Starting an eCommerce business? Funding is often essential to manage cash flow, especially when you need to pay suppliers before generating revenue. Here’s what you need to know:

- Cash Flow Challenges: 82% of small businesses fail due to cash flow issues, and 29% run out of cash entirely. Funding can help bridge revenue gaps.

- Choosing the Right Option: Fixed loans suit stable businesses, but revenue-based financing adjusts to sales, offering flexibility for seasonal operations.

- Eligibility Basics: Lenders typically require $3,000 monthly revenue and access to sales data from platforms like Shopify or Amazon.

- Purpose of Funding: Use short-term loans for inventory or marketing with quick returns. Avoid expensive advances for long-term needs.

- Repayment Terms: Match repayment schedules to your revenue patterns. Revenue-based financing ties payments to sales, making it easier during slow periods.

- Avoid Common Mistakes: Don’t overborrow, underestimate costs, or choose rigid loans that don’t align with your cash flow cycles.

Smart funding choices can help you grow without financial strain. Always calculate total borrowing costs, including fees, and align funding with your revenue cycle for sustainable growth.

eCommerce Funding Secrets Every Seller Should Know

sbb-itb-d7b5115

Is Your Business Ready for Funding?

Before diving into funding applications, make sure your eCommerce business meets the necessary qualifications. This step is crucial, especially given the cash flow challenges often faced in this industry.

Basic Requirements for Approval

To qualify for most eCommerce funding, your business typically needs to generate at least $3,000 in monthly revenue [4]. Lenders evaluate your sales history, including digital data, conversion rates, and seasonal trends, to gauge risk and determine how much funding to offer [5].

Approval usually involves granting lenders read-only API access to platforms like Shopify, Amazon, Walmart, or TikTok Shop. This allows them to review your real-time performance and aggregate data across multiple sales channels [4][1][9].

In addition to revenue, lenders assess your inventory turnover and stockout history. Frequent stockouts can lead to lost sales and hurt your search rankings on platforms like Amazon [3]. Efficient inventory management not only boosts your chances of approval but also signals operational reliability, which could justify your need for working capital.

Once you've confirmed eligibility, the next step is to clearly define how you plan to use the funding.

Identifying Your Funding Needs

Having a clear purpose for your funding is essential. Different goals require different financing strategies. For example:

- If you're restocking inventory with a turnover cycle of 60–120 days, short-term capital is a good fit.

- Planning an advertising campaign? Consider your Customer Acquisition Cost (CAC) compared to the Lifetime Value (LTV) of your customers. For instance, if acquiring a customer costs $30 and they generate $100 in LTV, funding your marketing efforts could be a smart move [5].

Another key factor is your cash conversion cycle - the time it takes to turn investments in inventory into cash. If your cycle is lengthy, bridging capital might be necessary [5]. Experts also suggest keeping at least two months of operating expenses in reserve to handle unexpected challenges [4].

Be specific about your funding objectives. Whether it's restocking popular products ahead of peak seasons, launching a new product line, or covering payroll during slow periods, aligning your funding needs with your revenue cycle ensures you choose the right financing solution.

