If you're an eCommerce seller, chances are you've faced cash flow challenges - unexpected expenses, delayed payouts, or seasonal spikes that leave you scrambling for last-minute funding. This reactive approach often leads to high-interest loans, missed growth opportunities, and strained profitability.

The solution? Plan ahead. By forecasting cash flow and securing funding early, you can avoid costly emergencies, negotiate better terms, and align capital with your business goals. Tools like cash flow forecasting software and revenue-based financing options can streamline this process, ensuring stable growth and financial health.

Key takeaways:

- Reactive funding leads to high costs and operational risks.

- Planned capital strategies help forecast needs, reduce costs, and improve cash flow.

- Use tools like QuickBooks or Onramp Funds for flexible, sales-aligned financing.

This guide explores how to evaluate your financial health, forecast capital needs, and secure funding that supports your growth without unnecessary stress.

Cash Flow Challenges In E-Commerce

What Is Reactive Funding and Why It Causes Problems

Reactive funding refers to emergency financing that sellers rely on when cash runs out. This often happens unexpectedly, forcing them to scramble for money to cover inventory, supplier payments, or marketing expenses [3]. The main culprits? Delayed payouts and sudden spikes in costs.

At its core, the issue stems from a mismatch between cash inflows and outflows. Sellers have to pay upfront for inventory and advertising, but they don’t get paid immediately. This delay frequently pushes them into taking last-minute loans, creating a ripple effect of operational headaches.

Problems with Last-Minute Funding

When cash is needed urgently, options narrow quickly. Emergency loans and merchant cash advances often come with sky-high APRs - ranging from 20% to 50% or more. This eats into profit margins and reduces the money available for growth.

Traditional banks aren’t much help in these situations. Their loan approval processes are too slow, leaving sellers to turn to alternative lenders with unfavorable terms. The result? Disruptions like stockouts due to delayed inventory purchases, missed marketing opportunities during critical sales periods, and strained supplier relationships caused by late payments.

Real-World Examples of Reactive Funding

These challenges come to life in real-world scenarios.

Take a clothing retailer during Black Friday. After a sluggish summer, demand suddenly surges. Without enough cash to restock inventory, the seller takes out a high-interest loan with a 40% APR. While this solves the immediate problem, it slashes profit margins and limits the ability to fully capitalize on the holiday rush. Worse yet, the seller risks losing repeat customers due to stock shortages.

Now consider an electronics store generating $50,000 in Amazon sales. With payout delays of 14–30 days, the store lacks the cash to fund a critical Google Ads campaign for Cyber Monday. To bridge the gap, they borrow at steep rates. By the time the funds are available, the opportunity has slipped away, costing them an estimated $20,000 in lost revenue. This missed chance not only impacts short-term sales but also stalls their long-term growth - underscoring the importance of having a solid capital strategy to avoid such setbacks.

