Want to grow your business without giving up equity? Non-dilutive funding is the answer. It gives you the cash you need for inventory, marketing, or scaling without sacrificing ownership. Options like revenue-based financing (RBF), lines of credit, and trade credit offer flexible repayment terms aligned with your sales or cash flow.

Here’s what you need to know:

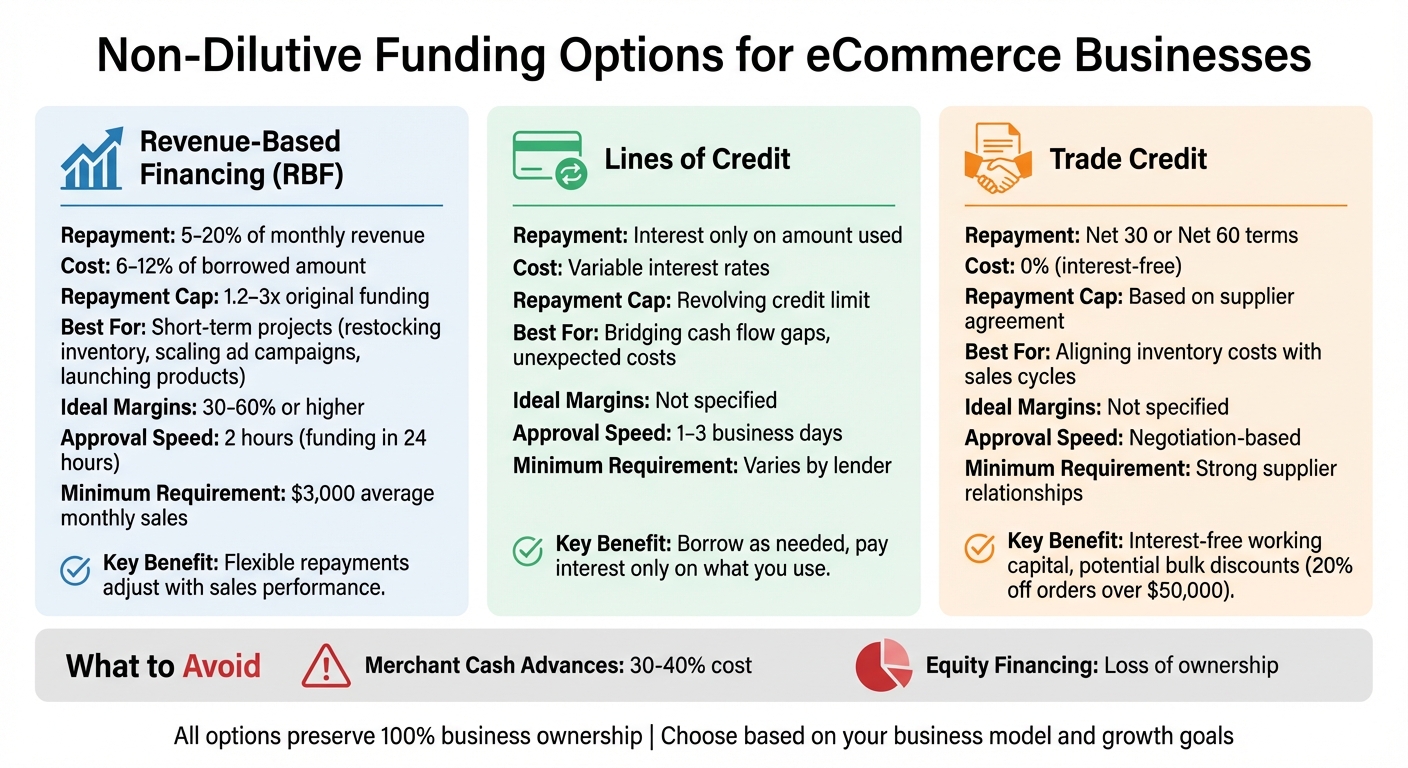

- Revenue-Based Financing (RBF): Get funds upfront and repay as a percentage of future revenue. Ideal for short-term projects like restocking inventory or scaling ad campaigns.

- Lines of Credit: Borrow as needed and only pay interest on what you use. Great for bridging cash flow gaps or handling unexpected costs.

- Trade Credit: Negotiate payment terms with suppliers (e.g., Net 30 or Net 60) to align inventory costs with sales cycles.

Why it works: Non-dilutive funding focuses on sales performance, not collateral or credit scores. This means faster approvals, flexible repayments, and no loss of control over your business. For example, brands like Hedoine and SPOKE used RBF to fuel growth, achieving impressive sales results without giving up equity.

