Revenue-based financing (RBF) is a flexible funding option that adjusts repayment based on how much your business earns each month. Unlike fixed-payment loans, RBF allows early-stage eCommerce brands to manage cash flow more effectively, especially during slow sales periods or seasonal fluctuations. Here's why this matters:

- Repayments scale with revenue: Pay less during slow months and more during peak months, keeping cash flow stable.

- No equity loss: RBF doesn’t require giving up ownership, unlike venture capital.

- Faster approval: Funds can be available within 24 hours, with minimal paperwork and no need for collateral.

- Tailored for eCommerce: Perfect for businesses with fluctuating revenue due to inventory cycles or seasonal sales.

RBF is growing rapidly, with the market projected to reach $42.3 billion by 2027. It’s a smart alternative for brands seeking growth without the constraints of fixed-payment loans or equity loss.

Deep Dive on Revenue Based Financing

sbb-itb-d7b5115

What Is Revenue-Based Financing?

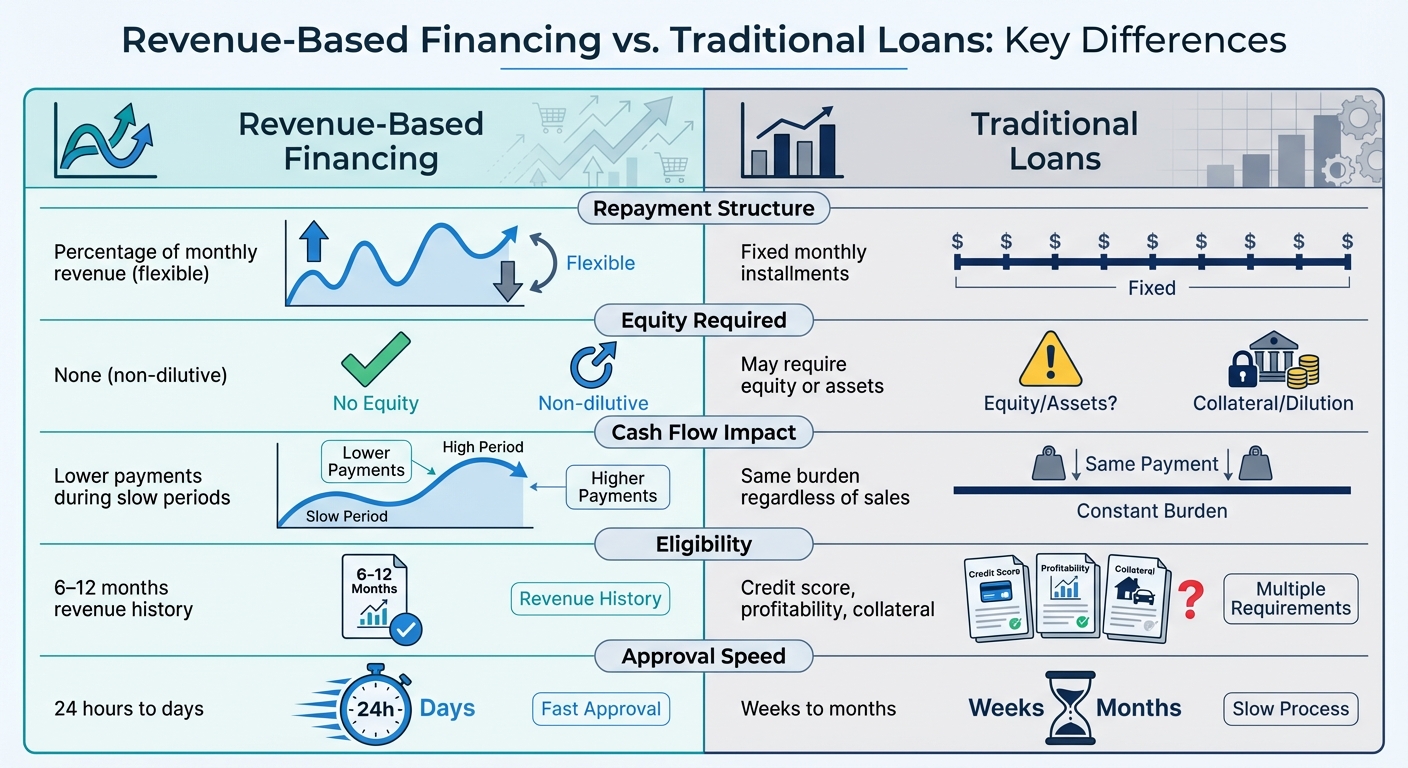

Revenue-Based Financing vs Traditional Loans Comparison

Revenue-based financing (RBF) is a funding option where businesses receive a lump sum upfront and repay it through a fixed percentage of their monthly revenue. Payments adjust based on how much the business earns - higher payments during strong months and smaller ones during slower periods.

Here’s an example: If you borrow $100,000 with a 12% fee, you’ll repay $112,000 in total. Payments are variable, typically ranging from 5% to 25% of your monthly revenue, and there’s no set repayment deadline.[1][2]

One major advantage of RBF is that it’s non-dilutive - you don’t have to give up any ownership in your business. Plus, there’s no need for collateral or personal guarantees. Instead, lenders focus on your revenue history, typically looking at the past 6 to 12 months. Once approved, funds can be delivered in as little as 24 hours after connecting your financial accounts.[2][4]

This flexibility sets RBF apart from traditional financing options, as shown below.

Revenue-Based Financing vs. Traditional Loans

The key difference between RBF and traditional loans lies in their repayment terms and approval requirements. Traditional loans, such as those from banks or the SBA, come with fixed monthly payments that remain the same regardless of your sales. For instance, if you secure a $100,000 loan with a $2,500 monthly payment, you’ll owe that amount whether your sales hit $10,000 or $100,000 in a given month. This can strain your cash flow during slower periods, leaving less money for essentials like inventory or operations.