Evaluating Your Current Financial Health

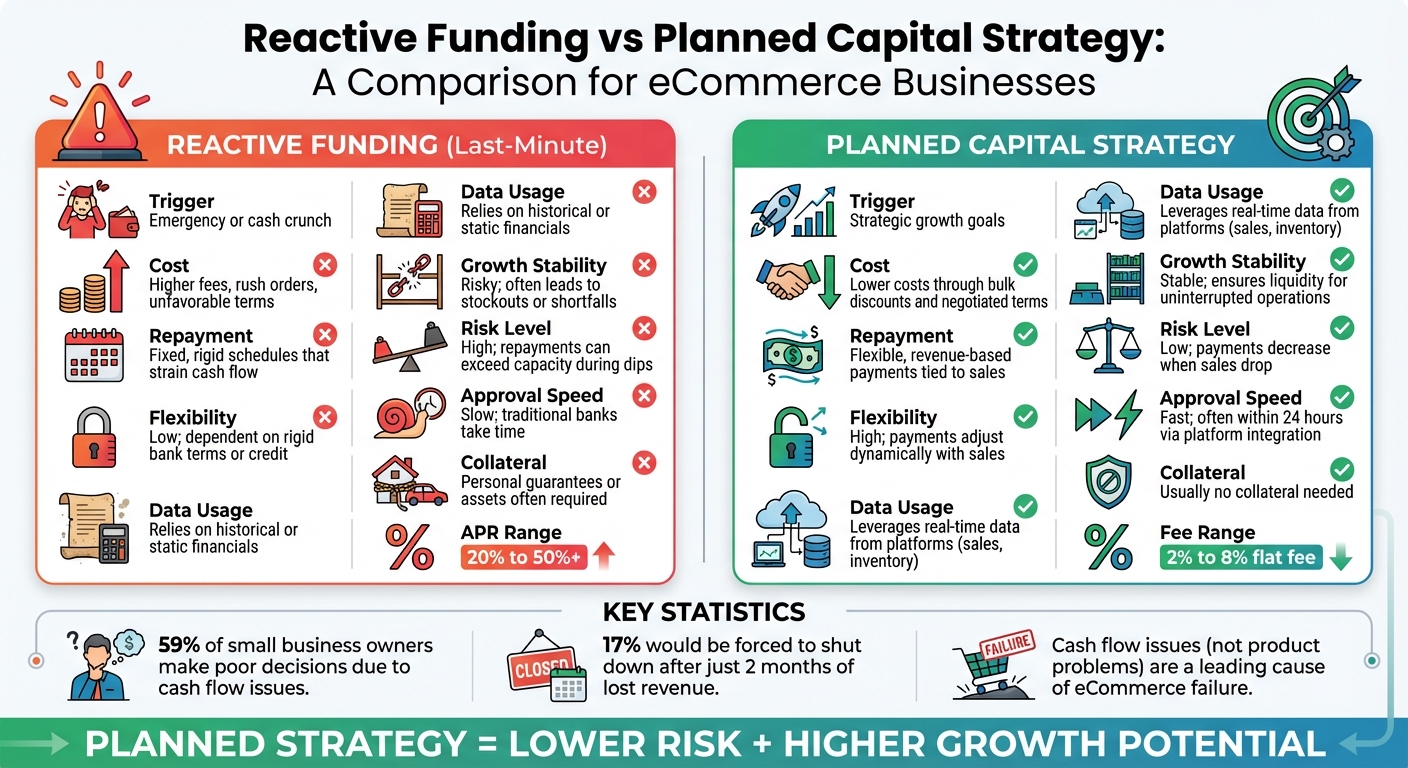

Taking a close look at your financial health is essential. Research shows that 59% of small business owners make poor decisions due to cash flow issues [5], while 17% would be forced to shut down after just two months of lost revenue [5]. These numbers underscore the importance of understanding where you stand financially. This kind of evaluation lays the groundwork for a deeper dive into your cash flow.

Analyzing Your Cash Flow Statements

Start by examining your cash flow statements using the direct method, which tracks actual cash inflows and outflows during a set accounting period [6]. Unlike other methods, the direct approach focuses solely on real cash movement, skipping over non-cash adjustments [6].

Break down your cash flow into three main categories: operating, investing, and financing activities [4]. Here’s a quick rundown of what each category includes:

- Operating activities: Revenue from sales or marketplace payouts.

- Investing activities: Proceeds from selling equipment or earned interest.

- Financing activities: Loan proceeds or contributions from owners.

On the expense side, separate your spending into fixed costs (like rent and salaries), variable costs (such as shipping, packaging, and raw materials), and one-time expenses (like equipment purchases or tax payments) [5].

"Cash flow represents the movement of money through a business during a specific period. It encompasses all incoming funds from sales and investments alongside outgoing payments for expenses." – Ramp [5]

To get a clear picture of your cash position, calculate your net cash flow (inflows minus outflows). Then, add this to your opening balance to determine your closing balance [4]. This final figure shows whether you’re ending the period with a surplus or a deficit. Compare these numbers to your projections to identify where factors like seasonality, late payments, or inaccurate estimates might be affecting your bottom line [5].

For a more streamlined process, integrate your eCommerce data to automate tracking. Real-time insights can help you avoid pitfalls like "zombie spending" or subscription creep - those sneaky recurring charges that drain funds without adding value [5][6].

