Managing inventory while maintaining healthy cash flow is a common challenge for eCommerce businesses. Inventory often requires significant upfront payments, tying up cash for months before products are sold. This can limit your ability to invest in marketing, operations, or growth. To address this, you need strategies that align inventory funding with your sales cycle and cash flow needs.

Key Takeaways:

- Cash Conversion Cycle: Track how long your money is tied up in inventory from supplier payment to customer purchase. A shorter cycle means better cash flow.

- Metrics to Monitor: Days Inventory Outstanding (DIO), Days Payables Outstanding (DPO), and Days Sales Outstanding (DSO) help pinpoint bottlenecks.

- Forecasting Needs: Analyze demand and plan ahead to avoid overstocking or running out of inventory.

- Funding Options: Choose from term loans, lines of credit, supplier credit, or revenue-based funding. Each has pros and cons depending on your cash flow patterns.

- Operational Improvements: Optimize inventory management, focus on high-margin products, and improve sell-through rates to reduce funding needs.

By combining better planning, operational efficiency, and the right financing tools, you can fund inventory without straining your cash flow.

How does inventory management affect cash flow?

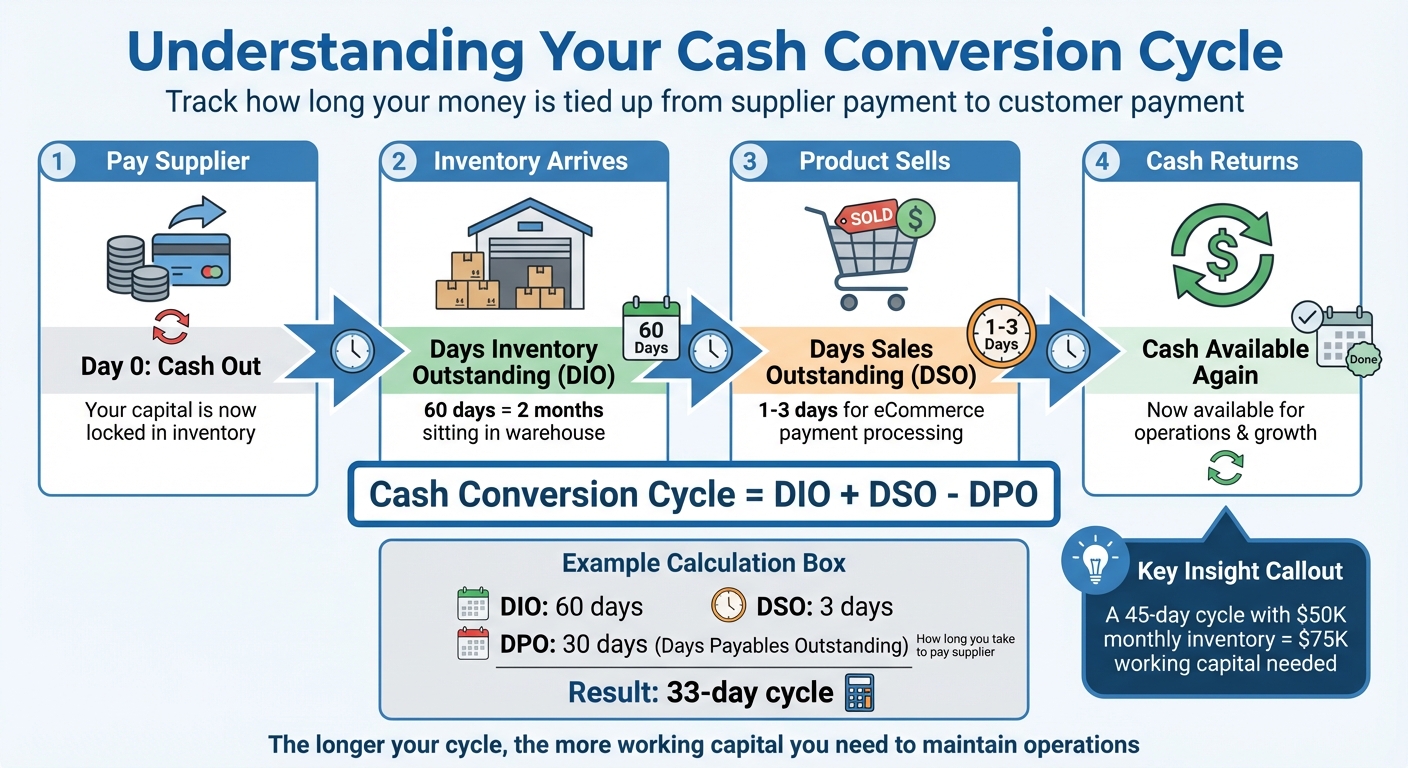

How the eCommerce Cash Conversion Cycle Works

eCommerce Cash Conversion Cycle: How Money Flows Through Your Business

The cash conversion cycle tracks the time between paying your suppliers and receiving payment from customers. This period determines how long your money is tied up in inventory instead of being available for other business needs.

Here’s how it works: the cycle begins when you place an order and pay your supplier. From that point, your cash is locked in until the inventory sells and customer payments clear. This can take weeks or even months, during which your capital is unavailable for critical activities like marketing, hiring, or daily operations.

"Retailers typically try to limit the amount of working capital tied up in inventory since, despite inventory usually being considered a liquid asset, it isn't as liquid as cash and can also depreciate if retained too long." - Fiona Lee, Former Content Lead, Ramp [1]

Seasonal demand can amplify cash flow challenges. For instance, preparing for the holiday season often requires placing large inventory orders in August or September, months before you see the bulk of your sales revenue in November and December [1].

Key Metrics to Track

Three essential metrics can help you understand how cash moves through your business:

- Days Inventory Outstanding (DIO): Measures how long it takes to sell your inventory after it arrives. For example, a DIO of 60 days means your products sit for two months before converting to sales.

- Days Payables Outstanding (DPO): Tracks how long you take to pay suppliers after receiving inventory. A DPO of 30 days gives you a month to settle supplier payments.