Traditional lenders also require strong credit scores, extensive paperwork, collateral, and sometimes personal guarantees. The approval process can take weeks or even months. In contrast, RBF offers a more adaptable approach. Payments adjust based on your revenue, there’s no interest rate to calculate, and approvals are based on revenue data, not credit scores, with decisions often made in days.[2][3]

| Aspect | Revenue-Based Financing | Traditional Loans |

|---|---|---|

| Repayment Structure | Percentage of monthly revenue (flexible) | Fixed monthly installments |

| Equity Required | None (non-dilutive) | May require equity or assets |

| Cash Flow Impact | Lower payments during slow periods | Same burden regardless of sales |

| Eligibility | 6–12 months revenue history | Credit score, profitability, collateral |

| Approval Speed | 24 hours to days | Weeks to months |

Why eCommerce Sellers Benefit from Revenue-Based Financing

For eCommerce businesses, RBF is especially helpful because it accounts for the unpredictable cash flow that comes with online retail. Revenue in eCommerce often fluctuates wildly - sales might soar during Black Friday, the holiday season, or a successful marketing campaign, only to dip during quieter months. On top of that, inventory cycles require upfront capital, but the revenue from those products may not arrive until weeks or months later.

RBF aligns perfectly with these challenges. When sales are slow, payments remain low. During peak seasons, higher revenue allows for larger payments. This flexibility ensures that eCommerce sellers have the operating capital they need when it matters most, without the risk of fixed payments draining their resources during slower periods.[1][2]

A great example is Hedoine, a company that used $50,000 in RBF in 2019 to fund social media campaigns. The result? A staggering 1,106% increase in sales during Q1 2020.[1][2]

Benefits of Flexible Repayment for Early-Stage Brands

Flexible repayment, a key feature of revenue-based financing, can provide early-stage eCommerce brands with solutions to some of their most pressing challenges. Whether it's navigating slow seasons, seizing growth opportunities, or retaining full ownership, this model offers tailored advantages that traditional financing often can't match.

