Your revenue performance directly impacts how much you can borrow for your business. Lenders evaluate your sales consistency, growth trends, and cash flow to determine funding eligibility. Revenue-based financing connects to your eCommerce platforms like Shopify or Amazon, using real-time data to offer funding that adjusts with your sales. Here's the key takeaway:

- Higher revenue = Higher borrowing capacity: As your sales grow, lenders offer more funding with better terms.

- Flexible repayment: Pay back a percentage of daily sales instead of fixed monthly amounts.

- Quick access to funds: Approval and deposits can happen within 24 hours.

To increase borrowing capacity, focus on consistent sales, customer retention, and diversifying sales channels. Use tools like Onramp Funds to estimate your funding potential and reinvest in inventory and marketing to drive growth. Revenue-based financing scales with your success, offering the working capital you need to grow without overextending financially.

How Revenue-Based Financing Works

What Revenue-Based Financing Means

Revenue-based financing provides a way to secure capital without sacrificing ownership in your business or committing to fixed monthly debt payments. Instead of adhering to a rigid repayment schedule, you pay back a percentage of your daily sales - contributing more on busy days and less when sales slow down. This approach blends elements of both debt and equity, allowing you to access funds while maintaining full control of your business [1][2].

This structure is especially well-suited for the unpredictable nature of eCommerce, where daily sales can vary significantly [3]. With remittance rates starting as low as 1% of daily sales, there are no monthly minimums, fixed payments, or hidden fees to worry about [3].

Curious about how Onramp Funds tailors this model to your business? Let’s break it down.

How Onramp Funds Calculates Your Borrowing Limit

Onramp Funds streamlines the process by linking directly to your eCommerce platforms - such as Amazon, Shopify, Walmart, or TikTok Shop - to evaluate your real-time sales and cash flow [1][4]. The integration is quick, taking just 5 minutes, with an initial funding estimate provided in as little as 1 minute [3]. By analyzing transaction patterns, monthly revenue averages, and growth trends, Onramp creates funding offers tailored to your business’s performance.

To qualify, your business must generate at least $3,000 in average monthly sales and operate as a legal U.S. entity, such as an LLC or S-Corp [4]. Once connected, funding offers are available within 2 hours, and approved funds are deposited into your account within 24 hours [1][3]. This data-driven approach ensures that your borrowing limit aligns with your revenue, supporting growth while minimizing financial risk. Essentially, your business’s performance directly influences your access to capital, enabling funding that scales with your success [4].

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales." - Jeremy, Founder and Owner of Kindfolk Yoga [4]

Revenue Metrics That Affect Your Borrowing Limit

What Lenders Look at in Your Revenue

When determining how much you can borrow, lenders focus on specific revenue metrics that highlight your financial health and ability to repay. Net Revenue - which accounts for gross sales minus returns, discounts, and fees - is more insightful than total sales. It reveals the actual cash your business retains [7][9]. Keeping return rates low further clarifies your net revenue.

Another key metric is Gross Profit Margin, which shows the funds left after covering the cost of goods sold (COGS). For eCommerce businesses, the average gross profit margin is 41.54% [5][7]. Strong Net Profit Margins, typically between 10% and 20%, indicate a stable and resilient financial position [7].

Lenders also evaluate your Revenue Growth Rate, tracking how your sales grow month-over-month or year-over-year [5][8]. Average Order Value (AOV) - calculated as total revenue divided by the number of orders - offers insights into customer spending patterns and pricing strategies [7][9]. Metrics like Churn Rate and Repeat Purchase Ratio help assess how consistent and predictable your sales are, giving lenders a clearer picture of future revenue potential [5][9]. Together, these metrics provide a well-rounded view of your business's financial strength.

"What is not defined cannot be measured. What is not measured, cannot be improved. What is not improved, is always degraded." - William Thomson Kelvin, Physicist [7]

Why Real-Time Data Integration Matters

Static numbers only tell part of the story. Real-time data takes financial assessments to the next level. By linking your eCommerce platforms - such as Amazon, Shopify, Walmart, or TikTok Shop - directly to Onramp Funds, you provide a live snapshot of your sales performance [4][6][7]. This read-only connection enables the system to analyze your complete sales history and offer a cash advance tailored to your current business performance [4]. Instead of basing borrowing limits on outdated figures, this approach ensures funding aligns with your present revenue and cash flow, helping you avoid overextending financially [4].