- Days Sales Outstanding (DSO): Shows the time between making a sale and collecting payment. For most eCommerce businesses using standard payment processors, this is typically 1-3 days.

To calculate your cash conversion cycle, add DIO and DSO, then subtract DPO. For instance, a 45-day cycle means your cash is tied up for a month and a half before it comes back. The longer the cycle, the more working capital you’ll need to maintain operations. If you sell $50,000 in inventory each month with a 45-day cycle, you’ll need around $75,000 in working capital to sustain your sales without external funding.

By monitoring these metrics, you can identify where cash flow bottlenecks occur and plan accordingly.

Finding Your Cash Flow Gaps

Cash flow gaps happen when your inventory expenses outpace your available cash reserves. This is particularly common during periods of growth or seasonal stock preparation. To pinpoint these gaps, compare your upcoming inventory costs to your current cash balance and expected revenue for each month. For example, if you need $80,000 for inventory in September but only have $50,000 in cash and $20,000 in anticipated revenue, you’re staring at a $10,000 shortfall.

Forecasting at least three months ahead can help you spot these low points. Look for times when your cash reserves fall below what’s needed to cover both inventory and operational expenses like advertising, fulfillment, and software subscriptions. These gaps show you when and how much extra funding you’ll require. Many lenders will finance up to 80% of your inventory’s appraised value [1], so to secure $10,000 in funding, you’d need inventory worth at least $12,500.

Improving Operations Before Seeking Funding

Streamlining inventory management can reduce your reliance on external funding. Even small improvements in forecasting, product selection, and sell-through rates can free up valuable working capital.

Demand Forecasting and Inventory Planning

Getting demand forecasting right is essential to avoid ordering too much or too little inventory. Overestimating demand can result in excess stock, forcing you to borrow additional funds and pay higher interest costs [3]. To avoid this, connect your customer acquisition costs, order volume, and fulfillment expenses to better understand your future cash flow [2].

"Inventory is critical in ecommerce - too little and you lose sales, too much and you burn cash." - Dan Kang, CFO, Mercury [2]

Keep your forecasts up to date by reviewing Shopify or accounting data monthly to validate sales targets and profit margins. Build three forecast scenarios: a "Base" model for your most realistic outcome, a "Stretch" version for optimistic growth, and a "Conservative" plan for slower sales. This approach helps you determine the minimum funding you'll need for various situations. Use your order volume to calculate monthly unit sales and develop a purchase order plan that aligns with actual demand [2].

