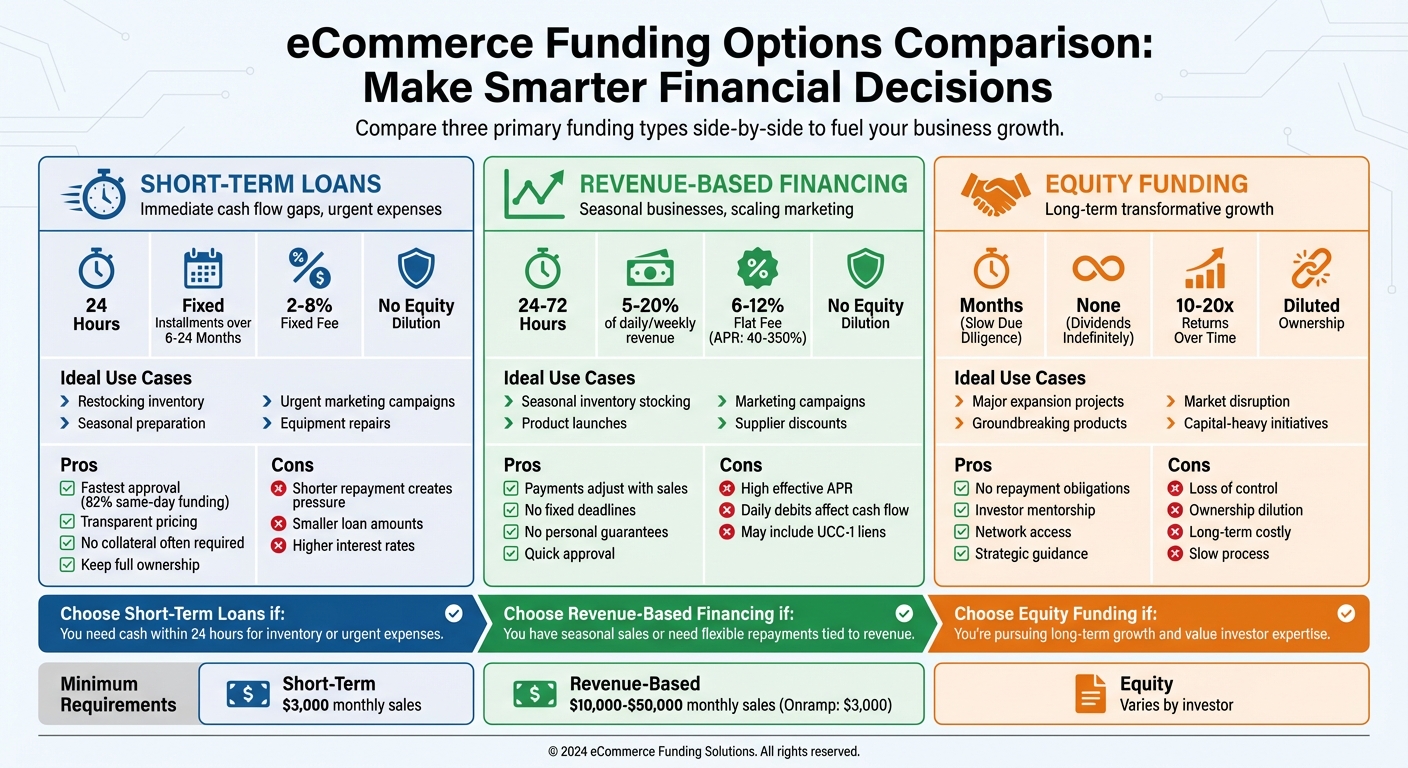

Running an eCommerce business means managing cash flow while navigating seasonal sales, supplier payments, and marketing expenses. Traditional funding options like bank loans are slow and often require collateral, while venture capital has become scarce. For fast, flexible funding, short-term loans and revenue-based financing have emerged as practical solutions.

- Short-term loans: Provide quick cash (within 24 hours) with fixed repayments over 6-24 months. Ideal for restocking inventory or covering urgent expenses.

