Funding is more than just money - it's a tool to grow your eCommerce business. Experienced founders carefully weigh their options, balancing growth opportunities with risks like ownership dilution or repayment terms. With global eCommerce sales projected to hit $8.1 trillion by 2026, the stakes are high, but funding landscapes have shifted dramatically (Direct-to-Consumer funding is down 97% since 2021). Here's what you need to know:

- When to Seek Funding: Look for signs like product-market fit, strong revenue traction, or inventory constraints. Start preparing 6–12 months before you need capital.

- Funding Options: Choose from venture capital, revenue-based financing, retailer loans, inventory financing, bootstrapping, or crowdfunding - each has trade-offs in speed, equity cost, and repayment terms.

- Metrics to Watch: Focus on key numbers like Customer Acquisition Cost (CAC), Lifetime Value (CLV), Gross Margins (50–60%), and Cash Conversion Cycle (CCC).

- Smart Strategies: Build relationships early, keep financials organized, and align funding choices with specific goals like scaling inventory or marketing.

Quick Comparison:

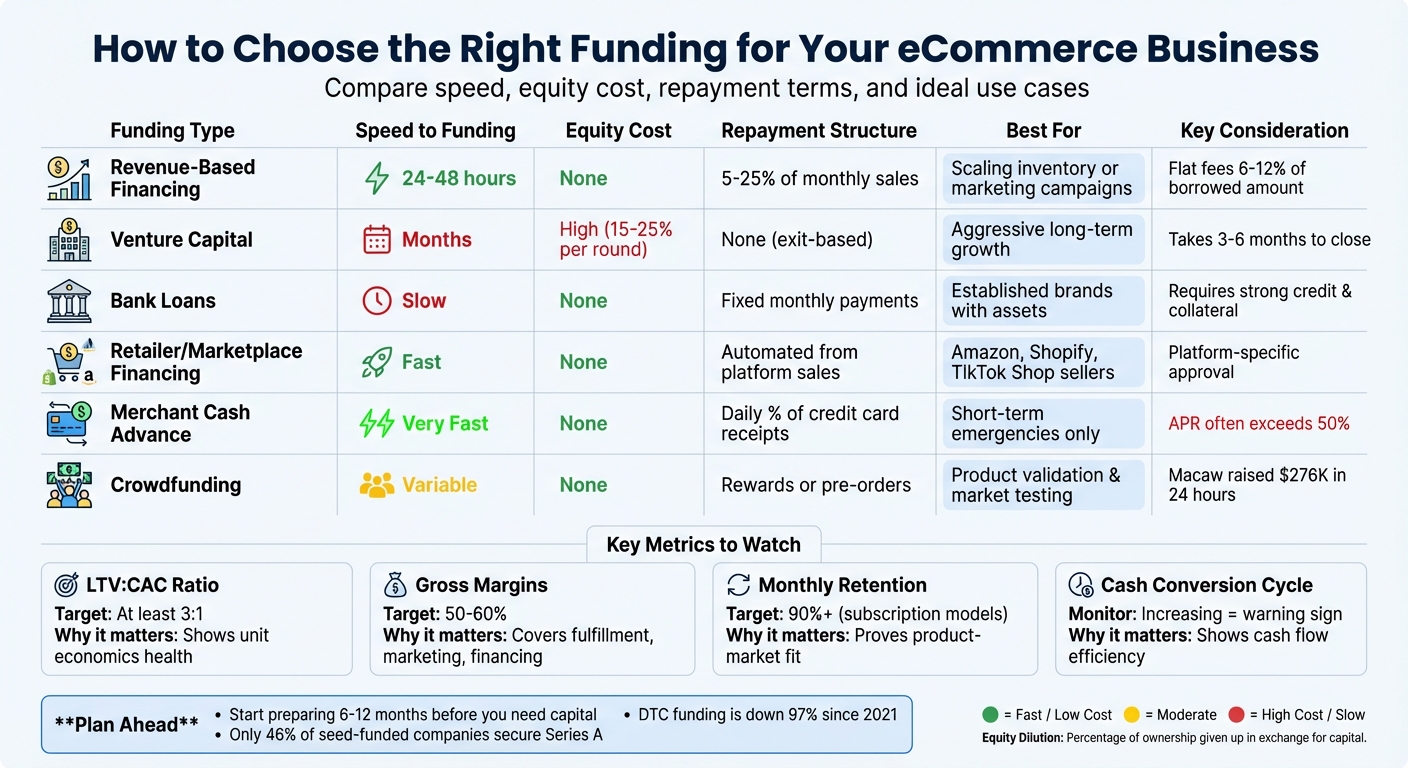

| Funding Type | Speed | Equity Cost | Repayment Type | Best For |

|---|---|---|---|---|

| Revenue-Based Financing | 24–48 hours | None | % of monthly sales | Scaling inventory/marketing |

