Revenue-based financing (RBF) is reshaping how eCommerce businesses secure funding. Unlike traditional loans, RBF provides upfront capital in exchange for a percentage of future sales, making repayments flexible and aligned with revenue cycles. This approach is fast, requires no collateral, and avoids equity dilution, making it especially appealing to online sellers with fluctuating cash flow.

Key Highlights:

- Fast Funding: Funds are delivered in 24–72 hours, compared to weeks for bank loans.

- Flexible Repayments: Payments adjust with sales, easing cash flow during slower months.

- No Collateral, No Equity Loss: Businesses retain full ownership without risking personal assets.

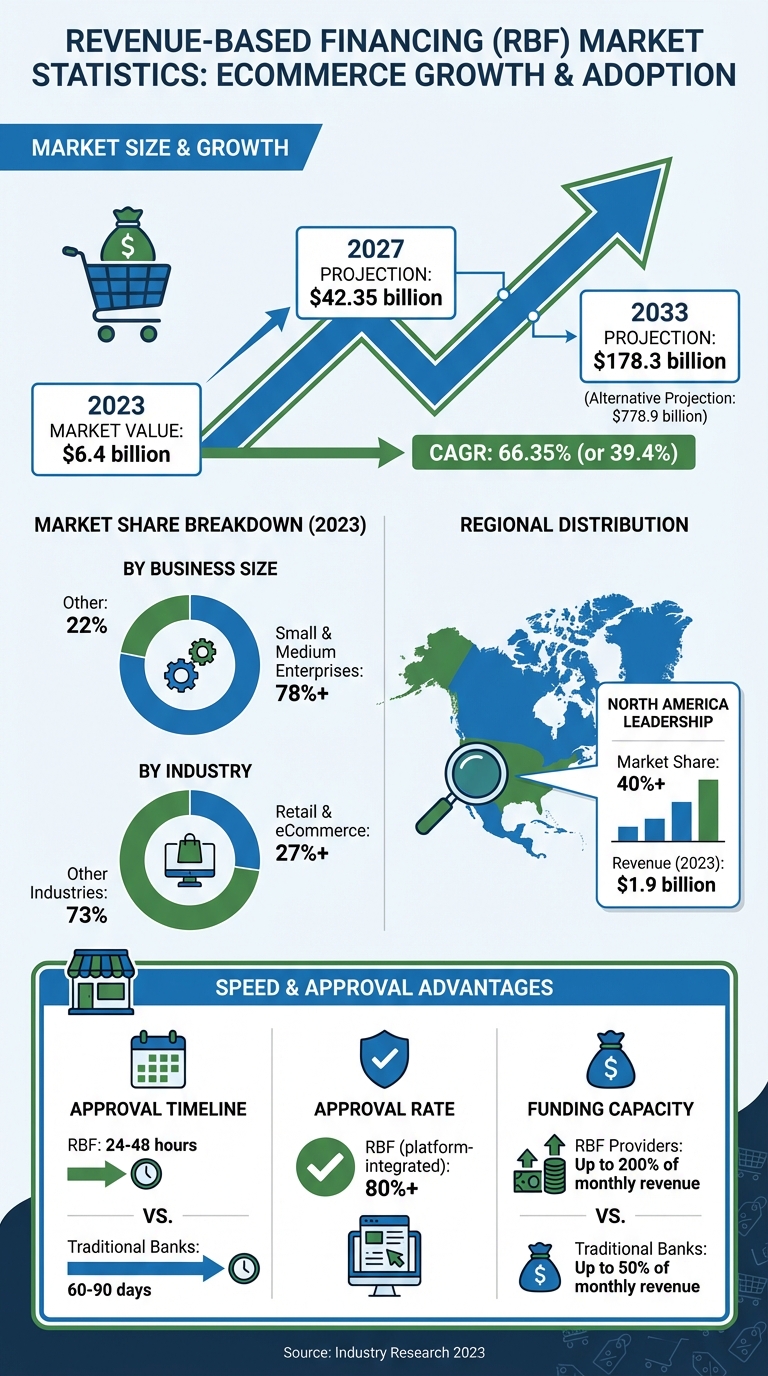

- Market Growth: The RBF market, valued at $6.4 billion in 2023, is projected to hit $178.3 billion by 2033, driven by eCommerce and small businesses.

With advancements in AI, platform integrations, and global expansion, RBF is becoming a preferred option for eCommerce sellers looking to fund inventory, marketing, or channel expansion. It’s a practical solution for businesses needing fast, scalable capital without the constraints of traditional financing.

