety net for unexpected downturns [4]. Planning ahead is essential - waiting too long could force you into costly options like personal credit cards [10]. Use slower periods to invest in areas like technology or marketing infrastructure, rather than just scraping by until the next sales spike [10].

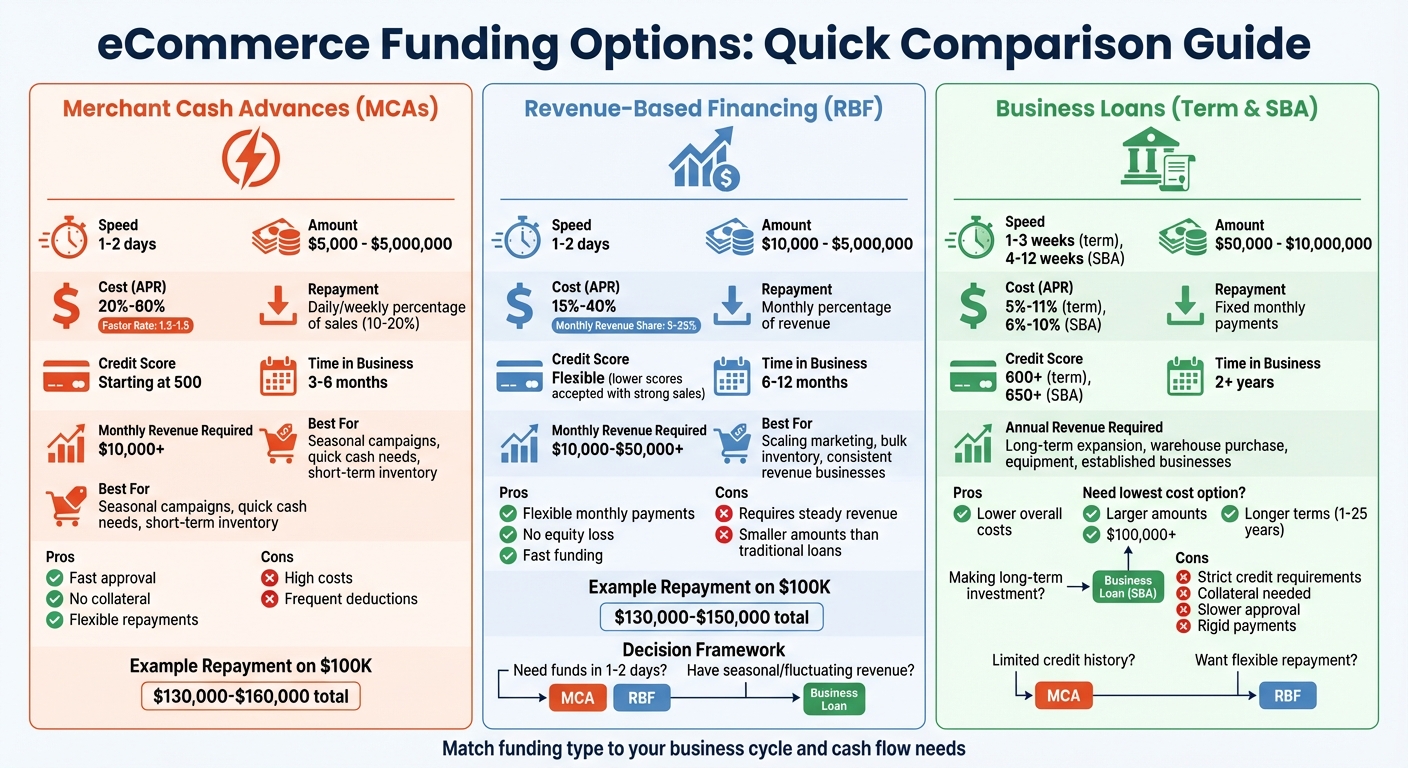

Comparing Funding Options for eCommerce Businesses

Deciding on the right funding method is crucial for managing cash flow and supporting both short-term and long-term growth. Let’s break down three main options for eCommerce sellers: Merchant Cash Advances (MCAs), Revenue‐Based Financing (RBF), and Business Loans. Each has its own way of providing funds, structuring repayments, and impacting your bottom line.

Merchant Cash Advances

Merchant Cash Advances (MCAs) provide a lump sum upfront, based on your projected sales. Instead of fixed monthly payments, repayment is drawn as a percentage of daily or weekly credit card sales - typically between 10% and 20%. These deductions continue until the advance and associated fees are fully paid back [7][15].

