Running an eCommerce business often requires balancing inventory costs with cash flow. Sellers face challenges like paying upfront for stock, managing ongoing expenses, and waiting for sales revenue. To address this, there are three main financing options:

- Revenue-Based Financing: Repayments adjust based on daily sales, offering flexibility during slow periods. Platforms like Onramp Funds provide quick approvals and funding within 24 hours.

- Trade Credit: Suppliers allow delayed payments (e.g., Net 30/60/90 terms), enabling sellers to sell inventory before paying for it.

- Inventory Lines of Credit: A revolving credit option secured by inventory, letting sellers borrow as needed and only pay interest on used amounts.

Each method helps sellers maintain cash flow while scaling their business, avoiding the strain of fixed repayment schedules or large upfront costs. Choosing the right option depends on sales patterns, supplier relationships, and operational needs.

Inventory Financing 101: What Business Owners Need to Know

Revenue-Based Financing with Onramp Funds

Revenue-based financing offers a more adaptable way for businesses to access capital. Instead of being tied to fixed monthly payments - regardless of your sales - repayments adjust depending on how much revenue you’re generating. This model is especially helpful for eCommerce sellers, allowing them to increase inventory without putting unnecessary strain on cash flow. Onramp Funds focuses on this type of financing, providing funding that aligns with the natural ups and downs of your sales. It’s a practical way to manage cash flow while scaling your business.

How Onramp Funds Works

Getting started is straightforward. You simply connect your eCommerce platform - whether it’s Amazon, Shopify, TikTok Shop, Walmart, or another marketplace - so Onramp can view your sales data. This process only takes about five minutes and skips the need for personal credit checks or piles of paperwork. Once approved, funds are deposited into your account within 24 hours.

Repayment is just as simple. A set percentage of your daily sales is automatically deducted. When sales are strong, you pay more; during slower periods, payments scale down naturally.

"Applied, received our offer, and had cash in our bank account within 24 hours."

To qualify, your business needs to generate at least $3,000 in average monthly sales and be a U.S.-based legal entity, such as an LLC or C-Corp. This streamlined process eliminates unnecessary hurdles, making it an appealing option for eCommerce businesses.

Benefits of Using Onramp Funds

One of the biggest perks is speed - funding is available in less than 24 hours, a stark contrast to the lengthy timelines of traditional bank loans. Plus, you keep 100% ownership of your business since this isn’t equity financing. There’s no need for personal guarantees or collateral, reducing risk on your end.

The flexible repayment system is another major advantage. It ensures that you’re not overburdened during slower sales periods, keeping your cash flow intact.

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales."

Onramp’s track record speaks for itself. With over 3,000 eCommerce loans funded and an average revenue growth of 73% within six months, their approach clearly helps sellers grow inventory without the stress of fixed payments. They charge a single transparent fee - no hidden costs - and 75% of their customers return for additional funding. It’s a model built for scaling without surprises.

Using Trade Credit from Suppliers

What Trade Credit Means

Trade credit allows you to receive inventory upfront while delaying payment for 30, 60, or even 90 days. Essentially, it acts as a short-term, interest-free loan, giving you breathing room to manage your cash flow effectively[5][6]. As your orders grow, your accounts payable scale naturally, offering a built-in financing option to support your business growth[3][7][8]. In fact, about 60% of small businesses rely on trade credit to keep day-to-day operations running smoothly[7].

Paying your invoices on time isn’t just about avoiding late fees - it’s also a key way to build your business credit history. A solid credit record can unlock larger credit limits down the road, giving you even more flexibility[5][6]. Plus, many suppliers sweeten the deal by offering discounts for early payments, which can help you cut costs.

How to Negotiate Better Payment Terms

The best time to negotiate payment terms is during onboarding. Align these terms with your sales cycle. For example, if it typically takes 60 days to sell your inventory, aim for Net 60 terms. This way, your sales can cover the cost of the inventory before the invoice is due[3][7].

If you’re placing consistent or large orders, use that as leverage to secure better terms[4]. Smaller businesses can get creative - offering to spotlight the supplier in marketing campaigns or committing to exclusive sourcing can sometimes open the door to extended payment windows. Transparency also helps; sharing financial statements or trade references can show suppliers that you’re a trustworthy partner[3][6].

"Negotiating favorable payment terms becomes crucial... as it can help stabilize cash flow, mitigate the impact of rising costs, and maintain operational continuity."

– Yassir Malik, Sage

If a supplier pushes back on your request for Net 90 terms, propose a middle ground like Net 45 or Net 60 to build trust[4]. Another tactic is to ask for slightly more than you need - requesting Net 90 when you’re aiming for Net 60 - so there’s room to negotiate. Just remember to finalize pricing before discussing payment terms. Otherwise, suppliers might quietly raise unit costs to offset the extended credit period[9].

Lastly, consider exploring inventory lines of credit as another way to keep your funding flexible.

sbb-itb-d7b5115

Inventory Lines of Credit for Flexible Funding

How Inventory Lines of Credit Work

Inventory lines of credit function as a revolving credit option for businesses. Think of it as a financial safety net: you can borrow, repay, and borrow again, all within a preset limit. The best part? You only pay interest on the amount you actually use [10]. These credit lines are secured by your inventory, meaning there’s no need to put up personal assets as collateral [26,28].