Businesses that use data effectively in decision-making are 6% more profitable than those that don’t [9].

"Metrics serve as a compass for marketplace businesses, guiding decision-making, strategic planning, and operational adjustments." - Stripe [9]

How to Increase Your Borrowing Capacity by Growing Revenue

Creating a Consistent Revenue Track Record

Building a steady revenue history is key to unlocking higher borrowing limits. Lenders look closely at your digital sales data, conversion rates, and seasonal trends to decide how much funding to provide [12]. One way to ensure consistent revenue is by optimizing inventory management. Running out of stock can disrupt your cash flow and hurt your reputation, both of which can limit your borrowing potential. Considering that cash flow issues are responsible for 82% of small business failures [10], maintaining a smooth inventory flow safeguards your income and strengthens your financial standing.

Focusing on customer retention can also pay off significantly. Acquiring a new customer is 5-25 times more expensive than retaining an existing one [11]. Using CRM tools and offering installment payment options can improve customer loyalty and stabilize monthly sales. Businesses that implement installment plans often see a 20-30% boost in conversion rates and a 30-50% increase in average order value [11][13].

Another effective strategy is diversifying your sales channels. Selling on platforms like Amazon, TikTok Shop, and even in international markets can broaden your revenue streams, which makes your business more appealing to lenders [13]. Paul Voge, Co-founder and CEO of Aura Bora, took this approach and secured credit limits 30 to 40 times higher than what traditional banks like Chase or Amex offered. This allowed Aura Bora to cover upfront inventory costs while waiting for customer payments [12].

"Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital." - Paul Voge, Co-founder and CEO, Aura Bora [12]

Seasonal trends can further enhance your borrowing capacity, so let’s dive into how to make the most of them.

Making the Most of Seasonal Sales

Seasonal sales events, like Black Friday or the Q4 holiday season, can significantly impact your borrowing potential. Lenders often connect to your store data in real-time to assess performance, and revenue spikes during these periods demonstrate your business’s earning potential [14][1]. Revenue-based financing providers typically offer funding that ranges from one-third of your annual recurring revenue to four to seven times your monthly recurring revenue [15].

To prepare for these high-revenue periods, use capital to stock up on inventory 2-4 months in advance. This ensures you’re ready to meet demand and avoid stockouts, which could negatively affect the revenue data lenders analyze for future funding decisions [1]. Additionally, running targeted ad campaigns during these peak times can maximize your sales. High-revenue months often lead to faster repayment schedules, which can make you eligible for follow-on funding sooner [15][16].

During slower seasons, focus on SEO and website improvements. This positions your business to capture more revenue when the next peak season arrives [11][12].

Finally, let’s explore tools that can help estimate your borrowing potential.

Tools to Estimate Your Borrowing Limit

The Onramp Funds calculator offers a quick way to estimate your borrowing capacity. By entering your average monthly revenue, you can get results in about a minute [4][17]. For a more precise evaluation, link all your sales channels. The system analyzes your complete sales history across platforms like Amazon, Shopify, Walmart, and TikTok Shop to provide a tailored cash offer [1][4].

Unlike traditional banks that rely heavily on personal credit scores, these tools focus on your business performance data, current debt levels, and cash flow to determine your funding limit [1][4]. To qualify, your business needs to generate at least $3,000 in monthly sales and be legally registered in the U.S. [4][17]. Businesses using Onramp’s revenue-based financing have reported an average revenue growth of 73% within 180 days of receiving funding, and 75% of customers choose to borrow again [17].

Once you secure funding, invest it in inventory and marketing efforts. These activities directly improve the revenue metrics that lenders use to calculate your next borrowing limit [1].

"Applied, got our offer, and had cash in our bank account within 24 hours. Their Austin, TX based team was very professional and helped me deploy the cash to effectively grow our business." - Nick James, CEO of Rockless Table [4]

sbb-itb-d7b5115

How to get Revenue-based Financing for your Shopify Store?

