For growing eCommerce businesses, managing cash flow becomes increasingly challenging. One-off advances like Merchant Cash Advances (MCAs) or Revenue-Based Financing (RBF) provide quick funding but come with high fees, rigid repayment terms, and limited flexibility. As your business scales, these limitations can strain your finances.

A rolling cash line offers a better solution. It provides continuous access to capital that replenishes as you repay, aligning with your sales cycles. This approach reduces costs, simplifies cash flow management, and eliminates the need to reapply for funding repeatedly. It’s especially useful for businesses facing recurring cash flow gaps or increasing inventory and marketing expenses.

Key Takeaways:

- One-Off Advances: Fast but costly, ideal for short-term needs like bulk inventory purchases or viral trends.

- Rolling Cash Line: Flexible, ongoing access to funds with lower costs, tailored to support growing businesses.

| Feature | One-Off Advances | Rolling Cash Line |

|---|---|---|

| Funding Structure | Lump sum upfront | Draw as needed |

| Repayment | Fixed % of sales | Monthly or interest-based |

| Costs | High factor rates (e.g., 1.3x) | Lower, interest-based |

| Reapplication | Required for new funds | Automatic replenishment |

If you’re stuck in a cycle of borrowing to cover recurring gaps, it’s time to consider a rolling cash line. It’s a smarter way to manage cash flow and drive growth without the financial strain of one-off advances.