How to get Revenue-based Financing for your Shopify Store?

sbb-itb-d7b5115

The Current State of Revenue-Based Financing in eCommerce

Revenue-Based Financing Market Growth and Key Statistics for eCommerce 2023-2033

Revenue-based financing (RBF) has transformed from a niche concept into a widely-used funding method for eCommerce businesses. The numbers speak for themselves: in 2023, small and medium enterprises dominated the RBF market, holding over 78% of the market share. Retail and eCommerce made up more than 27% of total RBF usage[4]. North America leads the charge globally, capturing more than 40% of the market and generating $1.9 billion in revenue during the same year[4].

Why eCommerce Sellers Choose RBF

RBF stands out by eliminating the need for traditional collateral and lengthy documentation processes. Providers use API integrations to connect directly with platforms like Shopify, Amazon, and Stripe, enabling them to analyze real-time metrics such as Return on Ad Spend (ROAS) and Customer Acquisition Cost (CAC)[3]. This streamlined approach allows for approvals in just 24–48 hours, compared to the 60–90 days typically required by banks[3]. Some providers even report approval rates exceeding 80%[3].

"Banks generally require physical collateral... Most ecommerce brands lack these assets, and their value lies in digital presence, customer lists, and inventory." – Nicole Cruz, Redline Capital[3]

The flexibility of RBF makes it even more attractive. While traditional banks limit loans to 50% of monthly revenue, RBF providers can offer up to 200%[3]. Repayments adjust based on sales, easing the burden during slower months and scaling up during busy seasons. Founders also retain full ownership and control, avoiding the lengthy due diligence and board oversight that come with venture capital funding[8].

These advantages have driven widespread adoption, supported by the numbers outlined below.

Market Growth and Adoption Data

The RBF market is growing at an impressive compound annual growth rate of 66.35%[4]. In 2023, valuations ranged between $4.8 billion and $6.4 billion, with projections suggesting the market could hit $42.35 billion by 2027 and potentially reach $778.9 billion by 2033[4][8]. This rapid growth underscores how well revenue-based financing aligns with the fast-moving, cash flow–dependent nature of eCommerce.

How Revenue-Based Financing Works for eCommerce Businesses

Revenue-based financing (RBF) adjusts your repayments based on your actual sales. Providers automatically deduct a set percentage of your daily or weekly revenue until the total funding amount is repaid. This means payments are higher during busy periods, like the holiday season, and lower during slower months, offering a flexible repayment structure that aligns with your cash flow [1].

To get started, you connect your eCommerce platform (such as Shopify, Amazon, or TikTok Shop) and payment processors (like Stripe) to the lender's portal. This allows the lender to analyze your real-time sales data and provide a funding offer, typically within 24 to 72 hours. Once approved, the agreed-upon repayment percentage is automatically deducted from your business bank account or payment processor [1].

"Repayments move with your sales... this means repayments are lighter during slow periods and speed up during high-demand seasons."

– Shabnam Mansukhani, CrediLinq [1]

The repayment continues until you reach a cap, generally between 1.08x and 1.3x of the original funding amount, though some agreements may go as high as 3.0x. Instead of compounding interest, RBF charges a flat fee - usually 6–12% of the funding. The actual cost depends on how quickly you repay, with effective annual rates ranging from 40% to 350% [1].

Core Features of RBF

Funding amounts typically range from 150% to 200% of your monthly revenue. Some providers may cap funding at one-third of your annual recurring revenue or up to seven times your monthly recurring revenue. The repayment percentage - your share of daily or weekly sales - usually falls between 1% and 25% of your monthly revenue. While this percentage stays fixed, the actual dollar amount adjusts based on your sales performance.

This structure helps maintain cash flow during slower months while allowing for faster repayment during peak seasons. For example, if your November sales triple compared to March, your repayment amount also triples, helping you pay off the funding sooner. On the flip side, lower sales mean smaller repayments, giving you breathing room without penalties.

Most RBF agreements don’t require personal guarantees or physical collateral, such as real estate or equipment. However, many providers file a UCC-1 blanket lien against your business assets. This could limit your ability to secure additional financing until the RBF is fully repaid. Be sure to check your contract for any "weekly minimum repayment floors", which could override the flexible repayment structure and turn your RBF into a fixed-payment plan during slower months [1].

This adaptability is one of RBF's standout features compared to traditional loans.