Focus on High-Impact Inventory

Not every product deserves equal attention. Using ABC inventory analysis, you can classify items based on their revenue contribution. Your "A" products - typically the top 20% of items that generate 80% of your revenue - should command most of your focus.

Analyze sales history to identify products with high turnover and healthy margins [1]. Inventory that sits for more than 90 days ties up cash that could be better used elsewhere. Prioritize purchasing nonperishable items that retain value and sell quickly [4]. By managing inventory more efficiently, you not only improve your cash flow but also make your business more appealing to potential lenders [5].

Optimizing your inventory mix is a practical way to strengthen cash flow and set the stage for better funding opportunities.

Improving Margins and Sell-Through Rates

Boosting margins and increasing sell-through rates can accelerate cash generation, reducing the need for external funding. Dynamic pricing - adjusting prices based on demand and market conditions - can help you maximize revenue while maintaining healthy profit margins [6][7]. For example, testing small price increases on best-selling products can improve cash flow without significantly impacting demand.

For slower-moving products, consider running targeted promotions or bundling them with popular items to increase sales and average order value [7]. Reassess your marketing spend to identify underperforming channels, and redirect that budget toward campaigns that drive results [6]. Additionally, negotiating early payment discounts with suppliers - often in the range of 1% to 2% - can improve margins without changing your product pricing [1].

These operational adjustments not only improve cash flow but also position your business for more favorable funding options down the line.

sbb-itb-d7b5115

Inventory Funding Options for eCommerce

Growing your eCommerce business often means expanding your inventory, and sometimes that requires external funding. The best funding option for your business will depend on how well it fits with your sales cycle and cash flow needs. Let’s take a closer look at the main options and how they align with your financial patterns.

Term loans and lines of credit are two common choices. Term loans provide a lump sum that you repay in fixed monthly installments, which can be challenging during slower sales periods. In contrast, lines of credit offer more flexibility. You can draw funds as needed and only pay interest on the amount you use, making them ideal for handling seasonal inventory demands. Both options typically require collateral and can take days or weeks to secure approval.

Supplier credit is another option, allowing you to defer payment for inventory through terms like Net 30, Net 60, or Net 90. This approach helps conserve working capital. Some suppliers even offer early payment discounts - usually 1% to 2% - if you pay ahead of schedule, which can save money compared to borrowing costs.

Short-Term Loans and Lines of Credit

Short-term financing is a solid choice for businesses with steady revenue and good credit. Term loans provide a fixed sum with consistent monthly payments, but if sales slow, those payments can strain cash flow. Lines of credit, on the other hand, offer more flexibility. They work like a business credit card - you’re approved for a maximum amount and can borrow as needed. You’ll only pay interest on what you use, making them a good tool for managing seasonal ebbs and flows in sales.

Supplier Credit and Payment Terms

Supplier credit is a powerful but often overlooked funding strategy. With terms like Net 30, Net 60, or Net 90, you can receive inventory immediately but delay payment. This works especially well if you can sell your inventory quickly. For example, if you sell products within 20 days but have 30 days to pay, you create positive cash flow without taking on any borrowing costs.

Revenue-Based Funding with Onramp Funds

Revenue-based funding offers a flexible repayment structure that adjusts based on your sales performance. When sales are strong, payments increase; when sales dip, payments decrease. This approach aligns perfectly with the cash flow challenges of eCommerce businesses.

Onramp Funds specializes in revenue-based financing. Their platform connects directly to your store data on platforms like Amazon, Shopify, Walmart, and TikTok Shop through read-only access. This allows them to base approval decisions on your actual sales performance rather than relying solely on credit scores. Even better, funds are typically available within 24 hours - much faster than traditional bank loans.

With Onramp, you retain full ownership of your business since the funding is equity-free. There’s no need for personal credit checks or collateral. On average, businesses using Onramp have seen a 73% revenue increase within 180 days of funding, and 75% of customers return for additional funding.