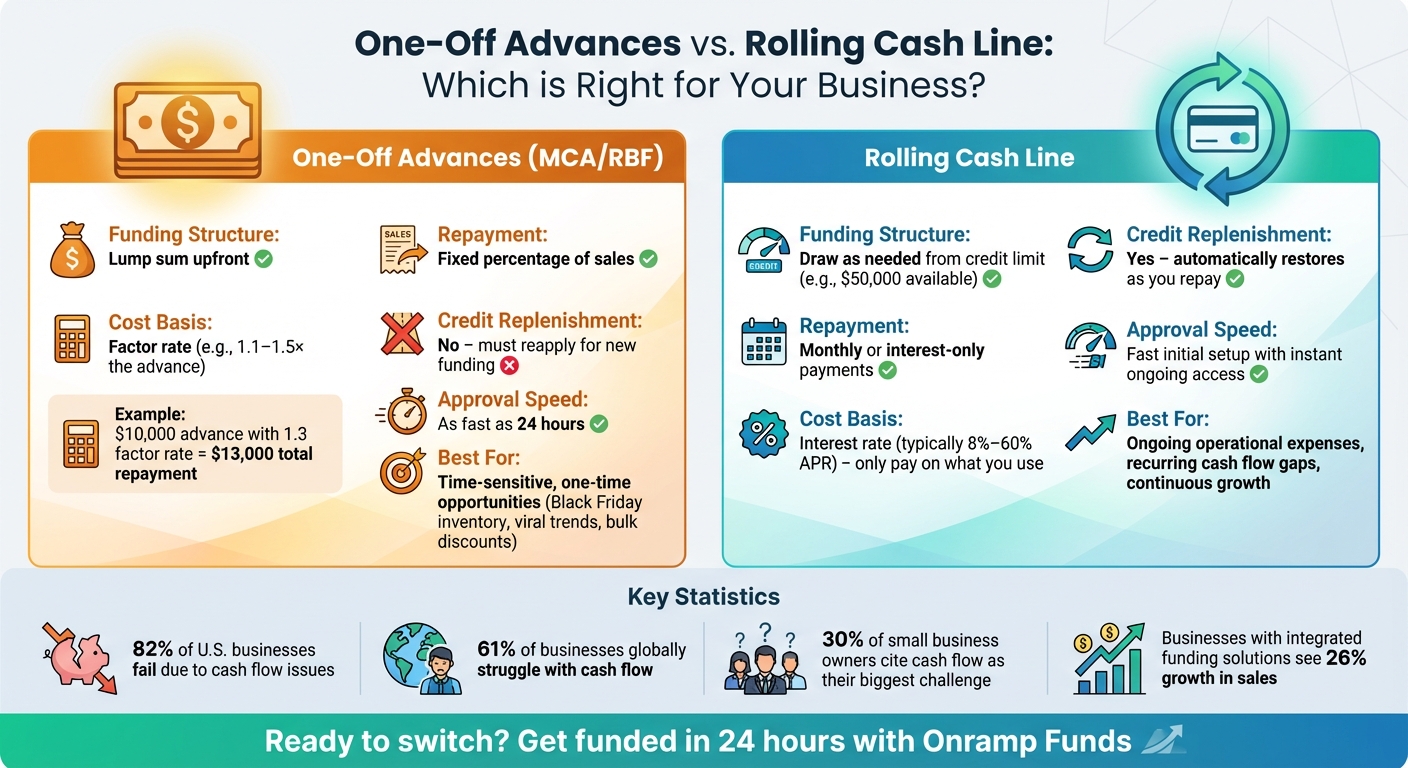

One-Off Advances vs Rolling Cash Line Comparison for eCommerce

One-Off Advances vs. Rolling Cash Lines: What's the Difference?

How One-Off Advances Work

One-off advances, like Merchant Cash Advances (MCAs) and Revenue-Based Financing (RBF), offer businesses a lump sum upfront in exchange for a portion of their future receivables. These are not traditional loans; instead, providers purchase your future receivables at a discounted rate [5][6]. For instance, if you secure a $10,000 advance with a factor rate of 1.3, you’ll repay a total of $13,000 [7].

Approval for one-off advances can be as quick as 24 hours. Instead of relying solely on credit scores, these advances often factor in real-time sales data. Repayments are typically tied to your revenue, adjusting automatically based on your earnings [5][9][7]. This makes them a great fit for time-sensitive opportunities - like stocking up for Black Friday, jumping on a viral product trend, or securing a bulk inventory discount. However, since these advances are one-time funding solutions, you’ll need to reapply if additional capital is required.

How Rolling Cash Lines Work

A rolling cash line, also known as a revolving line of credit, provides ongoing access to funds. After being approved for a maximum credit limit (say, $50,000), you can draw funds as needed. As you repay what you’ve used, your available credit replenishes automatically, eliminating the need to reapply for funding each time [8][7].

Unlike one-off advances, which charge a flat factor rate on the full amount, rolling cash lines charge interest only on the funds you actually use. While there may be some maintenance fees, the cost structure is generally straightforward. Repayment terms can vary - some require monthly payments, while others allow interest-only payments on the amount drawn. This flexibility makes rolling cash lines particularly useful for managing the cash conversion cycle, the period between paying suppliers and receiving payments from customers [1][2]. Think of it as a financial tap connected to your revenue stream: it refills as you repay, ensuring you always have access to capital when you need it.

To better understand the differences, here’s a side-by-side comparison:

Side-by-Side Comparison

| Feature | One-Off Advance (MCA/RBF) | Rolling Cash Line |

|---|---|---|

| Structure | Lump sum provided upfront [7] | Revolving credit limit; draw as needed [8] |

| Repayment | Fixed percentage of sales [7] | Monthly or interest-only payments [8] |

| Cost Basis | Factor rate (e.g., 1.1–1.5× the advance) [7] | Interest rate (typically 8%–60% APR) [7] |

| Credit Replenishment | No – must reapply for new funding [11] | Yes – available credit is automatically restored [7] |

| Best Use Case | Time-sensitive, singular opportunities [5][7] | Ongoing operational expenses and growth [7][8] |

| Approval Speed | As fast as 24 hours [5][9] | Fast initial setup with instant access [10] |

When to Switch from One-Off Advances to a Rolling Cash Line

Dealing with Recurring Cash Flow Gaps

If recurring cash flow gaps are becoming a regular headache, it might be time to move beyond one-off advances. These gaps occur when your business consistently faces a mismatch between outgoing costs - like inventory, payroll, and marketing - and incoming payments from platforms such as Amazon or Shopify, which often operate on net-30 or net-60 terms [17][4].

"Cash flow issues do not usually appear overnight. They build slowly, hidden beneath the surface of strong sales or rapid growth." - Artemis Clarke [18]

The signs are hard to ignore: relying on personal credit cards or family funds to cover expenses, or cutting back on critical marketing to pay suppliers [12]. With 30% of small business owners citing cash flow as their biggest challenge [15], it's clear that one-off advances only provide short-term fixes. A rolling cash line, on the other hand, offers ongoing access to funds as you repay, eliminating the need to reapply every time a gap arises [19][20].