Managing Cash Flow During Sales Slumps

One standout benefit of revenue-based financing is how repayments adjust based on your revenue. Instead of fixed monthly payments, you pay a small percentage - typically between 2% and 5% - of your monthly income[7]. If your sales drop to $20,000 in a month, your repayment might shrink to just $400 to $1,000, leaving you with more cash to cover essential expenses.

For eCommerce brands that experience seasonal slowdowns, like the post-holiday dip, this flexibility can be a lifeline. It helps ensure you can manage operating costs without the added stress of rigid repayment terms.

Reinvesting Profits During Peak Sales

During busy seasons, like Black Friday or the holidays, revenue tends to spike - and so do repayments under this model. But here's the catch: because payments scale with revenue, they remain proportional. This means you're not stuck with fixed, hefty payments that eat into your profits. Instead, you can reinvest a portion of your earnings into inventory, marketing, or other growth-focused initiatives[8].

This adaptable repayment structure also helps you avoid the financial strain often associated with traditional loans, where fixed payments can feel burdensome during high-growth periods. It ensures you have the resources to take full advantage of your most profitable months.

Retaining Ownership with Non-Dilutive Capital

Beyond the cash flow benefits, revenue-based financing offers a huge advantage when it comes to ownership. Unlike venture capital, which typically requires giving up equity and sometimes board seats, this funding model allows you to secure capital without sacrificing control[5].

This non-dilutive approach is particularly appealing to founders who want to maintain decision-making authority. In fact, about 70% of SaaS and eCommerce founders reportedly favor revenue-based financing over venture capital for this very reason[7]. It’s a funding solution that supports growth while keeping your business firmly in your hands.

How Onramp Funds Provides Revenue-Based Financing for eCommerce

For early-stage eCommerce brands, having a funding solution that adapts to fluctuating revenue is a game-changer. Onramp Funds focuses on revenue-based financing designed specifically for eCommerce sellers. By connecting directly to your sales channels, it offers capital that adjusts based on your revenue, unlike the rigid terms of traditional banks. This approach helps bridge the gap between inconsistent sales cycles and the need for timely cash flow.

Quick Access to Funds Without Losing Ownership

With Onramp Funds, you can access capital within 24 hours of approval. This speed makes it easier to restock inventory or ramp up marketing during busy seasons. Plus, the funding is equity-free, meaning you retain 100% ownership of your business.

Works with Leading eCommerce Platforms

Onramp Funds integrates with major platforms like Amazon, Shopify, BigCommerce, WooCommerce, Squarespace, Walmart Marketplace, and TikTok Shop. Once your store is connected, the platform reviews your sales history - requiring at least six months of data - to determine funding options. Repayments are automated and tied to your actual sales performance. To qualify, your business needs a minimum of $3,000 in monthly sales.

This seamless integration also comes with transparent pricing, helping you plan your repayments with confidence.

Transparent Pricing and Flexible Repayments

Onramp Funds charges a flat fee of 2%–8% of the funded amount, with no compounding interest or hidden charges. Repayments are automatically calculated as a percentage of your monthly sales - usually between 5% and 25% - and adjust based on how your business performs.

Here’s an example: if you receive $20,000 in funding with a 6% fee ($1,200), your total repayment would be $21,200. If your monthly sales are $40,000 and your repayment rate is 10%, you’d pay $4,000 that month. However, if sales drop to $15,000, your payment adjusts to $1,500, making it easier to manage during slower periods.

How to Use Flexible Repayment Models Effectively

Flexible repayment models can be a game-changer for managing cash flow and fueling growth. Here’s how to use them strategically.