Key tip: Before applying, map out your cash conversion cycle, set clear growth goals, and ensure your gross margins can handle repayment terms. Choose the funding option that aligns best with your business model and growth plans.

Keep reading for actionable tips on how to secure funding, improve cash flow, and pick the right strategy for your eCommerce business.

Non-Dilutive Funding Options for eCommerce: RBF vs Lines of Credit vs Trade Credit

Non Dilutive Financing Funding Growth Without Losing Ownership

Identify Your Growth and Funding Needs

Before applying for funding, it’s important to figure out exactly how much money you need and how you’ll use it. Instead of estimating, take the time to map out your specific growth drivers and analyze your cash flow patterns. This groundwork helps you set clear growth objectives and determine precise capital requirements.

Set Your Growth Goals and Capital Requirements

Start by pinpointing the activities that will drive revenue. Whether it’s restocking inventory, launching a new product line, or ramping up advertising, each initiative will require a different amount of capital [7].

Your business model also plays a big role in shaping your funding needs. For instance, B2B sellers often require upfront capital for bulk inventory purchases and warehousing. On the other hand, direct-to-consumer brands typically prioritize spending on marketing, website optimization, and automating fulfillment processes [4]. Advanced funding platforms can streamline this process by integrating with platforms like Shopify, Amazon, or Walmart to analyze real-time sales data and provide performance-based funding offers [7].

It’s equally important to ensure that repayment terms align with your profit margins. For businesses with gross margins below 30%, high-cost flexible funding could put unnecessary strain on operating profits. Ideally, gross margins of 60% or higher allow you to comfortably handle revenue-based financing payments [8].

Map Your Cash Conversion Cycle

The cash conversion cycle, or the time between paying your suppliers and receiving payouts from marketplaces, is a critical period where liquidity challenges can arise. Track each stage of this cycle, including inventory procurement, warehousing, fulfillment, shipping, and advertising expenses [4][9].

Seasonal fluctuations can make this even trickier. For example, preparing for the holiday season often requires significant upfront capital long before sales roll in. Monitoring supplier payment schedules and inventory turnover rates can help you identify potential cash flow bottlenecks [4][9].

Calculate How Much Capital You Need

After mapping out your cash cycle, you can calculate the funding amount you’ll need. A simple method is to multiply your monthly revenue by the remit rate. For instance, if your monthly revenue is $50,000 and the remit rate is 5%, your repayment would be $2,500. Borrowing $20,000 with a 1.5× repayment cap would mean a total repayment of $30,000 [10].

Tracking key metrics such as Monthly Recurring Revenue (MRR), Annual Recurring Revenue (ARR), and Net Dollar Retention can also demonstrate consistent performance to potential lenders. Many revenue-based financing providers require at least $30,000 in MRR to approve funding [8].

For short-term needs, aim for funding that covers 2–4 months of revenue [8]. This strategy keeps repayments manageable while giving you enough resources to generate returns. With a clear understanding of your capital needs, you can now explore financing options that preserve your equity.

Use Revenue-Based Financing to Scale Without Giving Up Equity

How Revenue-Based Financing Works

Revenue-based financing (RBF) offers upfront funding in exchange for a percentage of your future gross revenue [7][11]. Typically, you’ll repay between 5% and 20% of your monthly revenue until you reach a predetermined cap - usually 1.2 to 3 times the original funding amount. What makes this model flexible is that repayments adjust automatically based on your sales: higher payments during strong months and lower ones when sales dip [8][12].

Unlike traditional bank loans, RBF focuses on your sales performance instead of relying on credit scores or collateral. Providers use secure API integrations to connect directly with platforms like Shopify, Amazon, or Walmart Marketplace, enabling fast, data-driven underwriting without the hassle of lengthy approval processes. A key benefit? You retain full ownership and control of your business. Once the capped repayment amount is met, the agreement ends - there are no ongoing dividends, board seats, or external interference [12].

This financing method allows you to scale while keeping control, making it an appealing option for many businesses.

When to Use Revenue-Based Financing

RBF works best for short-term projects with high potential returns. Common scenarios include restocking inventory ahead of busy seasons, scaling effective ad campaigns, or launching new products. For instance, Dock & Bay uses RBF to manage cash flow when purchasing inventory before peak sales periods [13].