| Venture Capital | Months | High | None (Exit-based) | Aggressive long-term growth |

| Bank Loans | Slow | None | Fixed monthly payments | Established brands with assets |

| Retailer Financing | Fast | None | Automated from sales | Platform-specific sellers |

| Merchant Cash Advance | Very Fast | None | Daily % of receipts | Short-term emergencies |

| Crowdfunding | Variable | None | Rewards/Pre-orders | Product validation |

Key Takeaway: The right funding depends on your business stage, goals, and financial health. Plan ahead, monitor metrics, and choose funding that aligns with your growth strategy.

eCommerce Funding Options Comparison: Speed, Cost, and Best Use Cases

When to Seek Funding

Signs Your Business Is Ready for Funding

Timing is everything when it comes to funding. The best moment to seek investment is when your business model is proven, and growth is undeniable.

One of the clearest indicators is achieving product–market fit. Investors want to see that customers not only like your product but also keep coming back for more. Metrics like repeat purchase rates and low churn demonstrate this [1][7]. If your business has strong unit economics - where your Customer Lifetime Value (CLV) significantly outweighs your Customer Acquisition Cost (CAC) - you’re on solid ground. Many consumer brands aim for gross margins between 50% and 60% [3][6].

Struggling with inventory constraints is another signal. If you’re constantly tying up cash in stock or producing months in advance to meet demand, it may be time to consider funding to scale up and break through those limitations.

Revenue traction is another key factor. For example, Series A investors often look for SaaS-based eCommerce tools with Monthly Recurring Revenue (MRR) exceeding $40,000 or strong Gross Merchandise Value (GMV) [7][1]. For subscription-based businesses, a 90% monthly retention rate is a strong benchmark [7]. Keep in mind that only 46% of seed-funded companies successfully secure Series A funding, so hitting these milestones is critical [8].

Once you’ve checked these boxes, it’s time to start planning your fundraising strategy.

Planning Ahead for Fundraising

The best time to prepare for fundraising? Long before cash flow becomes a problem. A proactive approach not only secures capital but also ensures that growth stays on track. Savvy founders typically begin preparing 6 to 12 months before they actually need the funds [7][8]. This is important because closing a funding round in the U.S. often takes 3 to 6 months, and sometimes even longer [10].

Your financials need to be airtight before you approach investors. Create a complete data room with all the essentials: financial records, legal documents, and customer contracts. The due diligence process can take anywhere from 2 to 6 weeks, and missing information can cause unnecessary delays [10]. A key part of this preparation is accurately calculating your Landed Cost of Goods Sold (LCOGS), which includes freight, customs, and packaging. This ensures you’re not underpricing your products before seeking capital [6][3].

Building relationships with investors early is another smart move. On average, it takes 20 to 30 pitches to secure one term sheet, and warm introductions are far more effective than cold outreach [10]. Networking well in advance means you’ll already have connections when you’re ready to raise funds.

Cash flow modeling is equally important. Since inventory ties up cash, you’ll need models that account for both optimistic and pessimistic sales scenarios [3]. Keep an eye on your Cash Conversion Cycle (CCC) - if it’s increasing, it may indicate that cash is taking too long to flow back into the business, signaling the need for working capital funding [6]. As Simon Davis from SBO Financial puts it:

"Cash is the oxygen. You can have great sales, but if you're out of cash, operations will stall." [6]

Weighing Growth Against Risk

Once your financials and investor relationships are in order, it’s time to weigh the potential for growth against the risks involved. Experienced founders view funding as a strategic decision, aligning it with their readiness and growth goals.

