Pulling capital at the right time is crucial for eCommerce businesses to maintain liquidity, avoid unnecessary costs, and fuel growth. This guide simplifies the decision-making process, focusing on cash flow, inventory cycles, and financing options. Here’s the gist:

- Track Cash Flow: Understand key metrics like opening cash, cash in/out, and net cash flow to identify funding gaps.

- Forecast Needs: Use a 13-week cash flow model and plan 30-90 days ahead, factoring in payout schedules, expenses, and sales cycles.

- Align with Inventory: Time capital pulls to match supplier lead times and sales trends, avoiding stockouts or overstock.

- Set Triggers: Define clear rules for pulling funds, like low inventory or upcoming sales events.

- Choose Financing Wisely: Match short-term needs (e.g., inventory, marketing) with flexible options like revenue-based financing, and reserve term loans for long-term projects.

- Manage Risk: Monitor metrics like working capital ratio, stress-test repayment plans, and maintain liquidity buffers.

eCommerce Funding Secrets Every Seller Should Know

Track Your Cash Flow and Find Funding Gaps

To stay on top of your business’s financial health, focus on five key cash flow elements: opening cash, cash in (like sales payouts, funds, or refunds), cash out (expenses such as inventory, marketing, shipping, and payroll), net cash flow (the difference between cash in and out), and closing cash. Together, these metrics give you a clear picture of your liquidity. Once you understand these, the next step is to build a model that puts them into action.

Create a Basic Cash Flow Model

Start by connecting your revenue sources - like Shopify, Amazon, PayPal, or Stripe - and your bank accounts to capture real-time transactions. Align your "Cash In" projections with the actual payout schedules for each platform. For instance, Amazon may release funds every two weeks, while Shopify might follow a different timeline. Considering that 82% of small businesses fail due to cash flow issues, it’s vital to stay proactive in spotting potential shortfalls [3]. Use tools like color coding to flag weeks where your net cash flow dips into the negative. A 13-week model can provide quick insights, helping you address problems before they escalate [5].

Spot Common Cash Flow Gaps

Some cash flow challenges are more common than others. For example:

- Delayed marketplace payouts can leave you waiting days or even weeks to access funds [4][6].

- Inventory prepayments often require substantial upfront investment, particularly when scaling high-demand products or preparing for seasonal spikes. You might need to pay suppliers up to 60 days before selling the inventory [6].

- Marketing and ad spend typically demands immediate cash outlays, which rarely align with payout cycles - especially during aggressive growth phases [4][6].

By closely monitoring payout schedules, you can better anticipate when cash will actually be available [4].

Forecast Your Cash Flow

Once your cash flow model is in place, the ideal timeframe for manual forecasting is six months, as going beyond this tends to reduce accuracy [3]. For short-term planning, focus on forecasting 30-90 days ahead, using known income and expenses. Pay special attention to months with three bi-weekly payment cycles instead of two, as this can significantly impact your cash-out projections [3][7]. Don’t forget to account for larger, less frequent expenses like quarterly software fees, annual insurance payments, and taxes [7].

Your forecast should also track the cash conversion cycle - how long it takes to turn your inventory investments back into cash - and your working capital ratio to ensure you have enough liquidity. A good rule of thumb is to maintain enough cash to replace your current inventory at least twice, which can help you avoid stockouts during periods of growth [3].

Use Inventory and Sales Cycles to Time Capital Pulls

Once you've built a solid cash flow model, the next step is to align your capital pulls with your inventory and sales cycles. This approach ensures your operations run smoothly and minimizes financial hiccups.

Your inventory schedule and sales trends should guide when you access funding. Dan Kang, CFO at Mercury, highlights the importance of this connection:

"Cash flow and inventory management are tightly linked in ecommerce. Forecasting when and how much inventory to buy - and how those decisions affect your cash balance - is critical" [8].

Align Capital Needs with Inventory Planning

Start by calculating your average monthly sales and work backward based on your supplier's lead times. The goal is to time your capital pulls so they match your inventory turnover. For example, if your supplier takes several weeks to manufacture and ship your products, you’ll want to secure funding well before your stock runs low. This buffer not only prevents stockouts but also helps you manage unforeseen delays in production or shipping [1].

Different business models require different funding strategies. B2B sellers often need larger upfront capital to manage bulk inventory and logistics, while B2C and D2C brands benefit from smaller, more frequent funding cycles that align with faster inventory turnover [1]. To avoid tying up too much cash in overstock or risking stockouts, keep a close eye on your ending inventory balance - both in units and dollars - at the end of each month [8].

