When it comes to borrowing for your eCommerce business, timing and intent are everything. There are two main approaches: planned borrowing and emergency borrowing. Here's the difference:

- Planned Borrowing: This is when you secure funds ahead of time for specific goals like restocking inventory, running ad campaigns, or expanding into new markets. It aligns the type of funding with your business needs, helping you manage costs and protect ownership. For example, short-term loans for quick returns and long-term capital for growth projects.

- Emergency Borrowing: This happens when you need immediate cash to cover unexpected shortfalls, like payout delays or rising costs. While fast, it often comes with higher fees and rigid repayment terms that can strain your business.

Planned borrowing helps maintain stability and supports growth, while emergency borrowing is a short-term fix that can lead to higher costs and risks. To avoid the pitfalls of reactive borrowing, plan ahead, secure funding early, and match the loan type to your needs.

1. Planned Borrowing

Purpose

Planned borrowing is all about securing funds ahead of time to fuel growth initiatives like inventory restocking, marketing pushes, or entering new markets. It ensures steady cash flow while protecting your equity stake in the business [2]. The key here? Match the type of funding to your investment's timeline. For short-term needs - like stocking up on inventory or running ad campaigns with quick returns (under nine months) - working capital or revenue-based financing is ideal. On the flip side, save equity for long-term projects like research and development or expanding internationally [2]. Knowing what you're funding helps you decide when to act.

Timing

Timing can be the difference between staying ahead or constantly playing catch-up. Take mid-year sales events, like Prime Day: you need to secure capital and scale production as early as March to prepare [1]. This lead time is critical to cover manufacturing, shipping, and the marketing spend you'll need to drive traffic when the event goes live. And don’t forget about platform payout delays - Amazon holds funds for 14 days, and TikTok Shop can take up to 30 days to release payments [1]. Without planned capital, you risk campaign interruptions right when momentum matters most. Once you've nailed the timing, understanding the costs becomes your next priority.

Cost Structure

The cost of borrowing depends heavily on how well your funding choice matches your needs. Revenue-based financing, for instance, takes a percentage of your monthly revenue - typically between 5% and 25% - until the original loan plus a fixed fee is repaid. This setup avoids compounding interest and late penalties [1]. Credit lines, on the other hand, can give you access to larger amounts (up to $2 million for qualified sellers) and charge fees or interest only on the funds you actually use [1]. Opting for non-dilutive funding methods like these helps you hold onto ownership and keep your options open for the future [2].

Impact on Cash Flow and Stability

When done right, planned borrowing can smooth out your cash flow. Repayments tied to revenue automatically adjust - slowing down in slower months and speeding up during sales surges - so you can cover fixed costs without stretching your finances [1][2]. This flexibility is invaluable for maintaining stability. A great example? In 2025, Shopfront used recurring revenue financing to branch out from pharmaceuticals into consumer retail. With flexible funding instead of giving up equity, they brought in top-notch marketers, launched well-tested campaigns, and secured a major retail client. The result? A 20% boost in projected revenue - all while keeping full ownership of the business [1].

sbb-itb-d7b5115

2. Emergency Borrowing

Emergency borrowing is a reactive approach to addressing critical cash flow gaps. Unlike borrowing that's planned to fuel growth or expansion, this type of financing is all about solving immediate, unforeseen financial challenges.

Purpose

The main goal of emergency borrowing is to quickly cover unexpected shortfalls in cash flow. These gaps often arise from delays in platform payouts or sudden spikes in costs. For instance, eCommerce platforms sometimes hold payouts for longer than expected, leaving businesses scrambling to cover expenses. On top of that, unexpected cost hikes - like the more than 20% increase in Meta and Google ad prices in 2025 - can create urgent funding needs. Shabnam Mansukhani of CrediLinq explains the stakes clearly:

"If you pause campaigns because of cash flow gaps, you lose algorithm momentum and end up paying more to regain traction" [1].

Timing

Emergency borrowing comes into play when funds are needed immediately. Whether it's to keep an ad campaign running or to cover inventory costs while waiting for delayed payouts, these situations demand speed. This type of borrowing is often a response to a cash flow crunch, where upfront expenses outpace incoming revenue. To address this urgency, some lenders offer approvals and fund disbursements in as little as one business day [1]. However, this rapid access to funds often comes with higher costs.

Cost Structure

Quick access to capital doesn’t come cheap. Merchant Cash Advances (MCAs), for example, can carry effective APRs ranging from 20% to 60%, with daily or weekly repayment schedules that can quickly strain liquidity. Revenue-based financing, another option, deducts 5% to 25% of monthly revenue until the loan is repaid. Compared to planned financing, emergency borrowing tends to be more expensive [1].