This repayment model adjusts with your revenue, making it easier to manage during slower periods. MCAs are a great fit for short-term needs, like stocking up on inventory before a busy season or funding a time-sensitive marketing campaign. For instance, a Shopify seller might use an MCA for a holiday ad push, with repayment tied to daily sales [7].

However, convenience comes at a price. Factor rates for MCAs range from 1.2 to 1.5, translating to effective APRs of 20% to 60% [7][15]. While approval is quick (1–2 days) and doesn’t require collateral or top-tier credit, frequent repayments can strain cash flow, especially if your revenue fluctuates.

| Merchant Cash Advances | Details |

|---|---|

| Maximum Amount | $5,000 – $5,000,000 |

| Starting Cost | 1–6% per month (20–60% effective APR) |

| Approval Speed | 1–2 business days |

| Repayment | Daily/weekly percentage of sales |

| Best For | Short-term needs, seasonal campaigns, businesses with limited credit history |

| Pros | Fast approval, no collateral, flexible repayments |

| Cons | High costs, frequent deductions, less ideal for inconsistent revenue |

If you’re looking for a repayment structure that’s still flexible but tied to monthly revenue instead of daily sales, Revenue‐Based Financing could be the answer.

Revenue‐Based Financing

Revenue‐Based Financing (RBF) is similar to MCAs but offers a key difference: repayments are tied to a fixed percentage of your monthly revenue (typically 5%–25%) instead of daily credit card sales [7]. You receive upfront capital and repay a set total (principal plus a flat fee) without worrying about compounding interest or late fees.

RBF works well for growth-oriented businesses with steady revenue streams. It’s particularly effective for scaling marketing efforts or buying bulk inventory, especially when you can predict returns on investment. For example, a high-margin Amazon seller might use RBF to expand their ad campaigns, repaying 10% of monthly revenue while maintaining healthy cash flow during slower months [7][13][14].

This option relies on performance metrics like monthly revenue, order volume, and sales trends. Funding decisions are often made within 24–48 hours, thanks to direct integration with sales data [7][8][14].

| Revenue-Based Financing | Details |

|---|---|

| Maximum Amount | $10,000 – $5,000,000 |

| Starting Cost | 1–6% per month (capped total repayment) |

| Approval Speed | 1–2 business days |

| Repayment | Monthly percentage of revenue |

| Best For | Scaling marketing, bulk inventory purchases, businesses with consistent revenue |

| Pros | Flexible monthly payments, no equity loss, fast funding |

| Cons | Requires steady revenue, generally offers smaller amounts than traditional loans |

For businesses with strong financials and a need for larger, long-term funding, Business Loans might be the better option.

Business Loans

Business Loans provide access to larger sums at lower costs but come with stricter requirements. Term loans involve fixed monthly payments over 1–5 years, while SBA loans (backed by the government) offer rates starting at Prime Rate + 1% and repayment terms as long as 25 years [14][15].

These loans are ideal for significant investments, such as expanding warehouse space, hiring staff, or purchasing equipment. For instance, an eBay seller could use an SBA loan to buy a warehouse, benefiting from low rates and extended repayment terms, even if the process takes longer [14][15].

The tradeoff? You’ll need strong credit (usually a score of 600 or higher for term loans), collateral, and detailed documentation. Traditional banks may also struggle to understand the needs of online-only businesses, making approval more challenging [2]. Additionally, funding can take anywhere from one week to three months, and fixed monthly payments might strain cash flow during slower seasons [15].

| Business Loans | Details |

|---|---|

| Maximum Amount | $50,000 – $10,000,000 |

| Starting Cost | 1–4% per month (term loans), Prime Rate + 1% (SBA) |

| Approval Speed | 1–3 business days (term loans), 4–12 weeks (SBA) |

| Repayment | Fixed monthly payments |

| Best For | Long-term expansion, established businesses with strong credit |

| Pros | Lower overall costs, larger funding amounts, longer repayment terms |

| Cons | Strict credit requirements, collateral needed, slower approval, rigid payments |

The takeaway: MCAs are the fastest way to get funds but come with higher costs and frequent deductions. RBF offers a middle ground with moderate costs and repayments that adapt to your revenue. Business Loans provide the lowest rates and largest amounts, but they require strong credit and take longer to secure. The right choice depends on how quickly you need funding, the stability of your revenue, and whether you prefer fixed or flexible repayment terms.

