The Ups and Downs of eCommerce

Online selling has completely transformed how we buy and sell products. Statista reports that the broader eCommerce market that includes B2C retailers, B2B companies, and C2C sellers (those who sell products on eBay, Etsy, and Amazon) is approaching $500 billion. The COVID pandemic has only added fuel to the fire.

With more than 2 billion people worldwide purchasing online, there’s plenty of opportunities for sellers to capture an audience and build a brand. While they have every opportunity to be optimistic, the truth is there are still challenges, specifically when it comes to eCommerce funding. eCommerce sellers shouldn’t have a one-size-fits-all approach to financing; they need access to multiple funding sources that are aligned with a specific purpose.

eCommerce Financing Challenges

Are you an online seller or considering it? As with any budding business, you will need to secure different types of financing for different purposes. Business loans, for instance, are ideal for longer-term assets, such as leases, equipment and real estate leases. Those products are easy to find.

But short-term funding is a different story. Cash flow to purchase inventory is almost always a concern, and eCommerce funding options that are built for the unique conversion cycles of an eCommerce business are relatively scarce. Traditional financing such as business credit cards and short-term loans have yet to catch up with how eCommerce businesses operate. But you can find short-term funding alternatives geared specifically for eCommerce sellers who need cash flow support.

This guide to eCommerce funding will help you analyze your financing options and learn about an innovative, short-term financing solution that is the only one built to serve the unique needs of online sellers.

Cash Flow Woes

Getting your hands on cash is almost always cited as a business growth roadblock. A commonly cited U.S. Bank study found that 82% of small businesses fail because of cash flow problems, and 29% run out of cash.

There are plenty of culprits, but the takeaway is that even conventional businesses suffer from cash flow issues. eCommerce businesses are likely at more risk because the vast majority of funding methods are built for traditional retail, not eCommerce. Traditional financing products used by small businesses - like credit cards - aren’t designed for the unique requirements of eCommerce. They don’t map to supply chain replenishment timelines, sales cycles, or inventory turnover performance.

Without cash, or maybe we should say, without cash that has so many strings attached, eCommerce sellers can’t ever get ahead. You can’t keep your head above water without growth capital, but traditional banks and credit card companies only offer long-term products that don’t align with these shorter eCommerce lifecycles.

Before we get to a more innovative funding option that is purposely built for online sellers, let’s review the traditional funding options most commonly found in a capital stack.

The Small Business Capital Stack

The capital stack will have short-term, mid-term, and long-term financing options broken into debt and equity options. These funding types are ideal for different types of costs. For instance, you will have various expenses, including inventory, marketing and advertising, facilities, shipping, headcount, technology, and other operating costs.

There is no single funding option that is ideal for all of these expenses; therefore, you need to build a diverse capital stack to account for your various expenses as you grow.

There are several types of capital to consider in your stack. Here are the most common for online startups or small businesses:

Debt Financing

Bank loans and lines of credit

Perhaps the most familiar type of funding is senior debt. Banks offer interest-based, multi-year fixed loans and lines of credit, where you can spend the money any way you want but are required to make a minimum monthly payment or suffer a penalty charge.

Long-term loans have lower interest rates and you pay off that debt over 20 or 30 years, much like a mortgage. Mid-term loans are generally 12 months and have higher rates (typically around 12%) than their longer-term counterparts.

While these loans are ideal to finance longer-term assets, they aren’t designed for short-term assets like inventory or marketing efforts. If you don’t sell product to cover repayment, you quickly can rack up debt and run out of cash.

Banks and traditional lenders don’t often offer a short-term option other than a line of credit, which require proof of profitability before they’ll even consider it. Once you have enough revenue in the bank, with a line of credit, you can borrow any amount from that line when you need it, but these are similar to credit cards or loans. You’ll have to make minimum monthly payments whether you have revenue coming in or not, and lines of credit have fluctuating rates you can’t budget for.

With all of these lending options, the approval process takes typically two-to-three months and requires you to provide a long history of financial and personal paperwork. The lending institution will review your financial history, credit score, debt to credit ratio, and your business operations before approving or declining your loan application.