Prepare for Seasonal Peaks and Sales Events

Seasonal events like Black Friday, back-to-school, or product launches bring unique challenges. Use data-driven AI tools to forecast SKU-level demand during these busy times [2]. Running "what-if" scenarios can help you model different demand levels - base, stretch, and conservative - so you can plan for varying capital needs [8].

During peak seasons, your funding needs go beyond just inventory. You’ll also need to account for increased marketing costs to drive traffic and sales during these events [2]. Automated reordering systems tied to your demand forecasts can help you secure inventory early, reducing the risk of stockouts or the need for expensive rush shipping [2].

Establish Clear Timing Triggers

Set specific rules for when to pull capital. For instance, you might decide to secure funding when your inventory reaches a critical level relative to your sales velocity. If you’re gearing up for a major sales event, make sure to access funds well in advance, keeping supplier lead times in mind.

Financing options like revenue-based financing can also help. These solutions align repayments with your actual sales, giving you flexibility to access funds as needed without committing to fixed monthly payments [1]. Stay vigilant for warning signs like late supplier payments or inventory shortages, as these may indicate you need additional capital [2]. By linking your funding triggers to precise sales and inventory metrics, you can avoid cash flow gaps and maintain steady operations.

How to Decide When to Pull Capital

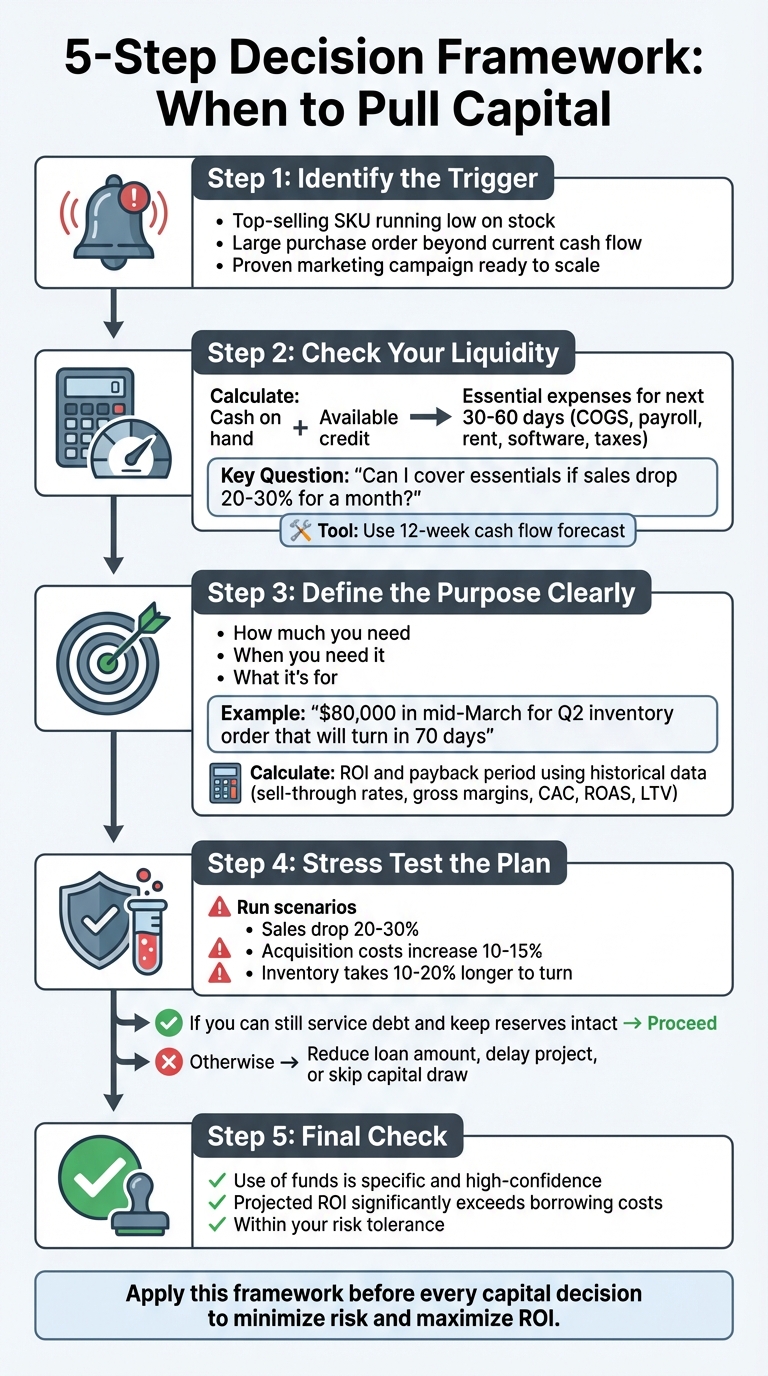

5-Step Framework for Deciding When to Pull Capital in eCommerce

Once you've assessed your cash flow and inventory, it's time to decide whether pulling capital makes sense. Here's a step-by-step guide to help you make that call.