"Onramp offered the perfect solution with revenue-based financing to secure the capital we needed to invest in inventory and pay it back at a reasonable time frame once we made sales." – Jeremy, Founder and Owner of Kindfolk Yoga [8]

"Applied, got our offer, and had cash in our bank account within 24 hours." – Nick James, CEO of Rockless Table [8]

| Funding Type | Repayment Structure | Collateral Required | Approval Speed | Cash Flow Impact |

|---|---|---|---|---|

| Term Loan | Fixed monthly payments | Often business/personal assets | Days to weeks | Strains cash flow during slow sales |

| Line of Credit | Interest on drawn amount | Often inventory or other assets | Days to weeks | Flexible with revolving structure |

| Revenue-Based | Percentage of sales | None (equity-free) | Less than 24 hours | Low impact; aligns with sales volume |

| Supplier Credit | Net 30/60/90 terms | None | Immediate (if approved) | Very low impact with interest-free period |

To qualify for Onramp Funds, your business must be a U.S.-based legal entity (such as an LLC or C-Corp) with at least $3,000 in average monthly sales. Onramp has supported over 3,000 eCommerce loans and holds an A+ rating from the Better Business Bureau [8].

Creating a Funding Plan That Protects Cash Flow

A solid funding plan ensures you borrow just enough to meet your needs, repay comfortably within your cash flow limits, and adjust as your business evolves. This approach is critical for securing inventory without putting your cash flow at risk.

Calculating How Much Funding You Need

Start by identifying your baseline inventory requirements for non-seasonal periods, then factor in additional needs for peak demand [9]. Most lenders provide funding based on a percentage of your inventory value - typically up to 80% [1].

Don’t overlook hidden costs that can chip away at your cash flow. Expenses like Amazon seller fees, FBA storage charges, PPC campaigns, tariffs, and fuel surcharges all influence how much capital you’ll truly need [9]. To stay ahead, calculate your net profit margin using this formula:

(Total Revenue – Total Expenses) ÷ Total Revenue x 100.

This calculation helps you detect shrinking margins caused by rising supplier costs or inflation [9]. For reference, the average profit margin for Amazon FBA sellers ranges between 15% and 25%. Margins below 8% are a red flag for potential trouble [9].

Keep your financial documents - income statements, cash flow statements, and balance sheets - up to date for sound decision-making. Use forecasting tools to predict future capital needs based on inventory turnover, loss rates, and damage rates [9][1].

Once you’ve determined the amount of funding required, the next step is to structure repayments around your cash flow patterns.

Matching Repayments to Your Cash Flow

Aligning repayments with cash flow ensures you can meet obligations without straining your finances. Revenue-based financing is an excellent option, as payments adjust automatically based on sales performance. When sales are strong, payments increase; when sales slow down, payments decrease [8]. As Onramp Funds puts it:

"Your payments sync with your sales, you'll never have to worry about your ability to repay during a slower month." [8]

To manage liquidity effectively, create 13-week cash flow projections using cash flow management software. This helps pinpoint gaps and align repayment dates with marketplace payouts [11]. If you’re using supplier credit, negotiate extended terms - switching from Net 30 to Net 45 or Net 60 gives you extra time to sell inventory before invoices are due [10][11]. For inventory financing, pay off debt proportionally as inventory sells. For example, if you financed $10,000 worth of inventory and sold $3,000 in the first week, pay off that $3,000 immediately to reduce interest expenses [13].

It’s also wise to maintain a cash reserve for slower periods, so you’re not forced to liquidate inventory at a loss [12]. Segment suppliers by their importance to your operations and prioritize discussions about extended payment terms or early payment discounts [11].

Once repayment terms are in place, regular monitoring and adjustments keep your plan effective.

Tracking and Adjusting Your Plan

A funding plan isn’t a one-and-done deal - it requires ongoing attention. Track inventory turnover, loss, and damage rates to ensure inventory converts to cash quickly enough to meet repayment obligations [1]. Regularly review cash flow statements, balance sheets, and profit-and-loss statements to stay on top of your net income and debt management capacity [14][5].

Automated systems can sync sales data with your financing platform, ensuring repayments are triggered by actual sales events [11][13]. This reduces the risk of over-leveraging. Periodic reviews of your debt positions are also essential to avoid borrowing beyond what your business can handle [8].