To truly understand your cash flow health, track your cash conversion cycle. This involves adding Days Inventory Outstanding to Days Sales Outstanding, then subtracting Days Payable Outstanding [20]. If this number keeps climbing, it’s a sign that a rolling cash line could help bridge the gap between paying suppliers and collecting customer payments. Using a 13-week rolling forecast can also help determine whether your cash shortages are sporadic or part of a recurring pattern [17][18].

These persistent cash flow challenges often signal the need for more flexible financing to support your business's growth.

Growing Inventory and Marketing Expenses

As your business scales, the limitations of one-off advances become more apparent. Growing companies must juggle increasing inventory investments while keeping marketing spend steady [23].

"Inventory isn't just a product - it's capital in physical form." - Shipfusion Team [23]

Take the example of Sarah's Bakery in January 2025. Facing a post-holiday slowdown, Sarah used a rolling cash flow model to manage the dip. By closely monitoring weekly inflows and outflows, she spotted a February revenue gap. She delayed non-essential ingredient orders and introduced a prepaid gift card strategy to generate immediate cash. This funded a Valentine's Day promotion that brought her business back to profitability by mid-February [22]. Such quick adjustments aren’t feasible with one-off advances, which often lock businesses into rigid spending plans [23].

If your business has transitioned from seasonal sales spikes to continuous reinvestment cycles - where ad spend and supplier payments are constant - a rolling line is a better fit [16]. Research from McKinsey shows that businesses that respond faster to market changes see a 20% to 30% boost in financial performance [3]. Additionally, rolling forecasting methods can improve revenue accuracy by around 14% compared to static approaches [3], giving you the flexibility to reallocate funds to popular products or delay reorders based on demand [23].

When One-Off Advances No Longer Meet Your Needs

Beyond inventory and marketing challenges, broader financial pressures often highlight the need for a more adaptable funding solution. If your leadership team spends more time scrambling to address immediate cash flow issues than planning long-term strategies, it’s a clear sign you’ve outgrown one-off advances [15].

Specific red flags include running out of high-demand items but lacking the funds to reorder without resorting to tight credit terms [12]. Another is watching your creditor list grow even as your revenue increases [18]. In 2023, U.S. consumers returned $743 billion worth of products, creating significant cash flow strain for eCommerce businesses [13] - a strain that one-off advances simply can’t alleviate.

"As you grow, you are spending money to perform on increased demand and volume while collecting on receivables from the lower-volume period that just passed." - John Torrens, Professor of Entrepreneurial Practice, Syracuse University [15]

With 61% of businesses globally struggling with cash flow [14] and 22% of U.S. small businesses unable to pay bills due to cash flow issues [15], the problem isn’t just access to funding - it’s access to the right kind of funding. Frequent stockouts, payout delays, and the constant need to reapply for financing are clear indicators that one-off advances are no longer enough to meet your growing needs [19]. When paired with recurring cash flow gaps and mounting inventory demands, these challenges make a compelling case for switching to a rolling cash line.

Stop Bleeding Cash: Simple E-Commerce Finance for Better Cash Flow & Profit | Sourabh Nolkha

sbb-itb-d7b5115

How Onramp Funds' Rolling Cash Line Works for eCommerce Businesses

When you realize your eCommerce business needs more adaptable financing, understanding how Onramp Funds’ rolling cash line operates is key. The platform tackles common challenges eCommerce sellers face - like delayed payouts, unpredictable sales cycles, and the need for quick access to funds. By syncing funding with your business’s cash flow, it offers a payment structure that adjusts to your sales performance.

A Repayment Plan That Matches Your Sales

Onramp’s repayment model is tied to your revenue, not rigid schedules. Instead of fixed daily or weekly payments that can strain your cash flow, you repay as a percentage of your sales. When sales are strong, repayments increase. During slower periods, they decrease.

"Our funding is 100% aligned with your sales and repayment, and fees are responsive to actual performance." - Onramp Funds [24]

This approach ensures you’re not repaying advances while your inventory is still sitting on shelves [24]. For context, marketplace payout schedules can take up to 14 days on platforms like Walmart and even longer on Amazon [24]. Some terms stretch to 60 days, with total cash cycles extending to 100 days [25]. By aligning repayments with sales, Onramp helps protect your working capital during these natural fluctuations.

"You repay faster when sales are up, but when the sales take a dip on a slow month, we collect less, thus helping you protect your cash flow." - Onramp Funds [24]

The system connects to your eCommerce store and bank account using a read-only API. This setup automates deposits and repayments, eliminating the need for manual tracking [24]. Onramp also charges 0% interest [24], with fees based solely on your actual sales performance - offering relief during off-seasons when cash flow might be tighter.