Follow This Decision Process

Use this checklist to guide your decision-making:

- Identify the trigger: Is there a pressing reason to pull capital? Common triggers include a top-selling SKU running low on stock, a large purchase order beyond your current cash flow, or a proven marketing campaign ready to scale.

- Check your liquidity: Add up your cash on hand and available credit. Compare this total to your essential expenses for the next 30–60 days - things like COGS, payroll, rent, software, and taxes. Ask yourself: Can I cover these essentials if sales drop by 20–30% for a month? Then, use a simple 12-week cash flow forecast to track your weekly starting cash, expected inflows (from platforms like Shopify or Amazon), and scheduled outflows. Pay close attention to any week where your ending cash falls below your minimum reserve.

- Define the purpose clearly: Be specific about how much you need, when you need it, and what it’s for. For example: "$80,000 in mid-March for a Q2 inventory order that will turn in 70 days." Estimate the return on investment (ROI) and payback period using historical data, such as sell-through rates, gross margins, and customer acquisition metrics like CAC, ROAS, and LTV. Calculate how many days it will take to recover the principal and cover fees.

- Stress test the plan: Run scenarios where sales drop by 20–30%, acquisition costs increase by 10–15%, or inventory takes 10–20% longer to turn. If you can still service the debt and keep your reserves intact, proceed. Otherwise, consider reducing the loan amount, delaying the project, or skipping the capital draw altogether.

- Final check before pulling capital: Only move forward if the use of funds is specific and high-confidence, the projected ROI significantly exceeds your borrowing costs, and you're still within your risk tolerance. If any of these conditions aren't met, adjust your plan or hold off on borrowing.

Use These Financial Thresholds

Set clear financial guardrails to minimize risk:

- Keep 1.5–3.0 months of fixed operating expenses in liquid assets. If pulling capital would drop reserves below one month, it's a red flag.

- Maintain a debt-to-revenue ratio below 0.25–0.40. If it climbs above 0.50, you're entering risky territory unless your margins and repeat purchase rates are strong.

- Ensure your EBITDA covers monthly interest expenses by at least 2–3 times.

- Focus on gross margins of 40–60% or higher. Avoid scaling products with margins under 30–35%, as this limits your ability to cover ad spend, fees, and other costs.

- Use debt for marketing only when metrics like CAC, ROAS, and payback periods (ideally 90–120 days) are well-established.

These thresholds provide a solid foundation for making informed decisions.

See How It Works in Practice

Let’s break it down with two examples:

- A home goods brand on Shopify: A 12-week forecast shows that a $50,000 inventory payment in week seven will drop cash reserves to $15,000 - below the three-month target of $45,000. However, the trigger is a large purchase order for a best-selling SKU with a proven 60-day sell-through at a 52% gross margin. The order is expected to generate $26,000 in gross profit, with a 6% financing fee ($3,000 total cost) and a 75-day payback period. Even with a 25% drop in sales, essential reserves remain intact. All thresholds are met, so the decision is to pull $50,000 in capital.

- A fashion accessories seller: This business considers borrowing $30,000 for a new marketing campaign. However, sales are declining, CAC is rising, and gross margins are just 28%. The 12-week forecast shows ongoing negative cash flow even without new debt. The decision here is to avoid borrowing. Instead, the focus shifts to improving unit economics and testing the campaign with existing cash.

These examples show how applying the framework can lead to better financial decisions, whether it's a green light to borrow or a signal to hold back.

sbb-itb-d7b5115

Choose the Right Financing for Your Needs

Short-Term Needs vs. Long-Term Investments

Start by identifying the purpose of the financing and the timeframe for repayment. If you need quick cash for short-term needs - like stocking inventory that will sell in 60–90 days, bridging delays in marketplace payouts, or funding ad campaigns with fast returns - look for flexible options. These might include revenue-based financing, business credit cards with 0% introductory periods, or lines of credit. While the annualized costs of these options may be higher, they work well because the funds are repaid quickly.

For long-term projects, the approach shifts. Whether you're launching a new product line, upgrading facilities, or hiring permanent staff, the payback period could stretch over 12–36 months or more. In these cases, term loans or longer-term financing options are a better match. They come with lower interest rates and predictable payments, aligning with the long-term benefits of the investment. Avoid using high-interest credit cards or daily-repayment products for these types of projects - those tools are better suited for short-term needs.