One critical consideration is how much capital to raise. Aim for enough funding to cover 12 to 18 months of operations, allowing your team to hit key milestones without constant fundraising interruptions. Add a 20% to 25% buffer to account for unexpected expenses or market changes. This can be calculated using your monthly burn rate multiplied by the desired number of months of runway [10].

Equity dilution is another factor to think about carefully. The "Rule of 20" suggests limiting dilution to 20% to 25% per funding round to preserve ownership for future rounds [10]. With Direct-to-Consumer funding down 97% from its 2021 peak, maintaining leverage in negotiations is more important than ever [1].

Timing your fundraising can also make a huge difference. The best moment to raise capital is when you’ve reached a "valuation inflection point" - a milestone that significantly increases your company’s value. This could be achieving product–market fit, consistent revenue growth, or proven scalability. Raising funds when your business is strong, rather than in a desperate situation, can lead to better terms and less dilution.

Take Atlassian as an example. The company bootstrapped for eight years, growing to over $50 million in annual recurring revenue before accepting its first outside investment - $60 million from Accel in 2010. Co-CEO Scott Farquhar explained that the funding wasn’t driven by a cash shortage but by strategic goals, such as providing liquidity for employee shareholders and expanding the board to support long-term growth [9]. This deliberate approach resulted in favorable terms and minimal dilution.

sbb-itb-d7b5115

Funding Options for eCommerce Businesses

Types of Funding Sources

Once you've figured out the right time to raise funds, the next step is understanding your options. eCommerce founders today can tap into a variety of funding sources, each tailored to different business needs and growth stages.

Venture capital and angel investors offer funding in exchange for equity. VCs often look for businesses with high growth potential and may also provide mentorship and valuable industry connections.

Revenue-based financing (RBF) gives you upfront capital, repaid as a fixed percentage of future sales - usually between 5% and 25% [2]. This approach is flexible, adjusting payments during slower sales periods. For instance, in 2019, fashion brand Hedoine secured $50,000 through RBF to boost its marketing efforts. By early 2020, their sales had surged by 1,106% [2].

Retailer and marketplace financing is available from platforms like Amazon, Shopify, and Stripe. These loans are based on your sales data and marketplace performance, making the approval process quicker [12].

Inventory financing focuses on providing funds specifically for purchasing stock, using the inventory itself as collateral [11]. It’s a handy option during seasonal peaks or when placing bulk orders to secure better supplier terms.

Bootstrapping involves using personal savings or reinvesting company profits to fund growth. While it lets you maintain full control, it can limit how quickly your business scales.

As Brandon Ackroyd, Director at TigerMobiles, puts it:

"I want to see founders who have the confidence to put their money where their mouth is" [5].

Merchant cash advances (MCAs) provide a lump sum in exchange for a portion of your daily or weekly credit card receipts. However, the effective APRs can often exceed 50% [2][11]. Crowdfunding is another option, allowing you to raise smaller amounts from many individuals. For example, the web design tool Macaw raised $276,000 in just 24 hours, far surpassing its $75,000 target [2]. Similarly, Tesla generated a waitlist of nearly 200,000 customers in one day for the Model 3 by taking $1,000 deposits to fund production [5].

Below, you’ll find a comparison of these funding options to help you weigh the trade-offs.

Side-by-Side Funding Comparison

Each funding source has its pros and cons. Here’s a quick breakdown to help you decide:

| Funding Source | Speed | Equity Cost | Repayment Type | Best For |

|---|---|---|---|---|

| Revenue-Based Financing | Fast (24–48 h) | None | % of monthly sales | Scaling marketing/inventory |

| Venture Capital | Slow (Months) | High | None (Exit-based) | Long-term aggressive growth |

| Bank Loans | Slow | None | Fixed monthly payments | Established brands with assets |

| Retailer Financing | Fast | None | Automated from sales | Platform-specific sellers |

| Merchant Cash Advance | Very Fast | None | Daily % of receipts | Short-term emergencies |

| Crowdfunding | Variable | None | Rewards/Pre-orders | Product validation |

Revenue-based financing often includes flat fees ranging from 6% to 12% of the borrowed amount [2]. On the other hand, merchant cash advances can be much pricier, with effective APRs often exceeding 50% [11].