Credit cards

Business or personal credit cards are relatively quick and easy to obtain and give you the freedom to spend as you wish, but they come with a credit limit and monthly minimums that don’t care about whether you have revenue coming in. While some offer attractive introductory interest rates, be aware that those rates often increase after the first year. Your rate will be based on your creditworthiness and payment history.

Your balance accrues with interest unless you pay off your debt in full each month. In most cases, you will be granted larger credit limits with business credit cards than personal accounts, and you will begin to build your business credit. As your business credit score increases and your payment history strengthens, the credit card lender is more apt to increase your credit limit.

Cash Advances

These products have found their way into eCommerce and most are based on traditional lending metrics and collections expectations. As with most bank products, there is a lack of understanding of specific eCommerce business drivers, and they are not always aligned with your eCommerce performance.

There are a couple of types of cash advances: a daily advance is best for getting sales dollars in before your sales channel makes a deposit. A short-term advance supports sales and inventory turnover. Both are fee-based.

Equity Financing

Investors

There are several stages involved with equity financing. Also known as seed capital, the first stage of financing is for startups. Seed capital is just enough money to cover the essentials, including a business plan and initial inventory. Its primary goal is to attract more financing, either from banks or venture capitalists who will want to see some operating history before they invest.

Once you can show promise and stability, you can seek venture capital financing. Private equity financing is reserved for more established companies. For startups, venture capital is your best bet.

The biggest issue with these routes is that they are not easy to obtain and you lose some control of your company. Even if you do get investors’ attention, it can take up to six months to get approved and funded.

Unless you are able to obtain investment capital from friends and family who are willing to loan you the money without the expectation of ownership shares, your investors will demand a percentage equity stake in your company and/or a share in the profits of your product.

Private equity firms gain a majority stake in your company, make operating decisions, and look to improve and then sell your business for a profit; venture capital firms take a minority stake, lend their expertise and connections, and are more interested in the long-term growth of your company.

Bootstrapping

Bootstrapping is simply using your own savings (or donations from friends and family) and your company’s cash flow (if any) to fund your business and its growth. Bootstrapping often leverages short-term funding solutions like credit cards and cash advances as the amounts are typically smaller and manageable for payoff over a few months. You retain 100% ownership of your company, but you have to have enough cash to keep it going. This may mean depleting your savings or retirement funds and increasing your debt, adding significant risk to your venture.

Another disadvantage of bootstrapping is that it often won’t pay for larger investments, such as purchasing a warehouse. Without the necessary funds, you can quickly run out of money and hit a wall when it comes to growth. Many entrepreneurs and startups begin with this route and then seek additional funding types to sustain their growth.

Crowdfunding

A relatively recent option is crowdfunding, where you present your business on an online platform to anyone interested in investing. With this financing type, you retain complete ownership of your company and do not have to repay your investors. It can also be a good way of attracting customers early on to build some momentum.

Crowdfunding has a dismal success rate, however. Less than 23% of crowdfunding campaigns are successful, and the average amount raised is less than $6,000. You will also have to give a portion of what you raise back to the platform on which you advertised your campaign. And because crowdfunding platforms are public forums, you risk someone taking your idea. If your idea fails, it can be even more difficult to get investors to buy in to your business plan.

Funding your eCommerce Business

eCommerce Working Capital

Even though the traditional financing options have their merit in certain circumstances, eCommerce sellers need more modern financing. eCommerce cash advances are built specifically for online sellers and how eCommerce works. This relatively new funding option is becoming popular among online sellers because it is completely aligned with the sales cycle, has no interest and requires no minimum monthly payments.

Onramp was one of the first to enter the market with its eCommerce working capital product. It’s a flexible option that works well in a diverse capital stack, allowing business owners to scale expenses up and down as they arise, such as purchasing more inventory or investing in marketing, advertising, and headcount.

In this model, you can borrow money and pay it back as you sell products. Here’s how it works:

You create an account and request a capital amount. Onramp connects to your store via a read-only API to see how sales are going before they pre-qualify you for funds. This process takes about 10 minutes.

