Running an eCommerce business requires careful financial planning to grow without risking instability. Cash flow problems are a major cause of business failures, and traditional funding options like bank loans or merchant cash advances often don't meet the needs of fast-moving, digital-first businesses. Here's how you can scale responsibly:

- Optimize Cash Flow First: Understand your Cash Conversion Cycle (CCC) and reduce delays caused by slow inventory, late customer payments, or marketplace payout gaps.

- Match Payment Schedules to Sales Cycles: Aim for a negative CCC, where you get paid before paying suppliers. Strategies like preselling products or negotiating payment terms can help.

- Use Flexible Financing:

- Revenue-Based Financing (RBF): Get upfront capital tied to your sales performance, with flexible repayments that adjust during slow periods.

- Inventory Funding: Cover stock costs without draining cash reserves, with repayments aligned to inventory sales.

Example Solution: Onramp Funds offers RBF tailored for eCommerce sellers, providing fast capital with a transparent flat fee (2–8%) and no rigid monthly payments. This approach supports growth while avoiding over-leveraging.

eCommerce Funding Secrets Every Seller Should Know

sbb-itb-d7b5115

Improve Cash Flow Before Seeking Funding

Before looking for external funding, it’s crucial to tighten up your cash flow. Why? 61% of businesses struggle with cash flow issues, and 82% of small business failures are linked to it [4]. By improving cash flow, you might even find that you don’t need outside capital at all.

A good starting point is understanding your Cash Conversion Cycle (CCC) - the time it takes for money spent on inventory to return as revenue. The formula is simple: Days Inventory Outstanding + Days Sales Outstanding - Days Payables Outstanding = Cash Conversion Cycle [6]. A shorter CCC means better flexibility and financial stability.

Here’s the payoff: businesses that streamline their inventory systems often see 10–30% higher profit margins compared to those with inefficient processes [4]. On top of that, optimizing inventory can free up 20–30% of cash that’s been tied up in stock [4]. That’s money you can reinvest in growth - without taking on debt. Once you grasp your CCC, it’s easier to pinpoint where cash flow delays might be holding you back.

Find and Fix Cash Flow Delays

Cash flow delays happen when your outgoing payments outpace incoming revenue. For example, Amazon third-party sellers often face this issue - they’ve already paid for inventory and shipping, but they’re waiting weeks to receive revenue [4]. It’s a common scenario, and it’s no surprise that 32% of eCommerce businesses fail because they run out of money [4].

To tackle this, you first need to identify where your cash is getting stuck:

- Slow-moving inventory ties up funds that could be used elsewhere. Analyze sales margins and inventory turnover ratios to identify underperforming products [5]. Switching to Just-In-Time (JIT) inventory - ordering materials only when needed - can minimize costs from unsold stock [5].

- Late customer payments are another common issue. Keep an eye on your "Days Sales Outstanding" and invoice aging reports to spot delays [6]. Shorten payment terms, offer early payment discounts, and make it easier for customers to pay using multiple methods [5].

- For marketplace sellers, map the gap between when you ship a product and when the money hits your account [6].

Here’s a quick breakdown:

| Delay Factor | How to Identify It | Solution |

|---|---|---|

| Slow Inventory | Check sales margins and inventory turnover ratios [5] | Use JIT inventory or liquidate underperforming SKUs [5] |

| Marketplace Payouts | Map time between shipping and bank deposits [6] | Use daily payout services or negotiate better terms [6] |

| Late Customer Payments | Track "Days Sales Outstanding" and invoice aging [6] | Offer discounts for early payments or rewards [5] |

Match Payment Schedules to Sales Cycles

One of the best ways to improve cash flow is by aiming for a negative Cash Conversion Cycle - essentially, getting paid before you have to pay your suppliers. This strategy lets vendors finance your operations. Gymshark, for instance, achieved a CCC of -101 days, which played a major role in its success as a billion-dollar company [1]. Amazon operates at -21 days, while Walmart runs at 2 days [1].

Taylor Holiday, CEO of Common Thread Collective, explains this concept perfectly:

"A negative cash conversion cycle [in which] vendors are financing their operations. As their sales grow, their cash balance magically increases instantly." [1]

To move toward a negative CCC, consider these strategies:

- Negotiate Net on Delivery terms (e.g., Net 30 starting upon receipt), giving you more time to hold onto your cash [1].

- Reduce Minimum Order Quantities (MOQs) so you can order smaller amounts more frequently. While this might slightly increase per-unit costs, it improves inventory turnover and keeps cash from being tied up in stagnant stock [1].