Evaluating Costs, Eligibility, and Repayment Terms

Once you’ve got a handle on the basic differences between funding types, the next step is to dig deeper into their costs, check if you qualify, and figure out how repayment terms might impact your business operations.

Cost Breakdown by Funding Type

The real cost of funding isn’t just about the advertised rates. To make fair comparisons, it helps to convert fees, factor rates, and interest into a common metric like APR, which reflects the total cost [5].

Here’s a quick breakdown of how costs stack up across different funding types:

| Funding Type | Typical Cost Structure | Total Repayment (Example: $100K) | Effective APR | Speed |

|---|---|---|---|---|

| Merchant Cash Advance | Factor rate 1.2–1.5 | $130,000–$160,000 | 20%–60% | 1–2 days |

| Revenue-Based Financing | 5%–25% monthly revenue share | $130,000–$150,000 | 15%–40% | 1–2 days |

| Business Loan (Term) | 5%–11% APR | $135,000–$150,000 over 5–10 years | 5%–11% | 1–3 weeks |

| SBA Loan | Prime Rate + 1% (6%–10%) | $146,000 (over 10 years at 8%) | 6%–10% | 4–12 weeks |

Factor rates, common in MCAs and some RBF options, set a fixed repayment amount, making APR comparisons easier. MCAs are typically the most expensive but offer the quickest access to funds. On the other hand, traditional loans are more affordable over time but involve a longer approval process. RBF strikes a middle ground, balancing speed and moderate costs.

"Factor Rate Defined: A fixed multiplier applied to the principal that determines the total payback amount, regardless of payback speed." – Onramp Funds [5]

Eligibility Requirements for eCommerce Sellers

Once you’ve assessed the costs, the next step is checking if your business meets the requirements for these funding options. Eligibility criteria vary widely depending on the funding type. Traditional lenders often focus on credit scores and tax returns, while newer eCommerce funding options rely on real-time sales data [5].

Here’s a snapshot of common requirements:

- Merchant Cash Advances (MCAs): Require at least $10,000 in monthly revenue, 3–6 months in business, and credit scores starting at 500.

- Revenue-Based Financing (RBF): Targets businesses with $10,000–$50,000 in monthly revenue, 6–12 months of operating history, and accepts lower credit scores if sales are strong.

- Business Loans (including SBA loans): Typically require $100,000+ in annual revenue, a minimum of 2 years in business, credit scores around 650 or higher, and supporting documents like tax returns and business plans.

For eCommerce sellers who lack significant physical assets or strong credit, revenue-based options can be easier to qualify for. Many modern lenders streamline the process by integrating with platforms like Shopify or Stripe to analyze sales, order volumes, and even advertising performance.

Repayment Structure Comparison

Repayment terms can have a big impact on your cash flow. Traditional loans usually come with fixed monthly payments, which don’t change even if your revenue fluctuates. In contrast, MCAs and RBF solutions offer repayment structures that adjust based on how much you’re earning.

For example:

- A $100,000 business loan at 8% over seven years would require a fixed payment of about $2,000 per month. If sales slow down, that payment could take a larger chunk of your cash flow.

- An MCA with a 1.4 factor rate might deduct $4,500 during a strong week and $2,000 during a slower one.

- An RBF option deducting 12% of monthly revenue might result in $3,600 in repayments during a good month but only $1,800 during a weaker one.

While flexible repayment options can ease cash flow pressures during slow periods, they often come at a higher overall cost. For instance, total RBF repayments over a year might reach $130,000.

"One of the biggest differences between traditional loans and the best eCommerce financing options is repayment flexibility. Fixed monthly payments can strain cash flow when sales fluctuate." – Onramp Funds [1]

For seasonal businesses, like those that see a surge during Black Friday but slower months afterward, flexible repayment options like MCAs or RBF can be a lifeline. They allow you to preserve working capital during leaner periods. However, businesses with steady, year-round income might prefer the predictability of fixed payments.

Choosing the Right Funding Option

Matching Funding to Business Goals

Once you've evaluated costs and eligibility, the next step is to find the funding option that aligns with your business goals.

Your choice should depend on factors like cash flow, growth plans, and risk tolerance. For instance, if your sales are seasonal - peaking during events like Black Friday but slowing down in January - revenue-based financing might be a solid choice. This option adjusts repayments based on your monthly revenue, typically between 5–25%. That means lower payments during slower months, helping you manage cash flow more effectively [7]. Tailoring your funding to match your sales cycles can help you maintain steady growth in your eCommerce business.