For added flexibility, consider a revolving line of credit. This allows you to borrow, repay, and borrow again up to a set limit, which is especially useful for seasonal businesses [1][14]. Regularly audit inventory and facilities to maintain accurate collateral values [1]. If needed, combine different funding types to balance immediate cash flow needs with long-term goals [1].

Conclusion

Securing inventory funding without straining your cash flow begins with understanding where your money is tied up. Start by analyzing your cash conversion cycle - pinpoint the gaps between when you pay suppliers and when you collect from customers. Streamlining operations, improving demand forecasting, prioritizing high-margin products, and boosting sell-through rates can all reduce the amount of funding you’ll need. These steps lay the groundwork for a funding strategy that works in harmony with your business operations.

When it comes to choosing financing, it’s essential to pick a solution that aligns with your sales cycle. Revenue-based funding, for example, adjusts to your sales performance - higher payments during strong months and lower payments when sales slow down. As Onramp Funds explains:

"We evaluate your sales history, cash flow needs, and debt positions to make you an offer that fits with your cash flow capability. We structure your financing to ensure you're not putting your business at risk with too much debt." [8]

Businesses that partner with Onramp Funds experience an average revenue growth of 73% within 180 days of receiving funding [8].

The key is to develop a funding plan tailored to your specific operational needs, ensuring repayments align with your cash flow and can adapt as your business grows. The right funding strategy creates a self-reinforcing growth cycle, strengthening your business over time. By integrating funding decisions with operational insights, you build a solid foundation for sustainable eCommerce growth.

FAQs

What are the best ways to speed up my cash conversion cycle?

To make your cash conversion cycle faster, focus on strategies that free up cash and boost efficiency. Inventory financing is a smart way to unlock funds tied up in your stock, giving you quicker access to capital. You could also negotiate longer payment terms with suppliers, which provides more flexibility to manage your cash flow. Another option is revenue-based financing, where repayments adjust based on your sales, making it a more adaptable solution. On top of that, improving your inventory forecasting can prevent overstocking and reduce the time products linger in your warehouse. These approaches can help you keep your cash flow steady while supporting business growth.

What are the advantages and disadvantages of using revenue-based funding for inventory?

Revenue-based funding provides fast access to capital, often within just 24–48 hours, making it a great option for quickly restocking inventory ahead of a busy sales season. What makes it stand out is that payments are based on a fixed percentage of your monthly revenue, which means they scale with your sales. If you hit a slow month, your payments decrease accordingly. Plus, there’s no need for collateral or personal guarantees, and you retain full ownership of your business. Another bonus? The total repayment cost is capped, offering a clear and predictable repayment structure.

That said, there are some downsides to consider. The effective APR can be higher than what you’d find with traditional loans. For businesses with unpredictable revenue or slim profit margins, this can be a challenge, as repayments might take a big bite out of earnings. On top of that, the repayment period isn’t fixed - it depends on how quickly your sales grow. Slower revenue could stretch out the repayment timeline. Before diving in, take a close look at your cash flow and growth plans to decide if this funding model aligns with your inventory needs.

How can I figure out how much funding I need for my inventory?

To figure out how much funding you'll need for inventory, start by reviewing your recent sales data - ideally from the past 3 to 6 months. Look for trends, seasonal peaks, or growth patterns to help estimate the number of units required to meet demand. Once you have that estimate, multiply it by your supplier’s unit price. Don’t forget to include a safety buffer of 5–10% to cover unexpected demand or potential delays.

After calculating the total inventory cost, deduct any available cash, supplier credit, or existing credit lines. The remaining balance is the funding you'll need. Here's an example: if your projected inventory cost is $30,000, you add a 7% safety buffer ($2,100), and you already have $8,000 in cash and $4,000 in supplier credit, your funding gap would be $30,000 + $2,100 – ($8,000 + $4,000) = $20,100.

Before moving forward, make sure the funding amount aligns with your business's ability to repay. Revenue-based funding is a good option if your business generates at least $10,000 in monthly sales with gross margins of 30% or more. This type of funding adjusts repayments based on your cash flow, helping you secure inventory without putting excessive strain on your finances.