Speed is crucial for eCommerce businesses. Modern lenders increasingly rely on AI and real-time analytics, integrating with platforms like Shopify and Stripe to assess your business and approve funding in as little as 24 hours [11]. While traditional bank loans offer lower interest rates, they take longer to process and require more paperwork.

For sellers on platforms like Amazon, Shopify, BigCommerce, WooCommerce, Squarespace, Walmart Marketplace, and TikTok Shop, revenue-based financing is an attractive option. It provides funding within 24 hours, with repayments tied to daily sales. Companies like Onramp Funds offer transparent pricing and flexible repayment plans, ensuring you can scale during peak seasons without depleting your working capital during slower times.

Choosing Funding Based on Your Needs

Once you’ve laid the groundwork, your funding choice should align with your business goals and operational needs. Smart founders match their funding source to their specific objectives rather than just taking the first available option.

- Inventory management: Revenue-based financing works well for bulk inventory purchases, helping you lower per-unit costs and avoid stockouts during busy periods - all without locking you into fixed payments when sales slow down.

- Marketing growth: Flexible funding can support paid advertising on platforms like Amazon, Google, TikTok, and Meta. With revenue-based options, repayments adjust to your sales, so you won’t have to cut ad spend to meet fixed payments.

- Multi-channel selling: Avoid loans tied to a single marketplace. Independent lenders that evaluate your overall revenue give you the freedom to invest in the channels offering the best growth opportunities.

- Cash flow gaps: Look for financing options with automated repayments tied to daily sales. This ensures your repayment pace matches your revenue flow.

Lastly, keep an eye on your margins. eCommerce businesses should aim for gross margins of at least 50% to 60% to cover costs like fulfillment, marketing, and financing [3].

Matching Funding to Your Business Goals

Setting Clear Funding Goals

Start by clearly defining what you need the funding for. Seasoned entrepreneurs align their funding sources with specific business objectives.

For instance, if you're preparing for Q4 and need to stock up on inventory, inventory financing could be the right fit - it allows you to use that inventory as collateral. On the other hand, if you're ramping up marketing efforts on platforms like TikTok or Meta, revenue-based financing might be a smarter choice. This option ties repayments to your sales performance, so you’re not burdened during slower weeks.

Expanding into international markets is another common goal. With nearly half of global shoppers now making cross-border purchases, and cross-border eCommerce projected to reach $1 billion by 2030 [13], having access to capital that supports localization efforts - without rigid repayment terms - is key.

Other objectives, like upgrading technology, streamlining supply chains, or launching new products, will require different funding structures. By defining your specific needs, you’ll be better equipped to evaluate and compare funding options.

Once your goals are set, it’s time to weigh the trade-offs of each funding type.

Understanding Trade-Offs Between Funding Types

Every funding source comes with its own set of pros and cons. For example, venture capital provides large sums of money and strategic expertise, but it often comes with ownership dilution and pressure to grow quickly. As Mercury explains:

"Equity financing involves selling a stake in your company to investors in exchange for capital... this route typically comes with pressure to grow fast (and potentially raise subsequent capital)" [3].

Revenue-based financing offers flexibility because repayments adjust based on your sales. However, if your growth is steady and predictable, this option might end up costing more than a traditional bank loan.

Traditional bank loans are known for their lower interest rates and fixed terms, but they often require strong credit, personal collateral, and a lengthy approval process [1][2]. Alternatively, marketplace financing from platforms like Amazon or Shopify can provide quick cash flow to cover payment delays of 30–60 days. The downside? Fees can eat into your profit margins.

The key is to evaluate these trade-offs in the context of your cash flow and growth plans.

Decision-Making Frameworks for Funding

Once you’ve outlined your goals and understood the trade-offs, a structured framework can help guide your decision. Start by calculating your total cost of capital - this includes not just interest rates but also fees, revenue share percentages, and potential equity dilution [11].

Next, map out your cash flow. Use sensitivity models to account for different revenue scenarios. If your revenue is seasonal or unpredictable, revenue-based financing may be a better fit since repayments scale with earnings. But if your sales are consistent, a traditional loan with fixed payments might be more cost-effective.

Lastly, think about how your funding choice could impact your operations. Investors often focus on metrics like Customer Acquisition Cost (CAC), Customer Lifetime Value (CLV), and Gross Merchandise Value (GMV) to gauge long-term growth potential [1]. If a funding decision forces you to compromise on these metrics, it might not align with your broader business strategy.

