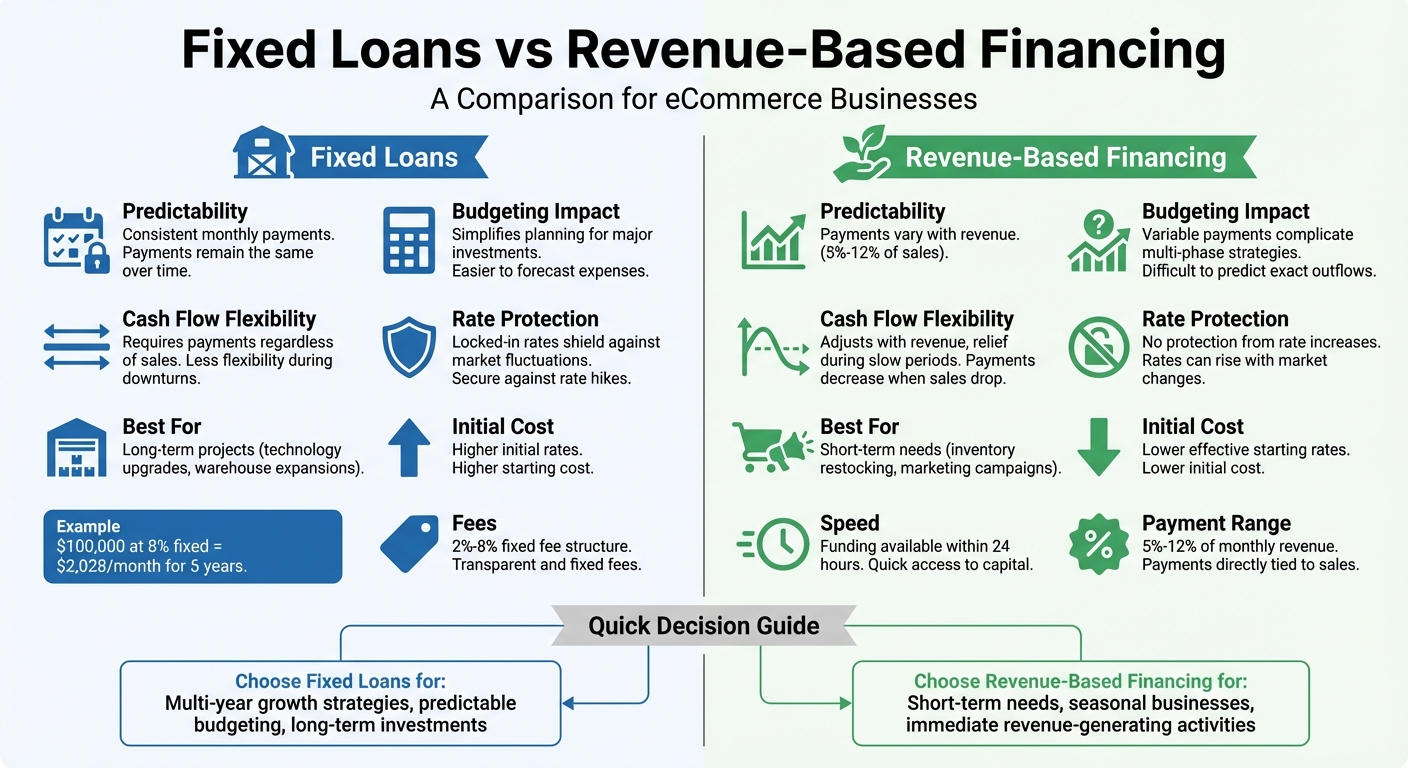

Fixed loans are a reliable choice for businesses planning long-term growth. They offer predictable monthly payments and locked-in interest rates, making financial planning easier. For example, borrowing $100,000 at an 8% fixed rate over five years means paying about $2,028 monthly, ensuring stability even if market rates rise. This makes them ideal for structured investments like upgrading technology or expanding facilities. On the other hand, revenue-based financing adjusts payments based on revenue, offering flexibility but introducing unpredictability, which complicates long-term planning. Fixed loans provide the consistency needed for growth-focused strategies.