RBF vs. Other Financing Options

To decide if RBF is the right fit, it's helpful to compare it with other financing options like merchant cash advances and traditional bank loans. Each option has its pros and cons in terms of cost, flexibility, and approval process.

| Feature | Revenue-Based Financing | Merchant Cash Advance | Traditional Bank Loan |

|---|---|---|---|

| Repayment Structure | Percentage of daily/weekly revenue | Fixed daily debit or percentage with floors | Fixed monthly installments |

| Cost | Flat fee (6–12%); effective APR 15–60%+ | Factor rate (e.g., 1.2x–1.5x) | Interest rate (8–15%) |

| Collateral Required | None (revenue-linked) | None (purchase of future sales) | Physical assets often required |

| Approval Speed | 24–72 hours | 1–3 days | 6–8 weeks |

| Payment Flexibility | High; adjusts with sales | Moderate; may include minimums | Low; fixed regardless of sales |

| Ownership Impact | No equity dilution | No equity dilution | No equity dilution |

The main advantage of RBF is its flexibility. While merchant cash advances often include minimum payment requirements that can strain your cash flow, and traditional bank loans may offer lower interest rates but demand collateral and long approval times, RBF provides faster access to funds with repayment terms that scale with your sales. This makes it particularly appealing for eCommerce businesses that experience fluctuating revenue throughout the year.

Key Benefits of Revenue-Based Financing for eCommerce

Revenue-based financing (RBF) offers eCommerce businesses three standout advantages: repayments that adjust to your sales, quick access to funds, and flexible capital that supports growth - all while safeguarding your ownership and personal assets.

Repayments That Align with Your Sales

One of the biggest perks of RBF is how repayments adjust to your revenue cycle. Instead of a fixed monthly payment, you repay a set percentage of your daily or weekly revenue - usually between 5% and 20% [5]. This means when sales peak, like during the holiday season, you pay down your balance more quickly. On the flip side, during slower months, smaller repayments help you maintain cash flow for essential needs.

You continue these payments until you hit a predetermined cap, typically 1.2× to 3× the original funding amount [6]. Unlike traditional bank loans with rigid schedules, RBF offers a repayment structure that moves in step with your business, making it easier to manage the natural ups and downs of eCommerce cash flow.

Rapid Access to Funds

Speed matters in eCommerce, and RBF delivers. Most providers can fund businesses within 24 to 72 hours by tapping into real-time sales data from your eCommerce platforms and payment processors [5]. This efficient process eliminates the need for tax returns, business plans, or extensive credit checks.

Additionally, RBF agreements usually don’t require personal guarantees or collateral, meaning your personal assets stay protected, and you retain full ownership of your business. With the eCommerce segment of the RBF market growing at an estimated 61.8% annually, most providers look for businesses with at least six months of trading history and monthly revenues between $10,000 and $20,000 [5]. This fast access to capital helps sellers capitalize on growth opportunities without delay.

Flexible Support for Growth

RBF is designed to fuel high-impact, quick-return initiatives. Many eCommerce sellers use it to stock up on inventory before busy seasons, scale successful marketing campaigns, or expand to new sales channels - activities that generate revenue quickly enough to cover repayments with ease.

Unlike traditional loans, which often come with restrictions on how you can use the funds, RBF offers flexibility. You can allocate the money toward inventory, advertising, or even hiring seasonal staff. Funding amounts typically range from 1 to 2 times your monthly revenue, with a transparent fee structure - usually a flat fee between 6% and 12%, avoiding compounding interest [1]. While the effective APR can range from 15% to 60%, depending on how fast you repay, the clear costs and fast funding make RBF a practical choice for eCommerce sellers looking to grow while managing unpredictable cash flow.

Emerging Trends in Revenue-Based Financing

Revenue-based financing (RBF) is evolving quickly, thanks to advancements in artificial intelligence, tighter integration with eCommerce platforms, and expansion into new global regions. These developments are making RBF faster, smarter, and more accessible for businesses worldwide. By building on its existing strengths, RBF is becoming an even more effective way to meet the dynamic demands of eCommerce.

AI and Real-Time Data in Lending Decisions

Artificial intelligence is reshaping how RBF providers assess risk and approve funding. Instead of just relying on traditional financial statements, newer RBF models incorporate real-time data from sources like sales, inventory, and marketing performance. Tools like Apache Kafka and Amazon Kinesis make it possible to analyze this data instantly, enabling funding decisions based on live insights [10].

According to industry research, 70% of eCommerce decision-makers consider real-time data analytics "very important" or "critical" to their operations, and 42% plan to increase their investment in these tools within the year [10]. Businesses that adopt real-time data solutions are expected to outperform competitors by 30% in revenue growth and operating margins by 2025 [10].