- Experiment with preselling products. Crowdfunding or offering preorders on your site lets customers pay upfront, flipping the cash cycle and giving you precise data on how much stock to produce [1].

Lastly, plan your cash flow 12–18 months ahead, accounting for inventory, marketing, and taxes. This foresight helps you spot potential dips and handle seasonal fluctuations without scrambling for last-minute funding [2].

Use Revenue-Based Financing with Onramp Funds

Once you've optimized your cash flow, you may still need additional capital for things like inventory or advertising. This is where revenue-based financing (RBF) can be a game-changer. Unlike traditional loans or equity funding, RBF provides upfront capital in exchange for a fixed percentage of your future sales until the total amount, plus a flat fee, is repaid. The best part? You retain full ownership of your business, and there’s no need for personal guarantees.

Onramp Funds is designed specifically for marketplace sellers on platforms like Amazon, Walmart, Shopify, and TikTok Shop. By tapping into real-time sales data from your eCommerce platform, Onramp determines funding amounts that match your business's actual performance. This makes it an excellent option for covering costs like fulfillment, advertising, or even boosting your inventory during seasonal spikes.

Onramp Funds Custom Funding Offers

Onramp Funds takes a personalized approach to financing, creating offers based on your sales history and business needs. Instead of offering a generic loan, they analyze your revenue trends to determine the right level of support. If your business generates $3,000 or more in monthly sales, you can connect your storefront to Onramp's portal. This real-time sharing of revenue and order volume data strengthens your application and speeds up approval - often within 24 hours. Plus, since the funding is equity-free, you stay in full control of your business.

Benefits of Onramp Funds' Fixed Fee Structure

With Onramp Funds, you'll pay a transparent flat fee ranging from 2% to 8%, rather than dealing with fluctuating interest rates. This means you know upfront exactly what you'll owe - no hidden charges or unexpected terms. Compare this to traditional merchant cash advances, which can have effective APRs exceeding 50%, making them unsustainable for long-term growth. On top of that, Onramp's structure avoids the rigid monthly payments of conventional loans, helping you sidestep cash flow issues.

As LinkedIn/Cogsflow puts it:

"In a volatile demand environment, products that flex with revenue or allow low‑friction early repayment reduce stress when conditions change."

Flexible Repayments Based on Sales

Repayments with Onramp Funds are tied to a fixed percentage of your future sales. This means they automatically adjust to reflect your revenue - lower during slower periods and higher when sales pick up. Unlike traditional bank loans with fixed monthly payments, this flexible repayment model helps you manage cash flow more effectively while keeping your business on track for growth. It’s a financing approach that adapts to your needs and supports your expansion without sacrificing operational stability.

Fund Inventory Without Over-Extending Your Business

Inventory funding is a smart way to replenish stock without putting unnecessary strain on your business. By leveraging optimized cash flow and repayment flexibility, this approach ensures your shelves stay stocked during critical times without the risks tied to traditional loans.

Running out of inventory during peak periods can cost eCommerce businesses 4-8% of their annual revenue[7][8]. But relying on fixed-loan payments to load up on stock can drain your cash reserves. Inventory funding offers a better solution - it allows you to purchase inventory based on its value and aligns repayments with your actual sales pace.

How Inventory Funding Supports eCommerce Growth

Inventory funding provides short-term capital specifically for purchasing stock, helping you avoid tapping into your operating cash. Since the financing is tied to your inventory value, you can stock up for high-demand times like Black Friday or back-to-school shopping without overextending your resources. Best of all, repayments are tied to inventory sales rather than a rigid schedule.

This approach helps eCommerce businesses avoid costly stockouts, an issue that affects 62% of businesses and costs retailers a staggering $634 billion globally each year[9][11]. Sellers who use inventory funding often experience 25% faster restocking times and see an 18% boost in revenue compared to those who rely solely on cash reserves[9][11]. The biggest advantage? You can keep cash available for other critical needs, like advertising or logistics, while ensuring you never miss a sale due to empty shelves.

By providing targeted funding, inventory financing not only helps preserve cash but also creates opportunities for scaling your business without unnecessary risks.

Minimize Risk with Flexible Inventory Financing

The best inventory financing options are tailored to your sales patterns and growth goals. Look for providers offering usage-based advances (typically 70-90% of your inventory value) and repayments that start only after your products begin to sell[8][13].