How Revenue-Based Financing Works

Revenue-based financing (RBF) is a flexible option designed for eCommerce businesses dealing with seasonal or fluctuating sales. With RBF, you repay a percentage of your daily or weekly sales until you reach a predetermined total. For instance, a company like Onramp Funds might advance $50,000 with a repayment cap of $60,000, collecting 10% of your daily gross payouts. If sales are strong, you repay faster; if sales dip, payments adjust automatically. There's no fixed maturity date, compounding interest, or collateral requirements. Approval is based on your revenue history from platforms like Amazon, Shopify, Walmart, or TikTok Shop, and funds are often available within 24 hours after connecting your store.

This setup is ideal for financing inventory or marketing campaigns over multiple sales cycles. It usually offers higher limits than business credit cards - often several months’ worth of revenue - without the risk of hitting credit limits or missing manual payments. Compared to term loans, RBF provides faster approvals, requires less documentation, and adapts to your cash flow. However, it comes with higher costs, so it’s best suited for short- to medium-term needs with a high return on investment, rather than for low-margin projects or long-term assets.

Compare Your Financing Options

Here’s a breakdown of financing options to help you decide:

| Financing Type | Repayment Structure | Typical Speed | Optimal Use | Key Considerations |

|---|---|---|---|---|

| Revenue-Based Financing | Variable payments (% of sales) until cap is reached | 1–3 days | Inventory purchases, marketing campaigns, seasonal stock build | Payments adjust with sales; higher cost than bank loans; no collateral required. |

| Term Loan | Fixed monthly payments over 1–5 years | 1–4 weeks | Long-term projects, major equipment, refinancing high-cost debt | Predictable payments and lower rates; less flexible if sales fluctuate; may require collateral. |

| Business Line of Credit | Interest only on amounts used; minimum periodic payments | 1–2 weeks once established | Recurring short-term gaps, opportunistic inventory buys | Good for ongoing needs; watch credit utilization and renewal terms; may require strong financials. |

| Business Credit Card | Monthly payments; 0% during promo, otherwise high APR | Immediate once card is obtained | Very short-term expenses, small inventory buys, online ads | Offers rewards and short-term float; high interest if not paid off quickly; limited credit lines. |

When evaluating these options, focus on three key factors: the total dollar cost (including fees and interest or repayment caps), the effective annualized cost (similar to an APR), and the repayment structure. Simulate two scenarios - one with expected sales and another with slower-than-expected sales - to understand how each option affects your cash flow and reserves. This approach helps you stay financially secure, even if revenue drops by 20–30%.

Manage Risk When Pulling Capital

Safeguarding your business while pulling capital starts with careful risk management, building on insights from your cash flow and inventory analyses.

Key Metrics to Watch

Before taking on new financial obligations, keep a close eye on critical financial indicators. Start with your working capital ratio, which you calculate by dividing current assets by current liabilities. A ratio of 1.00 means you can just cover short-term obligations, while anything above 2.00 might suggest you're not fully utilizing available resources [9]. Also, evaluate your unit economics and customer acquisition cost (CAC). Persistently high CAC or declining sales could point to deeper issues rather than real growth opportunities [2].

Inventory health is another essential piece of the puzzle. Dive into SKU-level data to monitor which products are moving and which are sitting idle. Overstock ties up capital, while stockouts mean missed sales [2]. Combine these insights with real-time sales data from platforms like Amazon, Shopify, Walmart, or TikTok Shop to ensure funding decisions reflect your current business performance [2].

These metrics form the foundation for running effective stress tests.

Conduct Stress Tests

Stress testing helps measure your business's ability to withstand challenges. Focus on scenarios common in eCommerce, like rising production costs, shipping delays, or unexpected stockouts [1]. Simulate a downturn to confirm you can still meet repayment obligations and cover essential costs, even if operational expenses climb. If you're considering revenue-based financing, its flexible repayment terms can help adjust to fluctuating sales [1]. For fixed-repayment financing, ensure you have enough cash reserves to weather slower sales periods.

Once you've assessed these risks, formalize your approach to pulling capital.

Develop Internal Capital Guidelines

Create clear, written rules to guide decisions on when and how much capital to pull. For example, set repayment caps to protect your operating cash flow, ensuring financing costs don't overwhelm your monthly revenue. Tools like zero-based budgeting can help you allocate funds effectively, keeping profit margins intact as you grow [2].

If key metrics like your working capital ratio decline or supplier payments start lagging, pause additional capital pulls. Use data from ERP systems, financial models, and real-time sales metrics to create data-driven rules for pulling capital [2]. Finally, keep personal and business finances entirely separate to minimize risk [1].