- Revenue-based financing: Offers repayment flexibility tied to sales performance, adjusting during slow or high-revenue periods. Great for seasonal businesses or scaling marketing efforts.

- Equity funding: Best for long-term growth but requires giving up ownership and control.

Key takeaway: Choose funding that aligns with your needs. For immediate cash flow gaps, short-term loans work well. For scaling during seasonal peaks or launches, revenue-based financing offers flexibility. Equity funding suits major, long-term projects but comes with trade-offs in ownership. Platforms like Onramp Funds provide tailored, equity-free solutions for eCommerce sellers, ensuring quick access to capital without sacrificing control.

eCommerce Funding Options Comparison: Short-Term Loans vs Revenue-Based Financing vs Equity Funding

eCommerce Funding Secrets Every Seller Should Know

sbb-itb-d7b5115

Short-Term Loans for Immediate Funding Needs

Short-term loans are a quick solution for businesses needing immediate cash to stabilize cash flow or cover urgent expenses [8][9]. Unlike traditional bank loans, which can take months to process, online lenders can approve applications in as little as two hours and deposit funds within 4 to 24 hours [8][9]. This rapid funding is especially useful for eCommerce businesses facing time-sensitive needs, like restocking inventory before a busy season or handling unforeseen operating costs. The speed of these loans makes them a practical choice for businesses requiring fast access to capital.

These loans typically operate as installment credit, meaning you repay the borrowed amount plus interest in fixed installments - daily, weekly, or monthly - over a set term, usually 6 to 24 months [9][10]. Importantly, they allow businesses to secure funding without giving up equity, making them a useful tool for addressing immediate needs while maintaining long-term financial control.

Advantages of Short-Term Loans

The standout feature of short-term loans is their speed. For example, about 82% of personal loan applicants at certain fast-funding lenders receive their money the same day they finalize the agreement [7]. For eCommerce sellers, this quick turnaround means being able to seize market opportunities, like purchasing inventory in bulk to lower costs or running time-sensitive promotions [13].

"Short-term loans are the fastest business loans that stabilize your cash flow and meet immediate business needs." – Credibly [8]

Another advantage is their transparent pricing. Onramp Funds, for instance, offers a fixed fee structure ranging from 2% to 8% of the loan amount, with no hidden charges or prepayment penalties. This clarity helps businesses understand the total cost upfront and compare it to their expected returns. Additionally, unlike traditional loans that often require extensive collateral and documentation, short-term loans are often based on real-time sales performance, making them more accessible to eCommerce businesses [13].

Limitations of Short-Term Loans

While short-term loans come with many benefits, they do have limitations. The shorter repayment period - typically under two years - can create repayment pressure, especially if your business struggles to generate enough cash flow during that time [11]. Although the interest rates are higher than long-term loans, the total interest paid may be lower due to the shorter loan term [11].

However, these loans are generally smaller in size, making them less suitable for large-scale projects or long-term investments [11][12]. They’re best used for bridging temporary cash flow gaps, such as covering expenses between placing supplier orders and receiving customer payments, or funding specific activities like seasonal inventory purchases [8][9][11]. Over-reliance on short-term loans can also strain your liquidity, so they should be used thoughtfully [11].

Eligibility Requirements and Common Uses

Eligibility for short-term loans often depends more on your store's real-time performance than traditional credit scores or collateral [13]. For example, Onramp Funds requires a minimum of $3,000 in monthly sales [8]. To speed up approval - often within 24 hours - ensure you have your business documents ready, including bank statements, tax returns, and a government-issued ID [8][9].

These loans are commonly used for situations like seasonal inventory restocking, urgent marketing campaigns, equipment repairs, facility maintenance, or bridging gaps between sales cycles [8][9]. For instance, if you’re preparing for a major sales event and need to stock up on high-demand products, a short-term loan can provide the funds to purchase inventory in bulk, helping you avoid stockouts during peak periods [13].

