Scaling your Shopify brand past $1M in revenue requires smart funding choices to keep up with growing demands. Here’s what you need to know:

- Common Challenges: Cash flow issues from bulk inventory purchases, rising marketing costs, and seasonal revenue dips.

- Funding Options:

- Revenue-Based Financing (RBF): Flexible repayments tied to sales, ideal for inventory and marketing.

- Inventory Financing: Secured loans to fund stock purchases, with inventory as collateral.

- Bank Loans and Lines of Credit: Lower rates but slower approval and stricter requirements.

- Key Considerations: Match funding type to your business needs, assess total costs, and ensure repayment aligns with expected returns.

Pro Tip: Combine funding sources for maximum flexibility - use RBF for short-term growth and loans for long-term investments.

Identifying Your Funding Needs as a Scaling Shopify Brand

Cash Flow Challenges for $1M+ Shopify Brands

Hitting $1 million in revenue is a huge milestone, but it also brings a new set of cash flow challenges. A big one? Inventory. To get better supplier pricing, you often need to place larger bulk orders, which ties up cash for months. And if stock runs out, you risk losing sales momentum and damaging customer trust.

Marketing is another area where cash flow gets tricky. You’re spending heavily on Facebook ads, influencer partnerships, or SEO campaigns today, but the revenue those efforts generate often takes weeks - or even months - to roll in. Add seasonal slowdowns to the mix, where revenue dips but fixed costs like rent and payroll stay the same, and liquidity can get tight fast. On top of that, external factors like rising supplier costs or shipping delays can drain your cash reserves without warning [3].

These challenges highlight the shifting financial priorities that come with scaling a brand.

Main Expenses When Scaling Your Business

As your Shopify brand grows, your spending patterns change dramatically. Inventory becomes one of the biggest drains on capital. You’re not just restocking existing products - you’re expanding your offerings and placing larger orders to unlock volume discounts. For instance, Jordan Lee, owner of The Public Pet, used funding to add new products to their inventory, which boosted revenue by 40% to 50% [4].

Marketing and customer acquisition costs also rise sharply. To grow beyond $1 million, you’ll likely need to ramp up ad spend, roll out referral programs, and invest in content marketing - all of which require cash upfront, often long before you see the returns. Operationally, scaling means upgrading your tech stack, hiring more staff to handle increased order volumes, and keeping up with higher fulfillment and shipping costs [3][4].

How to Assess Your Funding Requirements

To figure out how much funding you need, start by identifying your biggest bottleneck. Is inventory running out and capping your sales? Are your marketing efforts struggling to reach more customers? Or is outdated technology slowing down your fulfillment process? Pinpointing the root issue will help you decide whether inventory financing, a term loan, or another funding option is the right fit. For example, inventory financing works well for brands dealing with stockouts, while a term loan might be better for expanding infrastructure to support growth [1].

Next, evaluate how much debt your business can handle. Revenue-based financing typically takes 1% to 25% of your monthly revenue for repayment [2]. Run an ROI analysis to ensure the revenue boost you’re expecting will outweigh the cost of borrowing. Shopify staff offer this wise reminder:

"Money can solve problems, but there's always a cost to debt. It might sound obvious, but taking money without a real plan to pay it back could lead to more problems." [1]

Finally, think about your sales ecosystem. Some funding options rely solely on your Shopify sales data, while others consider revenue from all your channels, like Amazon or Walmart. This difference can impact both the amount of funding you qualify for and how repayments are structured [6].

Revenue-Based Financing for Shopify Sellers

How Revenue-Based Financing Works

Revenue-based financing (RBF) links your repayment directly to your sales. Instead of fixed monthly payments, you repay a percentage of your revenue - known as the remit rate - which typically ranges from 1% to 25%, depending on your business profile and the lender [2]. When your sales are strong, you pay more; when they slow down, your payments automatically decrease. This makes RBF particularly appealing for eCommerce brands with seasonal sales patterns or unpredictable growth.

The total repayment amount is set by a repayment cap, usually between 1.2 to 3 times the original funding amount [2]. For example, if you receive $100,000 with a 1.5× cap, your total repayment would be $150,000. Unlike traditional loans, RBF uses a flat fee structure, with payments deducted daily or weekly based on your sales [2][6].