Understanding Revenue-Based Financing

Fixed Fee vs Revenue-Based Financing Comparison for eCommerce Businesses

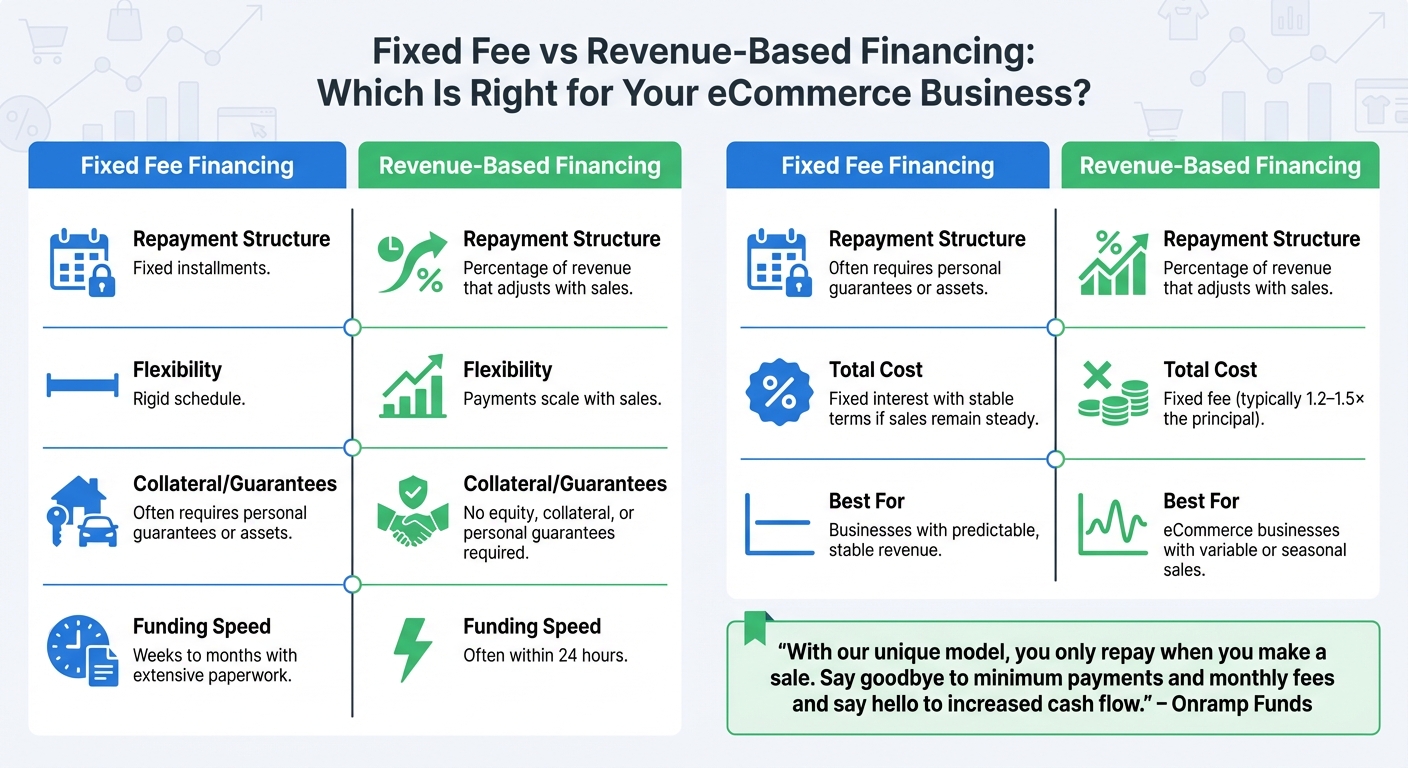

Once you've identified your funding needs, revenue-based financing (RBF) could be an option worth considering - especially if your business experiences seasonal sales or fluctuating growth. RBF provides capital without requiring you to give up ownership or take on a traditional loan. Instead, you repay a percentage of your revenue - typically between 5% and 25% - until the principal and a fee are fully repaid. This repayment structure adjusts automatically based on your sales performance, making it a flexible option for businesses with unpredictable revenue streams.

Unlike conventional loans, RBF offers funding amounts ranging from $10,000 to $5,000,000, often disbursed within just 24 hours. There's no need for equity, personal guarantees, or collateral, making it an attractive choice for first-time borrowers with strong sales data but limited credit history.

How Revenue-Based Repayment Works

With RBF, repayments are directly tied to your sales. Instead of fixed monthly payments, you remit a percentage of your revenue, ensuring payments decrease during slow periods and increase when sales pick up. Payments are handled automatically through read-only API access, which securely tracks your revenue. To prevent overextending your cash flow, most agreements cap repayments at around 30% of your revenue. Repayment terms typically range from 3 to 15 months, depending on the agreement.

"With our unique model, you only repay when you make a sale. Say goodbye to minimum payments and monthly fees and say hello to increased cash flow." – Onramp Funds [4]

This structure provides more flexibility compared to fixed-fee financing, as outlined below.

Fixed Fee vs. Revenue-Based Financing

Choosing between fixed-fee and revenue-based financing depends on your business's cash flow patterns and growth stage. Here's a comparison to help you decide:

| Aspect | Fixed Fee Financing | Revenue-Based Financing |

|---|---|---|

| Repayment Structure | Fixed installments | Percentage of revenue that adjusts with sales |

| Flexibility | Rigid schedule | Payments scale with sales |

| Collateral/Guarantees | Often requires personal guarantees or assets | No equity, collateral, or personal guarantees required |

| Funding Speed | Weeks to months with extensive paperwork | Often within 24 hours |

| Total Cost | Fixed interest with stable terms if sales remain steady | Fixed fee (typically 1.2–1.5× the principal) |

| Best For | Businesses with predictable, stable revenue | eCommerce businesses with variable or seasonal sales |

Fixed-fee financing works well for businesses with steady revenue and predictable expenses. On the other hand, if you're an eCommerce seller with seasonal sales spikes, RBF can help you maintain cash flow during slower months while allowing you to seize opportunities during peak seasons.