Conclusion: Match Capital Decisions to Your Business Goals

Key Points to Remember

Here’s a quick recap of the essentials: avoid making impulsive decisions about capital; instead, plan ahead using accurate and up-to-date data. Keep a close eye on your cash flow, checking it weekly or biweekly, especially during platform payout delays or when big expenses like inventory orders and ad campaigns come up. Take a good look at your cash conversion cycle to identify and address any bottlenecks.

Plan your capital pulls 60–120 days before major events like Q4 or Prime Day. This ensures you’ll have the funds ready for inventory and other expenses. Match the type of financing to the need: short-term options like working capital lines or revenue-based financing are perfect for quick-turn items like inventory or marketing, while term loans are better suited for big, long-term investments like warehouse equipment.

Keep repayments manageable by monitoring your debt-service coverage ratio and the portion of revenue going toward lenders. If sales slow down, make sure you have enough cash reserves to stay afloat. Every dollar you borrow should have a clear purpose and contribute directly to ROI - whether that’s inventory that moves quickly, proven marketing strategies, or infrastructure that supports growth.

These guidelines are designed to help you stay strategic and focused.

What to Do Next

Now it’s time to put these ideas into action. Start by creating a 13-week cash flow forecast that includes real payout data, inventory orders, fixed costs, and ad spend. This will help you pinpoint where your money is tied up. Next, identify your top three growth priorities for the next 6–12 months and calculate how much capital you’ll need, along with the expected payback period.

Set clear internal rules for managing capital. Define a minimum cash buffer - enough to cover 3–6 months of operating expenses. Determine the maximum percentage of revenue you’re comfortable allocating to repayments, and choose the right type of financing for each need. During strong sales months, save 20–30% of your profits in a reserve account to avoid scrambling for emergency funds during slower periods.

Finally, when seeking financing, partner with lenders who align with your business model and sales cycles. For example, Onramp Funds offers eCommerce working capital solutions based on real-time sales data, helping you align funding with your business’s natural rhythm instead of rigid repayment schedules.

FAQs

How do I accurately forecast cash flow for my eCommerce business?

To effectively forecast cash flow, begin by keeping track of your starting cash balance and estimating all cash inflows. These could include revenue from your website, marketplaces, or other income sources. Use past sales data to guide your estimates, making adjustments for seasonal trends (like Black Friday) and any planned promotions. Next, outline all cash outflows, dividing them into fixed expenses (such as rent or software subscriptions) and variable costs (like inventory, shipping, or advertising). Subtract your outflows from your inflows to determine your net cash flow, then add this to your starting balance to project your ending cash balance. Repeat this process monthly for at least a year, and consider creating multiple scenarios - optimistic, realistic, and conservative - to prepare for different outcomes.

To keep your forecast accurate, update it frequently - ideally on a weekly basis - and watch for patterns like inventory turnover rates or payment delays. While tools like Excel or Google Sheets are simple and effective, using accounting software or cash-flow management tools can automate much of the process and provide real-time updates. This approach helps you identify potential shortfalls early, ensuring you're ready to secure capital when needed to support growth or maintain steady operations.

What are the best financing options for meeting short-term capital needs in eCommerce?

For eCommerce sellers in need of short-term capital, having access to quick and flexible financing options can make all the difference. Consider options like revenue-based financing, where repayment adjusts based on your sales, or purchase-order financing, which helps you pay suppliers upfront. Other useful tools include revolving credit lines and invoice financing, both of which can help maintain steady cash flow without locking you into long-term obligations.

These financing methods are tailored to provide fast access to funds, enabling you to handle seasonal fluctuations, stock up on inventory, or jump on growth opportunities - all while keeping financial stress in check. Be sure to assess your business’s specific needs and repayment ability to find the best fit.

How can I align capital pulls with my inventory and sales cycles?

To sync your capital needs with inventory and sales cycles, it's crucial to start by analyzing your sales patterns and inventory demands throughout the year. Pinpoint key sales spikes, such as Black Friday or the holiday season, and identify when you typically need to stock up on inventory ahead of time. Metrics like inventory turnover, Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO) provide valuable insights into cash flow trends, helping you determine the best times to act.

Build a cash flow model that forecasts monthly inflows (like sales and deposits) and outflows (such as inventory purchases and supplier payments). Establish clear triggers for action - for instance, when your cash balance dips below a set limit or inventory levels surpass a certain point. Leverage tools like accounting software or spreadsheets to automate alerts for these triggers. This way, you can quickly access capital when needed, ensuring you’re well-equipped to handle expenses and seize growth opportunities as they arise.