Once approved, you connect your bank, and within 24 hours, they deposit money into your bank account. Instead of making payments to repay your “loan,” the company takes a small percentage of sales from your account automatically after your product sells, much like a royalty payment. You don’t have any recurring monthly bills, minimum payment requirements, late charges, or interest. Your payments are automatically debited from your bank account.

With payments synchronized with your sales cycle, Onramp only takes money out of your account when you get paid by your customers. No sales, no debits. Increased sales, increased debits that go towards paying off your balance. This model not only reduces your stress but your costs, saving customers an average of 50% over the traditional options listed above.

Let’s look at how this model benefits an online seller. First, if your sales are cyclical or seasonal, you don’t have to worry about not being able to make a payment when sales are dragging. As soon as sales pick back up, you resume payments. And the stronger your sales, the faster you repay the balance and request more funds.

How to Balance Different Funding Options to Grow Your Business

As we said, there likely isn’t a single funding option that covers all of your business needs from startup through your growth phases. Even with the eCommerce funding, you need to have some consistent sales under your belt before you can obtain financing. The key is to build the right balance in your capital stack to achieve your goals and provide the necessary cash at the right time.

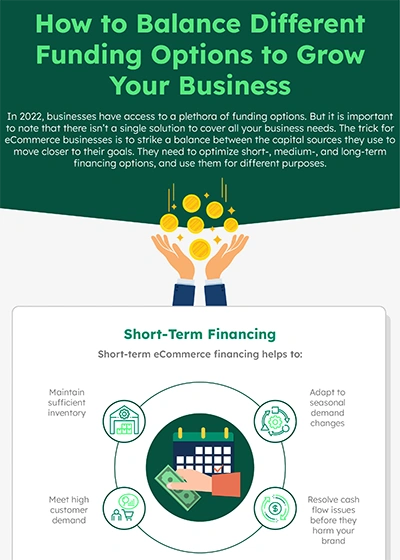

Short-Term Needs

For short-term cash flow needs such as maintaining proper inventory levels to meet demand, the eCommerce funding option is ideal. Consider this working capital that turns over every 60-120 days. It will provide you with a quick way to get the cash you need without all of the red tape and risk. For instance, if you see demand is outpacing supply, you can immediately purchase more inventory without worrying about increasing your debt.

One note with inventory: stockouts are one of the most dangerous threats to your business. If you run out of inventory to fulfill purchase orders, you significantly increase the risk of lost sales. Customers, especially those who shop on Amazon, expect their products to be in stock and delivered to their door within a day or two. If you can’t fulfill an order quickly, they will almost always go elsewhere.

This reality makes having working capital in hand essential. If you simply charge it to a credit card, unless you sell that stock before your payment is due, you aren’t going to be able to pay back the borrowed money, and your debt increases. However, with eCommerce financing, you have peace of mind that you won’t go into debt by purchasing inventory that doesn’t immediately sell.

Mid-Term Needs

If your sales are strong, you can likely still take advantage of eCommerce funding for slightly larger purchases, such as hiring an advertising or marketing agency to promote your brand across different channels or investing in technology. Otherwise, you can look to credit cards, lines of credit, or short-term loans - but be aware that these are debt financing options that increase your costs over time.

Long-Term Needs

Long-term loans may be best to fund larger expenses as you grow, such as purchasing a warehouse, hiring an executive or expanding headcount. In this case, traditional bank loans may be best as they are geared towards bigger costs you can pay off over time. These will enable you to pay off the debt over an extended period, making your payments more manageable.

Align Funding with Business Need

As an online seller, you have financing options available that didn’t exist even a few years ago. Thankfully, companies like Onramp have stepped up. By strategically leveraging different financing types and the right time, you can set your company up for the greatest chance of success.

Yes, cash flow is a common challenge for any business, but eCommerce financing is an excellent way to obtain working capital without all of the risk associated with traditional funding. By having your payments synchronized with actual sales, you lower your risk, costs and headaches.

Want to learn more about how eCommerce funding works and how it can give you the working capital you need to grow your business on your own terms? Talk with Onramp, get cash in days and work with a funding partner that wants to see you succeed.