For eCommerce sellers using platforms like Amazon, Shopify, BigCommerce, or TikTok Shop, revenue-based financing from providers like Onramp Funds can be particularly appealing. Their flexible repayment plans adjust to daily sales, helping you scale during peak seasons while preserving cash flow during slower periods.

Running an Effective Fundraising Process

Creating Your Investor Target List

When building your investor target list, focus on those who specialize in direct-to-consumer (DTC) and consumer brands. As the EasyApps Guide highlights:

"Target investors who specialize in DTC and consumer brands rather than generalist VCs" [14].

These investors understand the unique challenges of physical products, such as inventory lead times and customer acquisition dynamics, which generalist investors may overlook.

Aim for a list of 40–80 potential investors to increase your chances of securing 3–5 serious prospects, considering a typical 5–10% conversion rate from initial meeting to signed term sheet [14]. Group your list by funding stage - angel investors for $25,000–$250,000, seed-stage VCs for $500,000–$3 million, and growth-stage VCs for $5 million and above [14].

Seek out investors who bring more than just money. According to WePitched:

"You're looking for 'Smart Money' - people who have built brands before and can offer distribution or manufacturing contacts alongside their cash" [15].

These connections can provide manufacturing relationships, operational expertise, and networks that accelerate growth beyond funding alone.

Whenever possible, prioritize warm introductions. These are up to 10 times more effective than cold outreach [14]. Use your advisors, current investors, or professional contacts to facilitate these connections. Before reaching out, review your unit economics - most serious eCommerce investors expect an LTV:CAC ratio of at least 3:1 [14]. If your metrics fall short, focus on improving them first.

A targeted investor list paired with a strong pitch deck is essential for securing funding.

Building Your Pitch Deck

Your pitch deck needs to grab attention immediately. The first slide should clearly convey your value proposition in a single sentence, addressing your target customer, their pain point, your solution, and the outcome, supported by one compelling proof point [16]. As the WePitched team puts it:

"If you are using equity to pay for Facebook ads, you are effectively selling your house to pay for gas" [15].

Create two versions of your deck: a "send-ahead" version with more context for asynchronous reading and a "live" version with high-contrast visuals and minimal text for presentations [16]. Your problem slide should quantify the costs of the issue in terms of time, money, or risk - investors fund "expensive" problems, not just relatable ones [16]. Frame your solution as a clear "before vs. after" transformation rather than a list of features.

For market sizing, use a bottom-up approach grounded in real constraints like customer acquisition costs and fulfillment capacity [16]. In eCommerce, where products can be easily copied, defensibility often comes from brand trust, exclusive distribution channels, proprietary supply chains, or data-driven advantages [16][14]. Be prepared with a well-organized data room containing your 12-month P&L, customer retention analysis, CAC vs. LTV trends, and inventory turnover reports [15]. If you can't produce these in 10 minutes, you're likely not ready for professional capital [15].

Tie your funding request to specific milestones, such as improving margins, launching new SKUs, or expanding into retail [16]. Your Go-To-Market slide should focus on "channel math" - traffic, conversion rates, average order value, and CAC payback - rather than relying on organic virality [16]. For eCommerce brands generating $200,000–$500,000 in annual sales, a $50,000 investment typically translates to 5–10% equity [15].

With a polished deck in hand, the next step is to manage your time effectively throughout the fundraising process.

Managing Time During Fundraising

Once your investor list is finalized and your pitch deck is ready, managing your time efficiently becomes critical. Fundraising can take months if not approached strategically. Choose the right funding vehicle based on your needs and timeline. Venture capital typically takes 3–6 months, while revenue-based financing can be secured within 24–48 hours [14][11][15]. As WePitched notes:

"Chasing the wrong type of ecommerce business funding isn't just a distraction; it's often the primary reason brands run out of runway before they hit their stride" [15].

Automate your financial processes before starting. Use accounting tools and invoicing software to save time on manual tasks [3]. Connect your eCommerce platforms - whether Shopify, Amazon, or TikTok Shop - directly to lender portals for real-time data sharing, which speeds up underwriting and approvals [11][2]. For example, in February 2026, Sarah, founder of Green Pantry, secured $60,000 in revenue-based financing within 48 hours while maintaining $40,000 in monthly recurring revenue. This allowed her to retain 95% of her company and repay the debt in just eight months [15].