Impact on Cash Flow and Stability

While emergency borrowing can provide immediate relief, it can also create short-term cash flow challenges. Frequent repayment schedules can eat into funds needed for core operations. To mitigate the financial strain, businesses should focus on channels with a strong Return on Ad Spend (ROAS) when using high-cost capital. However, relying too often on emergency borrowing can lead to a cycle of dependency. Building a repayment buffer can help reduce risks and maintain financial stability over the long term [1].

Pros and Cons

Strategic vs Reactive Borrowing for eCommerce: Cost, Flexibility & Impact Comparison

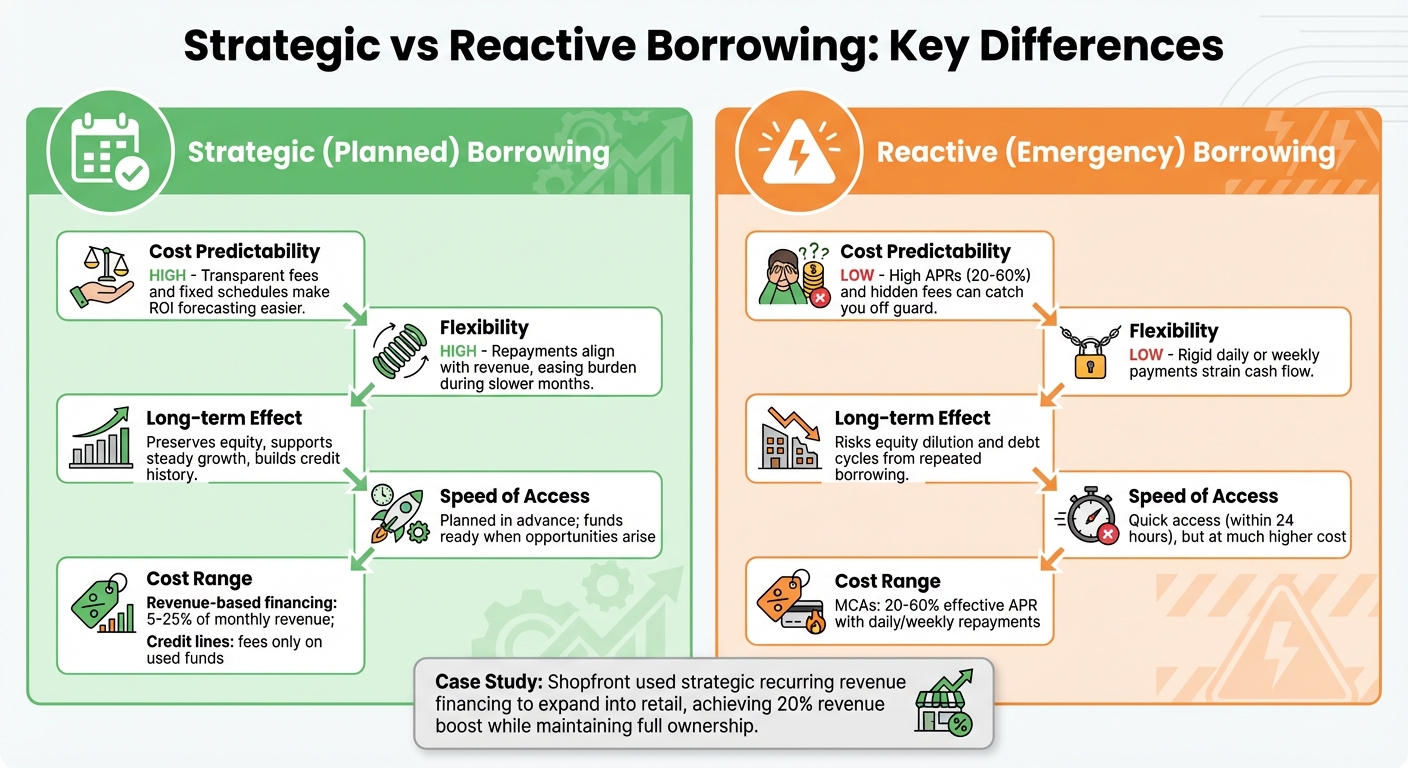

When it comes to planned versus emergency borrowing, each approach brings its own set of advantages and challenges. To make sense of their impact on your finances, let’s break it down. The table below highlights how these two strategies differ in terms of cost, flexibility, and long-term implications.