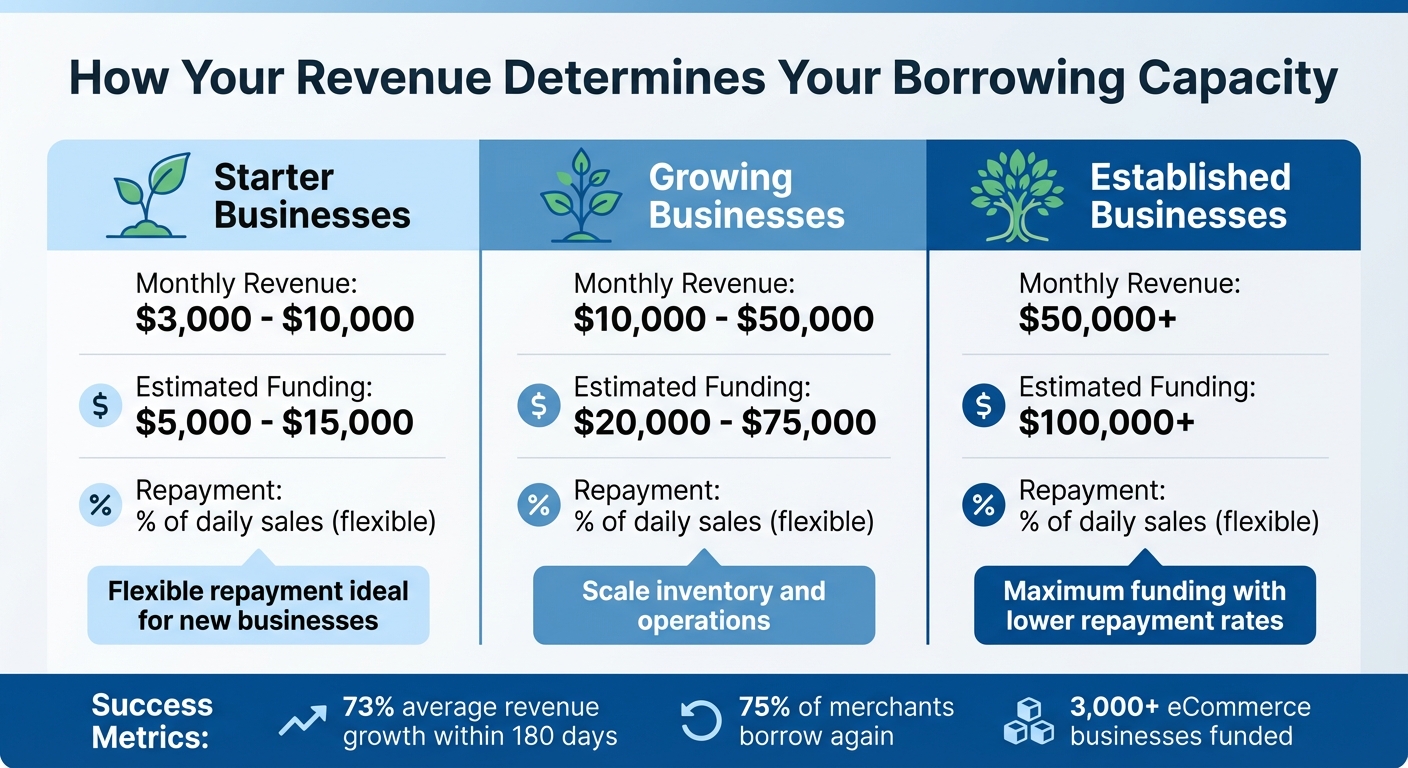

Revenue Levels and Borrowing Amounts

Revenue-Based Borrowing Capacity: Monthly Revenue vs Funding Amounts

How Revenue Ranges Connect to Funding Options

Your monthly revenue plays a key role in determining your funding options. Lenders assess your sales history, cash flow, and existing debt to ensure you’re not borrowing more than your business can handle [4]. Funding decisions are based on real-time performance data pulled from your connected platforms [1].