Calculating Key Financial Metrics

Once you’ve reviewed your cash flow, it’s time to calculate some key metrics to assess your liquidity. A good starting point is the Operating Cash Flow Ratio (OCFR), which you can find by dividing your operating cash flow by your current liabilities. If your ratio is below 1.0, it could signal trouble meeting short-term obligations. For eCommerce businesses, a healthy OCFR is typically 1.25 or higher [6].

"Operating cash flow ratios are measurements of liquidity. A OCRF of under '1' means that the company cannot meet its current obligations." – Ramp [6]

Use historical sales data to set funding thresholds that alert you when additional capital might be needed. For example, you may need extra funds for inventory restocking, marketing pushes, or seasonal staffing. Align your cash flow statements with both actual and projected expenses to spot recurring shortfalls, especially during slower months like August or the post-holiday dip in January and February [1].

Keep a close watch on inventory costs, product performance, and excess stock. Dive into return data to see how it impacts your net revenue. Review labor costs to identify when extra staffing or overtime might be necessary. Finally, evaluate your marketing efforts by calculating customer acquisition costs (CAC) and measuring the ROI of specific campaigns.

These metrics provide valuable insights to help you plan for capital needs that support your growth strategy.

Predicting Future Capital Requirements

Once you understand your current financial health, the next step is to forecast your future capital needs. This forward-looking approach helps you avoid scrambling for funds during a cash crunch. By planning ahead, you can secure funding or adjust spending well before any issues arise.

Your forecast should account for your business's seasonal patterns. Keep an eye on cash inflows and outflows to spot trends like Black Friday/Cyber Monday surges, slower summer months, or the post-holiday slump early in the year. Include key metrics such as Customer Acquisition Cost (CAC), Average Order Value (AOV) (after accounting for discounts and returns), and operating costs like shipping fees, payment processing, and payroll expenses as your business grows.

"Forecasts aren't about getting every number right, they're about thinking through how your business works and what it needs to grow - plus how you can do that with fewer surprises and greater visibility." – Dan Kang, CFO at Mercury [7]

To prepare for different scenarios, build multiple forecasts: a Base case, a Stretch case for optimistic growth, and a Conservative case for tougher conditions. Update these forecasts monthly with actual data from your accounting system or other platforms. This regular updating helps you spot patterns - like months when bi-weekly payroll occurs three times instead of two - that can significantly affect your cash flow [8]. Modern forecasting tools can then turn these insights into actionable plans.

Cash Flow Forecasting Tools

Automated forecasting tools connect directly to platforms like Shopify or Amazon, pulling real-time data to predict cash flow for the next 12–13 months [5]. For shorter-term needs, QuickBooks offers reliable 30- and 90-day forecasts, while tools like Cash Flow Frog and PlanGuru are better suited for long-term projections [8].

These tools can reveal potential cash shortfalls months in advance. For example, if your forecast shows a deficit in April, you could negotiate better payment terms with suppliers, delay non-essential spending, or secure funding ahead of time. In one case, simply shifting a major expense like website development from one month to another turned a projected cash balance from -$480 to +$2,020 [8].

For short-term planning, use the direct method, which tracks actual cash inflows and outflows. For longer-term projections (beyond six months), switch to the indirect method. This approach starts with projected net income and adjusts for non-cash items like depreciation [5]. Both methods provide the clarity needed to decide whether to save extra cash or reinvest it into growth opportunities.

Planning for Growth Investments

When you're ready to grow - whether by launching a new product, ramping up ad spend, or adding inventory for a new sales channel - your forecast becomes your blueprint. Tie purchase orders and Cost of Goods Sold (COGS) to expected sales volumes. This ensures you’re not over-ordering (and paying high storage fees) or under-ordering and missing out on sales during peak times [7].

Align your capital needs with specific business milestones. For example, if you’re transitioning from Amazon to a direct-to-consumer website, plan for expenses like website development, increased marketing, and changes in fulfillment. Schedule these major costs during months when your forecast shows surplus cash [8]. This proactive approach helps you avoid last-minute funding gaps.

