Merchant cash advances (MCAs) might seem like a quick fix for eCommerce cash flow issues, but they often come with serious downsides. High fixed costs, rigid repayment terms, and APRs ranging from 80% to 200% can cut deeply into profits. Many businesses, like Rogers Landworks LLC, have fallen into debt cycles, with MCA-related bankruptcies more than doubling between 2023 and 2025.

Instead, revenue-based financing offers a smarter alternative. Repayments adjust with sales, there's no collateral or personal guarantees, and fees are transparent. This approach provides flexibility without sacrificing control or profitability, making it a better fit for the unpredictable nature of eCommerce sales.

Key Takeaways:

- MCAs are fast but costly, with APRs up to 200%.

- Fixed payments clash with seasonal sales patterns.

- Revenue-based financing ties repayments to sales and avoids hidden costs.

- Onramp Funds simplifies funding with clear fees and fast approvals, helping eCommerce businesses grow sustainably.

How High-Cost Funding Hurts eCommerce Businesses

High Interest Rates Cut Into Profits

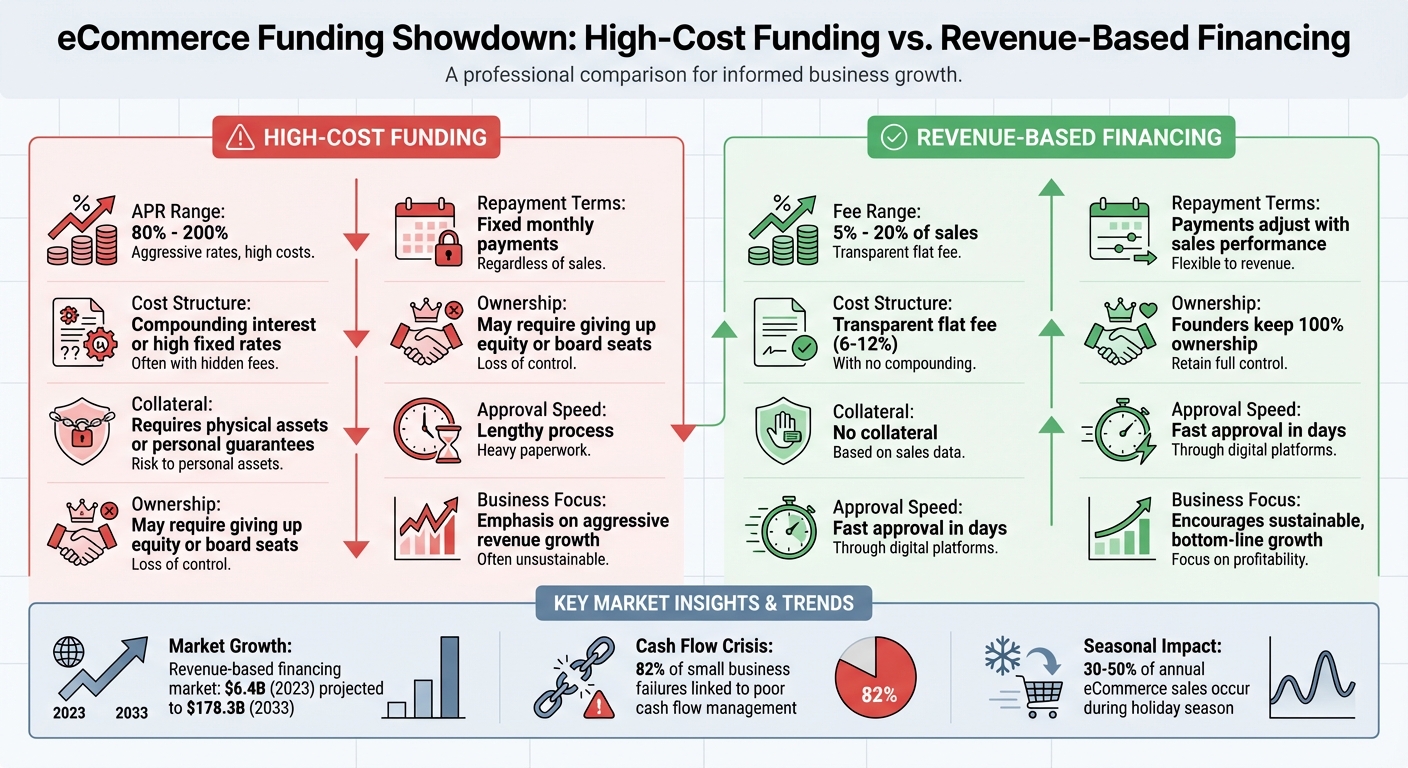

High-cost funding options, like merchant cash advances (MCAs), can put eCommerce businesses in a tough spot. While baseline capital rates hover around 5% [2], MCAs often come with steep annual percentage rates (APRs). These high rates force businesses to juggle debt payments alongside crucial expenses like inventory, marketing, and shipping [1]. Considering that shipping alone can eat up 10–20% of total revenue [3], such funding can make turning a profit feel like an uphill battle.