Revenue-Based Financing: Repayments That Match Your Sales

Short-term loans can provide quick access to cash, but revenue-based financing offers a repayment model tailored to your sales cycles. With this approach, you get upfront capital and repay it using a fixed percentage of your future sales until the total amount, plus a flat fee, is fully paid off [2][4]. Instead of rigid monthly payments, repayments adjust based on your revenue - lower during slow months and higher when business booms. This "pay-as-you-earn" system eliminates the stress of fixed deadlines and traditional interest rates [2].

For eCommerce businesses facing fluctuating sales - like those with seasonal peaks or during new product launches - this flexibility can be a game-changer. You don't have to worry about payments straining your cash flow during slow periods. Plus, this funding method is non-dilutive, meaning you keep full ownership of your business without surrendering equity or board control [14][15]. Companies like Onramp Funds streamline the process by using real-time sales data from platforms like Amazon, Shopify, and Walmart. Often, funding is approved within 24 to 48 hours [2][1].

How Revenue-Based Financing Works

Once approved, the funding amount is determined based on your sales performance. Repayments are taken as a fixed percentage of your daily or weekly revenue - typically between 5% and 20%. This percentage, known as the remittance rate, is automatically deducted from your sales until the principal and flat fee (usually 6% to 12%) are fully repaid [14][15].

Unlike traditional loans that often require strong credit histories or collateral, revenue-based financing focuses on your actual sales performance [14][15]. Onramp Funds, for example, integrates directly with your marketplace accounts to evaluate your business's health in real time, making the process faster and more accessible. Additionally, you won’t have to pledge personal assets or provide personal guarantees, which are common requirements for traditional loans [15][16].

Advantages and Disadvantages of Revenue-Based Financing

One of the biggest upsides of revenue-based financing is its flexibility. Payments grow with strong sales and shrink during slower periods, giving you more breathing room to manage essential expenses like inventory and marketing.

That said, there are some downsides. While flat fees of 6% to 12% may seem reasonable, the effective annual percentage rate (APR) can range from 40% to 350% for businesses experiencing rapid growth [14]. This means that the faster your revenue increases, the higher your annualized costs - a surprising drawback [15]. Additionally, daily or weekly auto-debits can tighten your available cash, and some agreements include minimum payment floors or UCC-1 blanket liens, which can limit your ability to secure other financing later [15].

| Feature | Revenue-Based Financing | Traditional Bank Loan | Merchant Cash Advance |

|---|---|---|---|

| Repayment | % of daily revenue | Fixed monthly installments | Fixed daily debit or % with floors |

| Cost Structure | Flat fee (6–12%) | Compounding interest | Factor rate (1.2×–1.5×) |

| Speed | 24–72 hours | 6–8 weeks | 1–3 days |

| Collateral | Rarely required | Often required | Rarely required |

| Flexibility | High (adjusts with sales) | Low (fixed) | Moderate (often has floors) |

To make this model work, ensure your cash conversion cycle aligns with the repayment schedule. If inventory takes too long to turn into cash, you might end up repaying the loan from existing funds rather than new profits [15]. Also, confirm whether the lender files a UCC-1 lien on your assets, as this can complicate future financing options [15].

Best Situations for Revenue-Based Financing

This type of financing works best for businesses with short-term growth opportunities and quick cash conversion cycles. It's ideal for funding time-sensitive initiatives like stocking up for peak seasons, scaling a marketing campaign, or taking advantage of supplier discounts [15][16]. The repayment structure aligns with the revenue generated by these investments, making it a practical choice for businesses with seasonal sales patterns.

For instance, if you're launching a new product line and need funds for inventory and promotional campaigns, revenue-based financing lets you ramp up spending during the launch and ease off during quieter periods.

Most lenders require a track record of 6 to 12 months of steady revenue and monthly sales of at least $10,000 to $50,000 [14][15]. Onramp Funds, however, has a lower entry point, requiring just $3,000 in monthly sales. That said, it’s crucial to ensure your gross margins can cover both the flat fee and the percentage of daily sales taken for repayment [2][4]. Avoid stacking multiple revenue-based financing deals, as combined daily debits could eat up over 25% of your revenue, creating a cash flow crunch [15].