Negotiating supplier terms can also be a game-changer. Extending payment terms by just two weeks can sometimes eliminate the need for external funding during tight months [8]. Additionally, during high-performing months, set aside 20–30% of your cash as a reserve. This cushion can cover unexpected disruptions or allow you to seize sudden opportunities [5].

Finally, track retention trends by customer cohort to better predict repeat purchases instead of relying solely on new customer acquisition. Use your forecast to experiment with strategies like bundling, upselling, or pricing adjustments. These insights can help you refine your capital needs and make smarter, data-driven decisions.

sbb-itb-d7b5115

Matching Capital to Business Goals with Onramp Funds

After defining your forecast and pinpointing your capital requirements, the next step is finding a funding solution that aligns with your business cycle. Onramp Funds specializes in financing tailored for eCommerce sellers, offering a way to grow without the pressures of traditional loans or giving up equity. Their approach ties repayment directly to your business's performance, creating a flexible and growth-friendly capital strategy.

How Revenue-Based Financing Works

Onramp Funds operates on a revenue-based financing (RBF) model, where repayments adjust based on your sales. Instead of rigid monthly payments that don’t account for your cash flow, you pay a percentage of your daily or weekly revenue - usually between 5% and 12%. When sales are strong, you repay faster. When sales slow down, payments decrease, helping you maintain cash reserves.

This financing is non-dilutive, meaning you retain full ownership of your business. There's no need for collateral, and approvals are quick - typically within 24 hours - by connecting your Shopify, Amazon, or other eCommerce platform to Onramp. The underwriting process relies on your sales data rather than credit scores or personal guarantees. Fees are straightforward, with a flat charge (generally 2% to 8% of the funded amount), and repayment terms typically range from 1 to 6 months [9][10].

For instance, in Q2 2024, Shopify store BeautyBakery secured $250,000 to scale inventory. By opting for an 8% revenue share, the store saw revenue grow by 180%, reaching $1.2 million in just six months. Repayments averaged $20,000 per month, with the loan fully paid off in a year, while cash flow improved by 45% [Onramp Funds Case Studies, 2024].

Onramp offers three funding options to suit different business needs:

- Variable Funding: Ideal for immediate growth, such as inventory purchases or marketing. Repayments can be as low as 1% of daily sales, with no monthly minimums.

- Fixed Funding: Provides predictable, fixed-dollar repayments, perfect for businesses needing stability while scaling strategically.

- Rolling Cash Line: Designed for established businesses, this revolving credit option allows access to funds every two weeks, with fees applied only to the capital in use [10].

Next, we’ll explore how the Funding Calculator helps you tailor financing to your business goals.

Using the Onramp Funds Funding Calculator

Onramp's Funding Calculator is a handy tool that lets you estimate your funding and repayment schedule before applying. By entering details like your average monthly revenue, desired funding amount, and growth rate, you can instantly see total repayment, monthly estimates, and the cash flow impact over 12–24 months.

For example, if your average monthly revenue is $40,000 and you request $150,000 at a 7% revenue share with a 20% growth projection, the calculator estimates a total repayment of $210,000 over 18 months. Monthly payments start at $2,800 and increase to $3,360 as your revenue grows, ensuring the funding aligns with your cash flow [3]. This allows you to plan funding for goals like expanding inventory for Q4, launching a new product line, or boosting ad spend for a direct-to-consumer campaign.

In November 2023, Amazon seller PeakPerformance Gear used the calculator to secure $180,000 for pre-Black Friday marketing. With a 10% revenue-share estimate, their sales hit $900,000 - 3.5 times the previous year’s. Repayments averaged $15,000 per month during peak season, delivering a 1.3× return in nine months and improving cash flow by 60% [Onramp Funds Blog, 2024].

The calculator also lets you test different scenarios. For example, if you’re planning a $200,000 inventory purchase at a 9% revenue share on $60,000 monthly revenue, you can verify that repayments stay within 15% of your revenue after growth - ensuring your business can manage the funding. Similarly, for marketing campaigns, you can input your expected ROI (e.g., a 2× return in six months) to confirm that the funding supports positive cash flow while achieving your sales growth targets [3].