The credit limit typically falls between 20% and 80% of your inventory’s liquidation value [26,30]. For instance, if your inventory is worth $100,000, your credit line might range from $20,000 to $80,000. Most lenders also set basic requirements, such as a personal credit score of 625–650 and at least 6–12 months of business operations [26,27].

These lines usually come with a draw period lasting 12–24 months, after which you’re expected to repay the principal [10]. Interest rates vary widely, from 8% to 30% with online lenders, while traditional banks often offer lower rates in the 3% to 9% range [26,30].

"Unlike a traditional term loan that gives you a lump sum loan upfront, a line of credit allows you to borrow, repay, and borrow again up to a preset limit."

– Nav [10]

Benefits for eCommerce Sellers

For eCommerce businesses, this type of funding can be a game-changer. Its primary advantage is flexibility: you can draw funds when needed and only pay interest on what you use [26,34]. This makes it particularly useful for managing seasonal sales cycles. For example, you can stock up on inventory ahead of major shopping events like Black Friday or Cyber Monday without depleting your cash reserves [29,31].

Another perk is the ability to negotiate better deals with suppliers. With instant access to capital, you can place larger orders upfront and secure volume discounts. Online lenders often approve and fund these credit lines within one to two business days, ensuring you’re ready to act on time-sensitive opportunities [26,33,34].

However, it’s essential to account for additional fees. These may include origination fees (1%–3% of the credit limit), draw fees ($25–$100 per transaction), and monthly maintenance fees ($25–$50) [10].

To make the most of an inventory line of credit, consider integrating an inventory management system. This can help you align your borrowing and repayment schedule with your sales cycle, ensuring smoother cash flow. Calculating your inventory turnover ratio (Cost of Goods ÷ Value of Inventory) is another smart move to figure out exactly how much credit you’ll need [26,31].

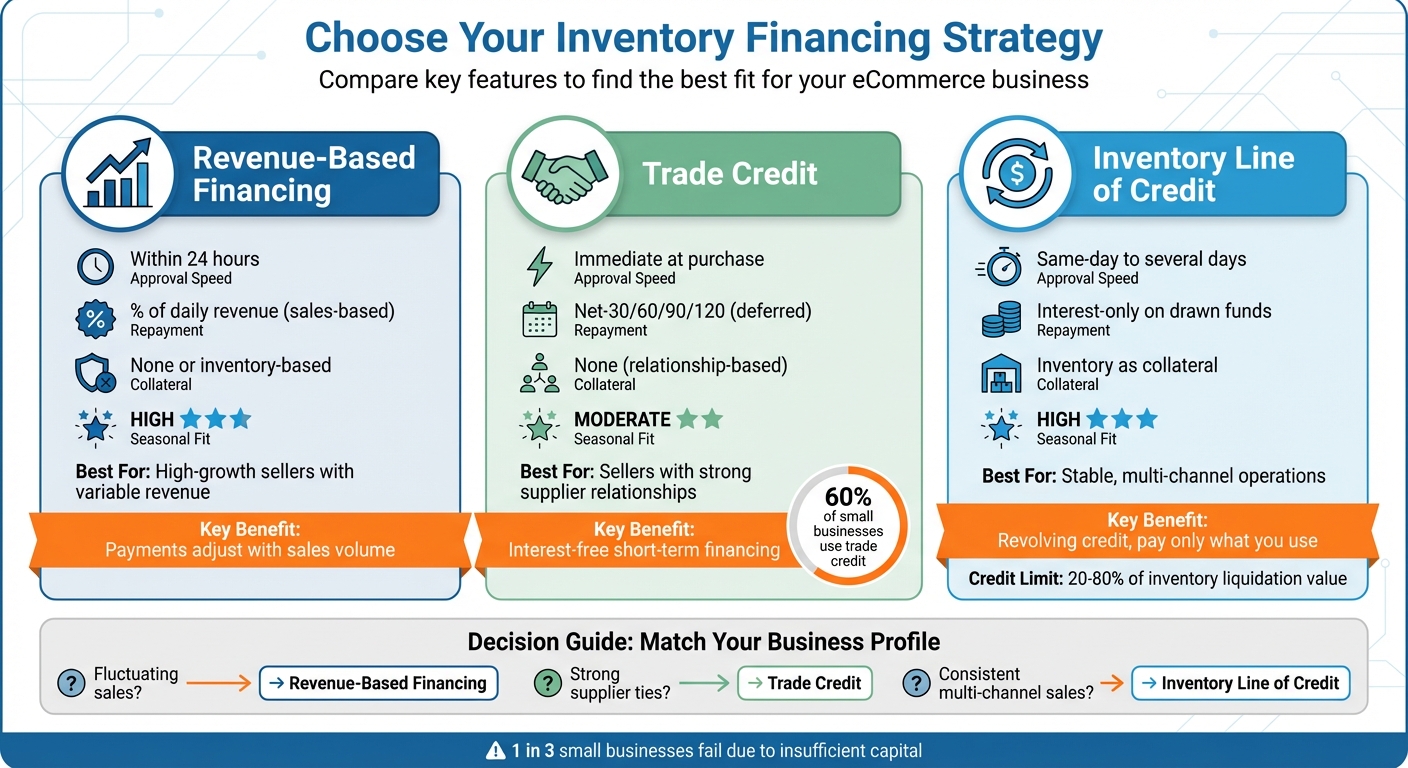

Comparing Financing Options for eCommerce Sellers

eCommerce Inventory Financing Options Comparison: Revenue-Based vs Trade Credit vs Lines of Credit