Equity Funding: Trading Ownership for Growth Capital

Equity funding offers a way to secure significant capital without the need for recurring repayments, making it a strong option for eCommerce businesses focused on long-term growth. Instead of taking on debt, you sell shares of your company to investors in exchange for the funds needed to scale. This approach is particularly suited for startups aiming to expand aggressively or launch groundbreaking products [2][17].

Benefits of Equity Funding

One of the biggest advantages of equity funding is the absence of repayment obligations. Unlike loans that require fixed monthly payments, equity financing allows you to channel all available resources into growth initiatives. This flexibility can be especially helpful for businesses tackling capital-heavy projects [2].

But the benefits don't stop at the funding itself. Equity investors often bring more to the table, including mentorship, industry insights, and access to networks that can help accelerate your business. For companies navigating complex challenges or breaking into new markets, this kind of support can be invaluable [3][6].

Downsides of Equity Funding

The main downside of equity funding is the trade-off in ownership. Selling shares reduces your stake in the company, and selling too much could mean losing majority control [18]. Investors might also seek board representation or other forms of oversight, which could lead to disagreements if their goals don't align with yours [18].

Another consideration is the long-term financial cost. While loans have fixed interest rates, equity investors receive dividends indefinitely. Over time, this could amount to payouts far exceeding the original investment - sometimes 10 to 20 times more [18]. Additionally, investors might pressure you to prioritize short-term profitability, which could mean making tough decisions, like cutting costs or scaling faster than your business can handle [18].

Equity funding also tends to be a slow process. Between due diligence, negotiations, and legal formalities, securing this type of funding can take months. If you're dealing with a time-sensitive opportunity, this delay could be a major drawback [3].

Equity Funding vs. Non-Dilutive Financing

For many eCommerce businesses, non-dilutive financing provides a strong alternative. It offers growth capital without requiring you to give up ownership or control. Here's a quick comparison:

| Feature | Equity Funding | Non-Dilutive Financing |

|---|---|---|

| Control Retention | Partial | Full (founder retains 100% control) |

| Ownership | Diluted (shares are traded for capital) | No dilution (equity-free) |

| Repayment Terms | No fixed repayments; based on eventual exit | Revenue-share or fixed fee that adjusts with sales |

| Funding Speed | Slow (months of due diligence) | Fast (often within 24 hours) |

| Long-term Impact | Includes mentorship and networking | Preserves full ownership and exit value |

| Collateral | None (equity is traded) | Future receivables; no personal guarantees or liens |

For recurring expenses like inventory restocking, seasonal marketing campaigns, or supplier payments, non-dilutive financing is often a better fit [1][5]. Save equity funding for transformative, long-term projects where the strategic guidance of an investor can bring added value beyond just the capital [2].

Choosing the Right Funding for Your Business Goals

Matching Funding Types to Business Situations

When deciding on financing, it's crucial to align the type of funding with your business's specific cash flow patterns and goals. Different funding options suit different needs, and understanding this can make a big difference.

For instance, short-term loans are a great choice when you need quick access to cash for things like restocking inventory. This is particularly helpful if you're aiming to take advantage of supplier discounts or preparing for a major product launch. These loans offer predictable monthly payments and allow you to retain full ownership of your business.

Revenue-based financing, on the other hand, is ideal for businesses experiencing seasonal sales spikes or scaling up marketing efforts. Since repayments are tied to your sales, this model ensures that your cash flow stays manageable even during slower periods. High-margin, fast-growing brands often benefit the most. A great example is the fashion brand Hedoine, which used $50,000 in revenue-based funding in 2019 to fuel social media campaigns, resulting in a staggering 1,106% sales growth in Q1 2020 [6].

For sellers on platforms like Amazon or Walmart, real-time, data-driven advances can be a lifesaver. These advances help cover fulfillment and advertising costs without the delays of traditional bank processes. Similarly, invoice factoring is a practical solution for B2B businesses dealing with 30- to 60-day payment terms. It provides immediate cash without adding debt to your balance sheet.