Your gross margins are a critical factor in deciding if RBF is the right fit. Ideally, margins should fall between 30% and 60% (or higher) to ensure that the repayment percentage doesn’t strain your operations [8][12]. It’s important to model how the revenue share will affect your cash flow, making sure you can cover essential costs like goods sold and operational expenses.

A real-world example? In 2022, SPOKE, an apparel brand, used RBF to boost its marketing budget, successfully acquiring around 30,000 new customers [13]. This shows how well-placed RBF investments can lead to measurable growth.

If RBF aligns with your business goals, here’s how to secure funding.

How to Get Revenue-Based Financing

The RBF application process is fast and straightforward. To qualify, you’ll need to be a U.S.-based legal entity (LLC, C-Corp, or S-Corp) with at least $3,000 in average monthly sales. You’ll also need to connect your sales channels to give providers a complete view of your revenue. A thorough data profile can help maximize your funding offer.

Since approval is based on actual sales performance, many RBF providers can deliver cash offers in as little as two hours, with funding available within 24 hours. Make sure all revenue streams are included in the repayment calculations for accuracy.

Timing is key. Apply when you need funds for high-return activities, like purchasing inventory, expanding advertising, or launching new products. And because RBF depends on accurate data, keeping your eCommerce analytics updated is essential. Once approved, put the capital to work immediately to generate measurable results.

Other Non-Dilutive Funding Options for eCommerce

When it comes to growing your eCommerce business, revenue-based financing isn't the only way to secure funds without giving up equity. There are several other non-dilutive funding methods that can help you manage predictable expenses, bridge short-term cash gaps, or align inventory costs with sales cycles. Each option serves different needs, so understanding them can help you make smarter financial decisions.

Term Loans and Business Lines of Credit

Term loans provide a lump sum upfront, paired with fixed interest rates and a set repayment schedule. These are particularly useful for larger, long-term investments like purchasing equipment or placing bulk inventory orders [3][4]. The predictability of fixed monthly payments makes budgeting easier for these types of expenses [3].

On the other hand, business lines of credit offer more flexibility. You can borrow funds as needed and only pay interest on the amount you’ve drawn [3]. This makes them a great choice for covering short-term cash flow gaps or handling unexpected costs without committing to large, fixed payments [3][2][14].

Since traditional banks often require collateral, many online businesses turn to alternative lenders. These lenders assess risk differently, using metrics like monthly revenue and sales volume to approve funding quickly - sometimes within one to three business days [5][16]. As Onramp Funds points out:

Banks can't usually lend to online businesses because they aren't equipped to assess the risk accurately, measure business performance, and typically want collateral [5].

This approach allows eCommerce sellers to meet their financial needs while retaining full ownership of their business.

Marketplace and Platform-Based Funding

Major eCommerce platforms like Amazon, Walmart, and Shopify have stepped into the funding space, offering programs directly tied to your sales performance. These funding options often work as merchant cash advances or revenue-based models, where repayment happens automatically as a percentage of your daily or weekly sales [3][14].

Eligibility for these programs is often determined automatically, using internal sales data from the platform. Many platforms even extend offers without requiring an application [16]. Repayments are seamlessly deducted during settlement periods, so the process doesn’t disrupt your cash flow [14]. For sellers operating across multiple channels, integrating all platforms with a third-party provider can increase the total funding available [16].

This type of funding is particularly appealing because it aligns repayment with your revenue, keeping your financial obligations manageable while you maintain full control of your business.

Trade Credit and Supplier Payment Terms

Trade credit is an often-overlooked funding option that comes directly from supplier agreements. When suppliers offer payment terms like Net 30 or Net 60, they’re essentially providing you with interest-free working capital [4][1]. This means you can purchase inventory, sell it, and use the revenue to pay the supplier - without needing to pay upfront.

This approach is especially helpful in addressing a common eCommerce challenge: manufacturers often require payment well before you start earning revenue from the products. By negotiating favorable terms, you can better align your inventory costs with your sales cycle, freeing up cash for other needs. Paul Voge, Co-founder and CEO of Aura Bora, highlights the benefits:

Access to higher limits and extended payment terms enables us to keep up with inventory without straining our working capital [15].

Additionally, strong supplier relationships can lead to perks like bulk discounts - such as 20% off orders over $50,000 - which directly improve profit margins and reduce the overall need for external funding [15]. As one strategic insight points out:

Having ready capital also strengthens your negotiating position with suppliers. When you can pay upfront or on shorter terms, vendors often provide better pricing or priority fulfillment [15].