Steps to Adopt a Planned Capital Approach

Reactive vs Planned Funding Strategies for eCommerce Businesses

Shifting from a reactive to a more structured funding approach starts with automating your financial processes and creating repeatable systems for managing capital. Begin by analyzing past sales data to spot patterns - like revenue spikes or dips - and to pinpoint funding needs for inventory, marketing, or staffing. Use this analysis to forecast operating expenses and match them with your cash flow. This way, you can anticipate funding gaps and address them before they escalate into urgent problems [1]. These insights lay the groundwork for automating processes that align funding with your sales trends.

To make this seamless, integrate your selling platforms - such as Amazon, Shopify, or Walmart - with financial tracking tools. This integration offers real-time insights into sales, inventory, and customer metrics [2]. It also enables flexible repayment structures tied to your revenue. For instance, if you’re using Onramp Funds, your repayments automatically adjust based on your sales performance. During slower months like February or August, when revenue dips, your payments decrease as well, helping you conserve cash reserves [1].

Avoid locking yourself into fixed costs. Instead, opt for flexible capital that scales with your needs [1]. Use HR data to plan for seasonal staffing and secure inventory ahead of peak seasons to negotiate better terms [1].

Implement a Just-In-Time inventory approach by using precise demand forecasting and strategic capital allocation [2]. This reduces excess inventory costs while ensuring you have enough liquidity for other operational needs like shipping and advertising. Additionally, reinvest capital into long-term customer retention strategies - think email campaigns or retargeting ads - to turn occasional buyers into loyal customers, boosting your return on acquisition costs [1].

Automating Financial Tracking and Payments

Automation plays a central role in adopting a planned capital strategy. By connecting your eCommerce platforms directly to financial tools, you gain real-time visibility into sales, inventory turnover, and cash flow - eliminating the need for manual data entry [2]. This kind of integration enables funding providers like Onramp Funds to approve financing within 24 hours, using your actual sales performance instead of outdated credit scores or static financial documents. Automated repayment schedules then adjust in line with your sales, allowing you to hold onto cash during slower periods.

To further optimize cash flow, automate overdue reminders and schedule supplier payments strategically [12]. Avoid paying invoices early unless it offers a financial benefit, like a discount. Taking full advantage of payment terms keeps cash available for your business longer. Also, keep an eye on key liquidity metrics like the Cash Conversion Cycle and the Current Ratio (aiming for a healthy range of 1.5 to 2) to continuously monitor your financial health [12].

Reactive vs. Planned Funding: A Comparison

| Feature | Reactive Funding (Last-Minute) | Planned Capital Strategy |

|---|---|---|

| Trigger | Emergency or cash crunch | Strategic growth goals |

| Cost | Higher fees, rush orders, unfavorable terms | Lower costs through bulk discounts and negotiated terms |

| Repayment | Fixed, rigid schedules that strain cash flow | Flexible, revenue-based payments tied to sales |

| Flexibility | Low; dependent on rigid bank terms or credit | High; payments adjust dynamically with sales |

| Data Usage | Relies on historical or static financials | Leverages real-time data from platforms (sales, inventory) |

| Growth Stability | Risky; often leads to stockouts or shortfalls | Stable; ensures liquidity for uninterrupted operations |

| Risk Level | High; repayments can exceed capacity during dips | Low; payments decrease when sales drop |

| Approval Speed | Slow; traditional banks take time | Fast; often within 24 hours via platform integration |

| Collateral | Personal guarantees or assets often required | Usually no collateral needed |

This comparison highlights how a proactive, planned capital strategy can stabilize your operations and support growth. By automating financial tracking and aligning repayments with your revenue, you turn funding into a tool for growth rather than a recurring source of stress. Flexible financing options, like those offered by Onramp Funds, make it easier to manage cash flow and focus on scaling your business sustainably.