When evaluating financing options, consider your current revenue and inventory turnover cycles. Many providers require at least $10,000 in monthly sales to qualify. Opt for terms ranging from 30 to 120 days, aligning with how quickly you turn over inventory. Also, prioritize financing without prepayment penalties, allowing you to pay off advances early if sales exceed expectations[7][10].

To reduce risk, focus on proven SKUs with profit margins above 30% rather than experimenting with untested products. Start with smaller advances - around 20% of your total inventory needs - to test how the financing works with your cash flow before scaling up[12][13]. This cautious strategy helps you seize growth opportunities while avoiding the pitfalls of over-borrowing.

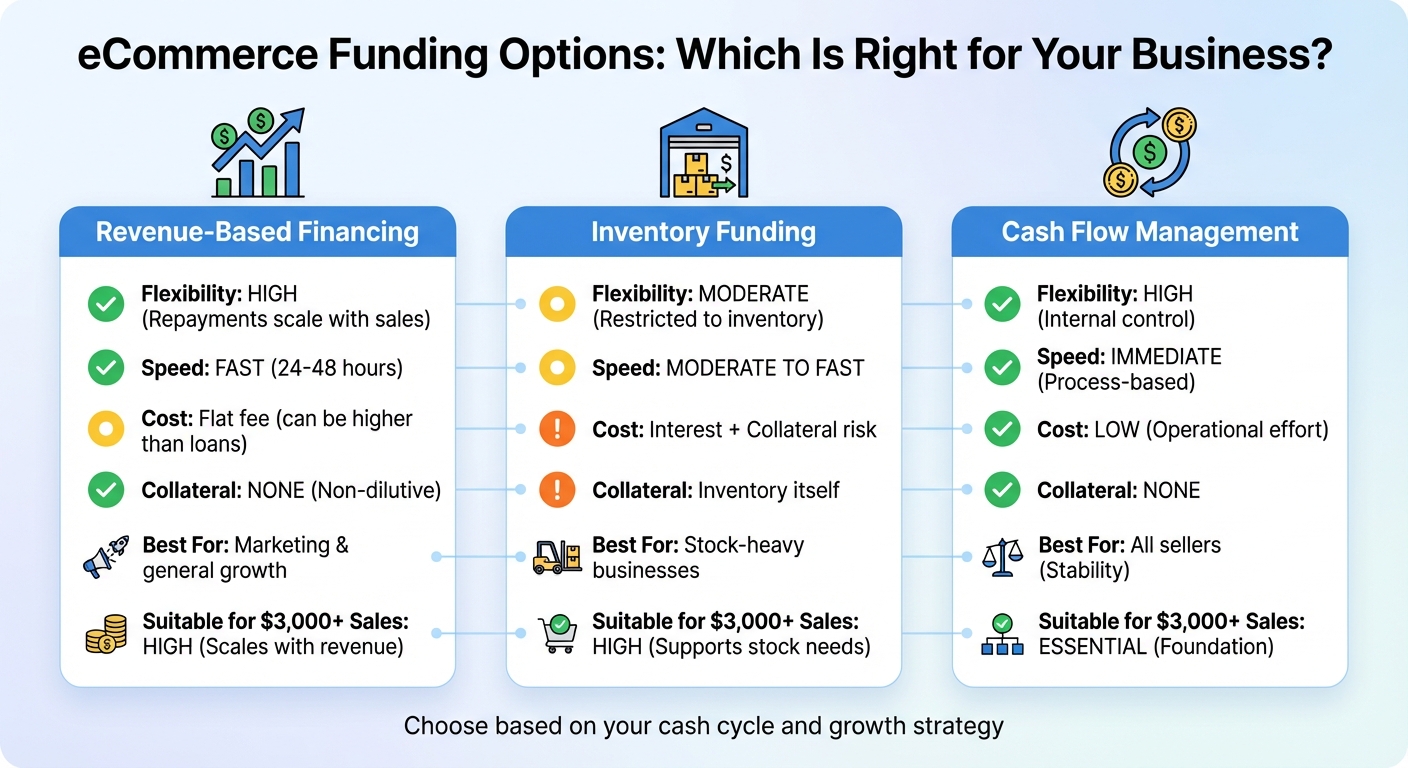

Compare Funding Options for Your eCommerce Business

eCommerce Funding Options Comparison: Revenue-Based Financing vs Inventory Funding vs Cash Flow Management

When it comes to financing your eCommerce business, understanding and comparing your options is crucial. The right funding mix depends on your business goals and how your cash flow operates.