This flexible repayment structure not only safeguards your working capital but also complements Onramp’s quick funding process.

Funding in Just 24 Hours

When opportunities arise - like securing discounted inventory, running a flash sale, or reacting to market trends - timing is everything. Onramp Funds delivers capital within 24 hours of approval [26][27], allowing you to act quickly without waiting weeks for traditional financing.

Nick James, CEO of Rockless Table, shared his experience:

"Applied, got our offer, and had cash in our bank account within 24 hours. Their Austin, TX based team was very professional and helped me deploy the cash to effectively grow our business." - Nick James, CEO, Rockless Table [26]

The process is simple: get an initial estimate in just one minute and connect your store in five minutes [26]. Onramp uses real-time sales data from your connected platforms, bypassing lengthy credit checks or collateral requirements [27]. Returning borrowers with a solid track record enjoy an even faster process [27].

Seamless Integration with Your eCommerce Platform

A standout feature of Onramp’s model is its ability to integrate directly with your sales channels, streamlining operations. It connects with major platforms like Amazon, Shopify, Walmart, Stripe, WooCommerce, BigCommerce, Squarespace, TikTok Shop, and SHOPLINE [26]. This integration automates underwriting by analyzing real-time sales data, order volumes, and customer behavior [27].

Onramp only requires read-only access to your performance metrics and doesn’t rely on personal credit checks [26]. To qualify, your business must be legally based in the U.S. and generate at least $3,000 in average monthly sales [26]. You’ll typically need to provide bank statements, profit and loss records, and accounting software access to give lenders a comprehensive view of your financial health [27].

"Onramp has simplified cash flow by automating everything: easy to request, set it and forget it payments - quick and fast!" - Torrie V., Founder and Owner, Torrie's Natural [26]

Having facilitated over 3,000 eCommerce loans [26], Onramp holds an A+ rating with the Better Business Bureau and a "Great" rating on Trustpilot from 220 reviews [26]. Users frequently highlight the convenience of automated payments and praise the Austin-based team for their support [26]. Whether you need funds for inventory, shipping, marketing, or logistics, Onramp gives you the freedom to allocate capital where it’s needed most.

How to Make the Switch to a Rolling Cash Line

Transitioning from one-off advances to a rolling cash line is all about fine-tuning how you handle cash flow. The process revolves around analyzing your cash flow patterns, integrating your eCommerce platform, and tracking how you allocate funds as your business scales. These steps align with the earlier discussion on syncing funding with operational needs.

Review Your Cash Flow Needs

To determine if a rolling cash line is the right solution for your business, start by taking a closer look at your cash flow. Identify recurring gaps in your cycle - like those caused by inventory restocking or seasonal marketing pushes. A dynamic forecast can help you pinpoint when and where these shortfalls are likely to happen [21].

Here’s a simple formula to calculate your net operating cash flow: Cash Receipts – Cash Outflows [28]. If you notice consistent shortfalls during key business activities, a rolling cash line can offer the flexibility to cover these gaps without the hassle of reapplying for funding each time. Once you’ve stabilized your cash flow, you can even negotiate better terms with suppliers, such as early-payment discounts or extended payment periods [28].

Once you’ve mapped out your cash flow needs, the next step is to connect your eCommerce platform for seamless, real-time funding adjustments.

Connect Your eCommerce Platform to Onramp Funds

Setting up the connection between your eCommerce platform and Onramp Funds is straightforward. Onramp uses REST APIs to link with your sales channels, providing instant updates on sales, inventory, and customer activity [32]. Secure this connection through OAuth or merchant tokens, which are easily accessible via native plugins like those found on the Shopify App Store [30][33].

"Integrating point of sale with ecommerce is a must... You want your channels to 'talk' to each other, so that sales, inventory, and customer data flow smoothly from one system to the next." - Francesca Nicasio, Retail Expert, Vend Point of Sale [29]

Onramp supports a wide range of platforms, including Amazon, Shopify, Walmart, BigCommerce, WooCommerce, and TikTok Shop. Businesses that use integrated funding solutions enjoy a 9 out of 10 approval rate when leveraging real-time data [31]. Moreover, small and medium-sized enterprises (SMEs) with integrated funding have experienced 26% growth in sales [31].