Understanding Repayment Terms and Cash Flow

When planning your funding strategy, it's crucial to grasp how repayment terms impact your cash flow. Before committing to any funding agreement, take time to evaluate how repayments might affect your daily operations. For many eCommerce businesses, quarterly sales cycles are the norm. This can make traditional repayment schedules, like 30-day credit card cycles or fixed monthly bank payments, tough to handle during slower sales periods [4]. A poorly structured repayment plan could drain your cash reserves just when you need them most. To avoid this, align your repayment schedule with your actual revenue patterns. Fixed payments, for example, can become a burden during low-revenue months. Tools like funding calculators can help you accurately project your repayment obligations under different sales scenarios.

How to Use Funding Calculators

Funding calculators are a handy tool for modeling repayment scenarios before taking on debt. To get a complete picture of your obligations, include all associated costs - such as origination fees (usually between 2% and 5% of the loan amount), maintenance charges, and any hidden fees [10]. If you're considering revenue-based financing, try modeling a situation where your sales drop by 20% to 30% during historically slower periods. This allows you to check if your operating expenses can still be covered. Running worst-case scenarios is an effective way to avoid overextending your finances.

For financing options that use factor rates - common in merchant cash advances - convert these rates into an annualized cost to make accurate comparisons. For instance, a factor rate of 1.10 means you'll repay 110% of the amount borrowed, which could translate into a much higher effective cost over a shorter repayment period [21,22].

Avoiding Overborrowing and Hidden Fees

Matching repayment schedules to your revenue is just one part of the equation. Careful budgeting is equally important to avoid overextending yourself financially. Overborrowing can create unnecessary repayment pressures, straining your finances and potentially impacting your ability to secure future loans [11]. Before applying for funding, draft a detailed budget that accounts for your specific needs - whether it's inventory, marketing, or equipment. Borrow only what you need, adding a modest buffer (about 10% to 15%) to cover unexpected expenses [11].

Be cautious of additional fees that can inflate the actual cost of borrowing. Beyond the interest rate, lenders may charge origination fees, annual maintenance fees, service charges, or even prepayment penalties [23,24]. Always request a detailed breakdown of all costs before signing any agreement.

Another common mistake is taking on additional funding while still repaying an existing balance. Overlapping repayment obligations can quickly overwhelm your cash flow, making it difficult to stay afloat [8].

Lastly, ensure the cost of borrowing is less than the profit it helps generate. For businesses with tight margins, it's essential to compare financing costs with the returns you expect to make. This careful analysis will help protect your cash flow and keep your business in a strong position [5,6].

Common Mistakes First-Time Borrowers Make

First-time borrowers often face challenges when choosing funding, and these mistakes can take a heavy toll on cash flow. One major issue is opting for rigid financing that doesn’t align with seasonal revenue patterns. For instance, traditional bank loans often require fixed monthly payments, regardless of whether sales fluctuate throughout the year. Similarly, credit cards demand repayment within 30 days, which can be problematic for eCommerce businesses operating on quarterly sales cycles [3]. When revenue dips but payments stay the same, businesses may struggle to meet obligations, leaving little room for growth. This mismatch can lead to deeper issues, such as inflexible repayment plans and poorly allocated capital.

Another common pitfall is failing to match funding to specific business needs. Many borrowers mistakenly apply a one-size-fits-all approach, using long-term loans for short-term expenses like inventory. This can create unnecessary financial strain and increase personal liability [1][3]. With cash flow challenges being a leading cause of business closures, aligning funding with operational needs is critical.

First-time borrowers also tend to underestimate the true cost of borrowing. While a low-interest rate might look appealing, additional charges like origination fees, factor rates, and prepayment penalties can significantly raise the effective APR [12][5]. To avoid surprises, it’s important to calculate the total borrowing cost, including all fees, rather than relying solely on the advertised rate.