Revenue-based financing offers flexible capital that adjusts with your sales, making it a solid choice for growth initiatives. On the other hand, inventory funding is tailored for businesses that need to stock up for seasonal peaks, as it directly ties the financing to inventory purchases. And, of course, maintaining a healthy internal cash flow remains essential for long-term stability.

Each option impacts daily operations differently. Revenue-based financing provides upfront funds without requiring collateral, and repayments automatically adjust during slower sales periods. In contrast, inventory funding is more restrictive, as it focuses solely on inventory purchases and uses the stock as collateral. Understanding these distinctions helps you align funding with your operational needs.

"The question leading brands are asking in 2026 is not 'Can we get approved?' but 'Does this structure fit our cash cycle and strategy?'" - Cogsflow [2]

Once you've outlined your funding options, it's time to evaluate your repayment capacity. Test your ability to handle repayments even if sales drop by 20–30%, and ensure the terms align with your funding objectives [2]. Many eCommerce businesses are now combining revenue-based financing with inventory funding to manage costs effectively while retaining equity [3].

Funding Options Comparison Table

| Feature | Revenue-Based Financing | Inventory Funding | Cash Flow Management |

|---|---|---|---|

| Flexibility | High (Repayments scale with sales) | Moderate (Restricted to inventory) | High (Internal control) |

| Speed | Fast (24–48 hours) | Moderate to Fast | Immediate (Process-based) |

| Cost | Flat fee (can be higher than loans) | Interest + Collateral risk | Low (Operational effort) |

| Collateral | None (Non-dilutive) | Inventory itself | None |

| Best For | Marketing & general growth | Stock-heavy businesses | All sellers (Stability) |

| Suitable for $3,000+ Sales | High (Scales with revenue) | High (Supports stock needs) | Essential (Foundation) |

Conclusion

Growing your eCommerce business requires careful attention to financial stability. Managing cash flow effectively and aligning payment schedules with your revenue are key steps toward sustainable growth.

With improved cash flow, targeted financing can provide the extra boost your business needs. For example, Onramp Funds offers revenue-based financing that delivers upfront capital with repayment terms tied to your daily sales. Their custom funding options feature a transparent fixed fee (ranging from 2–8%) and eliminate the stress of fixed monthly payments during slower periods. This model ensures your financing costs adjust naturally with your revenue, giving you the flexibility to scale without unnecessary pressure.

If your business relies heavily on inventory, inventory funding can be a game-changer. This option allows you to cover stock-related expenses as needed, helping you avoid pitfalls like excessive holding costs or running out of stock. It’s a practical way to meet your inventory demands without straining your operations.

Take a moment to assess the funding options outlined earlier and consider how they align with your cash cycle and growth plans. Start by reviewing your current cash flow, then explore Onramp Funds' eligibility to find a solution tailored to your needs. Flexible financing options can help you grow steadily without taking on more risk than your business can handle.

FAQs

How do I calculate my cash conversion cycle (CCC)?

To figure out your cash conversion cycle (CCC), use this formula:

CCC = DIO + DSO - DPO

Here’s how each component breaks down:

-

Days Inventory Outstanding (DIO):

(Average Inventory ÷ Cost of Goods Sold) × 365

This measures how long, on average, inventory stays in your possession before being sold. -

Days Sales Outstanding (DSO):

(Accounts Receivable ÷ Total Sales) × 365

This indicates how many days it takes, on average, to collect payment after a sale. -

Days Payables Outstanding (DPO):

(Accounts Payable ÷ Cost of Goods Sold) × 365

This reflects how many days, on average, you take to pay your suppliers.

By combining these metrics, the CCC provides insight into how efficiently your business manages cash flow tied to operations.

When should I use revenue-based financing instead of a fixed loan?

Revenue-based financing works well if you're looking for a repayment plan that adjusts to your income. Unlike traditional loans with fixed monthly payments, this approach aligns with your sales, offering relief during slower months. It's particularly helpful for businesses with fluctuating cash flow or seasonal sales, as repayments rise and fall with your performance, minimizing financial pressure during unpredictable revenue periods.

How much funding can I safely take without risking cash flow?

The amount of funding your business can safely secure depends heavily on your cash flow cycle and specific needs. It's important to focus on borrowing only what aligns with your immediate priorities - whether that's stocking up on inventory, boosting marketing efforts, or covering other essentials - without taking on unnecessary debt.

Flexible funding options, such as revenue-based financing or inventory loans, can be a smart choice. These options are designed to align with your cash flow patterns, making repayment more manageable and reducing financial strain. The key is to ensure that any funding you take directly supports growth while keeping your operations stable and sustainable.