| Factor | Strategic (Planned) Borrowing | Reactive (Emergency) Borrowing |

|---|---|---|

| Cost Predictability | High; transparent fees and fixed schedules make ROI forecasting easier. | Low; high APRs (20%–60%) and hidden fees, such as draw or maintenance charges, can catch you off guard. |

| Flexibility | High; repayments often align with revenue, easing the burden during slower months. | Low; rigid daily or weekly payments can strain cash flow. |

| Long-term Effect | Helps preserve equity, supports steady growth, and builds credit history. | Risks include unnecessary equity dilution and potential debt cycles from repeated borrowing. |

| Speed of Access | Planned in advance; funds are ready when opportunities arise. | Quick access (often within 24 hours), but at a much higher cost. |

Strategic borrowing allows you to take control of your finances. By planning ahead, you can mix funding sources to create a balanced capital stack, protecting ownership while optimizing your financial position.

Reactive borrowing, on the other hand, is designed for urgent situations. While it provides fast access to funds, it often comes with steep costs and rigid repayment terms. This can lead to a cycle of dependency, making it harder for businesses to regain financial stability. A great example of avoiding this pitfall is Shopfront. In 2026, instead of turning to emergency loans, they opted for strategic recurring revenue financing. This decision enabled them to expand into retail, bring on key hires, and boost projected revenue by 20% [1].

Choosing between these methods isn’t just about solving immediate problems - it’s about shaping the future of your business. By understanding the trade-offs, eCommerce companies can make smarter financing decisions that support sustainable growth.

Conclusion

The key takeaway here is the importance of timing and intent when it comes to financing. Strategic borrowing involves planning ahead - using short-term capital for immediate needs like inventory or ads and reserving long-term funding for growth initiatives. On the other hand, reactive borrowing stems from cash flow gaps, often leading to costly, last-minute decisions that can put unnecessary pressure on your business.

To make the shift toward strategic financing, start by using your financial data as a planning tool rather than just a historical record. Monthly forecasts that track revenue, expenses, and anticipated costs can transform uncertainty into actionable insights, helping you spot funding needs before they escalate into emergencies.

Another smart move is to build a repayment buffer by setting aside reserves for loan payments during slower periods. Direct borrowed funds to high-performing channels, like proven ad platforms or inventory investments, that offer quick returns. This ensures you maintain campaign momentum and avoid inflated costs down the line.

Platforms like Onramp Funds are designed to make strategic borrowing easier for eCommerce businesses. They offer funding within 24 hours and provide flexible repayment options tied to your sales performance. Whether you're gearing up for a major sales event or scaling a successful ad campaign, these tools can help you secure the capital you need when you need it. Onramp integrates with popular marketplaces like Amazon, Shopify, and TikTok Shop and provides transparent fees (ranging from 2–8%), with no hidden surprises. This proactive financing approach can help you seize opportunities before they pass you by.

Smart operators don’t wait for financial emergencies - they secure credit lines in advance. By aligning your funding strategy with your business goals and staying proactive with financial planning, you can safeguard your profits, maintain control of your business, and set the stage for sustainable growth.

FAQs

How do I know if I need planned or emergency borrowing?

To figure out whether you need planned borrowing or emergency borrowing, think about the timing and purpose of your financial need.

- Planned borrowing is for expected expenses, like stocking up on inventory for a busy season or preparing for a new project. It gives you the chance to plan ahead and secure funding in advance.

- Emergency borrowing, on the other hand, is for sudden, unexpected needs - like an unanticipated cash flow issue - that demand quick action.

If your borrowing ties into long-term growth or planned investments, it’s planned. If it’s about handling an urgent, unforeseen situation, it falls under emergency borrowing.

How much funding buffer should I keep to avoid cash crunches?

To steer clear of cash flow issues, eCommerce businesses should keep a funding cushion that matches their inventory and cash flow cycles. A practical rule of thumb? Aim for enough liquidity to cover 30–60 days of operating expenses and inventory costs. Keeping an eye on metrics like Days Inventory Outstanding (DIO) and Days Sales Outstanding (DSO) can guide you in setting the right buffer size. This approach helps maintain financial stability, even during slow sales periods or when unexpected costs arise.

What funding type best matches my inventory or ad spend cycle?

The right type of funding largely depends on what you're aiming to achieve. If you're working on growth-oriented goals - like boosting inventory levels or running seasonal ad campaigns - growth capital is a solid choice. It’s designed to fuel long-term expansion efforts. On the other hand, if you’re tackling short-term challenges such as cash flow gaps or unexpected costs, survival capital (like merchant cash advances) is a better fit.

The key is to match your funding to your business's current stage: use growth capital for strategic investments and survival capital for pressing, day-to-day operational needs.