Trade credit can also act as an internal safety net, helping you navigate supply chain disruptions without resorting to external loans. It’s a practical and cost-effective way to manage working capital while keeping full ownership of your business.

sbb-itb-d7b5115

Improve Cash Flow and Reduce Funding Needs

Keeping your cash flow in good shape is crucial for growing your business without giving up equity. By fine-tuning your current cash flow, you can lower your borrowing needs and cut down on fees. Essentially, it’s about making the most of the money you already have. A big part of this is managing your inventory effectively to ensure your cash is being used wisely.

Manage Inventory and Purchasing Better

For eCommerce businesses, inventory often ties up more working capital than anything else - especially if you’re buying in bulk or storing products in warehouses [4]. By leveraging real-time sales data, you can align inventory orders with actual demand. This frees up cash that can be reinvested elsewhere in your business.

Flexible financing can also help you take advantage of bulk order discounts without putting a strain on your cash reserves. This not only improves your per-unit costs but also keeps your operations running smoothly [4]. As Onramp Funds puts it:

Having flexible working capital allows online sellers to optimize inventory management, streamline operations, and deliver a seamless customer experience - essential elements for long-term success [4].

This strategy ensures you’re not overextending during slower periods while still having enough stock to meet demand during busy seasons. Additionally, coordinating payment schedules can further improve how you manage cash flow.

Coordinate Payment Timelines

When your supplier bills or ad costs are due before you receive payments from customers, it can create a cash flow bottleneck. The fix? Align your outgoing payments with your incoming cash.

Revenue-based financing simplifies this by syncing repayments with your sales deposits. Eric Youngstrom, Founder and CEO of Onramp, explains:

Your repayments synchronize with your sales deposits, so we only get repaid when you sell products. If sales speed up, you'll pay back faster; if they slow down, you'll pay back more slowly [18].

This repayment flexibility helps avoid cash flow issues, especially during slower sales periods. If platforms hold funds in reserve, you can also time your repayments to match when those funds are released [18].

Track Profitability and Unit Economics

To scale your business effectively, you need to keep a close eye on profitability metrics. Monitoring unit economics - like contribution margin per product and return on ad spend (ROAS) - can help you determine if your growth is actually profitable [4][17]. Regularly review daily sales, inventory costs, and marketing expenses to catch and address any issues early.

One key metric to watch is your Cash Conversion Cycle (CCC), which measures how long it takes to turn inventory into cash from sales [18]. A shorter cycle means you’ll rely less on external funding. To improve your CCC, focus on speeding up fulfillment, negotiating better terms with suppliers, and reducing the time between purchasing inventory and receiving customer payments.

Pick the Right Funding Strategy for Your Business

Choosing the right funding strategy is not a one-time decision - it’s a process that evolves as your business grows. The goal is to align your funding sources with how your business operates and what you aim to achieve. Nearly 90% of eCommerce companies fail within their first 120 days, with running out of cash being one of the top five reasons for failure [13]. To avoid this, it’s essential to develop a funding strategy that supports growth while maintaining control. The key is to match your funding options to your business model, ensuring flexibility and adaptability.

Match Funding Options to Your Business Model

Your funding approach should reflect the specific needs of your business model. For example, B2B companies often require upfront capital to manage bulk inventory and logistics. On the other hand, D2C and B2C brands may benefit from more agile funding options, like revenue-based financing, which can provide funds within 48 to 72 hours [4][13].

For short-term needs - such as restocking inventory or launching a marketing campaign - options like revenue-based financing or a line of credit are typically the most practical. However, if your focus is on long-term initiatives, like research and development or entering new markets, you’ll need to explore other funding solutions [13].

Revenue-based financing is particularly useful for businesses with seasonal or fluctuating sales. Since repayments are tied to a fixed percentage of daily sales, you pay less during slower periods and more when sales are strong [13]. This repayment model helps stabilize cash flow while allowing you to retain full ownership of your business.

Review Your Funding Strategy Regularly

As your business evolves and market conditions shift, your funding strategy should adapt as well. Make it a habit to review your funding approach and key performance metrics every quarter. Metrics such as cash conversion cycle, profit margins, return on ad spend, and cash flow are critical for ensuring your funding strategy aligns with your growth goals.

Regular reviews allow you to identify and address issues early. For instance, if your sales are growing faster than expected, you may need to secure additional funding. Conversely, if profit margins are shrinking, focusing on cash flow optimization could take priority over seeking external capital. The ultimate aim is to build a repeatable funding process that supports your growth without adding unnecessary pressure or requiring you to give up equity.