Run monthly margin checks on your SKUs to catch any supply chain or shipping cost increases that could affect your fundraising narrative [3]. Ensure your unit economics reflect at least a 20% net margin after variable costs, so additional capital drives growth rather than losses [15]. Instead of overwhelming investors with lengthy PDFs, provide a concise narrative supported by a well-organized digital data room [15]. For sellers on platforms like Amazon or Shopify, services like Onramp Funds offer revenue-based financing with funding available within 24 hours, allowing you to focus on growing your business instead of navigating a long fundraising process.

The 5 Money Systems The Top 1% of Ecommerce Founders Use (Steal These)

Key Takeaways for eCommerce Founders

Timing matters. The right moment to seek funding often aligns with key operational milestones. These include situations like a surge in demand requiring inventory purchases, scaling a proven marketing channel, or validating your market through pre-orders or launching a minimum viable product (MVP). Additionally, maintaining 3–6 months of operating expenses in reserve signals financial stability to potential investors or lenders [17]. These factors help determine when your business is ready to explore funding options.

Match funding options to your goals and ownership preferences. Different funding types come with their own pros and cons, so aligning them with your business objectives is critical. For example, revenue-based financing works well for inventory purchases or marketing campaigns when retaining full ownership is a priority and flexible repayment terms are needed. On the other hand, equity funding might be better if you’re looking for strategic guidance and access to a strong network, even though it involves giving up some ownership.

Focus on strong metrics before pursuing funding. A data-driven approach is crucial when seeking funding. Investors and lenders prioritize solid financial performance over ambitious visions. Key metrics to monitor include an LTV:CAC ratio of at least 3:1, gross margins in the 50–60% range, and consistent retention rates [3][4]. Connecting your eCommerce store to funding platforms can also speed up the process, with AI-enabled underwriting offering capital approvals in as little as 24 hours [1].

Be strategic in your investor outreach. Experienced founders often focus their efforts on investors who specialize in direct-to-consumer (DTC) and consumer brands. Warm introductions can significantly improve your chances, so prioritize those connections. Additionally, having a well-organized digital data room with up-to-date financial documents - such as a 12-month profit and loss statement, key metric trends, and inventory turnover data - ensures you’re prepared to respond quickly to investor inquiries.

For eCommerce businesses generating at least $3,000 in monthly sales and seeking quick, equity-free capital, Onramp Funds offers a flexible solution through revenue-based financing, with funding available within 24 hours. Repayments are tied to your sales, typically ranging from 2–10%, allowing you to manage payments more easily during slower periods while scaling up during busy times. This approach minimizes the hassle of traditional fundraising, letting you focus on growing your business. By aligning funding strategies with your operational needs, you can set yourself up for a successful fundraising journey.

FAQs

How do I know how much funding to raise?

To figure out how much funding your business needs, start by matching your financial requirements with your goals and growth strategy. Take a close look at performance metrics to pinpoint areas that could make the biggest difference - like inventory, marketing efforts, or technology upgrades. Next, use past sales data and seasonal patterns to forecast your cash flow and estimate the amount of funding necessary. Make it a habit to review and adjust your plans regularly to ensure that the capital you raise supports steady growth and keeps your cash flow stable.

Which funding type fits my cash flow and seasonality?

When it comes to funding, the best option often hinges on your cash flow and how seasonal your business is. Revenue-based financing stands out for its flexibility - it adjusts repayments according to your monthly revenue. This can be a lifesaver during slower months. On the other hand, traditional loans come with fixed payments, which might not be ideal if your income fluctuates with the seasons.

Crowdfunding or grants are also worth considering, especially if their timing aligns with your campaigns. However, these options can require significant effort and come with a level of unpredictability. Ultimately, the key is to pick a funding method that aligns with your revenue patterns and supports your growth goals.

What financials should I have ready before I apply?

Before seeking funding, make sure your financial statements are in order. This means having profit and loss statements, cash flow statements, and a solid grasp of your key business metrics. You'll also need to clearly articulate how the funds will be used to achieve your business objectives.