"Smart ecommerce financing should get you money, but it should also choose the capital structure that matches your business model." - Wise

When evaluating funding options, always calculate the total cost of capital, including origination fees, platform charges, and revenue shares. Make sure the structure allows for flexible payments if your revenue takes a dip.

Next, let’s explore how Onramp Funds can help you grow your eCommerce business.

How Onramp Funds Supports eCommerce Growth

Onramp Funds provides customized funding solutions designed specifically for sellers on platforms like Amazon, Shopify, BigCommerce, WooCommerce, Squarespace, Walmart Marketplace, and TikTok Shop. With Onramp, businesses can access funding within 24 hours, and the cost structure is transparent, ranging from 2% to 8%. Repayments are tied to your sales, meaning payments automatically adjust if your revenue decreases - a huge advantage for businesses with seasonal sales or those experimenting with new marketing strategies.

This funding model is built around the idea of securing growth capital while maintaining control of your business.

Onramp also offers a funding calculator on its website, allowing you to estimate your costs before applying. The platform is designed for businesses generating at least $3,000 in monthly sales and looking to scale inventory, invest in advertising, or bridge cash flow gaps between supplier payments and marketplace payouts. With a dedicated team based in Austin, Onramp provides personalized support to help you align your funding choices with your growth plans - all without giving up equity or control.

Conclusion

Choosing the right funding type depends on your immediate needs and long-term goals. Short-term loans are ideal for urgent cash flow issues, while revenue-based financing works well for scaling and managing seasonal fluctuations. Equity funding can fuel major growth initiatives, but it’s not the best choice for everyday expenses like inventory or advertising. For those needs, non-dilutive financing allows you to maintain full ownership and control of your business.

As mentioned earlier, aligning your repayment structure with your sales cycles is key. Look for funding options that offer flexibility, ensuring payments adjust with your revenue. Also, take the time to calculate the total cost of capital to understand how it will affect your margins and growth before committing to any specific option.

Onramp Funds provides equity-free financing designed to align repayments with your sales performance. Offering quick access to funds and clear pricing, the platform integrates with major eCommerce systems like Amazon, Shopify, and Walmart Marketplace. If your revenue dips, your payments automatically adjust, helping you manage cash flow during market fluctuations.

In the fast-paced world of eCommerce, performance-based funding gives you the ability to scale during growth periods while maintaining stability in slower times. The key to smart funding is securing the right capital when you need it, so you’re always ready to take advantage of new opportunities.

FAQs

How do I choose between a short-term loan and revenue-based financing?

When deciding between these options, think about your cash flow, need for flexibility, and future growth plans.

- Short-term loans provide a lump sum with fixed repayment terms. They’re great for covering specific expenses, like purchasing inventory or handling one-time costs. The predictability of repayments can help with budgeting.

- Revenue-based financing, on the other hand, adjusts your repayments based on your sales. This makes it a good choice if your income varies seasonally or is harder to predict, as it offers more flexibility during slower periods.

If you value predictable terms, a short-term loan might be the way to go. But if your income fluctuates, revenue-based financing could provide the adaptable repayment structure you need.

What’s the real cost of revenue-based financing if sales grow fast?

The cost of revenue-based financing (RBF) during periods of rapid sales growth hinges on two main factors: the repayment percentage and the repayment cap, which usually ranges from 1.1x to 1.5x the original funding amount. When sales grow quickly, monthly repayments rise accordingly. This can result in higher overall costs compared to traditional fixed-interest loans. While RBF provides the advantage of payments that scale with revenue, rapid growth can substantially increase the total cost of capital over time.

Will taking funding limit my ability to get future financing?

Taking funding doesn't have to restrict your future financing options - in fact, it can sometimes open new doors when handled carefully. Flexible choices like revenue-based financing adjust as your business expands, offering room to grow. On the other hand, traditional loans or equity funding might affect future opportunities by adding debt or reducing ownership stakes. The key is to choose funding that aligns with your long-term vision, helping you maintain adaptability and ensuring your business can scale effectively in the ever-changing world of eCommerce.