The Problem with Rigid Loan Terms

Traditional bank loans can be especially tough for eCommerce businesses due to their lack of flexibility. The approval process alone can take months and requires extensive documentation [3]. Once approved, borrowers are locked into fixed monthly payments that don’t adjust to slower sales periods. This makes it hard to manage fluctuating revenue streams. Additionally, many traditional lenders demand collateral or personal guarantees and may include hidden fees, such as processing charges and early repayment penalties [13]. These rigid terms often clash with the unpredictable nature of eCommerce supply chains, creating a risk of falling into a debt trap when payments are due before inventory is sold.

Matching Funding to Your Growth Stage

Choosing the right funding starts with understanding your business cycle and goals. A company in the early stages of product validation will need a different type of funding than one scaling marketing efforts or expanding into new markets. Securing funding too early can mean locking in unfavorable terms before achieving product-market fit, while waiting too long might result in missed opportunities [14].

A great example of aligning funding with business needs comes from the fashion brand Hedoine. In 2019, they secured $50,000 in revenue-based funding to boost Instagram and Facebook marketing campaigns. This decision led to a staggering 1,106% increase in sales during the first quarter of 2020 [7].

Your funding choice should reflect your specific needs. For seasonal inventory, inventory financing can provide liquidity during peak periods. Revenue-based financing offers flexible repayments that adjust with sales, while invoice factoring can unlock cash tied up in unpaid invoices for businesses operating on Net 30 or Net 60 terms [5][6]. Avoid giving up equity too early for routine working capital, as this can lead to unnecessary dilution and loss of control [3][2].

Before applying for funding, take a close look at your unit economics. Metrics like Customer Acquisition Cost (CAC), Lifetime Value (LTV), and Gross Margin can help ensure you’re borrowing for growth that makes financial sense [15][16]. Aligning financing with your cash flow and growth stage is key to building a sustainable business.

Conclusion

Align your funding choices with your business needs: use revenue-based financing for things like inventory or marketing campaigns, and reserve long-term loans for acquiring permanent assets.

Here’s a critical insight: 82% of small businesses fail due to cash flow problems [3]. This highlights why having repayment terms that adjust to your revenue is crucial for eCommerce sellers, especially during slower seasons when sales might dip.

Be thorough when calculating your total borrowing costs. Include every fee - origination fees, platform fees, and revenue share percentages - so you know exactly what you’ll owe [6]. It’s also wise to maintain a two-month cash reserve to handle unexpected issues like supply chain delays or sudden market shifts [4].

Smart funding choices can fuel growth without overburdening your finances. Pay close attention to your unit economics - your gross margins should be strong enough to cover borrowing costs comfortably. If the cost of financing eats into your profits, it could harm your business [6].

Take the time to weigh your options and choose financing that grows alongside your sales. This approach helps you avoid common pitfalls and sets the stage for steady, sustainable growth.

FAQs

What are the advantages of using revenue-based financing for your eCommerce business?

Revenue-based financing gives eCommerce businesses the advantage of repayment terms that align with your sales performance. You pay more only when your business earns more, offering a repayment structure that adjusts to your revenue flow. Plus, it allows you to maintain complete ownership of your business without sacrificing equity.

This funding option also provides quick access to capital without the need for personal guarantees or a perfect credit score. It's a straightforward and flexible solution designed to support entrepreneurs as they scale their businesses.

What do I need to qualify for funding for my eCommerce business?

If you're aiming to secure funding for your eCommerce business, the first step is to take a close look at your financial health. Start by examining your sales trends, cash flow, and any outstanding debts. Lenders typically want to see that your business is in a stable position. Many will require consistent monthly sales - often a minimum of $3,000 - and may also evaluate whether your business is compatible with specific eCommerce platforms.

It's also essential to check your credit score, as this could play a key role in the lender's decision. Beyond that, be ready to meet any additional requirements they might have. Keeping detailed and accurate financial records is another way to strengthen your case. Lastly, presenting a clear plan that outlines how you intend to use the funding to achieve your business goals can make a big difference in improving your chances of approval.

What mistakes should first-time eCommerce business borrowers avoid?

First-time borrowers should be mindful of borrowing only what their business genuinely requires, as taking on more debt than necessary can put undue pressure on finances. Carefully assess your cash flow to make sure you can handle repayments without disrupting your day-to-day operations.

Equally important is a thorough review of the terms and conditions tied to your funding. Pay close attention to interest rates, fees, and repayment schedules. Overlooking these details can result in unexpected expenses or complications later.

Lastly, don’t rush the process. Take the time to ensure the funding aligns with your business goals and supports steady, sustainable growth for your eCommerce venture.