A key difference between Shopify Capital and specialized RBF providers is how they assess your revenue. Shopify Capital focuses solely on your Shopify store sales, while other RBF providers consider your entire sales ecosystem, including platforms like Amazon, Walmart, and TikTok Shop [6]. For Shopify brands operating across multiple channels, this broader view often results in more accurate funding options. This setup lays the foundation for several advantages discussed below.

Benefits of Revenue-Based Financing

RBF has several advantages when compared to traditional funding. For starters, it’s equity-free, meaning you keep 100% ownership of your business without giving up board seats or control [2]. Plus, you won’t need to pledge personal assets like your home or car as collateral, reducing personal financial risk [2]. Another major perk? The funding process is fast - often completed in as little as 24 hours to a few weeks - unlike the lengthy timelines associated with bank loans or venture capital [2][6].

The flexible repayment structure is another standout feature. It helps protect your cash flow during slower sales periods, minimizing the risk of financial strain. Additionally, the RBF market is expected to grow significantly - from $6.4 billion in 2023 to $178.3 billion by 2033 [2]. This growth highlights its increasing importance as a funding solution for eCommerce businesses.

These benefits make RBF an attractive option for many entrepreneurs, but it’s worth carefully evaluating whether it aligns with your specific business goals.

Is Revenue-Based Financing Right for Your Business?

With its flexible structure and clear advantages, RBF can be a smart choice - if it aligns with your business needs. It’s particularly well-suited for brands with steady recurring revenue and high-growth potential. RBF is most effective when the funds are used for revenue-generating activities like purchasing inventory or launching marketing campaigns that help you quickly reach the repayment cap. For brands selling across multiple platforms, working with a provider that considers all your sales channels can maximize the benefits.

Before signing on, calculate the total cost by multiplying your funding amount by the repayment cap, and compare it to traditional loan rates. For example, as of May 2025, the maximum fixed interest rate for a U.S. Small Business Administration 7(a) loan of $25,000 or less was 15.5% [2]. While RBF might cost more over the long term, its speed, flexibility, and lack of collateral requirements often outweigh the higher expense for growth-focused brands.

That said, RBF isn’t ideal for every business. It’s generally not a good fit for pre-revenue companies or those with highly inconsistent sales, as offers are based on historical revenue. Additionally, it’s less suitable for covering long-term operational expenses, as the daily or weekly deductions work best when tied to revenue-generating activities.

Inventory and Purchase Order Financing for Product Growth

How Inventory Financing Works

Inventory financing is a type of secured loan or line of credit designed to help businesses purchase finished goods or raw materials. The inventory itself acts as collateral, meaning lenders can seize it if you default on the loan [8]. While this reduces risk for the lender compared to unsecured loans, it does put your inventory on the line.

Typically, lenders will only fund a percentage of the total inventory cost [8]. There are two main options: term loans, which provide a lump sum with fixed repayment terms, and lines of credit, which offer revolving funds where you only pay interest on the amount you actually use [8]. Some lenders also offer revenue-based repayment, where a percentage of daily sales is deducted - this can be helpful for managing seasonal cash flow fluctuations [4].

To secure inventory financing, you'll need to present detailed documentation. This includes inventory valuations, profit and loss (P&L) statements, sales forecasts, and supplier estimates covering at least six months [8]. Keep in mind, lenders are unlikely to finance perishable goods like food ingredients; they typically require collateral that’s stable and retains its value over time [8].

This type of financing strengthens your purchasing power, much like purchase order financing, which helps you fulfill customer orders without draining your cash reserves.

Benefits of Purchase Order Financing

Purchase order financing is a practical solution when you need funds to fulfill a large customer order but lack the upfront capital [9]. It’s particularly valuable for avoiding stockouts, which can lead to lost sales and damage customer relationships [9].

Cash flow problems are a major hurdle for small businesses - 82% of failures stem from these issues, according to one study [9]. For Shopify brands earning over $1 million annually, inventory financing can unlock bulk purchase discounts, improve profit margins, and support seasonal demand spikes. It also allows for the introduction of new product lines without exhausting your working capital [1][8]. Like revenue-based financing, the right inventory funding choice can create the cash flow flexibility needed for sustained growth.