"By tying up cash in inventory, software, or unnecessary operational expenses prior to making the sales to justify such expenditures, ecommerce startups are putting themselves in a position of risk that they may not be able to overcome."

– Alex Back, Founder and CEO, Couch.com [1]

The burden of servicing expensive debt often pushes founders to focus on aggressive revenue growth just to meet repayment deadlines. This can overshadow strategies like improving customer lifetime value or fostering organic growth [2]. For direct-to-consumer (D2C) brands, this approach is particularly risky. Many publicly traded D2C companies have seen their valuations plummet by over 80% since going public [2].

Fixed Payments Don't Match Sales Patterns

Seasonality plays a huge role in eCommerce revenue, with 30–50% of annual sales typically happening during the holiday season [3]. But high-cost funding often comes with fixed daily or weekly payments, regardless of how sales fluctuate. This creates a major issue when businesses face the slow months of January but are still required to make the same payments they managed during December's sales boom.

Adding to the strain, payment processors usually hold funds for 2–7 business days [3]. When combined with rigid repayment schedules, these delays can turn minor cash flow issues into full-blown crises. As D2C businesses scale, they also face growing fixed costs like warehousing, insurance, and utilities. Layering inflexible debt repayments on top of these expenses during low-sales periods can severely impact operations [2].

Credit Damage and Limited Future Options

High-cost funding can trap businesses in a cycle of financial strain. For example, a disappointing peak season can leave debt obligations lingering for months, limiting access to future financing [3]. This issue becomes even riskier when personal guarantees are involved, as entrepreneurs could end up putting their personal finances on the line [3].

"With market volatility on both the supply and demand side... it can be very hard to have all of the variables align towards a positive cash flow situation."

– Alex Back, Founder and CEO, Couch.com [1]

In volatile markets, investors are often reluctant to provide additional funding, leaving businesses with high fixed costs and few options to reposition their assets [2].

Locked-Up Capital Limits Growth Opportunities

High-interest debt can drain resources that might otherwise go toward marketing, technology, or inventory [3][4]. This creates a constant need for immediate returns, which stifles long-term planning and strategic growth.

"Cash flow management is one of the biggest financial challenges for eCommerce businesses. It can be tricky to balance inventory costs, marketing expenses, and operational overheads while waiting for sales revenue to come in."

– Mark Shust, Magento Educator and eCommerce Consultant [1]

When funds are tied up in inventory or other assets and debt repayments are due before those assets become liquid, businesses face liquidity crises [2]. Without accessible capital, companies struggle to reinvest in proven marketing strategies or maintain a financial cushion for unexpected challenges [1]. This lack of flexibility can stall the organic growth necessary for sustainable scaling.

sbb-itb-d7b5115

How To Fund Your Ecommerce Business For Cheap (Or Even Free)

Better Funding Options for eCommerce

High-Cost Funding vs Revenue-Based Financing for eCommerce

Running an eCommerce business can be tough, especially when expensive funding options put a strain on your cash flow. One alternative worth considering is revenue-based financing, which adjusts repayment based on your sales performance. Instead of sticking to fixed monthly payments - regardless of how your business is doing - this model takes a small percentage (typically 5%–20%) of your daily or weekly sales until the repayment amount is met [5]. When sales are booming, you pay more; when they slow down, you pay less. This flexibility can help you avoid cash flow problems during slower months.

Revenue-based financing is built on a flat fee model. For example, if you borrow $100,000 with a 6% fee, your total repayment is $106,000 - no surprises [5]. Repayment caps generally range from 1.2 to 3 times the borrowed amount [6], so you know exactly what you owe from the start.

"Revenue based financing is often a far more compelling proposition for Founders than venture capital or business loans... primarily, Founders get to keep full ownership of their business... and there is no risk of default as there is with a loan."

– Michele Romanow, President and Co-founder, Clearco [8]

This flexible repayment approach aligns with your sales, ensuring you’re not overburdened during slower periods.

Unlike traditional loans, revenue-based financing doesn’t require collateral or personal guarantees. Instead, it relies on your sales data from platforms like Amazon or Shopify [5]. This means you’re not risking your home or personal assets. Plus, approvals happen quickly - often in just a few days - by using real-time sales data rather than lengthy credit checks [5].

The popularity of this funding model is growing fast. The revenue-based financing market, valued at $6.4 billion in 2023, is projected to skyrocket to $178.3 billion by 2033 [7]. For eCommerce businesses that deal with seasonal fluctuations and tight margins, this option provides the flexibility to invest in inventory or marketing without sacrificing control or profitability.