"Real-time data is absolutely critical for online retailers today. It's not just about reacting quickly, but predicting and getting ahead of where the market is going."

- John Smith, eCommerce Industry Analyst, Gartner [10]

This approach allows RBF providers to dynamically adjust credit limits or repayment terms based on factors like marketing campaign performance or inventory turnover. To make the most of this trend, eCommerce businesses should focus on maintaining high-quality data, using robust validation processes to ensure accuracy and consistency for lenders [10].

Integration with eCommerce Platforms

RBF providers are increasingly integrating directly with platforms like Amazon, Shopify, and TikTok Shop, simplifying the funding process. These integrations eliminate the need for traditional paperwork, such as tax returns or business plans, by using platform-native data like revenue, order volume, and customer behavior to assess eligibility [3][5]. Pre-approved funding offers can even appear directly in merchants' dashboards, cutting down on application time and effort [2][3].

Automated repayment systems, which deduct a fixed percentage of daily sales through the platform's payment gateway, further streamline the process [5][6]. This commerce-based underwriting approach shifts the focus from personal credit scores to metrics that matter more for eCommerce, like Return on Ad Spend (ROAS) and Customer Acquisition Cost (CAC) [3][9]. Notably, over 80% of businesses applying through these data-integrated platforms receive approval [3].

For sellers, keeping accurate and consistent data across platforms is crucial. This includes maintaining clean sales reports, refund logs, and ad performance metrics. These integrations not only make funding more accessible but also set the stage for RBF to expand into new markets and industries.

International Markets and Niche Specialization

With advancements in technology and platform integration, RBF is expanding into international markets and targeting specialized niches. The Asia-Pacific region is poised for significant growth, driven by a thriving entrepreneurial ecosystem and the increasing availability of RBF for small and medium enterprises (SMEs) [11]. The global RBF market, valued at $6.4 billion in 2023, is projected to reach $178.3 billion by 2033, growing at a compound annual growth rate (CAGR) of 39.4% [11].

In October 2023, Uncapped, a U.K.-based provider, secured a $216.32 million debt facility from Fortress Investment Group to extend its RBF offerings to entrepreneurs in the U.S. and Europe [11]. Meanwhile, new players like Erad in Riyadh are entering the market, offering Shariah-compliant working capital to online businesses, SaaS companies, and restaurants using data-driven assessment models [12].

"RBF is already well-established in the U.S. and U.K., and it's gaining traction in Germany and across Europe."

- re:cap [13]

Providers are also focusing on niche markets to better serve specific business types. For example, Jenfi in Singapore caters to digital-native businesses and startups in Southeast Asia, while Viceversa in Milan combines RBF with tailored marketing insights for European SaaS companies and marketplaces [12]. This expansion into new regions and specialized sectors ensures that more eCommerce sellers can access flexible, equity-free funding options tailored to their unique needs, all while maintaining a data-driven approach that aligns with fluctuating cash flows.

How eCommerce Businesses Use Revenue-Based Financing

Revenue-based financing (RBF) has become a go-to option for eCommerce sellers tackling growth challenges. Its flexible repayment terms make it an ideal solution for needs like stocking up for the holidays, launching ad campaigns, or expanding to new sales channels. Here’s how sellers are putting RBF to work.

Buying Inventory for Peak Seasons

For many eCommerce brands, the winter holiday season can account for as much as 50% of their yearly sales [14]. The catch? Inventory orders need to be placed months ahead - often in August or September - to ensure stock is ready for the Q4 shopping frenzy. This gap between spending and revenue can put sellers in a tough spot financially.

RBF offers a quick fix by delivering funds within 24–72 hours [5]. This fast access to capital allows sellers to secure supplier deals or lock in production timelines before the holiday rush clogs supply chains. Plus, the repayment terms align with seasonal sales patterns: payments increase during high-revenue months like November and December and slow down in quieter months like January and February [5][2].

To avoid scrambling at the last minute, plan your working capital needs early - ideally by August [14]. It’s also smart to keep inventory and ad spend separate when planning finances. Inventory often takes 60 to 120 days to convert into cash, while ad spend typically cycles in 14 to 30 days. Using RBF for each independently ensures smoother cash flow [5].

Funding Marketing and Advertising

Scaling an ad campaign that’s already performing well often requires extra cash. Platforms like Meta and Google Ads may deliver great returns, but sellers may not have enough funds to increase daily budgets during critical periods, such as product launches or holiday peaks. RBF steps in to cover the 14 to 30-day cash conversion cycle typical of digital advertising, where expenses are paid upfront, but revenue comes later [5].