When to Use Inventory Financing

Inventory financing works best in specific scenarios where it can have a big impact. For instance, if a product suddenly goes viral and your cash flow can’t keep up with demand, this type of funding can help. It’s also useful during seasonal peaks when you need to stock up ahead of time or when launching new product lines after development costs have stretched your budget [8].

Before committing, ensure any bulk discounts from wholesalers outweigh the total interest and fees involved [8]. Compare options from banks, credit unions, and online lenders to find the best fit in terms of interest rates, speed of funding, and repayment terms [8]. Online lenders may provide funds within a day, while traditional banks could take weeks - decide whether the faster access is worth the potential trade-off of higher rates [8].

For larger, long-term investments like a major product launch requiring extended repayment (e.g., 12 months), a term loan is often the better choice [1]. On the other hand, lines of credit are ideal for short-term cash flow gaps or unexpected expenses [1][10].

Business Loans and Lines of Credit: Pros and Cons

For Shopify brands surpassing $1M in revenue, traditional bank loans remain a financing option worth exploring alongside newer funding methods.

Overview of Bank Financing Options

Traditional bank financing generally falls into three main categories:

- Term loans: These provide a lump sum that’s repaid on a fixed schedule, with interest rates ranging from 11.5% to 16.5% [12]. Term loans are best suited for major, one-time investments, like purchasing a warehouse or entering a new market [13].

- Business lines of credit: These act as revolving credit lines with a set limit. You withdraw funds as needed and only pay interest on the amount you use [5]. Once repaid, the credit limit resets, making this option particularly useful for managing short-term cash flow gaps or seasonal fluctuations.

- SBA loans: The 7(a) program is a standout, offering government-backed financing up to $5 million with capped interest rates [13]. For example, as of May 2025, the maximum fixed rate for an SBA 7(a) loan of $25,000 or less is 15.5% [11]. While SBA loans offer competitive terms, they involve extensive documentation and a slower approval process, often taking weeks or even months [12][13].

Now, let’s weigh the pros and cons of traditional bank loans for established businesses.

Pros and Cons of Bank Loans

Bank loans come with clear advantages but also notable challenges.

On the plus side, traditional banks typically offer lower interest rates, particularly for businesses with strong credit histories and proven profitability [1]. Banks can also provide access to financial expertise and accommodate larger capital needs for significant growth projects.

However, the downsides include stringent qualification requirements. Banks often demand strong personal and business credit scores, detailed financial statements, and may require collateral or personal guarantees [1]. The application process is lengthy - often taking weeks or months - which can be a drawback for fast-moving eCommerce brands.

Another limitation is the potential for debt covenants, which may restrict your ability to secure additional funding, thereby reducing operational flexibility [1]. In Q3 2023, only 21% of small businesses sought loans from banks or credit unions, partly because approval rates remain selective [12].

| Feature | Traditional Bank Loan | Business Line of Credit | Revenue-Based Financing |

|---|---|---|---|

| Best For | Long-term investments, equipment | Short-term cash flow, payroll | Inventory, marketing, growth |

| Repayment | Fixed monthly payments | Interest only on drawn amount | Percentage of daily sales |

| Speed | Slow (weeks to months) | Fast (once established) | Very fast (24–72 hours) |

| Cost | Lower interest rates | Low if repaid quickly | Higher "factor" cost |

| Collateral | Often required | May be required | Usually none |

With these considerations in mind, traditional financing options stand in contrast to faster alternatives like revenue-based funding.

When Bank Financing Makes Sense

Understanding the pros and cons helps clarify when bank financing aligns with your business needs.

Bank loans are ideal for long-term investments with clear returns, such as purchasing manufacturing equipment, opening a retail location, or securing a warehouse mortgage. Term loans, with their predictable fixed payments, simplify financial planning for these large-scale projects [1][13]. For commercial real estate, banks often require a 20% to 30% down payment [13].

On the other hand, lines of credit are better suited for managing short-term cash flow needs. It’s wise to arrange a line of credit during times of financial stability - even if you don’t need the funds immediately - so you’re prepared for unexpected downturns or seasonal dips [12]. Lines of credit are particularly helpful for covering payroll, managing marketing expenses, or restocking inventory [14].