Comparison: High-Cost Funding vs. Revenue-Based Financing

Here’s a quick look at how revenue-based financing stacks up against traditional high-cost funding:

| Feature | High-Cost Funding | Revenue-Based Financing |

|---|---|---|

| Repayment Terms | Fixed monthly payments, regardless of sales | Payments adjust with your sales performance |

| Cost Structure | Compounding interest or high fixed rates, often with hidden fees | Transparent flat fee (e.g., 6–12%) with no compounding |

| Collateral | Requires physical assets or personal guarantees | No collateral; based on sales data |

| Ownership | May require giving up equity or board seats | Founders keep 100% ownership |

| Approval Speed | Lengthy process with heavy paperwork | Fast approval in days through digital platforms |

| Business Focus | Emphasis on aggressive revenue growth | Encourages sustainable, bottom-line growth |

For eCommerce entrepreneurs, revenue-based financing offers a practical way to manage cash flow while keeping control of your business. It’s a modern solution tailored to the unique challenges of online retail.

How Onramp Funds Solves These Problems

Onramp Funds provides a financing solution designed specifically for the unpredictable nature of eCommerce sales. Unlike traditional loans with rigid terms and compounding interest, Onramp uses real-time sales data to create funding options that align with the ups and downs of your business.

Repayments Based on Your Sales

With Onramp Funds, repayments are tied directly to your daily sales. You contribute as little as 1% of your daily revenue[9]. This means when sales slow down during off-seasons, your payments automatically decrease to match. For those who prefer a steady repayment plan, there's also an option for fixed payments with a locked-in APR, so you always know exactly how much you'll pay each time[9].

"Sales can be like a rollercoaster, and making sure there's enough money to keep things running during the slow dips is tough."

– Rhett Sturbbendeck, Finance and Insurance Expert[1]

This adaptable repayment system ensures that cash flow challenges don’t derail your operations.

Fast Funding with Clear, Fixed Fees

Speed and transparency are at the heart of Onramp’s funding process. You can get an initial estimate in just one minute and receive full funding within 24 hours - much faster than the weeks of paperwork required for a bank loan[9]. The cost is simple: a flat fee ranging from 2% to 8% of the borrowed amount[9]. For instance, if you borrow $50,000 with a 6% fee, your total repayment will be $53,000. No hidden charges, no multiplying interest - just clear terms you can plan around.

Onramp customers experience an average revenue increase of 60% after receiving funding, and 75% return for additional financing[9]. This straightforward approach helps businesses grow without the burden of traditional high-interest loans.

Works with Your eCommerce Platform

Onramp Funds seamlessly connects with major eCommerce platforms like Amazon, Shopify, Walmart, and TikTok Shop[9]. The integration process takes only five minutes[9]. Once connected, the system analyzes your real-time sales data to create funding offers tailored to your unique business needs. Payments are then automated, calculated as a percentage of daily sales, so you don’t have to worry about tracking or missing deadlines.

The platform has earned an "Excellent" rating from 225 reviews[9], with users frequently highlighting the ease of the process and the helpfulness of the support team.

"Onramp has been the bridge when it came to quick capital for additional inventory."

– Ashunta, Verified User[9]

Conclusion

Managing high-cost funding is a tough hurdle for eCommerce businesses. Fixed repayment schedules often clash with seasonal sales fluctuations, while compounding interest eats into already slim profit margins. With 82% of small business failures linked to poor cash flow management[10], choosing the wrong funding option can make or break your success.

Revenue-based financing offers a practical alternative to these challenges. Repayments adjust based on daily sales, keeping cash flow steady even during slower periods. Plus, transparent fees mean you’ll know exactly what you’re paying from the start - no surprises.

Onramp Funds provides a tailored solution for eCommerce sellers. By connecting directly to your store, it automates repayments as a percentage of daily revenue. On average, customers see a 60% increase in revenue and a 75% return rate for additional funding[9], showcasing the effectiveness of this approach.

"Financing should be viewed as a growth tool and as an opportunity."

– Oliver Whelan, Chief Revenue Officer, Storfund[11]

The right funding solution can align with your sales cycles and fuel long-term growth. Whether you’re expanding to new platforms, taking advantage of bulk inventory discounts, or building cash reserves for seasonal slowdowns, choosing wisely will help your eCommerce business thrive while keeping your cash flow intact.

FAQs

How do I know if my funding is “too expensive”?

Funding becomes “too expensive” when its costs - such as steep interest rates, hefty fees, or inflexible repayment terms - put a strain on your cash flow. This can make it challenging to handle everyday expenses, maintain inventory, or invest in opportunities for growth. If the funding eats into your profitability or forces you into unsustainable financial decisions, it’s a clear sign to reconsider. The right funding should help drive growth while keeping your financial health intact. If it doesn’t, the drawbacks likely outweigh any potential benefits.

What sales data do I need to qualify for revenue-based financing?

To be eligible for revenue-based financing, you’ll need to share sales data that reflects a steady flow of income. This usually involves providing monthly or quarterly sales reports that highlight your business's ability to maintain consistent revenue generation.

How much funding can I take without hurting cash flow?

The funding amount your business can handle depends largely on its cash inflows and outflows. Ideally, you should only borrow what your cash flow surplus can comfortably cover. Taking on excessive, high-cost funding could result in financial strain or disrupt operations. To stay on solid ground, align your funding needs with the surplus you can reliably predict.