The key is to use RBF strategically - focus on campaigns that are already delivering strong returns rather than pouring money into untested or underperforming efforts. Many modern RBF providers integrate with advertising platforms and analytics tools, helping sellers identify where their ad dollars will go the furthest [5].

When planning, map out your cash flow for the next 180 days to ensure that daily revenue share deductions (typically 10–20%) don’t disrupt your ad budget [5]. Thomas Bishop, a Trustpilot reviewer, shared a cautionary tale:

"Sales team was great, Ops team was terrible. They pulled funds far faster than the contract stated, thereby increasing the effective interest rate significantly" [5].

This highlights the importance of understanding how automated repayments can impact your daily operations.

Beyond inventory and advertising, RBF also supports eCommerce sellers looking to diversify their sales channels.

Expanding Across Multiple Sales Channels

Expanding from one sales channel to several - like adding Amazon or Walmart to a Shopify store or venturing into TikTok Shop - requires upfront investments. These might include listing fees, extra inventory, channel-specific marketing, and new fulfillment arrangements. RBF providers often use platform-based underwriting to evaluate real-time sales across multiple channels, including Amazon, TikTok Shop, Shopify, eBay, and Walmart [1][5][7].

This approach allows sellers to diversify revenue streams without draining the cash needed for day-to-day operations. The repayment flexibility is especially useful since different sales channels often have varying sales patterns. For example, a seller might see strong Q4 performance on Amazon but notice their Shopify store peaks during a spring launch. RBF adjusts to the combined revenue flow instead of enforcing fixed monthly payments.

That said, daily auto-debits can create cash flow challenges, especially while waiting for sales from new channels to materialize. Carefully review contracts for clauses like "weekly minimum floors" or UCC-1 blanket liens, which could limit your ability to secure additional financing in the future [5].

Conclusion

With its adaptable structure and quick funding process, Revenue-Based Financing (RBF) has become a key tool for driving eCommerce growth. Unlike traditional loans with fixed payments or equity financing that requires giving up ownership, RBF aligns repayments with your revenue cycle. This approach helps safeguard cash flow while offering the capital needed to stock inventory, ramp up advertising, or enter new marketplaces.

In 2023, the global RBF market was valued at $6.4 billion, and it's expected to soar to $178.3 billion by 2033 [8]. This rapid growth highlights a shift in how eCommerce entrepreneurs approach funding - favoring speed, flexibility, and maintaining control over the rigid terms of traditional financing. As Mayur Toshniwal from Qubit Capital aptly states:

"Revenue based financing sits in that sweet spot between loans and equity: you get growth capital without surrendering control, and repayments flex with your actual revenue instead of a bank's calendar" [8].

Onramp Funds offers working capital within 24 hours, with repayment terms that adjust to your daily sales. Whether you're gearing up for Q4, scaling a successful ad campaign, or branching out into new sales channels, the platform connects directly to your storefronts, ensuring you get the funding you need, exactly when you need it.

FAQs

How do I know if RBF is affordable for my store?

To figure out if revenue-based financing (RBF) works for your budget, focus on these key points:

- Repayment Terms: Since RBF ties repayment to a percentage of your revenue, make sure the terms align with your store’s cash flow and revenue trends.

- Cash Flow Flexibility: Payments fluctuate based on sales, which can be helpful if your revenue is steady or increasing.

Take a close look at the repayment percentage, terms, and how consistent your store’s revenue is. This will help you decide if RBF is a good financial fit.

What business metrics do RBF providers look at besides revenue?

RBF providers look beyond just revenue when evaluating a business. They dive into key metrics that paint a clearer picture of financial health and growth potential. These include profitability ratios like profit margins, financial KPIs such as net income and ROI, and indicators tied to cash flow, solvency, and liquidity.

By examining details like cash flow statements and debt-to-equity ratios, they can gauge whether the business has the financial stability needed to consistently generate enough revenue for repayment. This thorough analysis helps ensure that the company is well-positioned to meet its obligations.

Will an RBF agreement make it harder to get other financing later?

Revenue-based financing (RBF) agreements generally don’t hinder your ability to secure additional financing down the road. Since these agreements are tied to your revenue and typically don’t require collateral or personal guarantees, they allow you to maintain financial flexibility. This makes RBF an appealing choice for businesses looking for growth capital without compromising future funding opportunities.