If possible, consider bundling your business loan with other banking services, such as a commercial mortgage. This strategy may help you negotiate lower interest rates [1][5]. Always review loan agreements carefully, especially for clauses that could limit your ability to secure additional working capital as your business grows [1].

sbb-itb-d7b5115

Combining Different Funding Sources for Growth

For many Shopify brands scaling beyond $1 million, relying on just one funding source often falls short. Instead, a blended approach - mixing revenue-based financing with inventory loans or lines of credit - can offer the flexibility needed to fuel growth while keeping cash flow in check.

Using Revenue-Based Financing with Inventory Solutions

Once brands explore individual funding options, they often discover that combining them creates the best path to growth. Revenue-based financing (RBF) is particularly effective for initiatives like digital advertising, where increased sales can accelerate repayment [2]. On the other hand, for inventory purchases with longer turnover cycles (e.g., 12 months), term loans or lines of credit with lower interest rates are a better fit [10].

This strategy allows businesses to use RBF for short-term growth drivers, such as marketing, while reserving traditional loans for larger, one-time investments. The secret lies in matching the funding type to the asset's lifecycle: RBF works well for quickly moving inventory, while fixed-payment loans suit assets with longer turnover periods [10]. This balance helps businesses maintain agility while supporting their broader operational goals.

Managing Multiple Funding Sources

Juggling multiple funding sources requires careful oversight, especially when it comes to debt covenants that might limit additional borrowing [10]. It’s essential to review existing contracts for clauses that could trigger defaults when you secure new financing. Additionally, calculate the total cost of debt, factoring in fees, repayment caps (typically 1.2x to 3x the loan amount for RBF), and remit rates (usually 1% to 25% of monthly revenue). These elements can significantly impact your cash flow and operational liquidity [2].

Case Study: Hybrid Funding Approach

A real-world example highlights how this hybrid strategy can drive growth. Jordan Lee, owner of The Public Pet, used a combination of revenue-based financing and inventory-specific funding to expand his business. This approach allowed him to boost revenue by 40% to 50% while maintaining healthy cash flow [4]. By aligning funding sources with specific needs - like using RBF for marketing and other solutions for inventory - The Public Pet achieved sustainable growth without straining daily operations.

The broader appeal of this approach is reflected in the growth of the revenue-based financing market, which is projected to jump from $6.4 billion in 2023 to $178.3 billion by 2033. This trend underscores the increasing shift toward flexible, fintech-driven funding solutions for eCommerce businesses [2].