Key Takeaways:

- Fixed loans ensure stable payments, unaffected by interest rate changes.

- They simplify budgeting for large, planned investments.

- Revenue-based financing suits short-term needs but lacks stability for long-term projects.

1. Fixed Loans

Predictability

Fixed loans offer stability by locking in your interest rate from the start, ensuring your monthly payments remain consistent throughout the loan's term. This eliminates surprises from rate increases and makes it easier to plan your finances for the long haul [1] [2].

Budgeting Impact

With fixed payments, these loans act like predictable expenses - similar to rent or payroll. This consistency allows you to allocate funds more effectively for growth strategies. Plus, the structured repayment schedule provides a clear timeline for becoming debt-free, which can enhance your credibility with stakeholders. Business term loans typically range from $25,000 to $500,000, with repayment terms spanning one to seven years. Opting for longer terms can lower your monthly payments, easing financial pressure [1].

Cash Flow Flexibility

While less adaptable than revenue-based financing, fixed loans with longer terms can reduce the strain on monthly cash flow. For example, a seven-year loan spreads out payments, making them more manageable compared to short-term options. However, the fixed schedule requires you to maintain enough reserves to cover payments during slower periods. Be sure to check for prepayment penalties, which could make refinancing expensive if interest rates fall or if you want to pay off the loan early. Also, account for additional costs like origination fees (typically 1%–5% of the loan amount) and application fees (ranging from $100 to $500), which can increase the total expense [1].

Suitability for Growth

Fixed loans are ideal for planned, long-term investments that promise steady returns - like purchasing manufacturing equipment, upgrading technology, or acquiring warehouse space. For instance, if you're installing automated fulfillment systems, a five-year fixed loan allows you to spread the cost over the asset's lifespan. The lump sum provided upfront ensures you can execute your plans without delays. Just make sure the expected returns comfortably cover the fixed monthly payments. This level of predictability sets fixed loans apart from more variable financing options, which will be discussed next.

sbb-itb-d7b5115

2. Revenue-Based Financing

Predictability

Revenue-based financing adjusts your payments based on your sales performance instead of locking you into fixed monthly amounts. Typically, you pay a percentage of your revenue - usually between 5% and 12%. When sales surge, your payments increase; when sales slow, your payments decrease automatically [3]. While this setup aligns payments with your business's current performance, it also makes long-term financial forecasting trickier. Unlike fixed loans, where payments remain constant, this model introduces a layer of unpredictability.

Budgeting Impact

The fluctuating payment structure of revenue-based financing can complicate budgeting. For instance, if you're planning a $50,000 inventory expansion or rolling out a multi-phase marketing campaign, the uncertainty around payment amounts can make it harder to allocate funds effectively. This is particularly challenging for eCommerce businesses aiming for structured growth, as payment variability can disrupt plans for sizable investments.

Cash Flow Flexibility

One standout benefit of revenue-based financing is how it adapts to your cash flow. When sales dip - due to seasonality or other factors - your payments decrease accordingly, unlike fixed loans that demand consistent payments regardless of revenue [3]. For eCommerce businesses that experience seasonal highs and lows, like those relying on Q4 holiday sales, this flexibility can help avoid cash flow crunches during slower months. However, in peak periods, higher payments can limit your ability to reinvest profits into growth initiatives. On the plus side, some providers offer quick access to funds, sometimes within 24 hours, through platform integrations [3].

Suitability for Growth

Revenue-based financing works best for short-term, revenue-driven activities rather than long-term investments. It's ideal for businesses needing to restock inventory multiple times a year, run agile marketing campaigns, or explore new sales platforms like TikTok Shop - initiatives that deliver immediate returns. However, its variable nature makes it less suitable for long-term plans, such as relocating a warehouse, expanding your team, or implementing complex fulfillment systems. This financing model shines in its ability to adapt quickly, but its limitations in long-term planning are worth noting as we explore its pros and cons further.

Fixed vs. Variable Rate Business Loans: Which is Right for You?