Conclusion

Expand your eCommerce business while keeping full control of your equity. Non-dilutive funding options - like revenue-based financing, lines of credit, and trade credit - offer a way to grow inventory, launch marketing campaigns, and enter new markets without giving up ownership. These alternatives are designed to fit the unique needs of eCommerce businesses, unlike traditional bank loans [5][3].

Choose the funding option that best suits your goals. Revenue-based financing provides flexibility, with repayment costs typically ranging from 6% to 12% of the borrowed amount [6]. Lines of credit are ideal for bridging short-term cash flow gaps [5][6]. Steer clear of merchant cash advances, which can carry steep costs of 30%–40% [6], and reserve equity financing for situations where strategic expertise is crucial [3].

Timing is everything. Align your funding decisions with your operational cycles for maximum efficiency. Use your cash conversion cycle to determine when funding is most needed [1]. Modern lenders often focus on real-time sales data, so connect platforms like Shopify, Amazon, Stripe, or TikTok Shop to simplify the application process [6]. Finally, monitor your unit economics to ensure your margins can handle fees and repayments without disrupting cash flow.

FAQs

What makes revenue-based financing a better option than traditional loans for eCommerce businesses?

Revenue-based financing (RBF) gives eCommerce businesses a faster and more flexible way to secure funding compared to traditional loans. Instead of locking you into fixed monthly payments, RBF ties repayment to a percentage of your monthly sales. This means payments go up during high-revenue months and drop when sales slow - perfect for businesses dealing with seasonal ups and downs.

What sets RBF apart is its simplicity. There’s no need for collateral or a credit check, and you can often get funds within 24 hours. Instead of dealing with ongoing interest, RBF uses a flat fee (usually 2%–8% of the funding amount), making it easier to plan your expenses. Plus, you keep 100% ownership of your business, avoiding the equity loss or personal guarantees that come with other funding methods.

For eCommerce brands looking for quick funding that doesn’t disrupt cash flow or ownership, RBF is a smart and practical choice.

How do I figure out the right amount of non-dilutive funding for my eCommerce business?

To figure out the right amount of non-dilutive funding, start by evaluating your monthly revenue and pinpointing the growth initiatives you want to tackle. These could include things like buying more inventory, boosting ad spend, or upgrading your tech stack. Once you've identified these needs, calculate the costs and add a 10–20% buffer to cover any unexpected expenses.

Next, consider how much you can afford to repay. Non-dilutive funding, such as revenue-based financing, usually involves repaying a fixed percentage of your monthly revenue (typically 2–8%). It's a good idea to model repayment scenarios for both your high and low sales periods to ensure the payments fit comfortably into your cash flow. A practical guideline is to keep annual repayments under 20–30% of your projected revenue, which often means borrowing no more than 3–6 months' worth of average sales.

Finally, make sure the funding aligns with your growth plans. For instance, if you're planning a $50,000 inventory purchase that’s expected to increase your monthly sales by $15,000 within three months, confirm that this projected revenue can handle the repayments while still leaving room for profit. This way, you can grow your business without compromising ownership or financial stability.

What should I consider when selecting a non-dilutive funding option for my eCommerce business?

When selecting a non-dilutive funding option, the first step is to evaluate your business stage and revenue levels. For instance, revenue-based financing (RBF) is typically a good fit for businesses generating steady monthly sales between $10,000 and $20,000 and with at least 6–12 months of operating history. This makes it a strong option for businesses experiencing growth and maintaining consistent cash flow. On the other hand, traditional bank loans or lines of credit often have lower revenue requirements, ranging from $3,000 to $8,000 per month, but they usually demand strong credit scores or collateral. If your business faces seasonal fluctuations, RBF’s flexible repayment model - where payments adjust based on your revenue - can be a lifesaver, as opposed to fixed-payment loans that may cause financial strain during slower months.

You’ll also want to weigh the cost, speed, and purpose of the funding. RBF generally comes with a flat fee of 2%–8% of the funded amount and can deliver capital in as little as 1–3 days without requiring you to give up ownership. In contrast, bank loans often have lower interest rates, typically between 6% and 15% APR, but the approval process can take weeks. For quicker access to cash, merchant cash advances are an option, though they tend to come with higher costs and daily repayments tied to your card sales. Ultimately, it’s crucial to ensure the funding aligns with your specific needs - whether it’s for inventory, marketing, or working capital - and that the repayment terms support your growth without putting undue pressure on your cash flow.