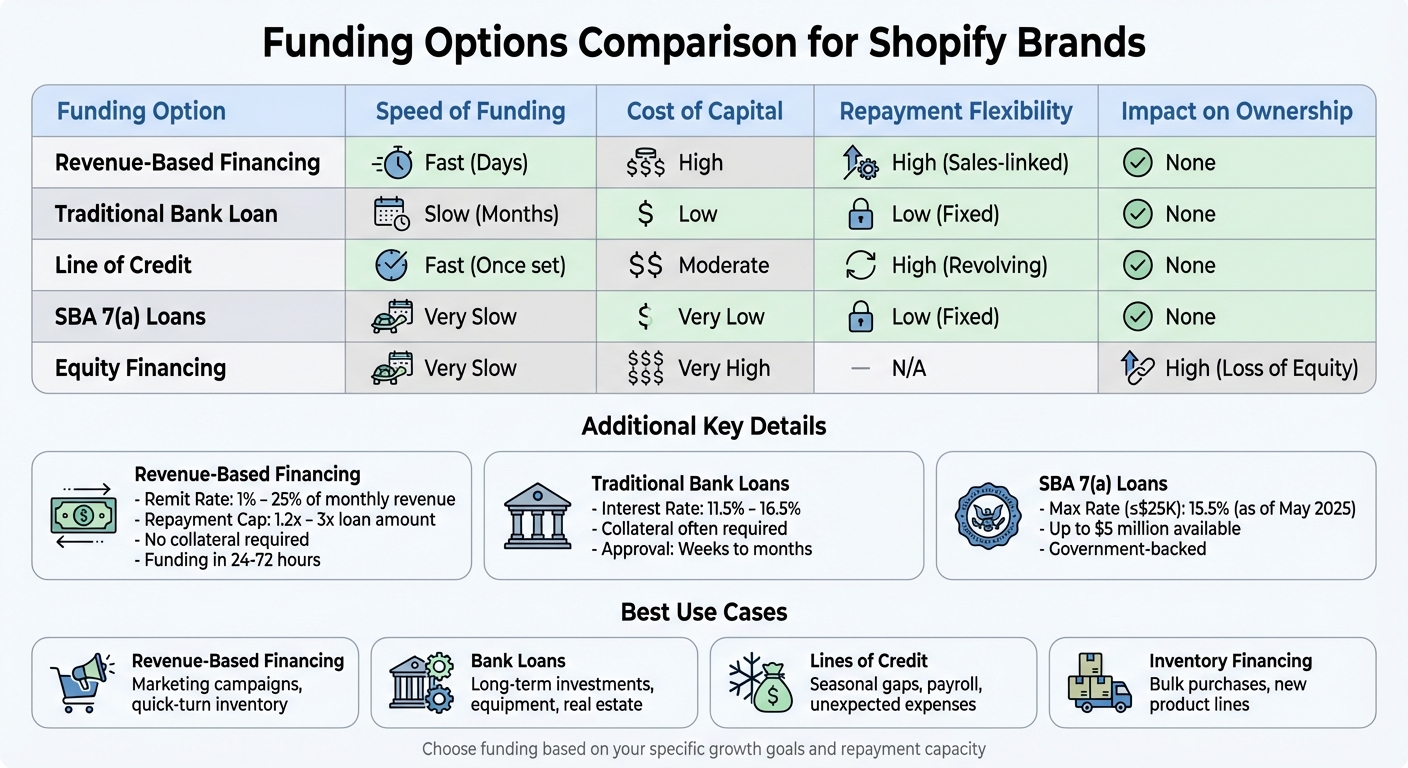

How to Choose the Right Funding Option

Comparison of Funding Options for Shopify Brands Scaling Past $1M Revenue

Factors to Consider When Choosing Funding

Start by determining your total cost of capital, which includes not just the interest rate but also fees and any hidden charges [1][11]. For revenue-based financing, repayment caps typically range from 1.2 to 3 times the initial loan amount, with remit rates (the percentage of monthly revenue dedicated to repayment) usually falling between 1% and 25% [11].

Two key factors to weigh are repayment flexibility and speed of access. Revenue-based financing adjusts repayments based on your daily sales, offering flexibility, while traditional bank loans require fixed monthly payments regardless of how your business is performing [11][4]. If you need funds quickly, fintech solutions can deliver in as little as two business days, whereas traditional bank loans or SBA loans might take weeks or even months [1][4].

Also, be mindful of restrictions tied to the funding. For example, some loans come with debt covenants that limit your ability to secure additional financing. Check if the loan requires personal guarantees or places liens on your business assets [1][11]. If maintaining full control of your business is a priority, equity financing might not be the best choice, as investors often expect a permanent share of your profits, higher returns than lenders, and sometimes even a board seat [11].

Using a Decision Matrix to Compare Options

To simplify your decision, create a comparison matrix that highlights the key aspects of each funding option:

| Funding Option | Speed of Funding | Cost of Capital | Repayment Flexibility | Impact on Ownership |

|---|---|---|---|---|

| Revenue-Based Financing | Fast (Days) | High | High (Sales-linked) | None |

| Traditional Bank Loan | Slow (Months) | Low | Low (Fixed) | None |

| Line of Credit | Fast (Once set) | Moderate | High (Revolving) | None |

| SBA 7(a) Loans | Very Slow | Very Low | Low (Fixed) | None |

| Equity Financing | Very Slow | Very High | N/A | High (Loss of Equity) |

Before committing to any funding option, ask yourself these five critical questions:

- Will this require a credit check that could lower my score?

- Are there restrictions on obtaining additional financing?

- What are the total fees, including penalties for late payments?

- Are there liens or other adverse actions if I default?

- Will I need strong business credit for future funding eligibility? [1]

By answering these questions and comparing the matrix, you can align your funding choice with your business goals.