Financing Options Comparison Table

Choosing the right financing option depends on your sales patterns, business model, and supplier relationships. Below, we break down the key aspects of revenue-based financing, trade credit, and inventory lines of credit to help you make an informed decision.

Revenue-based financing is ideal for sellers with fluctuating or seasonal revenue. Its repayment flexibility ensures you're not overburdened during slower months.

Trade credit works well for businesses with established supplier relationships and predictable order cycles. This option lets you acquire inventory immediately while delaying payment for 30 to 120 days [12][14]. It’s a great way to maintain liquidity without paying interest, though terms depend on negotiations with your supplier.

Inventory lines of credit provide revolving funds, where you only pay interest on the amount you use [12][16]. This solution is particularly beneficial for established multi-channel sellers who need consistent funding to handle occasional stockouts or manage cash flow challenges.

| Feature | Revenue-Based Financing | Trade Credit | Inventory Line of Credit |

|---|---|---|---|

| Approval Speed | Often within 24 hours [11][16] | Immediate at purchase [12] | Same-day to several days [11][16] |

| Repayment Structure | Sales-based (% of daily revenue) [16] | Deferred (Net-30/60/90/120) [12][14] | Interest-only on drawn funds [16] |

| Collateral Needs | None or inventory-based [11] | None (relationship-based) [12] | Inventory as collateral [13] |

| Seasonal Fit | High [11][16] | Moderate [12] | High [12] |

| Best For | High-growth, variable revenue sellers [11] | Sellers with strong supplier relationships [12] | Stable, multi-channel operations [16] |

The growing popularity of inventory financing and revenue-based financing reflects a shift toward non-dilutive capital solutions. These tools empower eCommerce sellers to scale their inventory while keeping cash flow intact.

Conclusion

Selecting the right financing option can help you maintain steady cash flow and keep your business running smoothly. Revenue-based financing adjusts with your sales, trade credit takes advantage of supplier relationships, and inventory lines of credit offer revolving funds to ensure you can restock consistently. These options, tailored to your revenue patterns, can make your business more adaptable to changing circumstances.

It's essential to align your financing with your sales cycle. Fixed monthly payments might strain your cash flow during slower periods, but revenue-based options, like those provided by Onramp Funds, adjust repayments based on your daily sales, offering more flexibility [1].

Speed is another crucial factor. Modern financing solutions can approve funds in as little as 24–48 hours, a stark contrast to traditional bank loans that may take 30 to 60 days [2]. This quick access to capital allows you to seize opportunities like bulk discounts, gear up for seasonal spikes, or replenish fast-selling inventory without losing momentum.

To choose the best financing strategy, evaluate your sales trends, inventory turnover, and growth stage. For Shopify or Amazon sellers with consistent revenue, integrated revenue-based financing offers automatic fund transfers that can simplify cash management. If you have strong supplier relationships, negotiating better payment terms can free up cash. For ongoing capital needs, an inventory line of credit that grows alongside your business might be the ideal solution.

The stakes are high - one in three small businesses struggle or fail due to insufficient capital [15]. Don’t wait until a cash crunch hits. Research your options while your business is thriving, so you can lock in favorable terms and maintain liquidity when you need it most. By aligning your financing with your business cycle, you can fuel growth and stay prepared for whatever comes next.

FAQs

Which inventory financing option fits my sales cycle best?

The right inventory financing choice hinges on your business's specific needs and cash flow patterns. Revenue-based financing is a solid option for businesses with seasonal sales, as repayments adjust based on your sales volume, offering flexibility. If your business has steady seasonal demand, consignment-style financing can be a great fit since you only pay after selling the inventory. For businesses dealing with long lead times, look for financing options with fast approval and adaptable repayment terms to keep your stock levels steady without straining your cash flow.

How much inventory funding can I realistically qualify for?

The amount of inventory funding you can secure hinges on several factors, including your monthly sales, credit profile, and how well your business performs on its platform. Generally, businesses need to show at least $3,000 in monthly sales and operate on platforms such as Amazon, Shopify, or Walmart. Funding amounts can reach as high as $2 million and are often accessible within 24 hours, giving you the flexibility to grow your business while keeping your cash flow steady.

What should I watch for in fees and repayment terms?

Watch out for steep fees, hidden charges, and repayment terms that could fluctuate based on your sales or inventory levels. Make sure these terms match your cash flow and business cycles to prevent unnecessary financial pressure. Prioritize clear and predictable terms to keep your operations running smoothly.