Advantages and Disadvantages

Fixed Loans vs Revenue-Based Financing Comparison for eCommerce Growth

The table below breaks down the main trade-offs between fixed loans and revenue-based financing, helping businesses weigh their options effectively.

| Criteria | Fixed Loans | Revenue-Based Financing |

|---|---|---|

| Predictability | Offers consistent monthly payments, making financial forecasting easier. | Payments vary with revenue, making long-term planning more challenging. |

| Budgeting Impact | Fixed payments simplify planning for major investments. | Variable payments can complicate multi-phase growth strategies. |

| Cash Flow Flexibility | Requires payments regardless of sales performance. | Adjusts with revenue, offering relief during slower periods. |

| Protection from Rate Increases | Rates are locked in, shielding against market fluctuations. | Provides no protection from potential rate increases. |

| Suitability for Growth Investments | Best for long-term projects like technology upgrades or warehouse expansions. | More suitable for short-term needs like inventory restocking or marketing campaigns. |

| Initial Cost | Typically involves higher initial rates. | Often starts with lower effective rates, though total costs may increase with revenue growth. |

For eCommerce businesses pursuing strategic growth, fixed loans offer a dependable framework for committing capital. Their predictable payment structure allows for precise resource allocation, ensuring that planned investments proceed without disruption. For instance, Onramp Funds’ Fixed Fee Structure - featuring fees between 2% and 8% - provides a straightforward and transparent model with no hidden charges.

On the other hand, revenue-based financing prioritizes flexibility over stability. This option may work well for businesses with fluctuating revenues or short-term funding needs. However, its variable nature can hinder long-term planning, making it less ideal for structured growth initiatives.

When it comes to long-term eCommerce growth, the stability and predictability of fixed loans often make them the stronger choice, particularly for businesses aiming to invest confidently in their future.

Conclusion

For eCommerce businesses planning for long-term growth, fixed loans offer the stability and predictability needed to execute strategic investments. Whether it’s expanding your inventory, upgrading your tech infrastructure, or launching consistent marketing campaigns, fixed loans make it easier to budget accurately with their predictable monthly payments. This ensures you can allocate resources without unexpected disruptions.

Fixed loans are especially suited for initiatives with clear goals and timelines. For example, if you’re building a new warehouse, implementing advanced fulfillment systems, or stocking up for a busy season, a locked-in interest rate protects you from market fluctuations. This predictability supports precise revenue forecasting and helps create a solid foundation for financial planning.

When comparing financing options, the decision between fixed loans and revenue-based financing hinges on your growth goals and risk tolerance. Fixed loans are ideal for businesses focused on multi-year strategies that require consistent budgeting. On the other hand, revenue-based financing may suit short-term needs but can complicate long-term financial planning.

As a trusted partner for eCommerce growth, Onramp Funds supports sellers across major platforms with transparent, equity-free financing. With a fixed fee structure ranging from 2% to 8% and funding available within 24 hours, Onramp Funds empowers businesses to seize growth opportunities while retaining full ownership and control.

Choosing the right financing structure is a pivotal step in scaling your eCommerce business. Fixed loans provide the stability and confidence to turn your planned investments into tangible results.

FAQs

How do I know if I can afford a fixed loan payment?

When deciding if a fixed loan payment is manageable, take a close look at your business's steady income. Since fixed loans come with consistent monthly payments, it's crucial that your eCommerce revenue can handle these payments without putting a strain on your cash flow. Compare your average monthly sales to the loan payment amount, and don’t forget to factor in slower sales periods - those payments won’t change, even during a dip in revenue. A reliable and stable income stream is key to making fixed payments work for your business.

When is revenue-based financing a better fit than a fixed loan?

Revenue-based financing works well for businesses with seasonal or fluctuating revenue. Unlike fixed loans that demand steady payments regardless of income, this model adjusts payments based on sales. During slower months, payments decrease, easing cash flow pressures, while in high-sales months, they increase accordingly. This flexibility makes it a practical option for businesses managing unpredictable income streams.

What fees or penalties should I watch for in a fixed loan?

Be aware of prepayment penalties - fees some lenders impose if you decide to pay off your loan ahead of schedule. These penalties are usually fixed amounts, often between $300 and $500, no matter how much is left to pay on the loan. It's important to carefully review your loan agreement to fully understand any fees that might apply.