Matching Funding to Your Business Goals

The right funding option depends on your specific goals and how repayment aligns with your revenue cycles. For instance, revenue-based financing is a great fit for digital marketing campaigns, SEO efforts, and influencer partnerships because repayments scale with the increased sales these activities generate [2][4]. This type of financing also works well for inventory purchases with quick turnover, allowing you to secure bulk discounts without worrying about fixed monthly payments.

For bulk inventory purchases with longer turnover cycles (up to 12 months), term loans or lines of credit with lower interest rates are more appropriate [10]. On the other hand, lines of credit and business credit cards are ideal for managing seasonal fluctuations, unexpected operational expenses, or short-term working capital gaps [5][7].

If you're planning large-scale projects - like opening new locations, expanding into international markets, or upgrading your tech infrastructure - traditional bank loans or equity financing are better suited. These options provide the larger sums and longer repayment terms needed for such initiatives [5][10].

Before committing to any high-cost financing, calculate your return on debt. For example, if you're using revenue-based financing to purchase inventory, ensure the expected revenue increase (e.g., a 40% boost in sales) more than offsets the repayment cap [2][5]. Also, align the duration of your debt with the lifecycle of the asset: use short-term funding for expenses you’ll recover within 30–90 days, and reserve term loans for inventory or projects that may take 6–12 months to yield returns [5].

Conclusion

Reaching beyond $1M in revenue requires funding choices that align closely with your growth objectives. The key is picking an option that supports your operational needs without compromising your momentum.

Consider revenue-based financing if you’re looking for repayment flexibility that adjusts with your sales, helping to maintain cash flow during slower periods. Traditional bank loans might come with lower interest rates, but their fixed payments and drawn-out approval processes could pose challenges. Lines of credit offer a quicker solution for accessing working capital to handle unexpected costs, while equity financing makes sense when you’re seeking strategic partners and are open to giving up a share of ownership.

Be sure to examine the full cost of capital - this includes fees, repayment caps, and any restrictive terms. Most importantly, ensure that the potential revenue growth justifies the expense.

FAQs

What are the key advantages of revenue-based financing for Shopify brands?

Revenue-based financing provides Shopify brands with a fast and hassle-free way to secure funding - often in as little as 24 hours. The best part? You don’t have to give up any equity or ownership in your business.

Repayments are designed to be flexible, automatically adjusting based on your sales. That means during slower months, you won’t be stuck with rigid payment amounts, giving you some breathing room when you need it most.

What makes this financing option particularly appealing is how easy it is to qualify. Instead of relying on traditional credit metrics, approval is tied to your revenue. This makes it an excellent choice for fast-growing eCommerce businesses that want to scale without unnecessary delays or complications.

How can I choose the best funding mix for my Shopify business as it grows?

To figure out the best funding mix for your business, start by clearly defining what the funds are for, how much you need, and when you’ll need it. Are you stocking up on inventory, ramping up your marketing efforts, or focusing on long-term growth initiatives? Once you’ve nailed down your goals, think about how they align with your cash flow. For instance, if your revenue is steady and predictable, revenue-based financing might be a good fit since payments adjust to your sales cycles. On the other hand, traditional loans could be a better choice for bigger, fixed investments.

It’s also important to weigh factors like cost, flexibility, and repayment terms. Many high-growth Shopify brands find that a mix of funding options works best. For example, you could use short-term financing to handle inventory needs, a low-interest loan for major strategic projects, and revenue-based funding to fuel marketing efforts that grow alongside your sales. Striking the right balance between these options can help you build a funding strategy that keeps your cash flow healthy while supporting ongoing growth.

What should I consider when deciding between a bank loan and inventory financing for my Shopify business?

When deciding between a bank loan and inventory financing, several factors should guide your choice. Bank loans generally offer lower interest rates and longer repayment terms, but they often come with stricter requirements. You’ll likely need a strong credit score, collateral, and patience for a lengthy approval process.

Inventory financing, on the other hand, is tied directly to the value of your stock. It’s designed for businesses that need quick access to funds for restocking. Approval is typically faster, and repayment schedules are often linked to your sales, making it a flexible option during busy seasons or periods of high demand.

To make the best decision, think about your cash flow, growth plans, and how quickly you need the funds. The right choice will depend on which option aligns better with your business's needs and timing.