If you're aiming for rapid growth and need funds quickly to scale marketing or stock up on inventory, merchant cash advances can deliver cash in just a few days based on your future sales. However, the downside is the high cost, with effective APRs ranging from 20–60% [7]. On the other hand, for long-term plans like upgrading your fulfillment system or launching new product lines, SBA loans are a better fit. They provide up to $5 million with interest rates between 5–11% over 5–25 years. Keep in mind, though, that these loans often require personal guarantees and take weeks to process [6].

For those who prefer lower risks, traditional loans offer predictable repayment terms and lower costs. If you're looking for flexibility without giving up equity, revenue-based financing - such as options offered by Onramp Funds - can help you grow in sync with your sales patterns.

Steps to Finalize Your Decision

Start by pinpointing the exact amount of capital you need. Many funding calculators can analyze your sales data, inventory cycles, and ad spend to give you a clear picture. Tools that integrate with Shopify or Amazon allow you to model various scenarios in real time, helping you estimate repayments under different funding structures [9]. Once you have this data, create a comparison table that evaluates options based on speed, APR, flexibility, and eligibility.

Before committing to any funding option, carefully review the contract for hidden fees like origination charges, monthly maintenance costs, or early repayment penalties. Convert all potential costs into a single APR figure so you can make accurate comparisons [5]. If anything seems unclear, consult with financial advisors or lenders who specialize in eCommerce businesses. They'll help you avoid common pitfalls, such as over-borrowing or repayment schedules that could strain your cash flow [6].

Finally, apply to multiple lenders to compare actual offers, not just advertised rates. Many modern lenders provide pre-approvals within 24 hours by accessing your sales data through read-only APIs. This lets you review real terms before making a decision. And remember to maintain a cash reserve equivalent to at least two months of operating expenses - this safety net can help you navigate tighter repayment periods if needed [4].

Conclusion

After evaluating costs, eligibility, and repayment terms, the final step is making a decision that fits your business’s unique needs and goals.

The right funding choice depends on your strategy. Whether you need quick access to cash, flexible repayment options, or a longer-term loan, there’s a solution tailored to your situation.

"Choosing the right type of financing is just as important as the funds themselves." - Onramp Funds [3]

Start by calculating how much capital you need, then compare effective APRs and repayment terms to ensure your cash flow remains stable. The funding options discussed here are designed to support both your immediate needs and your plans for future growth.

Today’s eCommerce funding is faster and easier than ever. Companies like Onramp Funds leverage real-time sales data from platforms like Amazon, Shopify, and Walmart to approve funding in as little as 24 hours. There’s no need for lengthy paperwork or collateral. With flat-fee pricing and repayments that adjust to your sales cycles, you can grow your business without sacrificing equity or control.

Simply connect your store data, review your options, and choose a funding partner that aligns with your vision. Onramp Funds provides solutions designed to help you grow while keeping your cash flow strong and your business fully in your control.

FAQs

How do I choose between an MCA and revenue-based financing?

To decide between a Merchant Cash Advance (MCA) and revenue-based financing (RBF), think about how each option fits with your cash flow situation.

With RBF, payments are tied to a percentage of your monthly revenue, making it a more flexible choice if your sales tend to fluctuate. On the other hand, an MCA offers fast access to funds but comes with fixed daily or weekly payments, which could put pressure on your cash flow during slower sales periods.

Take a close look at your revenue patterns and growth goals to figure out which financing option works best for your business.

What’s the best way to estimate how much funding I actually need?

To figure out how much funding you need, start by aligning your financial requirements with your business stage and cash flow patterns. Take a close look at your current cash flow, factoring in things like inventory costs, operational expenses, and any plans for growth. Ideally, you should aim to have enough funds to cover 12–18 months of expenses. This buffer can help you navigate slower periods without stress. Pair specific needs, such as inventory purchases or marketing efforts, with the right type of funding. Borrow carefully to ensure you maintain control over your finances.

What fees should I watch for before signing a funding agreement?

Before entering into a funding agreement, be sure to check for any hidden fees. These might include origination fees, late payment charges, or other unexpected costs that could catch you off guard. Pay close attention to the repayment structure as well - does it align with your cash flow? Taking the time to understand all the terms upfront can save you from unwelcome surprises and help you make a well-informed choice.