Track Performance and Adjust Your Approach

Once your rolling cash line is up and running, focus on activities that deliver the best returns, like stocking up for peak seasons or investing in proven marketing strategies [34][35]. Use these funds to shorten your cash conversion cycle [4] and keep your capital usage aligned with your sales trends.

You might also consider just-in-time (JIT) inventory management, which involves ordering stock only as needed to fulfill customer orders [36][38]. This approach reduces holding costs and keeps more of your cash line available for other priorities. Another strategic move? Allocate funds to subsidize shipping costs. Since 80% of shoppers are willing to spend more to qualify for free shipping [34], this can be a smart way to increase your average order value.

| Strategy | Impact on Cash Flow | Best Practice |

|---|---|---|

| Inventory Management | Reduces tied-up capital | JIT restocking and demand forecasting [4][36] |

| Accounts Receivable | Accelerates inflows | Automate invoicing and offer flexible payment options [4][37] |

| Accounts Payable | Delays outflows | Negotiate extended payment terms [4][37] |

| Marketing Spend | High ROI potential | Focus on high-conversion channels [34][36] |

Keep an eye on how quickly you’re drawing and repaying funds. If you’re consistently hitting your limit, it might be time to explore increasing your funding amount. On the other hand, if you’re using less than expected, consider redirecting funds to automate repetitive tasks like order processing or customer service. This can lower operating costs and free up cash for growth opportunities [36][37].

Conclusion

A rolling cash line syncs your financing with the rhythm of your business. By tying funding to your real-time sales, you no longer have to scramble to cover inventory restocks or fund marketing efforts with static, inflexible capital.

The numbers paint a stark picture: 82% of businesses in the United States fail due to cash flow issues [40], and 52% of senior business leaders report a widening gap between their current financial position and where they need to be [39]. These stats underline the importance of having a funding model that replenishes as you repay. A rolling cash line keeps liquidity flowing - ensuring you always have the funds to handle day-to-day expenses. This approach not only helps you manage cash flow shortfalls but also allows you to act quickly on opportunities like bulk purchasing discounts or launching new marketing strategies.

Integrations with platforms like Shopify, Amazon, and TikTok Shop add another layer of convenience, helping you avoid unexpected cash flow disruptions. Akbar Ahsan, Co-founder of Storfund, explains it best:

"Shortening your cash cycle even by a few days can make a significant difference, especially if your business is growing" [25].

When you consider these operational benefits, making the switch to a rolling cash line becomes a logical step forward.

If cash flow gaps and growing inventory needs are slowing your business down, a rolling cash line could be the solution. Onramp Funds offers fast funding within 24 hours, equity-free financing, and repayment terms that flex with your sales - so you pay more only when you earn more. With support for leading eCommerce platforms and a clear fee structure, you can retain full ownership of your business while driving sustainable growth.

FAQs

What are the key advantages of moving from one-time cash advances to a rolling cash line?

Switching to a rolling cash line can be a game-changer for managing your business’s cash flow. It provides continuous access to funds, so you can tap into capital whenever it’s needed. The best part? You only pay interest on the amount you actually use, helping you save money while maintaining flexibility.

This type of funding can also help fuel steady growth. With consistent access to capital, you’re better equipped to scale your operations, handle unexpected expenses, or jump on new opportunities as they arise. Since it adjusts to your business’s financial needs over time, a rolling cash line offers a practical solution for long-term financial planning.

What are the benefits of using a rolling cash line to handle cash flow gaps?

A rolling cash line offers continuous access to funds, helping businesses navigate periods of irregular income, seasonal fluctuations, or unforeseen expenses. It’s a practical way to keep your operations running smoothly by covering key costs like inventory, payroll, or marketing when revenue doesn’t arrive on time.

Unlike a one-time cash advance, a rolling cash line adjusts to your business's changing needs. This flexibility allows you to scale as your business grows, making it a reliable option for maintaining stability and supporting growth in the fast-paced world of eCommerce.

How can I transition my business from one-off cash advances to a rolling cash line?

To transition effectively, begin by assessing your cash flow and pinpointing the growth requirements of your business. Consider funding options that can adapt to your sales cycle, like a rolling cash line, which offers scalable access to capital whenever it's needed. Establish a partnership with a reliable lender and incorporate this financing method step by step. This approach can help maintain steady growth while ensuring smoother cash flow management.