Funding Inventory and Marketing During Peak Sales

Timing is everything when it comes to funding. High-demand seasons like Black Friday or the holidays are prime opportunities to leverage flexible repayment models. By securing capital within 24 hours, you can stock up on in-demand products or ramp up advertising efforts. The beauty of this approach? You’ll only need to repay 2%–5% of your daily revenue, keeping your cash flow intact[9].

Marketing also benefits from this setup. During peak demand, you can pour funds into scaling campaigns on platforms like Google Ads and Facebook without worrying about fixed monthly payments. Since repayments adjust based on your revenue, strong campaign performance allows for quicker payback, while slower results mean smaller payments. This flexibility lets you reinvest earnings into customer acquisition without giving up equity.

To make the most of this strategy, use your sales forecasts to guide repayment planning.

Planning Repayments with Sales Forecasts

Sales forecasts are your best friend when planning repayments. By analyzing trends from the last 6–12 months, such as a 30%–50% revenue increase in Q4, you can estimate repayments at 2%–5% of your monthly sales. Keeping a six-month financial buffer ensures you’re prepared for slower periods[6]. This data-driven approach helps align funding with your business cycles, so you can avoid stretching yourself too thin during off-peak times.

For even smoother management, consider automating your tracking.

Connecting Your Store for Automated Tracking

Automation makes repayment tracking effortless. By linking your eCommerce platform - like Shopify or Amazon - directly to your funding provider, you can automatically track sales data and manage repayments in real-time. This eliminates manual reporting and ensures your repayments adjust seamlessly with daily revenue. Plus, accurate sales data keeps your finances stable. To start, test the system with a smaller funding amount to ensure everything runs smoothly.

Flexible repayment models, when used effectively, can align perfectly with your revenue cycles, giving you the financial agility to grow without unnecessary risk.

Conclusion

Revenue-based financing offers early-stage eCommerce brands a way to grow while keeping cash flow manageable. By tying repayments directly to revenue, this model eases financial strain during slower months and allows for reinvestment during busier periods. When sales slow down, repayments automatically decrease, helping you maintain stability. Conversely, during peak seasons, the ability to reinvest earnings into inventory and marketing becomes a game-changer as repayments adjust to match your performance.

The global market for revenue-based financing surged from $901.41 million in 2019 to an anticipated $42.3 billion by 2027, showcasing its growing popularity and adaptability to varying revenue patterns[2].

One major advantage is its non-dilutive nature, meaning you retain full ownership of your business as it scales. Unlike traditional loans with fixed repayment schedules, revenue-based financing aligns with your business cycles, offering a more flexible and supportive approach.

For early-stage brands navigating market fluctuations, this model provides a practical solution to cash flow challenges. By automating repayment tracking and syncing payments with sales forecasts, you can secure the capital you need without losing focus on your core goals: growing your brand and delivering value to your customers.

FAQs

How is the revenue share percentage set?

The revenue share percentage is a set portion of your business's monthly revenue, usually ranging from 4% to 8%. This approach is flexible because it adjusts automatically based on how your sales are performing. If your revenue goes up, so does the repayment amount. If sales dip, the repayment decreases accordingly. This ensures that your payments stay in line with your business's cash flow.

What happens if my sales drop to $0?

If your sales hit zero, revenue-based financing provides a safety net. Since repayments are tied to a percentage of your revenue, you won’t need to make payments during times of no income. This means your repayment pauses automatically, giving you breathing room to manage cash flow without added financial pressure. It’s a practical way to help your business recover without the stress of fixed payment obligations.

Will revenue-based financing affect my cash flow forecasts?

Revenue-based financing (RBF) can be a game-changer for managing cash flow forecasts. Because repayments are tied to your sales, they naturally adjust - rising during high-revenue months and shrinking during slower periods. This flexibility makes it easier to handle cash flow, especially during seasonal dips, while reducing financial stress. Unlike traditional fixed loans, RBF aligns with your income, giving you a smoother path to plan expenses and maintain stability.