Conclusion

Shifting from a reactive approach to a planned capital management strategy can reshape how your eCommerce business operates. Instead of scrambling for last-minute funds when cash runs low, you can forecast your financial needs, monitor key metrics, and secure capital before challenges arise. This approach helps you avoid the steep costs of emergency loans - some of which carry APRs over 80% [11] - and reduces the risk of inventory shortages that could harm your marketplace rankings. Studies reveal that cash flow issues, not product problems, are a leading cause of failure for many eCommerce businesses [3]. Planning ahead is essential for maintaining stability and driving growth.

One practical solution comes from Onramp Funds. They offer customized financing options tailored to align with your revenue patterns, unlike traditional bank loans with rigid repayment terms. Their revenue-based financing adjusts repayments based on your actual sales, ensuring flexibility in sync with your business cycles. You can use the Onramp Funds Funding Calculator to explore your capital needs and repayment scenarios, whether you're projecting $500,000 in annual revenue or preparing for a major inventory investment. With approvals in less than 24 hours and no personal guarantees required, Onramp Funds provides a stress-free alternative to conventional lending.

Planned capital management goes beyond avoiding cash flow crises - it empowers you to make strategic decisions based on accurate financial forecasting rather than reactive measures. As Cara Curphey, Founder of Albion Bookkeeping & Consulting, shared, "Finally found one that works for us! Great UX, intuitive software, accurate forecasting" [3].

By consistently monitoring your cash flow and applying the forecasting techniques outlined in this guide, you can position your business for growth. Whether you opt for Onramp Funds' Variable product for rapid scaling, Fixed for predictable expansion, or a Rolling Cash Line for continuous flexibility, you'll be financing your business with strategy, not urgency.

This proactive approach to forecasting and financing enables you to optimize supplier terms, manage inventory effectively, and invest in marketing with confidence. Transitioning to planned capital management puts you in control of your business's future, turning funding into a tool for sustainable growth.

FAQs

What advantages does a planned capital strategy offer over reactive funding?

Switching to a planned capital strategy can help eCommerce businesses maintain steady financial footing and set the stage for long-term success. By planning funding needs ahead of time, you can sidestep those last-minute cash flow crises that can disrupt daily operations or stall growth efforts. This approach ensures your resources are properly allocated to critical areas like inventory, marketing, or scaling.

It also gives you better control over cash flow, making it easier to handle seasonal shifts in demand without leaving gaps that could jeopardize your business. With finances under control, you’re in a stronger position to take advantage of opportunities, minimize risks, and create a business that can weather challenges. This strategy lays the groundwork for consistent growth and a more resilient future.

How can eCommerce sellers accurately predict their cash flow needs?

To get a handle on cash flow needs, eCommerce sellers should dive into their revenue streams - whether that's sales from their own website, marketplaces like Amazon, or subscription models. At the same time, they need to account for key expenses such as inventory, marketing, platform fees, and taxes. Taking a close look at past sales data can reveal seasonal trends and growth patterns, making it easier to predict when money will come in and go out.

Leveraging forecasting tools that sync with platforms like Shopify or Amazon can offer real-time insights and help with scenario planning. A cash flow tracking system is another must-have; it highlights timing gaps between income and expenses, giving sellers the chance to prepare and sidestep potential shortfalls. Regularly updating forecasts ensures they stay aligned with market shifts or changes in business performance, helping to keep finances stable and growth on track.

What is revenue-based financing, and how is it different from traditional business loans?

Revenue-based financing (RBF) offers businesses upfront capital in exchange for a fixed percentage of their future revenue until a predetermined repayment amount is met. What sets RBF apart from traditional loans is its flexibility - repayments adjust based on your actual revenue. When sales are strong, payments increase; during slower months, they decrease. This approach helps reduce financial pressure during challenging times.

Traditional loans often come with rigid requirements like collateral, fixed repayment schedules, and lengthy approval processes. These factors can make them less suitable for eCommerce businesses, which often deal with unpredictable cash flow. RBF, on the other hand, stands out for its speed and simplicity. Funds can often be accessed within 24 to 48 hours, without the need for collateral or giving up equity. This makes it an appealing option for businesses looking to manage growth or navigate seasonal ups and downs.