As your revenue grows, so does your borrowing capacity. Higher revenue not only qualifies you for larger funding amounts but also improves your terms, like reducing the percentage of daily sales used for repayment [3]. Essentially, the more your business thrives, the more favorable your financing conditions become.

Repayment is designed to adjust with your sales - if your revenue dips during slower months, your repayment decreases, and during busy periods, it increases [4][1]. This flexible, revenue-based model eliminates the pressure of fixed monthly payments, which can strain cash flow during off-peak times. The borrowing framework below breaks down how revenue levels translate into funding options.

Table: Revenue Range vs. Borrowing Amount

| Revenue Range (Monthly) | Estimated Funding | Repayment Structure | Key Benefits |

|---|---|---|---|

| $3,000 - $10,000 | $5,000 - $15,000 | Revenue-based (% of sales) | Flexible repayment; ideal for small or new businesses |

| $10,000 - $50,000 | $20,000 - $75,000 | Revenue-based (% of sales) | Larger funding amounts; great for scaling inventory or operations |

| $50,000+ | $100,000+ | Revenue-based (% of sales) | Access to maximum funding; lower repayment rates relative to revenue |

This model has already supported over 3,000 eCommerce businesses, with merchants experiencing an average revenue growth of 73% within 180 days of receiving funding [17]. The system works because it aligns lender success with your business growth. As your revenue increases, your borrowing potential expands, and 75% of merchants opt to borrow again [17]. Check the table above to see how your revenue range could translate into funding opportunities.

Conclusion

Your revenue performance is the cornerstone of your borrowing power. Lenders and platforms like Onramp Funds assess key factors such as your sales history, consistency, and real-time metrics to determine funding eligibility. As your monthly revenue grows - say, from $10,000 to $50,000 or more - your funding limits increase in step, providing the working capital you need to stock up on inventory before Black Friday, ramp up ad campaigns, and steer clear of stockouts.

Boosting your sales not only unlocks greater funding but also creates a cycle of reinvestment in inventory and marketing. With flexible repayment terms that align with your sales cycles, this approach helps you maintain cash flow while scaling your business.

To make the most of this growth opportunity, focus on tracking at least 12 months of sales, maintaining accurate records, and leveraging real-time data. Direct your funding toward activities that drive revenue, such as high-turnover inventory, successful ad campaigns, or improvements in fulfillment.

That said, higher borrowing capacity comes with responsibility. While revenue-based financing adjusts repayments to your sales performance, overextending your capital can strain margins if growth doesn’t meet expectations. Be strategic - monitor essential metrics like inventory turnover and contribution margin, and reassess your funding limits as your revenue evolves.

Take a closer look at your sales trends and see how Onramp Funds can help bridge the gap between where you are now and where you want to go. Consistent revenue growth sets the stage for flexible and scalable financing options.

FAQs

What makes revenue-based financing different from traditional loans?

Revenue-based financing gives businesses the option to repay a set percentage of their monthly revenue. This approach is ideal for companies with fluctuating income because payments adjust based on earnings. Plus, it skips the need for collateral or personal guarantees, and the approval process is usually quicker and less dependent on credit scores.

In contrast, traditional loans come with fixed monthly payments, no matter how much revenue a business generates. They often require collateral and involve a more detailed and time-consuming underwriting process. For businesses needing fast and flexible funding that aligns with their cash flow, revenue-based financing can be a much more practical choice.

What key factors can help improve my borrowing capacity as an eCommerce business?

To improve your borrowing power, prioritize steady revenue growth and a strong monthly sales track record. Maintaining healthy cash flow, keeping existing debt low, and showcasing a reliable history of operations are equally important. On top of that, make sure both your business and personal credit scores are solid, and keep your financial records organized and up-to-date.

Lenders also appreciate when businesses integrate with major eCommerce platforms and use tools that clearly display revenue metrics. Highlighting these strengths can help your business stand out when seeking financing opportunities.

How fast can I get funding with revenue-based financing?

With revenue-based financing, getting funds is often a swift process - sometimes as fast as 24 hours. Generally, funds are transferred within 1 to 3 business days, though this can vary based on the lender and your particular situation.

This quick access to capital makes it a great choice for eCommerce businesses aiming to capitalize on growth opportunities or handle cash flow needs with ease.